Updated Supply and Demand Expectations for Corn and Soybeans in 2017/18

photo credit: AFBF Photo/Morgan Walker

John Newton, Ph.D.

Vice President of Public Policy and Economic Analysis

Third Time’s a Charm

USDA’s May 10, 2017, World Agricultural Supply and Demand Estimates (WASDE) provided the third round of corn and soybean balance sheet estimates for the 2017/18 marketing year. The first two balance sheet projections were provided in February 2017's USDA Agricultural Projections to 2026 and at USDA’s 2017 Agricultural Outlook Forum.

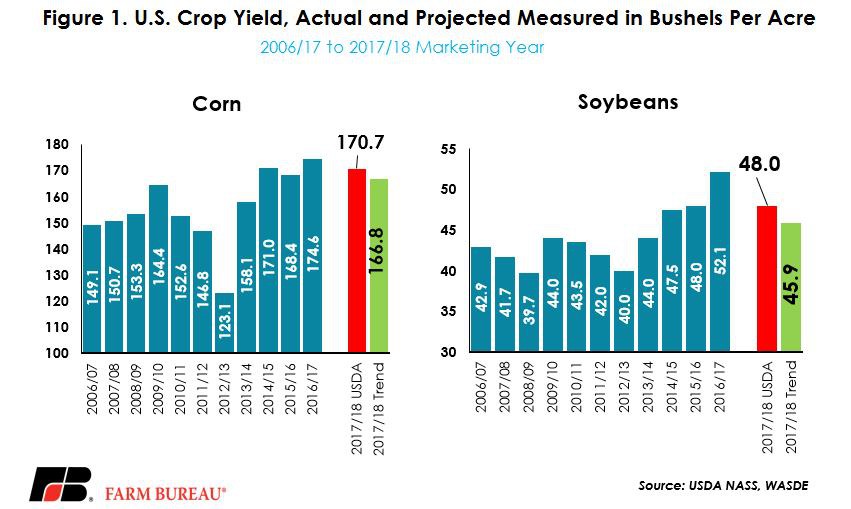

For the 2017/18 marketing year, corn yields are projected at 170.7 bushels per acre, down 3.9 bushels from last year’s record-high of 174.6 bushels per acre, but 3.9 bushels above a linear trend yield. Total production, based on USDA’s March 31 Prospective Plantings report, is projected at 14.1 billion bushels, down 7 percent from the prior year's levels.

Corn consumption is also projected to be lower in 2017/18 at 14.3 billion bushels, down 2.4 percent from the current marketing year. Finally, projected ending stocks are 2.1 billion bushels and would be down 8 percent from estimates of 2016/17 ending stocks levels. New-crop corn prices are projected to remain unchanged at $3.40 per bushel.

Soybean yields were projected at 48 bushels per acre, down 4.1 bushels from last year’s record of 52.1 bushels per acre, and 2.1 bushels above a linear trend yield. Despite prospective plantings of 89.5 million acres, total production is forecast at 4.255 billion bushels, down 52 million bushels from last year’s record crop. The lower production estimate is due to lower estimates for 2017/18 soybean yields.

Consumption of soybeans is expected to climb by 142 million bushels to a record 4.2 billion bushels. Despite record-high consumption, 2017/18 ending stocks are projected to climb by 45 million bushels from estimates of the current year’s carryout. New-crop soybean prices are projected to be down 25 cents per bushel to $9.30.

These Projections Will Change

Importantly, these estimates are subject to change. The 2016/17 marketing year does not end until the end of August, and old-crop corn and soybeans will continue to find homes as ethanol, crush, animal feed, or in the export market. Consumption of the old-crop above those currently projected will lower the carryout for the 2016/17 marketing year.

