Beef Demand – The Key to Cattle Prices

Bernt Nelson

Economist

Memorial Day is first and foremost a time for Americans to honor the men and women who died serving our country. It has also become the unofficial kick-off to summer – and grilling season, stimulating demand for all types of animal proteins, including beef.

U.S. demand for beef has remained strong even as beef prices hit record highs. With economic uncertainty growing, however, how long can this strong demand continue? This Market Intel will analyze the challenges facing beef demand, what it means for farmers and ranchers, and what consumers can expect for the unofficial start of summer.

What Fuels Demand?

Demand is the amount of a product consumers will purchase over a range of prices. In terms of the market for beef, demand is consumers’ financial ability and willingness, or desire, to purchase beef over other animal proteins, such as pork, poultry, or seafood.

Strong demand usually leads to higher retail prices. In the case of beef, this means higher prices paid for wholesale, which means higher prices for fed cattle, feeder cattle, and even new calves. Cattle supplies are currently at a 74-year low, and while tight supplies have been a major factor driving up cattle and beef prices, demand is the other part of the equation. With the supply side largely fixed, U.S. demand for beef is the lynchpin holding together razor thin profit margins for our nation’s cattle farmers and ranchers. If demand weakens, cattle prices will likely decline, creating a major obstacle to any meaningful expansion of the U.S. cattle herd.

How is Demand Measured?

Measuring demand can be tricky, but there are some tools that can help. USDA has several publications that help shed light on the consumer’s willingness to buy beef. Most of these utilize how much beef is being consumed at a certain price level.

One of the foundational tools used to measure demand is the USDA National Agricultural Statistics Service’s (NASS) monthly World Agricultural Supply and Demand Estimates (WASDE). While the WASDE report is more commonly known for grains and oilseeds, it also contains a lot of information on meat including “disappearance.” Disappearance refers to the estimated amount of a product, like beef, that is used domestically over a period of time, based on production, imports, exports and changes in storage. In the May WASDE report, USDA estimated that 2025 consumption of beef will be 28.91 billion pounds. This forecast is down about 49 million or 1.4% from last month and down just 0.5% from last year. This means USDA is forecasting a minimal slowdown in beef consumption compared to last year. This forecast predicts strong demand through 2025.

Beef Export Demand Slowing

Exports to other countries are a critical part of demand because they add value to nearly all players in the supply chain. The U.S. exported 1.29 million metric tons of beef in 2024 worth almost $10.5 billion. The top trade partners by value were South Korea, Japan, China, Mexico, and Canada. Export demand has been slower in 2025. So far, the U.S. has accumulated 277.6 thousand metric tons of beef export sales this year, nearly 22% less than the same time in 2024. While exports to countries like South Korea and Canada have remained strong, tariffs have slowed sales down, particularly to China. Total export sales to China are currently 32% behind 2024.

