2020/2021 Marketing Year Outlook Remains Foggy

TOPICS

Wheat

photo credit: Arkansas Farm Bureau, used with permission.

Shelby Myers

Former AFBF Economist

The May World Agricultural Supply and Demand Estimates is the highlight of spring reports as it gives the first look at the 2020/2021 marketing year since projections were announced in February at the USDA Agricultural Outlook Forum. Farmer planting decisions are incorporated from the March Prospective Planting report and planting progress reports are updated weekly throughout the spring. Top of marketers’ and analysts’ minds is how commodity markets will react to the COVID-19 uncertainty. This Market Intel breaks down the May WASDE as USDA tries to put into context the COVID-19 impacts.

Corn

2020/2021 corn acres planted are estimated at 97 million acres, up 8% from 2019 when producers planted 89.7 acres. USDA forecasts farmers will harvest 89.6 million acres of corn in 2020 at a yield rate of 178.5 bushels per acre.

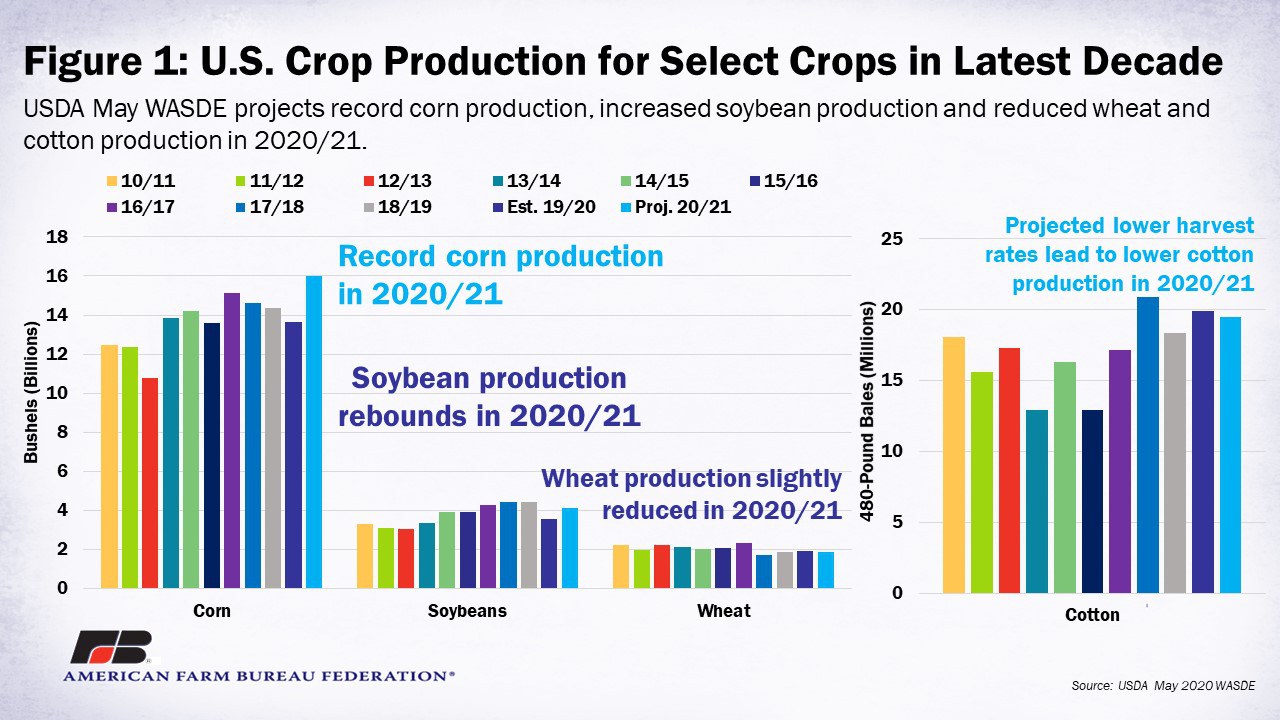

At that rate, corn production for 2020/2021 could come close to a record 16 billion bushels. It would also be 17% more corn than the 13.7 billion bushels produced in 2019, the lowest production level since 2015.

