Third Quarter Numbers Show Rail Service Improving Though Barriers Remain

TOPICS

Supply Chain

photo credit: Getty

Daniel Munch

Economist

Market access is vital to the operation of any business, including farms and ranches across the United States. The complex system of rail lines crisscrossing the nation are essential to delivering inputs to producers and goods to customers – when the network functions effectively and efficiently. Over the past several years, starting with the COVID-19 pandemic and exacerbated by global geopolitical rifts, rail service quality plummeted, limiting producers’ abilities to get product delivered. Previous Market Intels such as Increasing Freight Rail Rates Put Additional Pressure on Farm and Ranch Income, Farmers and Ranchers Feel Crunch of Railway Supply Chain Shortfalls and Rail Order Delays, Empty Exports and Equipment Shortages – Transportation Disruptions Persist outlined many of the factors complicating farmers and ranchers’ ability to cost-effectively utilize rail systems to market their products. Today, we provide a third quarter update on the status of railway service conditions.

Total grain rail cars loaded and billed dropped in the third quarter of 2022 from 398,000 cars in quarter two to 351,000 cars in quarter three. This 47,000-car difference, though drastic, is about half the drop that occurred between quarter two 2021 and quarter three 2021, when only 295,000 cars were loaded. In other words, railways loaded and billed fewer grain cars than last quarter but more grain cars than this time last year. Burlington Northern and Santa Fe Railway (BNSF) and Union Pacific Railroad (UP), railroads that together processed 60% of all grain rail cars in quarter three 2022, shipped 14% and 5% fewer grain rail cars than last quarter, respectively.

