January Cattle Inventory Shows First Herd Contraction Since 2014

TOPICS

USDAMichael Nepveux

Former AFBF Economist

photo credit: Alabama Farmers Federation, Used with Permission

Michael Nepveux

Former AFBF Economist

On Friday, USDA released its biannual U.S. cattle inventory report showing U.S. cattle totals as of Jan. 1. The report provides inventory data for the nation’s cattle herd, including estimates of the number of breeding animals for beef and milk production, as well as the number of heifers being held for breeding herd replacement. This important report identifies beef and milk cow herd trends, helping the cattle industry evaluate the amount of product moving to market.

Cattle Inventory

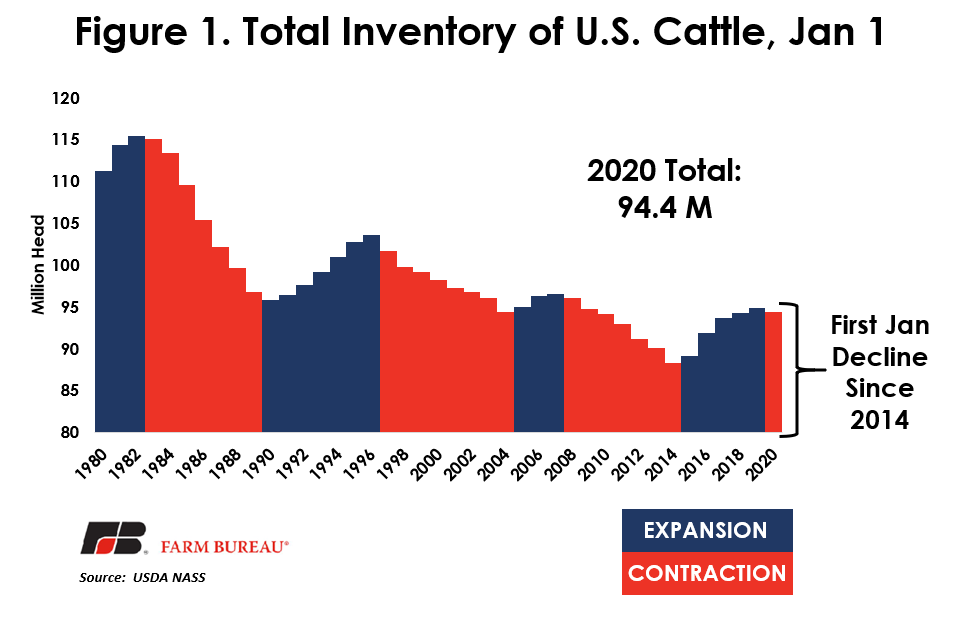

As of Jan. 1, all cattle and calves in the U.S. totaled 94.413 million head, slightly below the 94.804 million head reported for Jan. 1, 2019. This marks the first year-over-year January decline in cattle numbers since 2014, the beginning of the current cattle cycle. From 2014 to 2020 the herd grew by more than 6.5 million head, an increase of approximately 7.4%. Higher prices in previous years largely drove the expansion of the herd. However, as these prices have come back down, the expansion of the herd has appeared to level off. Moving forward, some in the industry are calling for a more moderated herd decline in the next phase of this cycle than has been seen in previous cycles.