On the demand side, during the 2019/2020 marketing year, USDA estimated a reduction in ethanol use of 475 million bushels from March to May as COVID-19 slowed ethanol consumption for about two months. Month-to-month, USDA estimates ethanol consumption to be 100 million bushels lower from April to May. Ethanol use of 4.95 billion bushels represents a 12% reduction in ethanol use compared to 2018. The drop in ethanol consumption has the largest demand impact for 2019/2020 and pushes corn ending stocks above 2 billion bushels, a 206-million-bushel increase from the March WASDE, which was released before COVID-19 really took hold. Corn stocks before COVID-19 were projected to be 1.7 billion bushels. As a result of the drop in demand and higher corn ending stocks, USDA dropped its estimate for the marketing year average price to $3.60 per bushel, down from the $3.80 per bushel the department estimated in March.

Moving into the 2020/2021 marketing year, USDA is projecting record corn planting and record supplies totaling 18 billion bushels. Though it is estimated that ethanol production will return to 5.2 billion bushels for the 2020/2021 marketing year and corn exports will rise above 2 billion bushels, the demand estimates do not use up enough expected corn supplies, leaving ending stocks for 2020/2021 at 3.3 billion bushels. This puts even more downward pressure on the price of corn, which USDA estimates to be $3.20 per bushel for 2020/2021.