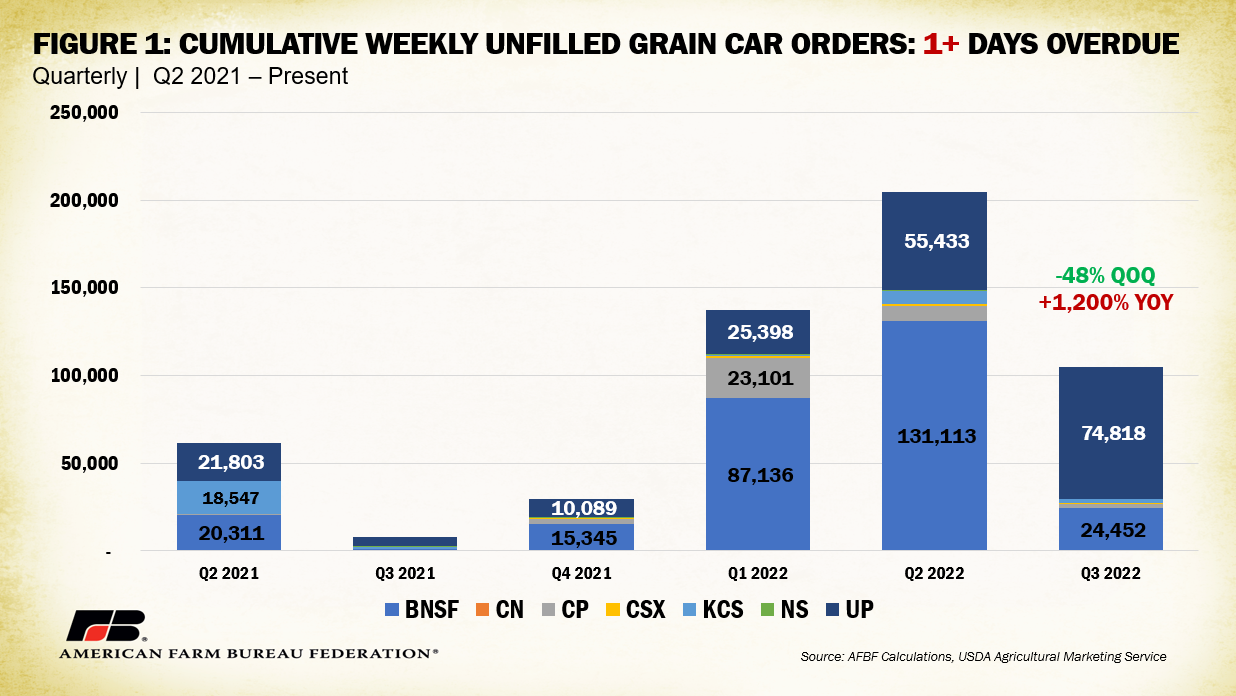

A look at cumulative weekly unfilled grain car orders, a metric that tracks grain cars not effectively loaded and billed, reveals these declines are still not due to reduced demand from shippers. As a reminder, each railroad reports its definition of “unfilled order” slightly differently but generally it is the number of cars a shipper (such as a grain elevator) ordered but did not receive. For example, if a grain elevator ordered 10 cars from a railroad and received seven, that would leave three unfilled orders. Though railroad companies report the number of these unfilled orders to the Surface Transportation Board weekly, the dataset does not distinguish between rail cars still undelivered between weeks or new undelivered grain cars. This means grain cars that are still undelivered over one week are counted again in the following week’s report until successful delivery. For example, in a quarter with 130,000 cumulative weekly unfilled grain car orders it is possible that 10,000 grain cars were undelivered consecutively over the 13-week period, 130,000 different grain cars went undelivered at one point within the 13 weeks, or some mix in between. Regardless, this unit allows for an over-time comparison of reported unfilled orders in one statistic. Figure 1 displays the cumulative number of weekly grain car orders by quarter from quarter two 2021 to quarter three 2022 that were one or more days overdue. Between the second quarter of 2022 and third quarter of 2022, the number of these cumulative unfilled orders dropped from 204,000 to 104,000 – a 48% decrease. BNSF saw an 81% drop in cumulative unfilled orders over last quarter from 131,000 to 24,452. In weekly metrics this translates to a drop from 10,086 average unfilled orders per week to 1,880. UP numbers are not as positive, showing an increase of 19,385 (55,000 to 74,000), or 35%, in cumulative unfilled orders between the second and third quarters of 2022. In weekly metrics this translates to an increase from 4,264 average unfilled orders per week to 5,755. Year-over-year, however, cumulative weekly unfilled grain car orders between quarter three of 2021 and quarter three of 2022 are up over 1,200% (7,962 compared to 104,610), illustrating there is still work to be done.

