Hog Prices Waiting On Seasonal Rally

AFBF Staff

photo credit: Getty Images

Earlier this week AFBF’s Market Intel article “Cattle Outlook: Will the Spring Rally Hold?” discussed the beef cutout moving higher in recent weeks. The pork cutout has done the opposite. Over the last six weeks, pork cutout has fallen over $8 per hundredweight from the year-to-date high of $82 per hundredweight.

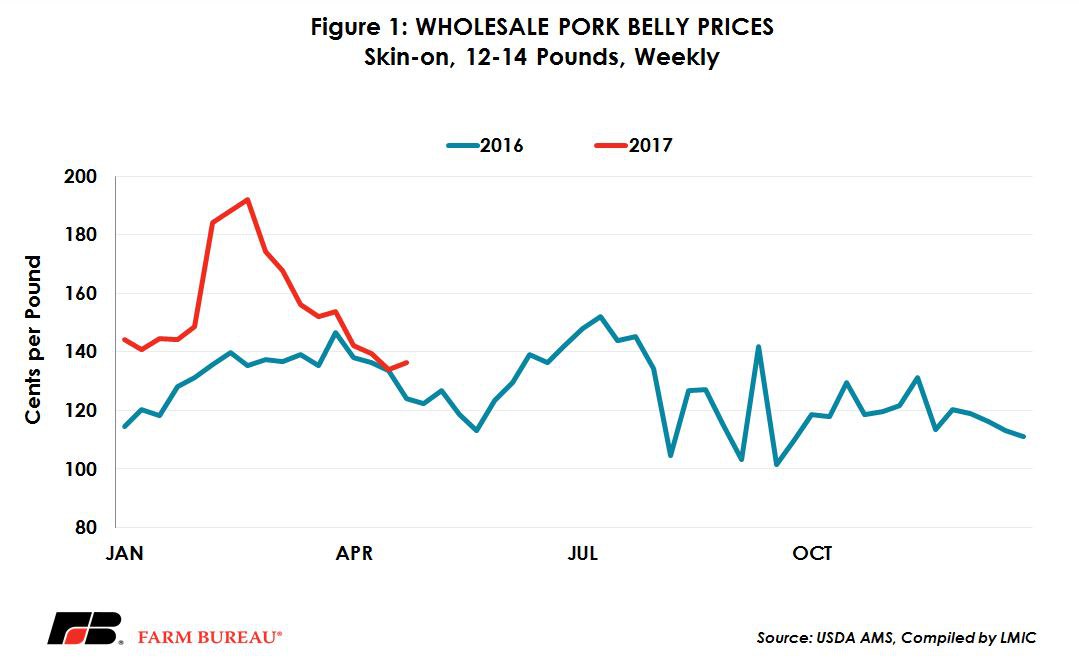

The early rally in pork cutout value was driven off a spike in wholesale belly prices, which hit $192 per hundredweight in mid-February, see Figure 1. The daily composite primal value for bellies reached $185 per hundredweight that same week, the highest seen since April 2014. Belly prices have eased off aggressively since mid-February, falling for 10 consecutive weeks.

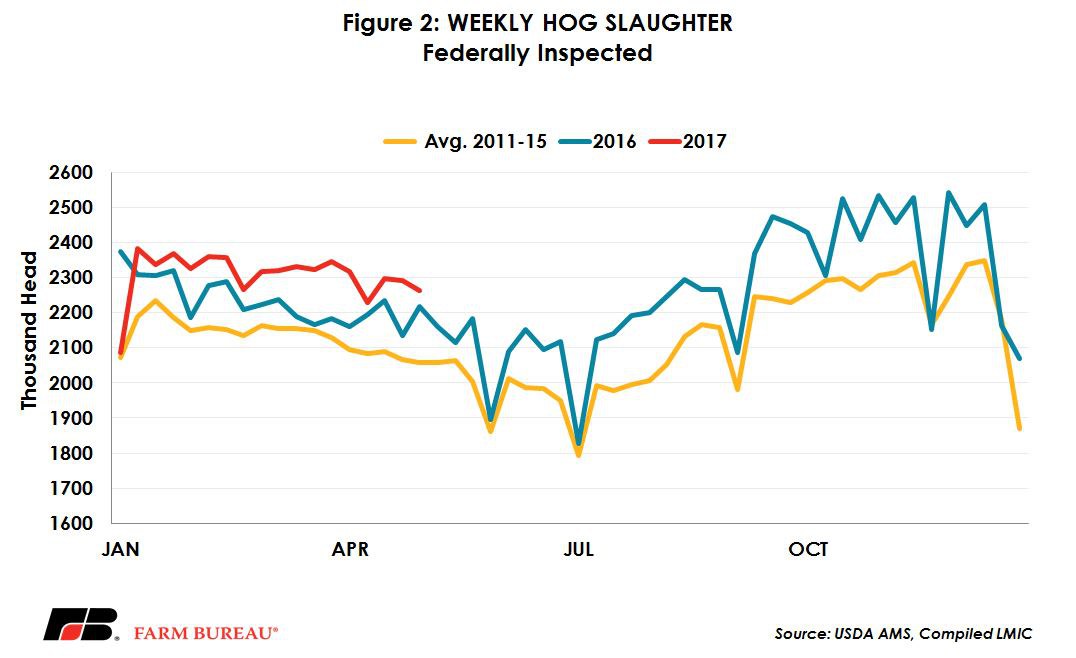

Barrow and gilt prices in Iowa-Minnesota and national base slaughter prices have experienced similar volatility in the first part of this year, locking in the highest prices in February. Seasonal norms suggest higher slaughter hog prices in the second quarter, which is typically driven by the decline in slaughter through the summer months. This year slaughter rates have not shown signs of significant slowing. A heavy supply of hogs have weekly hog slaughter maintaining figures well above those seen last year, as well as year-over-year increases in the number of hogs slaughtered on Saturdays. Dressed weights would imply the market is current and that hogs are not necessarily moving through slaughter channels at an accelerated rate. Figure 2 shows weekly hog slaughter compared to last year.

If slaughter rates do not slow down this summer, prices may not increase without a boost from demand. Domestic demand is expected to be stronger this year. USDA’s May 10, 2017, World Agricultural Supply and Demand Estimates Report (WASDE) projects domestic consumption on a per capita basis to be up four tenths of a pound in 2017, and a 1.6 percent rise in domestic use. Exports have been strong so far this year. Year-to-date USDA’s Foreign Agricultural Service has shown pork exports up 17 percent. Some of the strongest increases have come from Mexico (33 percent) and South Korea (31 percent). Only two of the major U.S. trading partners are showing year-over-year declines in pork purchasing. Hong Kong and China are down both in the month of March and through the first quarter of this year. Mexico and Japan (8 percent) are our two largest markets and the large increases look promising.

Pork production is expected to be over 4 percent higher than last year, but as long as both foreign and domestic demand remains strong, WASDE predicts hog prices only slightly below a year ago on an annual basis. WASDE is a bit of an outlier on prices at this point. Other analysts’ (LMIC, Chris Hurt (Purdue University), Robert A. Brown(Robert A. Brown, Inc)) forecasts see slightly higher annual hog prices than 2016. Many of these analysts see packer margin compression as a larger factor later in the year in stark contrast to the exceptional packer margins seen in the fourth quarter of 2016.

WASDE also released annual estimates for 2018. Pork production is expected to continue to increase, up another 3.2 percent from 2017 annual estimates. Estimates for per capita consumption are expected to take a large leap forward, adding eigth tenths of a pound to consumption in 2018. WASDE estimates hog prices to decline further based on increases in supplies.

Top Issues

VIEW ALL