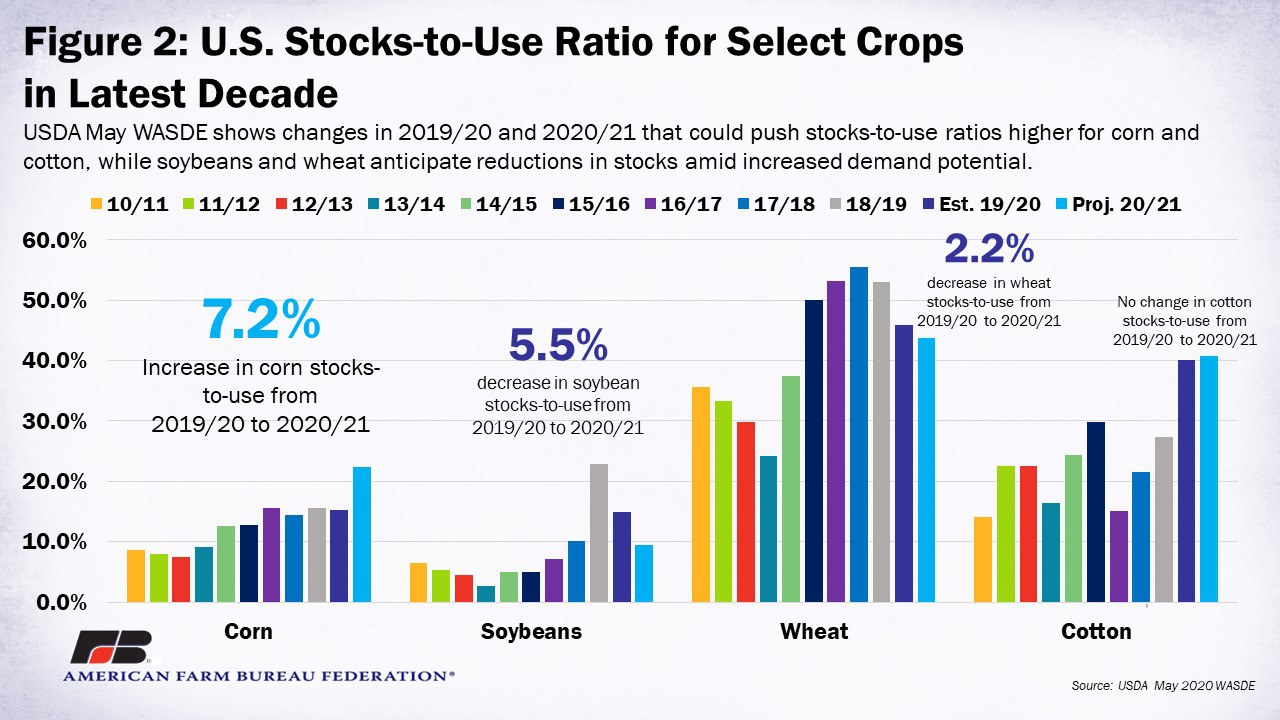

The 2019/2020 stocks-to-use ratio for corn is projected at 15.2%, which is in line with the 2018 stocks-to-use ratio of 15.5%. Heading into 2020/2021, current estimates put the stocks-to-use ratio for corn higher at 22.4%.

Soybeans

Farmers are expected to plant about 83.5 million acres of soybeans in 2020/2021, up 9.7% from 2019 when farmers planted 76.1 million acres. With an estimated yield of 49.8 bushels per acre, soybean production in 2020/2021 is projected to be 4.1 billion bushels, up 16% from 2019/2020.

With lower production in 2019/2020, soybean ending stocks are estimated to be 580 million bushels, cut nearly in half from 2018 when ending stocks were 909 million bushels. With stocks carrying over into 2020/2021 and soybean production anticipated to rebound, supplies are expected to increase. Soybean supplies for 2020/2021 are expected to reach 4.72 billion bushels, up 5% from 2019/2020 supplies of 4.48 billion bushels

2020/2021 demand is expected to increase as well. U.S. soybean crush is up 5 million bushels in 2020 compared to 2019 with expectations of increased domestic demand for soybean use. The anticipated crush rate of 2.125 billion bushels makes this the third consecutive year that soybean crush will be above 2 billion bushels.

Soybean exports in 2020/2021 are estimated at 2.05 billion bushels, up from 1.675 billion bushels in 2019/2020. The increase shows optimism that trade will return to normal and the completed Phase 1 agreement signed in January will spark more exports to China. It is anticipated that U.S. exports to China could begin accelerating as the new crop is harvested later this year.

An overall lowering of soybean stocks is expected to occur once again in 2020 as demand picks up and supplies rebound from 2019. Ending stocks in 2020/2021 are projected to be 405 million bushels, down from 580 million bushels in 2019. The 2019/2020 stocks-to-use ratio for soybeans is projected at 15%, compared to 23% in 2018, while current projections for 2020/2021 put soybeans on pace for a stocks-to-use ratio of 9.4%.

Figure 1 displays U.S. crop production for corn, soybeans, wheat and cotton over the past decade, including the new 2020/2021 projections.

Wheat

Wheat planted acres in 2020/2021 are anticipated to be just slightly lower than 2019/2020 planted acres at 44.7 million acres, down 1% from last year. Yield is estimated to be 49.5 bushels per acre and wheat production could reach just above 1.8 billion bushels, about 2% below 2019/2020 wheat production of 1.9 billion bushels.

Wheat demand in 2019/2020 had an unexpected uptick during COVID-19 as a flurry of grocery store purchases of wheat products increased the estimate for 2019/2020 food use by 7 million bushels. However, 2019/2020 wheat exports were also revised downward by 30 billion bushels.

Revisions in 2019/2020 wheat demand pushed ending stocks 8 million bushels higher for the 2019/2020 marketing year to 978 million bushels. Along with an expected reduction in production, USDA also anticipates an increase in imports for the 2020/2021 marketing year, moving from 105 million bushels in 2019/2020 to 140 million bushels. Total supplies of wheat for 2020/2021 are estimated to be 2.98 billion bushels, down almost 4% from 2019/2020.