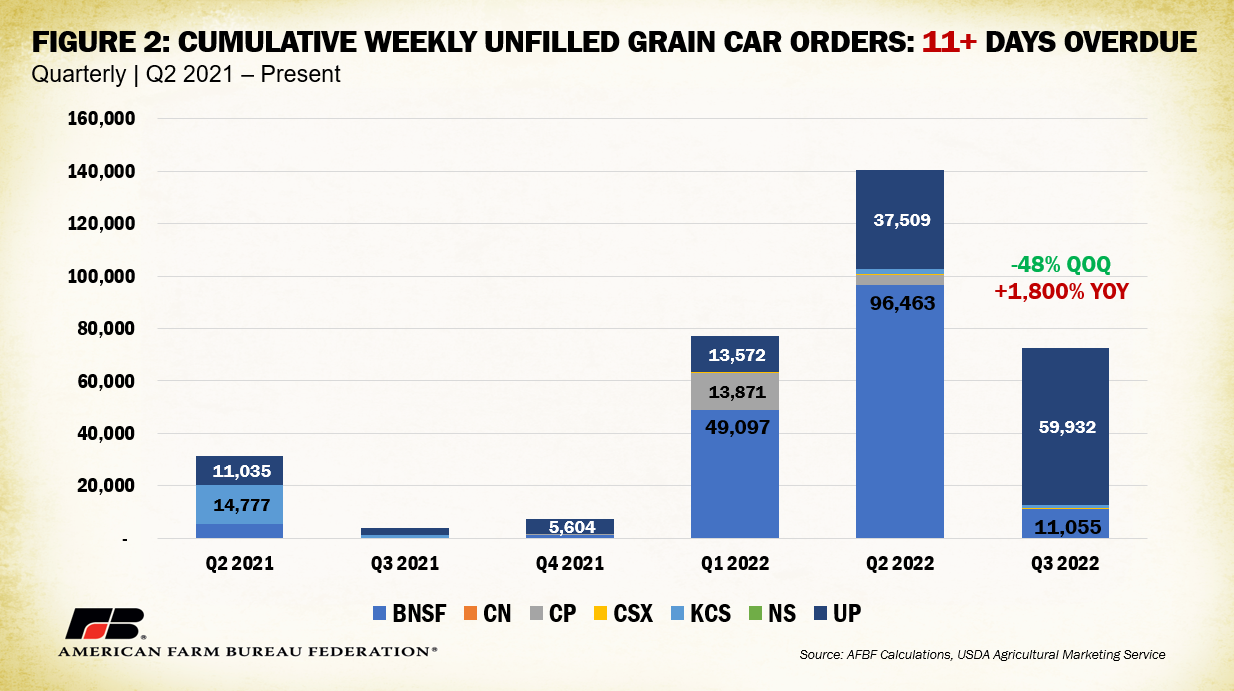

Of these 104,000 cumulative unfilled grain car orders one or more days overdue, nearly 70%, or 73,000, remain 11 or more days overdue – an 1,800% increase from the third quarter last year but a 48% decrease from last quarter. Comparing quarter three 2022 to quarter two 2022, BNSF saw a drop of over 85,000 cumulative unfilled orders 11 or more days overdue (-88%) while UP saw an increase of over 22,000 (+60%). Even though order delays are declining compared to last quarter, the bulk of delays are still lasting 11 days or more, leaving impacted grain mills or livestock operations reliant on a steady stream of raw materials and feed in limbo. By state, conditions have improved in North Dakota, which saw a drop in cumulative unfilled orders one or more days overdue from over 45,000 in quarter two to nearly 7,000 in quarter three (-85%), though rates there remain higher than most states. Other Upper Midwest and Central Plains states like Nebraska, Kansas, Iowa and Minnesota still faced cumulative unfilled orders of over 10,000 in quarter three, though they also experienced 35% to 50% drops in unfilled orders from last quarter.

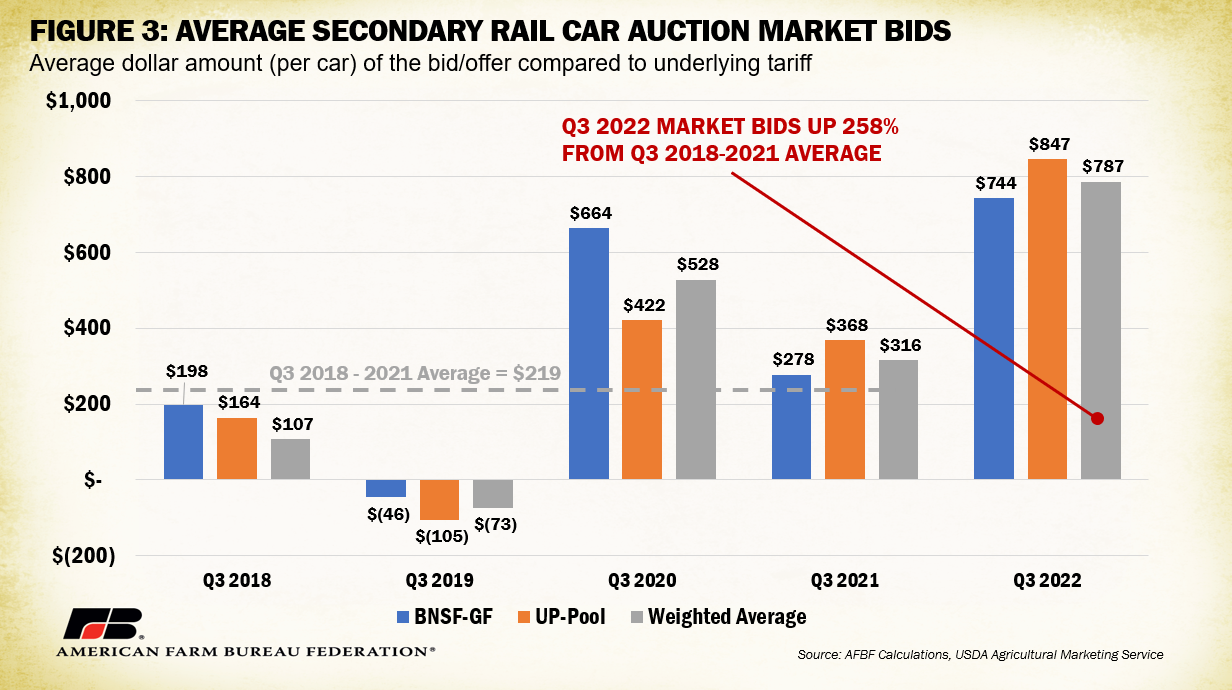

One area that further reveals the impacts of unfilled orders on shippers is the secondary rail market, where shippers bid against each other for contracts that could increase the chance of getting delayed product successfully moved. Last quarter, bidders faced a near 550% increase in secondary rail car auction bids from the prior four-year average (between BNSF and UP). This quarter, UP bidders faced lower bids (-36%) while BNSF faced higher bids (+41%), with the weighted average up about $5 (from $782 to $787). Compared to quarter three last year, weighted average bids are up 150% (from $316 to $787). Figure 3 displays these quarter three comparisons, highlighting that strong demand remains within secondary rail car markets. The values represent the average dollar amount per bid above or below the original primary market service contract value. Continued inflated rates in these auctions act as proxy for railway efficiency when shippers are forced to bid for a shrinking number of successfully loaded and billed contracts, as reflected in heightened unfilled order metrics.

