That Could Have Been More Exciting… April 2017 Jobs Report

Bob Young

President

photo credit: Alabama Farmers Federation, Used with Permission

Bob Young

President

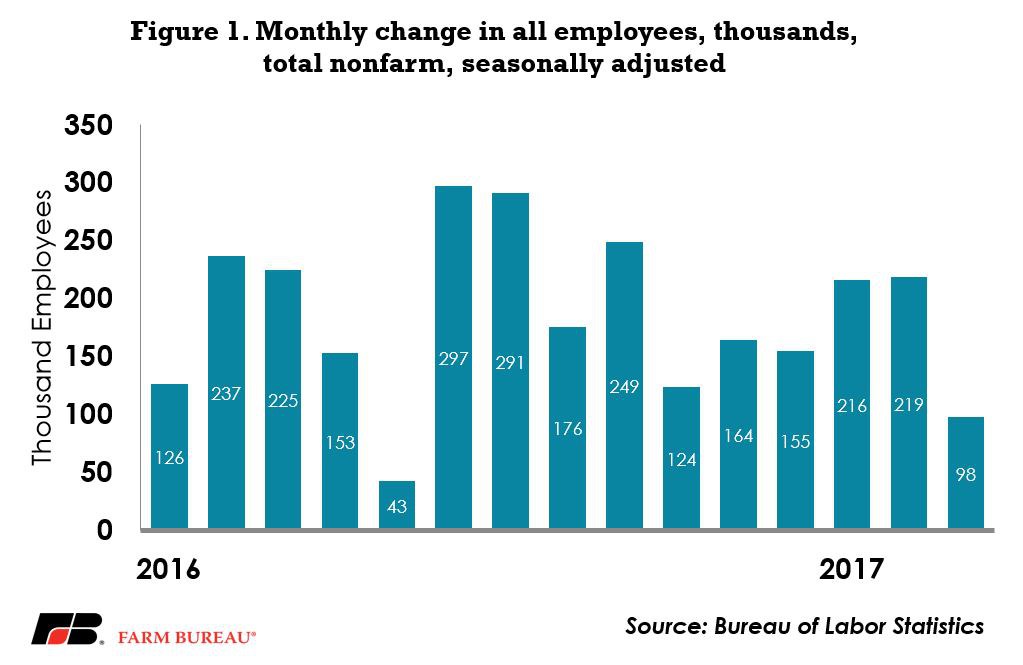

With headline numbers of 98,000 additional nonfarm employees following last month’s figure of 225,000 (initially, revised to 219,000 in this report) the April jobs report was underwhelming at best, disappointing at worst, Figure 1. The employment survey is a ‘noisy’ data series. And it is not at all unusual for revisions to substantially alter the numbers through time. Last September for example originally saw total nonfarm employment job growth reported at 156,000, but was later changed to 249,000 in the baseline revision. Initial reports for January of this year were revised higher in February and subsequently lower than the original report in the March report. So, take this figure with at least a pinch of salt.

March Job Creation By Category

Let’s look at some of the major components of the employment information. Construction is a category that showed great promise early this year with job growth of over 30,000 in January and nearly 60,000 in February. The figure for March was only 6,000. As one of my economist buddies says, you can only start a house once, meaning that the surge we had early in the year, probably couldn’t be sustained. We haven’t laid those folks off that were hired in January and February so we don’t need to hire that many more today. Weather in many parts of the country also allowed construction activity for the year to kick off early which also drove hiring. It’s not a story of a collapse in construction. In fact, it’s almost a story exactly the opposite when you think of year-to-date hiring.

Manufacturing is another sector that demonstrated higher than average job growth earlier this year, 12,000 in January and 26,000 in February, only to fall back to the 11,000 figure for March. Again, nothing like the 20,000 loss in this category in March of 2016, but nothing all that exciting either. Going a little deeper, fabricated metal products and motor vehicles and parts made up the bulk of this increase, suggesting the car body manufacturing as well as car/truck production at least thought it was doing well in March. Well enough to keep hiring.

Retail Trade, particularly those involved in direct sales to consumers, took another significant hit in March. Overall Retail Trade employment figures fell 29,700 positions, but General Merchandise category – part of the Retail Trade component – lost 34,700 slots. There has been quite a bit of conversation regarding challenges to retail stores coming from shifts in shopping patterns and competition from on-line sales. It is certainly showing up in the jobs market. This is another area where the age old question of trade versus technology is pretty clearly being answered. The technology of being able to custom order an item and have it shipped to your home in a matter of days is putting great pressure on the retail sector. It is not at all clear how they are going to work their way through this.

The opposite end of this is employment in the shipping industry. Overall figures there were up 3,500 with truck transport up 4,700 (other categories, transit and ground transportation were off 2,300 and messenger services were down 1,200). So, while consumers not going to stores is certainly impacting retail sales employment, somebody must take the packages to the door.

Health Care has been an amazing category to watch over the last several decades. It goes up. Recessions, downturns, collapses in other categories. It don’t matter. Health care employment has averaged a better than 23,000 new jobs every month for the last 25+ years. Sure some categories may grow more or less than others. Some may even contract once in a very great while, but health care has been a solid category for a long time. Until – maybe – lately. January growth figures were in the 15,000 range. February shot up to over 30,000 and now the March levels are back at 13,500. You have to look pretty hard over the last 10 years or so to find two out of three months in a row with growth under 20,000 in health care. Uncertainty over the whole health care industry because of the latest congressional debates? A fundamental shift in that industry? Have we finally gotten to the point where we can deal with all the baby boomers are we’re looking at the backend (open hospital gowns not part of this story) of that industry’s expansion? A few months of employment data do not a solid story make, particularly when one recognizes all of the adjustments in this data series that will likely happen, but it does raise a question.

Let’s close this discussion by looking at government employment. Very important here to look at the differences between Federal, State and Local employment categories. Federal employment continues to be a convenient political whipping post. Freeze hiring, let attrition reduce the work force, freeze pay hikes etc. Then complain about the quality of government service. Federal employment net of the Postal Service actually dipped by 2,600 employees. The Postal Service – remember that earlier conversation about home delivery – added 1,000. State government also added 1,000 slots, but local government was up 9,000, with all the growth coming in education. Outside of education, local government employment shrank by 1,200.

Implications

The job growth in the last few months was probably driven by the end of the uncertainty created by the election cycle. The question going forward is whether this month reflects the underlying mood of the economy now that we’ve moved past all of that pent-up hiring demand. A few more months of this kind of data may begin to raise more questions than answers, but will indicate the economy may be showing more fragility than the last quarter would have suggested. Again, employment data changes. It is one of the more volatile data series one can dig in to and should always be taken with a grain of salt. Certainly one report does not a trend make. But it does certainly raise the importance of next month’s report that much more.

Top Issues

VIEW ALL