Tariffs Impact Crop Insurance Coverage in 2019

photo credit: AFBF Photo/Morgan Walker

John Newton, Ph.D.

Vice President of Public Policy and Economic Analysis

Each year, prior to the beginning of planting season, USDA’s Risk Management Agency recalibrates crop insurance protection based on expected commodity prices and risk in the market. Market expectations for prices and volatility, i.e., level of riskiness associated with the crop price, are combined with yield history to determine both the level of revenue protection available during the crop year and the premium cost.

The 2019 growing season is unique in that it is the first season for which retaliatory tariffs on agricultural products were in effect prior to planting. The impact of these tariffs has weighed on commodity prices and markets for nearly a year and has now materialized in the crop insurance prices going into the 2019 growing season.

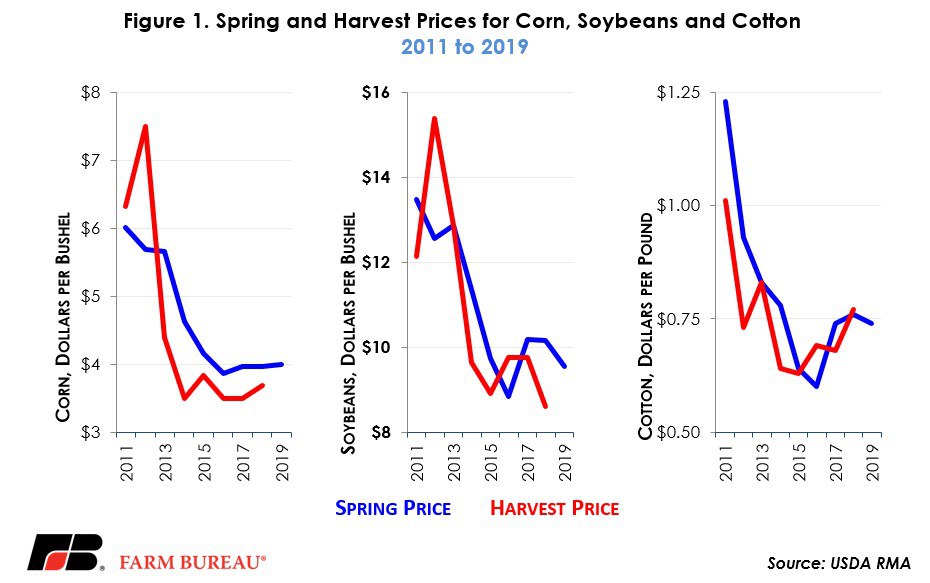

The decline in the spring crop insurance price is most notable in soybeans. RMA’s Crop Insurance Price Discovery tool revealed that for the 2019 crop year, the spring crop insurance price for soybeans was $9.54 per bushel, down 62 cents from 2018 and the second lowest level since 2009. The low crop insurance price is a direct result of the slowdown in soybean exports to China and the expectations for record-high soybean ending stocks.

While the spring price for soybeans reflects the current trade environment and a slowdown in demand, should the U.S. and China reach a deal that restores the Chinese soybean and cotton markets, higher harvest prices for soybeans and cotton could help boost crop insurance protection in the event a grower experiences a crop loss.

For cotton, the spring crop insurance price was 74 cents per pound, down 2 cents from 2018. Despite retaliatory tariffs on cotton, cotton prices have remained steady in recent years due to sharp reductions in global ending stocks, strong U.S. exports and a very high abandonment rate in 2018.

Due to strong demand for corn in both the domestic and export channels helping to draw down domestic inventories, the spring crop insurance price for corn was $4.00 per bushel, up 4 cents from prior-year levels and the highest spring price since 2015.

Historical spring and harvest prices for corn, soybeans and cotton are highlighted in Figure 1. These crop insurance prices, and thus the revenue guarantees, were determined by averaging Chicago Board of Trade (corn and soybeans) and Intercontinental Exchange (cotton) futures contract settlement prices during a month-long price discovery period. Spring prices for corn, cotton and soybeans are determined by averaging the new-crop futures contract settlement prices (December for corn, November for soybeans and December for cotton) during the month-long February price discovery period.