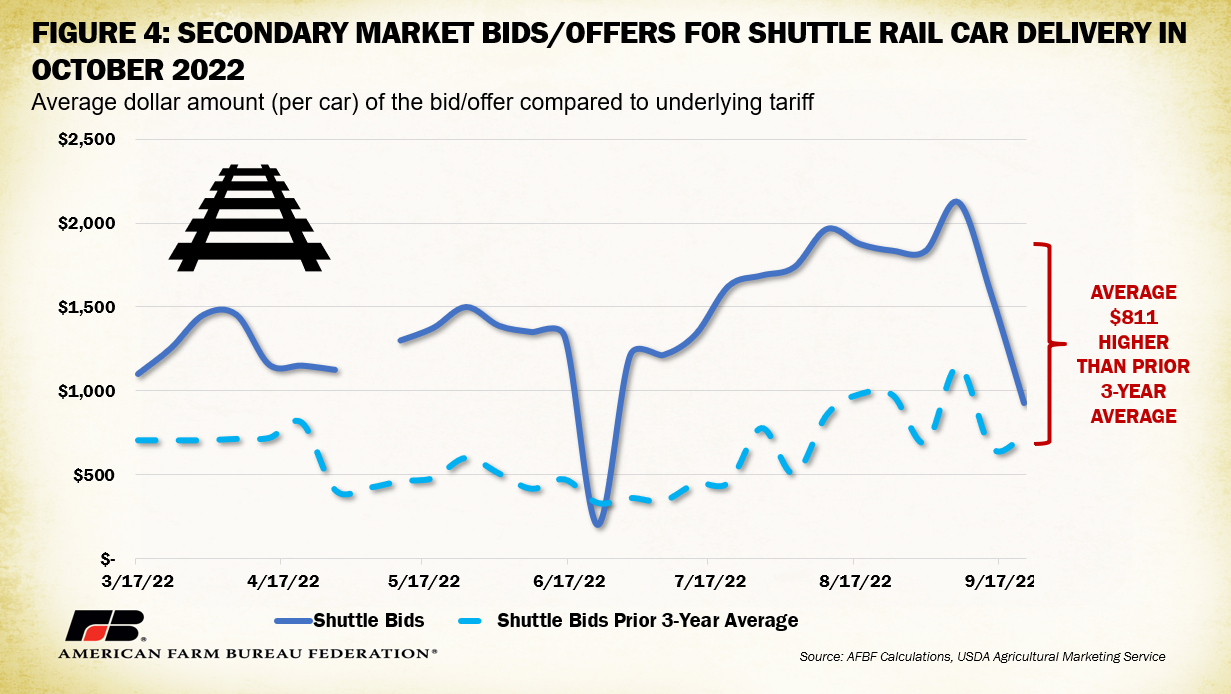

Secondary market bids for shuttle service have been elevated for deliveries to be made in October compared to bids for deliveries made in August. Figure 4 shows that for the period between March and September, weekly bids for October deliveries were, on average, $811 higher than the prior three-year average for October shuttle car deliveries and well above the underlying contract tariff (as reflected in a positive value). This is a much larger margin than the $111 difference previously analyzed for August contracts. Shippers with flexibility in moving product may participate into the secondary market to take advantage of high bids for existing contracts, further contributing to delivery uncertainty.