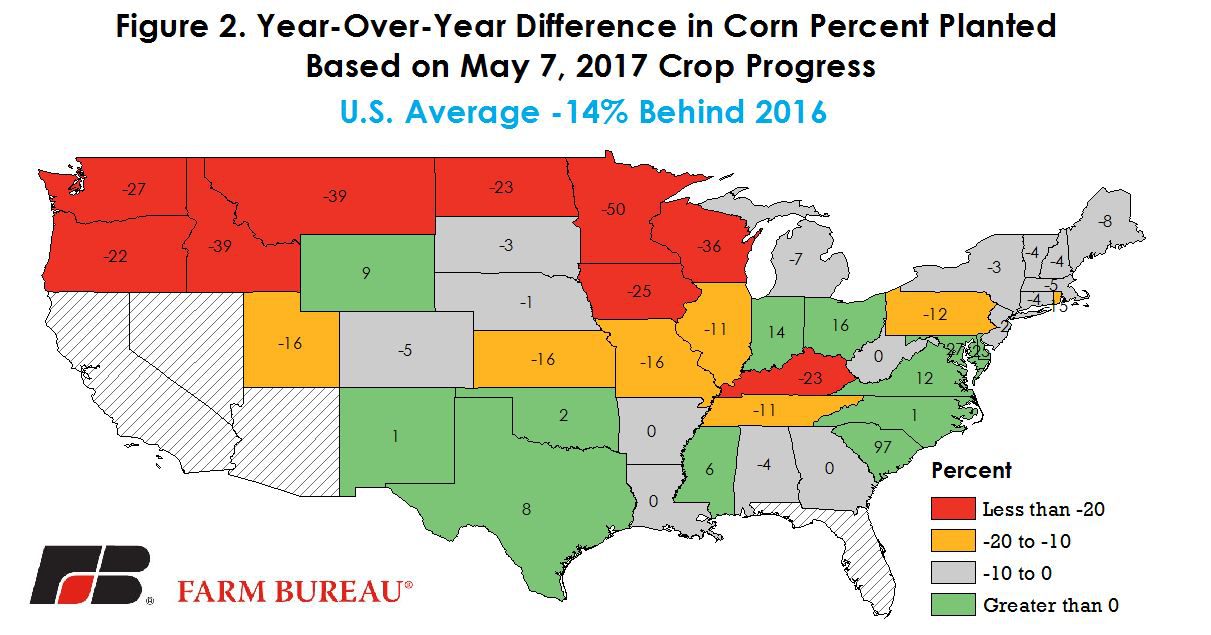

Crop yields and actual plantings will also change rapidly due to weather conditions. At this point in the growing season, only early-May planting progress data is available. In a recent Market Intel article, Corn Planting is Stalled in the Midwest, the planting delays due to excessive rainfall were noted. These delays have continued and led to much slower planting in parts of the U.S., especially in Iowa and the Upper Midwest, Figure 2.

USDA’s May 8, 2017, Crop Progress report revealed 47 percent of the corn crop and 14 percent of the soybean crop had been planted as of May 7, 2017. For corn, the pace of planting was 14 percent behind last year’s level and 5 percent below the 5-year average. Soybean plantings were 7 percent below last year and 3 percent below the 5-year average pace.

For every percentage point of mid-May planting progress, USDA’s weather-adjusted trend yield model suggests corn yield will increase 0.289 bushels per acre, holding all else constant. This is due to the impact of earlier planting on providing sufficient moisture and avoiding heat stress. Thus, continued delays in plantings could adversely impact corn yields, or change actual planting decisions.

USDA’s weather-adjusted crop yield model is updated monthly by the Economic Research Service through July. In the coming months, data on temperatures and precipitation will provide for more accurate weather-adjusted crop yield forecasts – adjusting production estimates along the way.

USDA’s June 30, 2017, Acreage report will provide the first survey-based estimate of actual plantings. Then, USDA’s August Crop Production report will provide the first survey-based estimate of corn and soybean yields and production for the U.S.

The pace of consumption will also play a role in the supply of corn and soybeans during the 2017/18 marketing year. Higher or lower use in export or domestic channels will change ending stock levels and price expectations.

USDA Forecast Accuracy

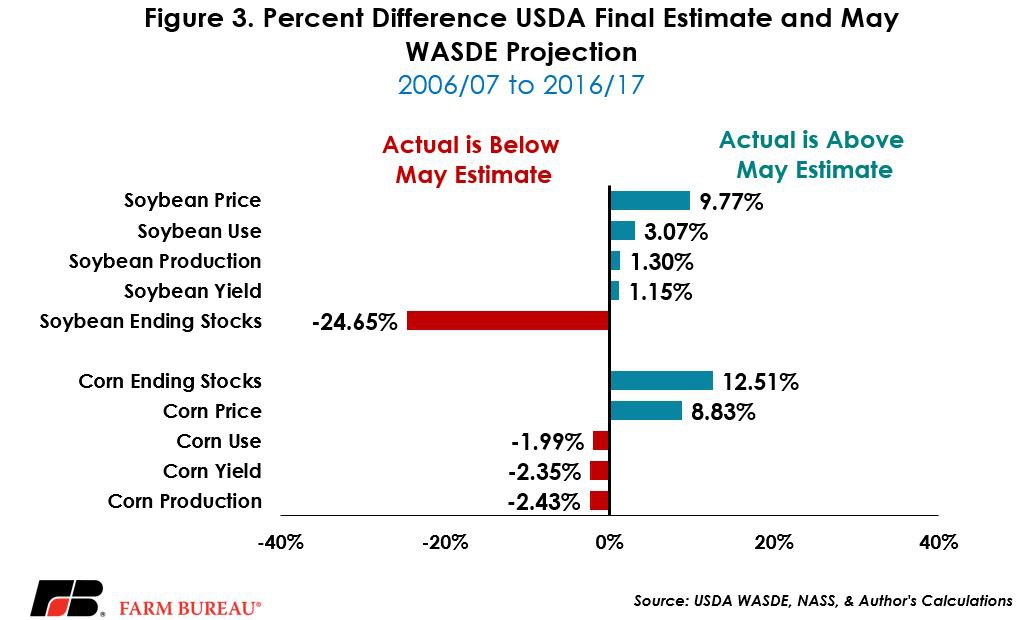

Final supply and use data for new-crop corn and soybeans remains uncertain. USDA’s monthly projections provide an opportunity for farmers, ranchers and agribusinesses to make informed decisions – so the accuracy of USDA’s projections is important.

Over the last decade, a review of USDA’s May projections for supply and use reveals a small margin of error for many categories. On average, only ending stock levels have a margin of error in absolute value greater than 10 percent, Figure 3. Soybean ending stocks have been significantly overestimated during the last decade on the back of continued improvements in demand from the world’s largest importer – China.

Sure, USDA does not always get it right, but forecasting a corn and soybean supply chain worth nearly $100 billion dollars in farm cash receipts is no easy task.

Top Issues

VIEW ALL