Marginal changes are expected for wheat-related food and seed demand for 2020/2021, but a 35-million-bushel reduction in feed and residual from 2019 is expected. The overall changes in domestic wheat demand move domestic wheat use from 1.157 billion bushels in 2019/2020 to 1.125 billion bushels in 2020/2021.

Wheat export expectations are reduced by 20 million bushels from 2019/2020, holding at 950 million bushels for the 2020/2021 marketing year. The reduction in demand is met with a reduction in production, which lowers ending stocks to 909 million bushels, 7% lower in 2020/2021 than the 978 million bushels in 2019/2020. At $4.60 per bushel, price expectations for the 2020/2021 marketing year remain similar to 2019/2020. The 2019/2020 stocks-to-use ratio for wheat is projected at 46%, which is lower than 2018/2019’s 53%. USDA estimates the 2020/2021 stocks-to-use ratio will go even lower, to 44%.

Cotton

Cotton planting expectations for the 2020/2021 marketing year mirror the prior year’s estimates. Cotton farmers are projected to plant 13.7 million acres of cotton in 2020/2021, as they did in 2019/2020. USDA anticipates a slight yield bump for the new crop but offsets the production estimate with fewer harvested acres. While cotton yield is estimated to reach 825 pounds per acre in the 2020/2021 marketing year, up from 823 pounds per acre in 2019/2020, farmers are expected to harvest only 11.35 million acres of cotton in 2020. This would be slightly lower than the 11.6 million acres harvested in 2019.

Demand for cotton, both global and domestic, declined in the final stretch of 2019/2020. USDA revised the 2019/2020 estimate of domestic use even lower from April’s estimate of 2.9 million 480-pound bales to 2.7 million 480-pound bales in May. Cotton exports in May for 2019/2020 remain at the 15 million 480-pound bales from USDA’s April estimates, which was down from the 16.5 million 480-pound bales USDA estimated in March. Total cotton use for 2019/2020 sits at 17.7 million 480-pound bales, almost equal to demand during the 2018/2019 marketing year.

With 2019/2020 cotton ending stocks as high as 7.1 million 480-pound bales and production estimates for 2020/2021 on that same track, cotton supplies in 2020/2021 are estimated to reach 26.6 million 480-pound bales, up 7.4% from 2019/2020.

The WASDE report indicates optimism for increased global demand for cotton in 2020/2021. Domestic use recovers to 2.9 million 480-pound bales in 2020/2021 and exports jump to 16 million 480-pound bales. Total use of cotton in 2020/2021 is estimated to be 18.9 million 480-pound bales, up 6.7% from 2019/2020.

Despite the recovery in cotton demand, the large supply estimates push 2020/2021 ending stocks to 7.7 million 480-pound bales, similar to ending stocks in 2019/2020. These hefty stocks weigh heavily on the 2020/2021 average marketing year price, which USDA puts at 57 cents per pound, 2 cents lower than the 2019/2020 marketing year average price. The 2018/2019 stocks-to-use ratio was 27.3%, but in 2019/2020, the stocks-to-use ratio for cotton rose to 40.1% and is projected at a similar level, 40.7%, for 2020/2021.

Figure 2 displays the U.S. stocks-to-use ratios over the past decade for corn, soybeans, wheat and cotton, including the 2020/2021 projections.

Summary

The May WASDE is the long-awaited first look at the upcoming marketing year. Like the first day of school, the report is greeted with hope and expectation. This May WASDE is very different from any previous reports as COVID-19 continues to force surprise revisions to the old crop estimates and the exchange of commodities is in flux. Farmer planting decisions will not be updated until the June 30 acreage report. With the estimated large production of corn and cotton and the potential to change planting intentions, there could be possible supply revisions for the 2020/2021 marketing year early on. Additionally, more demand changes in 2019/2020 could be on the docket as stay-at-home orders and continued COVID-19 precautions remain in place.

Top Issues

VIEW ALL