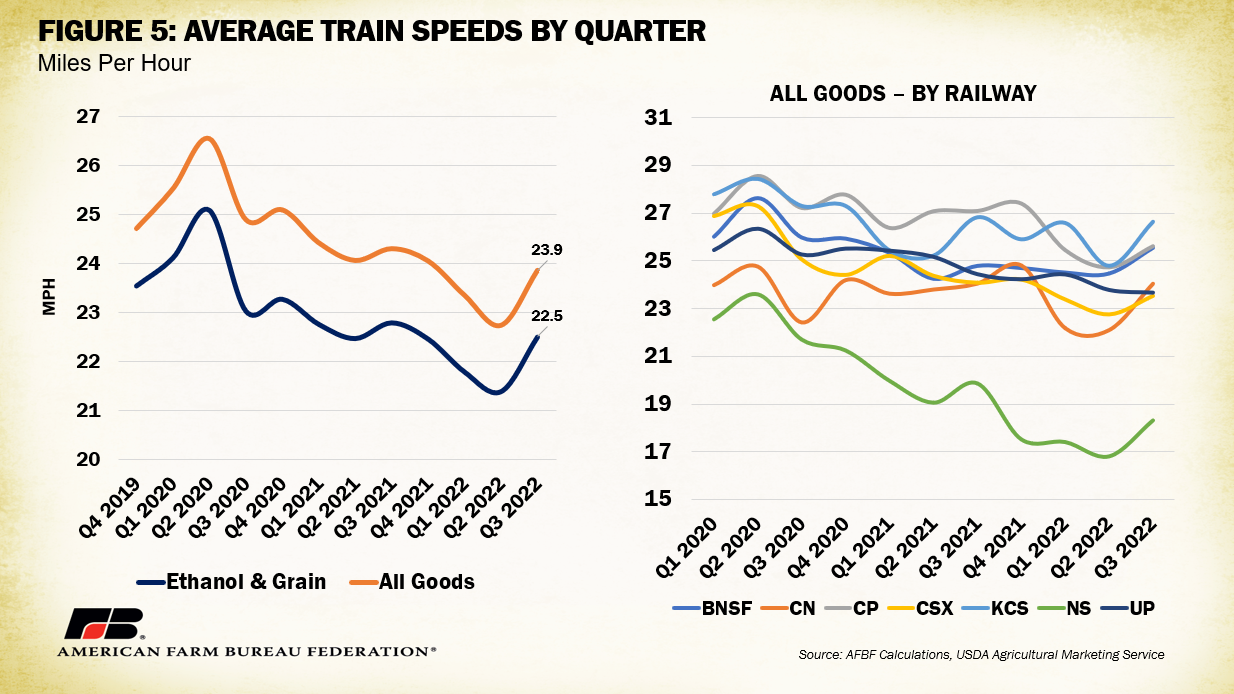

Considering other service quality metrics, rail speeds are improving. As part of their submission to the Surface Transportation Board, railroads provide data on the average speed of their trains (in miles per hour), broken out by commodity/type such as automotive, coal, crude oil, ethanol, grain, intermodal, manifest, etc. In early 2020 when the COVID-19 pandemic initially dropped demand for goods, rail speeds reached 26 mph for all goods and 25 mph for grains and ethanol – with less pressure on railways, fluidity was high. Last quarter, the average speed for all goods dropped to 22 mph (-14%) from quarter two 2020 and 21 mph (-15%) for ethanol and grains. This quarter, speeds have rebounded in both categories by about 5%, moving up to nearly 24 mph for all goods and 22.5 mph for ethanol and grain (though still 2%-5% below quarter three 2020). Even minor improvements in rail speeds compound downstream efficiencies. By railroad, all companies saw an improvement in rail speeds over last quarter though the magnitude varies. Compared to average train speeds in quarter three 2020, Norfolk Southern Railway (NS) remains 16% below, UP, CSX, and Canadian Pacific Railway (CP) 6% below, BNSF and Kansas City Southern Railway (KCS) 2% below, and Canadian National Railway (CN) has beat quarter three 2020 speeds by 7%.

Rail origin dwell times, the number of hours trains spend waiting after initial release at origin, have decreased by 18% across railroads between the second quarter of 2022 and the third quarter of 2022 and remain 30% higher from quarter three last year. KCS experienced a 79% decrease in origin dwell times between the second and third quarter, followed by CP, which faced a decline of 42%. On the terminal dwell time side, quarter-to-quarter waiting times have decreased by 4% this year and increased 9% comparing quarter three 2022 to quarter three 2021. Rail yards with the largest quarter-to-quarter increases included Louisville, Kentucky (+108%); Harvey, North Dakota (+88%); Decatur, Illinois (+73%); and Selkirk, New York (+59%). Slowed and delayed service contributes to increased rates of unfilled orders across the country.