Expected Price Distributions

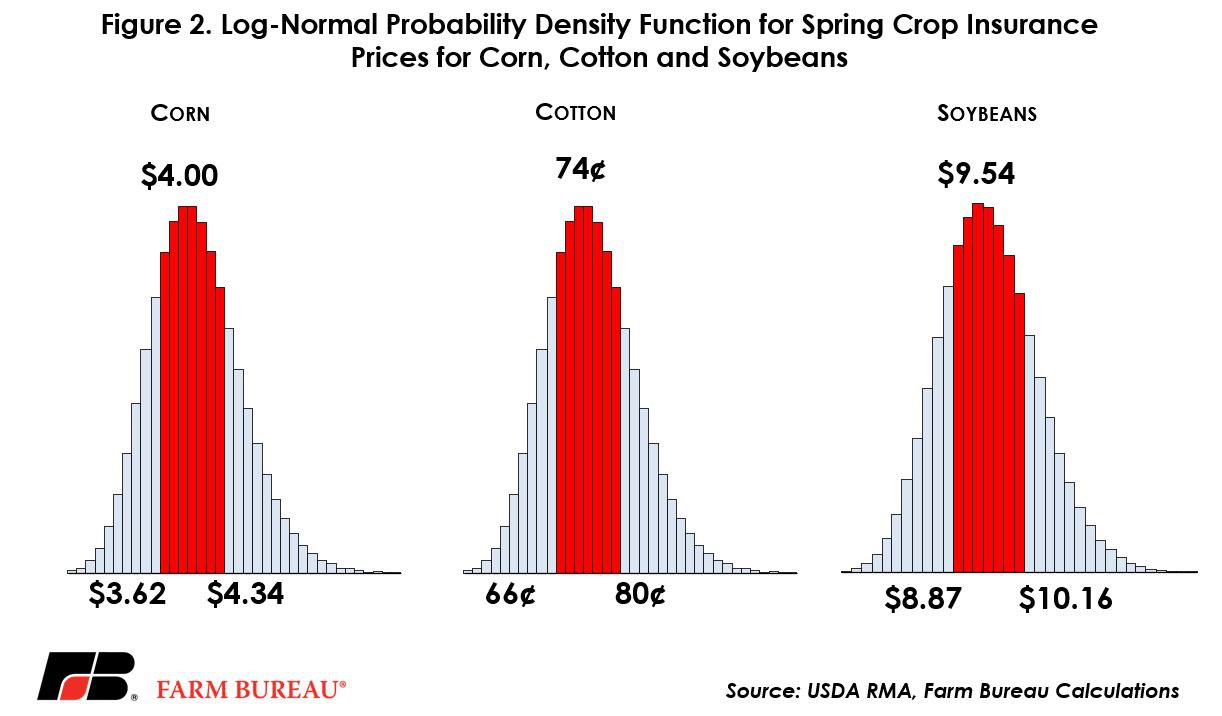

For the 2019 crop year the implied volatility factor for corn was announced at 0.15, in line with prior-year levels and down from 0.19 in 2017. Based on the projected price of $4.00 per bushel and the volatility factor, and assuming a log-normal distribution, there is a 50 percent probability that the new-crop corn contract will expire between $3.62 per bushel and $4.34 per bushel. (Note, these probabilities will differ if using contemporaneous futures prices, implied volatilities and days to maturity.)

The volatility factor for cotton was announced at 0.14, in line with prior-year levels. Based on the projected price of 74 cents per pound, and assuming a log-normal distribution, there is a 50 percent probability that the new-crop cotton price will expire at a value between 66 cents per pound and 80 cents per pound.

The volatility factor for soybeans was announced at 0.12, down from 0.14 in 2018 and the lowest implied volatility since 2016. Based on the projected price of $9.54 per bushel and implied volatility, and assuming a log-normal distribution, there is a 50 percent probability that the new-crop soybean price will expire at a value between $8.87 per bushel and $10.16 per bushel. Figure 2 highlights the price probability density functions for corn, cotton and soybeans derived using the projected price and implied volatility.

Harvest Price Option

Following the spring price discovery period, farmers may purchase revenue protection policies that provide insurance against declines in crop revenue from either a price decline, a crop loss, or a combination of both. In the event of a decline in revenue or a crop loss, a farmer purchasing a harvest price option policy would be indemnified at the higher of the spring planting price or the price during harvest. Harvest prices will be announced following the October price discovery period.

Currently, the new-crop prices for corn, soybeans and cotton are all below their spring projected prices. On March 1, new-crop corn futures settled at $3.94 per bushel, soybeans settled at $9.46 per bushel and cotton settled at 73.8 cents per pound.