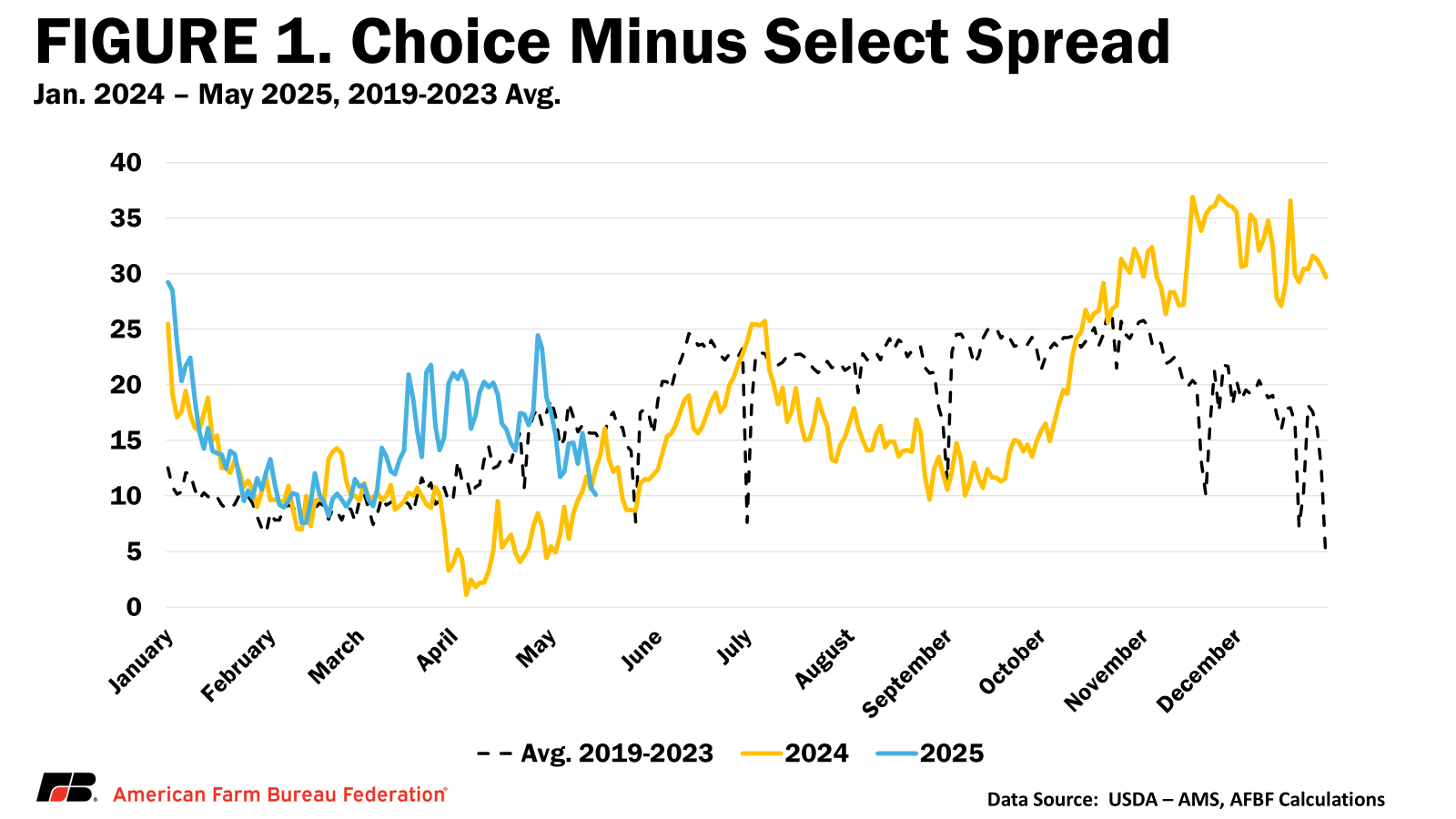

Narrowing Difference Between Choice and Select Beef

Another gauge of consumer demand for beef is the difference between the cutout value for choice grade and select grade beef. Choice grade beef is a premium product compared to select grade. When the difference between the two is greater than $10-$15, it can be an indicator of strong demand because consumers are more willing to pay for a premium product. A narrowing spread, on the other hand, can indicate softening demand for premium cuts or reduced availability of Select-grade beef. The choice-select spread has fallen from $18.89 on May 1 to $10.10 per cwt on May 16. During this time, the cutout value for select beef grew 5.6%, much faster than the price of choice grade which grew by 2.7% in the same time. (Figure 1.) This shift may reflect tighter supplies of Select beef rather than weakening overall demand, as consumers appear willing to continue purchasing both grades at elevated prices