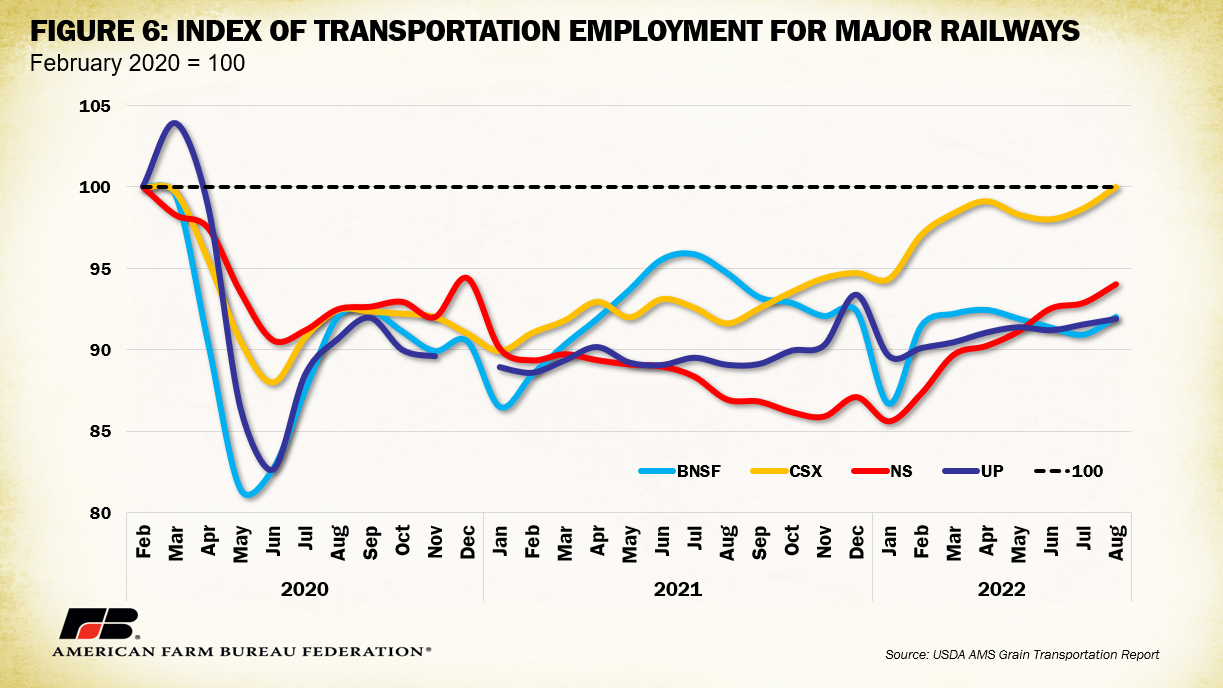

Many of the reasons for service and quality disruptions discussed in previous Market Intels remain relevant. Low container and equipment inventories have stalled operational capacity across all segments of the transportation system. Railroads have cited labor challenges as a primary hurdle to reaching pre-COVID efficiency. As noted in the Sept. 29 Grain Transportation Report, many railroads accelerated labor force cuts in the wake of low demand during early 2020. When demand returned, a tight labor market complicated the hiring of new employees. Figure 6 displays the index of transportation employment for four major railroads with employment indexed to pre-pandemic levels (February 2020). CSX remains the only railroad of the four to reach pre-pandemic employment levels. BNSF hit 95% of their pre-pandemic employment in July 2021 but has since hovered between 86% and 92%. UP has also struggled to hire, with an average employment of 90% between October 2020 and August 2022. NS has rebounded in the past 8 months, jumping from 85% in January to 94% in August. KCS and CN, which are not displayed, have surpassed or are near pre-pandemic employment. With BNSF and UP in control of 60% of grain movements, continued employment issues do not bode well for farmers and ranchers looking to move product, especially with harvest season well underway.

Conclusion

Railways are a vital piece of the supply chain and are usually a cost-effective and reliable way to get agricultural goods to their destination. Quarter three metrics show some signs of service improvements in terms of unfilled orders and rail speeds, though not enough to avoid slowdowns during harvest season. Lags in employment across railroads hinders the efficient movement of grain. Continuing rail service disruptions associated with these labor shortages, rail car inventory and capacity constraints, weather and other shortfalls put the profitability of many farms, ranches and agribusinesses at risk and contributes to uncertainty in already unsettled commodity markets.

Top Issues

VIEW ALL