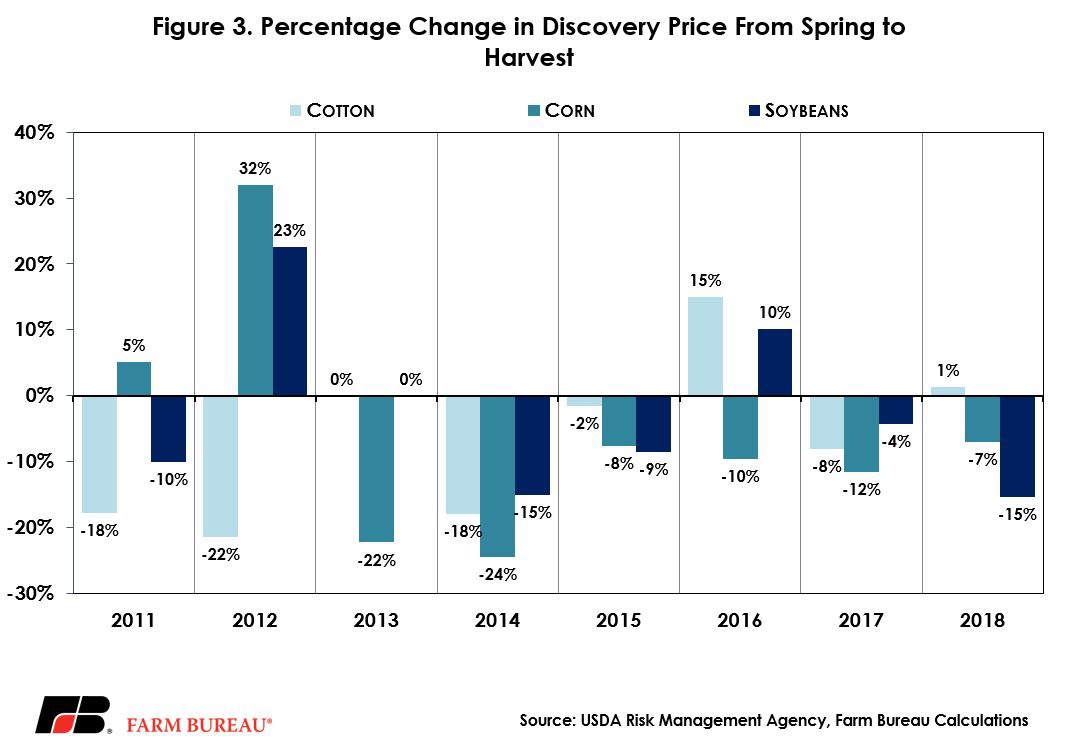

Over the past six years, the harvest price for corn has been below the spring price by an average of 60 cents per bushel, representing an average price decline during harvest of 14 percent. For soybeans, the harvest price has been below the spring price in four out of the last five years, with an average price decline of 11 percent, or $1.14 per bushel. In 2018, the soybean harvest price was $1.56 per bushel below the spring price guarantee. For cotton, the harvest prices were below the spring price in four out of the last five years, representing an average price decline of 7 percent.

It’s worth noting that in many cases the decline in crop insurance prices during the growing season coincided with very favorable, and above-trend, U.S. average crop yields. Figure 3 identifies the percentage change in crop insurance prices from the spring to harvest price discovery periods.

Clue For Acreage?

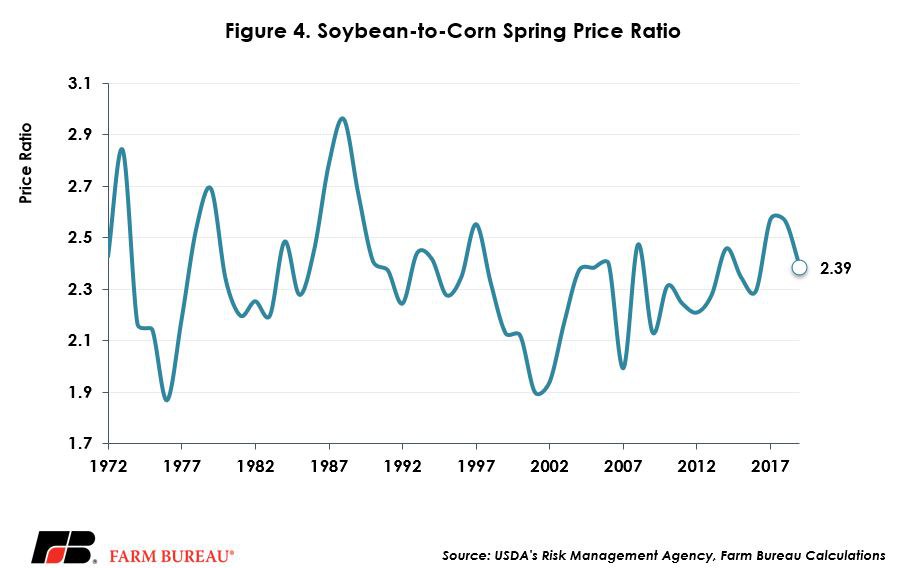

While the spring price discovery is important for crop insurance policies, many in the trade also use the spring prices to evaluate potential acreage shifts for corn and soybeans during the upcoming crop year. USDA currently projects corn acreage in 2019 at 92 million acres, up 3.3 percent from 2018. For soybeans, USDA projects 85 million acres planted in 2019, down 4.7 percent from 2018. Projections for 85 million soybean acres in 2019 are supported by the strength in the soybeans-to-corn spring price ratio at 2.39 – which is above the 10- and 20-year average, Figure 4.

The next opportunity to evaluate potential crop acreage will be the March 29 Prospective Plantings report. The Prospective Plantings report gives the first estimate of the acreage farmers are expected to plant to row crops for the upcoming year based on survey responses during the first two weeks of March. This report will remove some of the uncertainty on likely acreage decisions. Importantly, it will also reveal to what extent growers have responded to market signals by reducing soybean plantings in 2019.

Top Issues

VIEW ALL