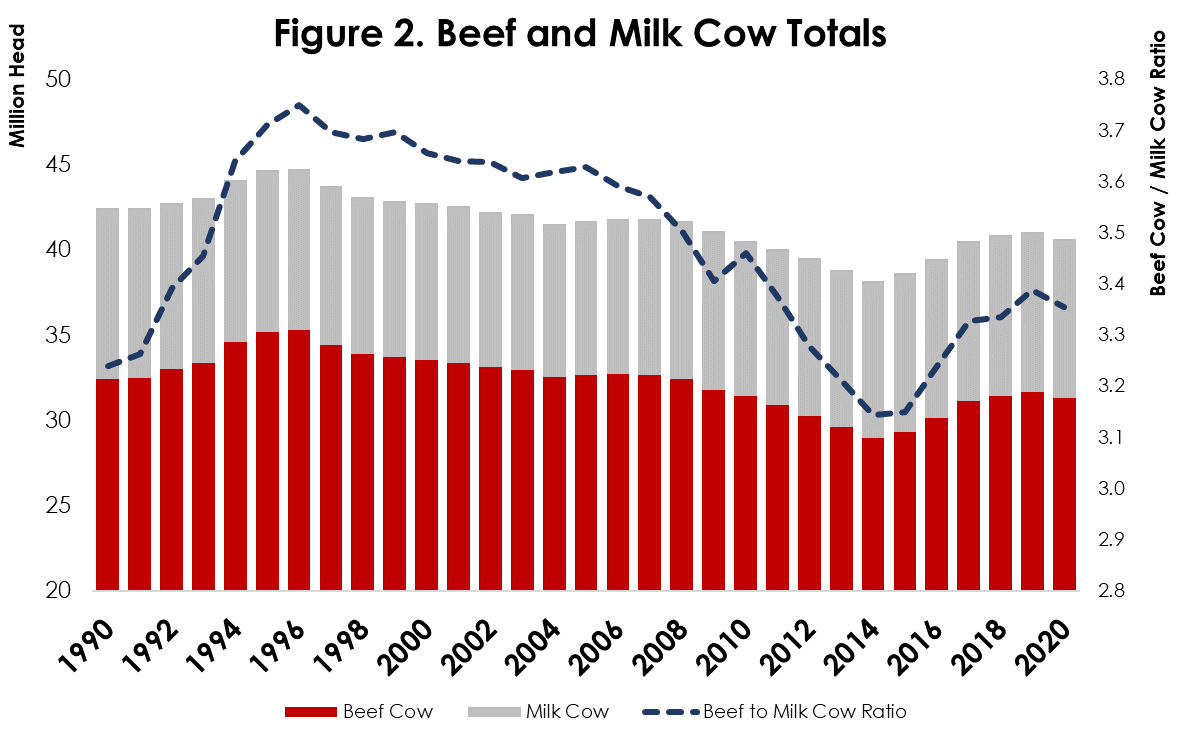

All cows and heifers that have calved totaled 40.651 million head, an approximately 1% decline from 41.044 million head in 2019. This decline is mostly reflected in a drawdown in beef cows rather than dairy cows, with beef cows declining almost 375,000 head compared to a nearly 20,000-head decline in dairy cows. Figure 2 shows the relationship between dairy and beef cows reported over time in the January report. When comparing the ratio of beef to dairy cows, the variation is largely driven by changes in the beef cow numbers as producers expand or contract in the cattle cycle. Over the past two decades, the number of dairy cows reported in the January report has remained relatively stable, especially when compared to the number of beef cows.

Apart from the total number of cattle and cows that have calved being down, another signal that producers are putting the brakes on expanding is a decline in the number of replacement heifers for both beef and dairy herds. The number of replacement heifers fell by 113,000 for beef cows and 65,000 for dairy cows.

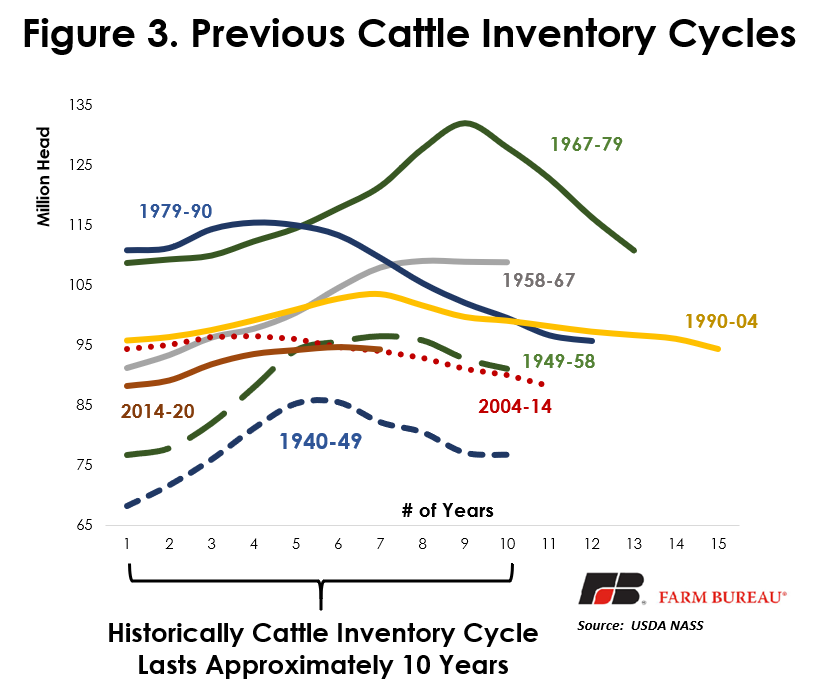

We’re at the Peak of the Cattle Inventory Cycle

Historically, the U.S. experienced a relatively predictable cattle inventory cycle of approximately 10 years in length. When talking about the cattle inventory cycle, the beginning of the cycle is marked by an expansion phase, followed by a peak and a contraction phase. Historically (but not always), the expansion phase was longer due to the relative length of time it takes to rebuild herds and the time between a producer making a breeding decision and the animal coming to market. However, the last three cattle inventory cycles have experienced shorter expansion phases followed by longer controlled contraction phases. What typically occurs in the expansion phase is slaughter numbers are falling and result in increasing prices, which in turn stimulate increasing future cattle numbers through heifer retention. Due to the biology of the cow, the cattle number increase lags the price increase, while harvest numbers will run somewhat countercyclical to price.

In recent decades there have been outside events impacting the cycle beyond normal marketing decisions. For a length of time in the 2000s, much of the U.S.-cattle-producing area experienced drought, and by 2012 much of the U.S. was experiencing tough drought conditions. This led to a confluence of poor pasture and range conditions, high corn prices and herd liquidation, even with high cattle prices. The current cattle cycle began in 2014 and includes a six-year expansion phase before the start of the contraction in 2020. It remains to be seen how long the contraction phase will last and to what magnitude the herd will decline.

Summary

January’s cattle inventory report marks the first year-over-year January decline in cattle numbers since 2014, the beginning of the current cattle cycle, and provides somewhat bullish news for cattle prices. From 2014 to 2020 the herd grew by more than 6.5 million head, an increase of approximately 7.4%. We have reached the peak of the current cattle cycle with this report, and the next phase is the contraction of the herd. Moving forward, some in the industry are calling for a more moderated herd contraction in the next phase of this cycle than in previous cycles, so this cattle cycle may look a little different.

Top Issues

VIEW ALL