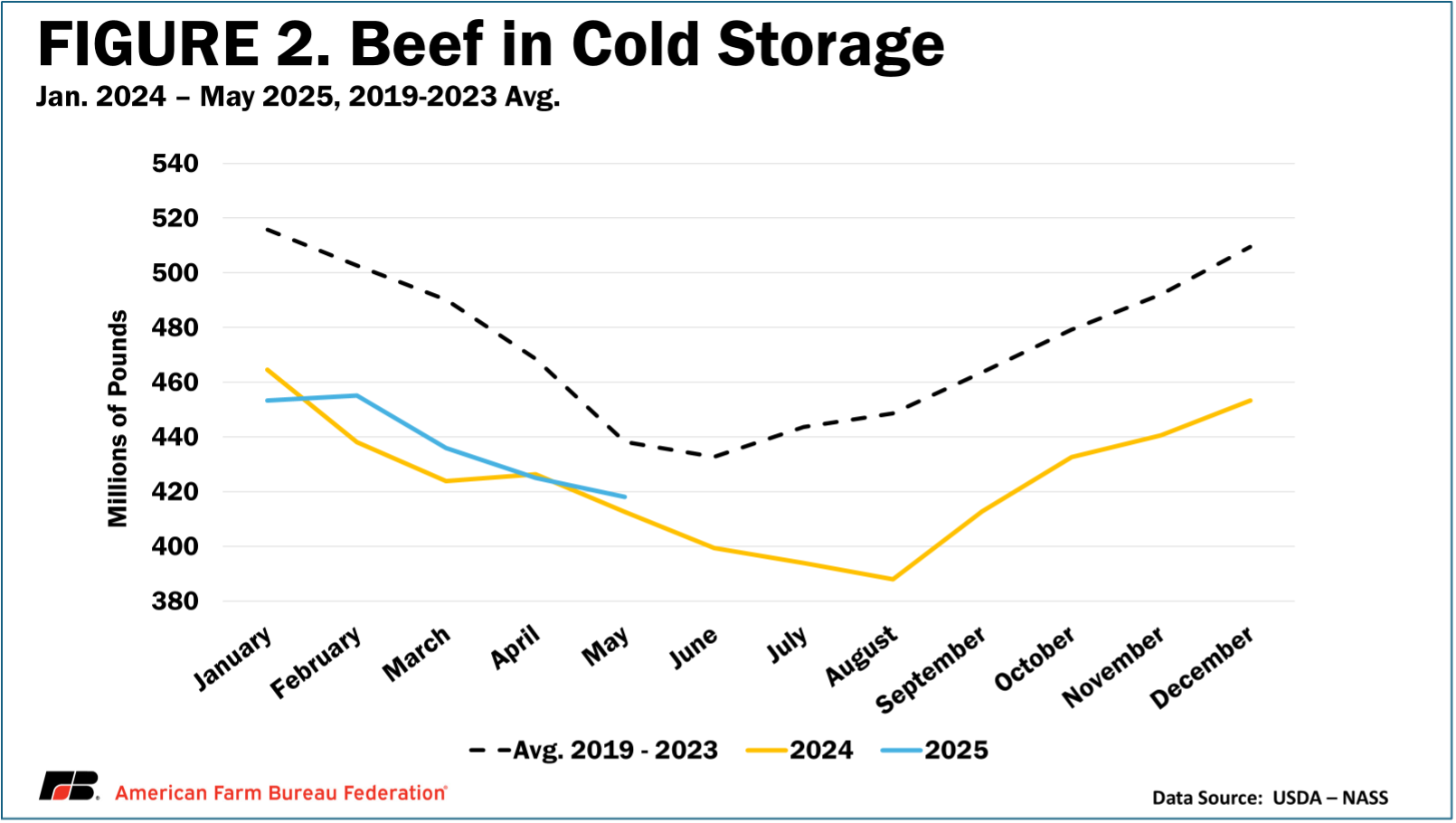

Cold Storage Supplies Dropping

USDA’s Cold Storage report measures reserve food supplies held in commercial and public warehouses including beef, pork and poultry. Changes in beef held in cold storage can be used to gauge demand. Declines in beef in cold storage over time means more beef is disappearing than is being placed in cold storage. This could be from increased demand, but it could also be because production has slowed down. This is why it’s important to use other tools like the ones in this article to put the story together. Beef in cold storage in May was 418 million pounds, up about five million pounds from 2024, but nearly 4.5% below the 5-year average and 5 million pounds lower than last month (Figure 2).

Note: This will be updated upon the release of USDA’s monthly Cold Storage report on Friday, May 23.

Consumer Sentiment on Shakey Ground

U.S. consumer demand for meat historically has grown with improved household financial situations and then falls when incomes drop. Consumer Confidence, also called consumer sentiment, describes the opinions and attitudes of consumers about the current and future strength of the economy. This means when U.S. households are doing well, they buy more meat, particularly beef.

The University of Michigan publishes a variety data related to consumer surveys including the Index of Consumer Sentiment. According to May 2025 data, the Index of Consumer Sentiment was 50.8. While this was only a small change from April, this rating is down 26.5% from May 2024. This is concerning for beef demand in the long run because of its close tie to consumer sentiment.

According to a recent study by Kansas State University, meat price inflation has outpaced inflation for other goods in 2025 and has been consistently elevated for the last five years. This could be a reflection of higher cost increases for the livestock producers, higher demand, or both.

Since the COVID-19 pandemic, Americans have developed a preference for beef over other meats, such as pork or poultry. , even though the average consumer eats about twice as much chicken by volume, beef remains the top choice when quality and taste are prioritized. If consumer confidence falls alongside household financial uncertainty, demand for beef could be at risk especially in the face of record high retail prices.

Conclusion:

Cattle prices Cattle prices have set records on multiple occasions already this year. Even with these record high prices, margins for cattle farmers and ranchers are razor thin thanks to continued elevated supply costs. Demand is currently strong, but this situation could quickly change. Any decline in consumer confidence or household financial health could weaken demand, forcing packers to lower bids and triggering financial losses for cattle farmers and ranchers. Mentioned in a previous Market Intel, the cattle inventory is continuing to be on contraction in this hypercycle. For the cattle inventory to expand, the industry needs to be profitable. If demand cannot remain strong at these price levels, prices will fall, and profitability will stand in the way of meaningful growth and the economic sustainability of the cattle industry.

Keep an eye out for more on beef and consumer demand with American Farm Bureau Federation’s 2025 July 4thCookout Survey, expected June 25th!

Top Issues

VIEW ALL