USDA Cold Storage Survey’s Importance to Livestock Producers

TOPICS

USDA

photo credit: Right Eye Digital, Used with Permission

Bernt Nelson

Economist

Cold storage, particularly for red meat and poultry, is an important part of the protein supply chain. Meat in cold storage comes from a variety of sources and is used in both domestic and global markets. USDA’s National Agricultural Statistics Service (NASS) releases the Cold Storage survey near the 22nd of each month. As of May 31, USDA’s June survey estimates red meat in storage was 1.087 billion lbs., down only slightly from April, but 20% greater than this time last year. This Market Intel will address common questions surrounding the USDA Cold Storage survey and what the USDA Cold Storage survey means to livestock farmers and ranchers.

What is it & how does it work?

The USDA Cold Storage survey measures reserve food supplies held in commercial and public warehouses. More specifically, the survey collects data from over 800 commercial and public refrigerated warehouses in 48 states that store products at or below 50 degrees Fahrenheit for 30 days or more. The survey, mailed out around the 24th of each month, collects data on around 150 items including dairy products, fruits, nuts, vegetables, poultry and red meat. All stocks in this survey represent “end of the month” numbers. This means that the June report represents inventory in cold storage on May 31. All late responses to the survey are included in the following month’s report. This means data for April in the June report may be different than the May report because of additional information.

The survey does not include stocks held in space maintained by wholesalers, jobbers, distributors, chain stores, locker plants containing individual lockers, meat packer branch houses or frozen food processors whose entire inventories are turned over more than once a month. NASS does not differentiate between commodities owned by a manufacturer, producer, wholesaler, retailer or government entity, or between domestically produced and imported.

What does it mean?

Data from this survey can be used for a variety of purposes by consumers, commodity producers and economists and analysts. One way it can be used is to analyze historical supply and demand for both the domestic and global markets.

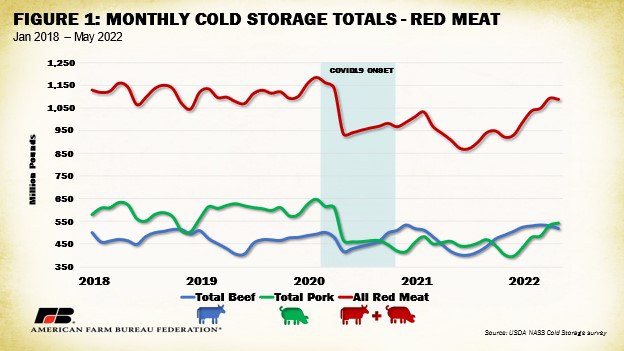

USDA defines frozen red meat as beef, pork, veal, lamb and mutton, and “other” red meat. In the May survey, which reports data from the previous month, USDA estimated 1.089 billion lbs. of red meat in storage, 16% greater than April 2021, and 4% above the previous month. Total frozen red meat inventory then decreased through May, but only slightly. Additionally, frozen beef stocks, a portion of red meat inventory, dropped 2% in May, but were still 25% above this time last year. Likewise, pork stocks rose 2% in May and are estimated to be 17% greater than this time last year.

Figure 1 illustrates the monthly cold storage totals for beef, pork and red meat between Jan. 1, 2018, and May 1, 2022. Figure 1 also illustrates a drop in red meat during the onset of the COVID-19 pandemic and the rise in 2022. During the pandemic, many meat processing plants were shut down. When this happened, persistent consumer demand began eating away at meat in cold storage as a substitute for more recently processed products.

What caused cold storage numbers to recover in 2022?

Many factors can contribute to the increase in inventory between 2021 and 2022. A primary indicator is red meat consumption. Retail prices for red meat and poultry have increased in 2022. USDA-Economic Research Service (ERS) Consumer Price Index Forecast indicates that the average price paid for a representative market basket of meat has increased by 12.3% between May 2021 and May 2022. As a result, per capita disappearance of red meat and poultry is forecast to decrease in 2022 as consumers opt for cheaper options in the store. The impact of Americans consuming less meat and poultry is increased meat in cold storage.

A second factor is the global market. Historically, China has been a major importer of both U.S. beef and pork. In fact, China was the number three importer of U.S. beef in 2021 and is on track to increase beef imports for 2022. In recent years, however, China is importing considerably less pork. The value of pork imported by China fell 26% between 2020 & 2021 while the value of U.S. pork imported into Mexico simultaneously increased by 45%. This dropped China from the number one importer of pork in 2020, to number four by the end of 2021.

During the pandemic China increased its imports of U.S. beef and pork. This was in part because China’s hog population was damaged by African Swine Fever. As a result of increased Chinese imports, to make up for their reduced domestic production, U.S. cold storage numbers fell. More recently, China has been able to rebuild its hog population and now imports less pork while remaining an active importer of U.S. beef. The decrease in China’s U.S. pork imports has resulted in less pork being removed from cold storage, allowing stored volume to steadily recover.

Summary and Conclusions

There is a combination of factors globally and on the domestic front that can contribute to the movement of red meat and poultry in cold storage. When plants shut down during the pandemic, more frozen products were consumed as live animals could not be readily processed. In China, a top importer of U.S. meat and poultry, COVID-19 and African Swine Fever lead to lower than usual domestic pork supply, which pressured international pork stocks and contributed to a drop in U.S. cold storage rates between mid-2020 and early 2021.

So far in 2022, cold storage has been on the rise. Processors have been able to remain open for business more consistently than during the pandemic. Consumers face rising prices at the grocery store and are, correspondingly, purchasing less meat. Additionally, China has re-built its hog population and is importing less U.S. pork.

These factors all contribute to the complexity of supply and demand in meat and poultry markets. Thankfully, the USDA Cold Storage survey is a tool that can illustrate change in the market. Farmers and ranchers can use cold storage inventory numbers to make better decisions related to demand for their product.

Top Issues

VIEW ALL