A Hot Summer – and Even Hotter Red Meat Demand – Forecasted

TOPICS

PorkMichael Nepveux

Former AFBF Economist

photo credit: Right Eye Digital, Used with Permission

Michael Nepveux

Former AFBF Economist

Summer 2021 will be remembered for many things: the summer where we as a society collectively emerged from lockdowns, the summer of the Brood X cicada invasion (at least in the Eastern U.S.), and the summer where red meat markets took off. Okay, maybe only people who live and breathe the animal protein complex will remember that last fact in 10 years, but high meat prices are certainly raising eyebrows in grocery stores and restaurants and around family dinner tables. The biggest culprit here is robust beef and pork demand, which is pushing wholesale beef and pork prices to historic levels. Couple this with a recent cyber attack targeting one of the largest meat processors in the U.S. and we have quite a bit to delve into in this Market Intel.

Beef

The exceedingly healthy beef market demand in 2021 has not quite trickled down the supply chain to the producer. Fed cattle markets have been fairly lackluster, while healthy domestic and export demand have driven the boxed beef cutout to record levels. Packing plants have been hampered by an increasing labor shortage problem that has made it difficult to run plants that are already operating at what can only be described as “hard” levels.

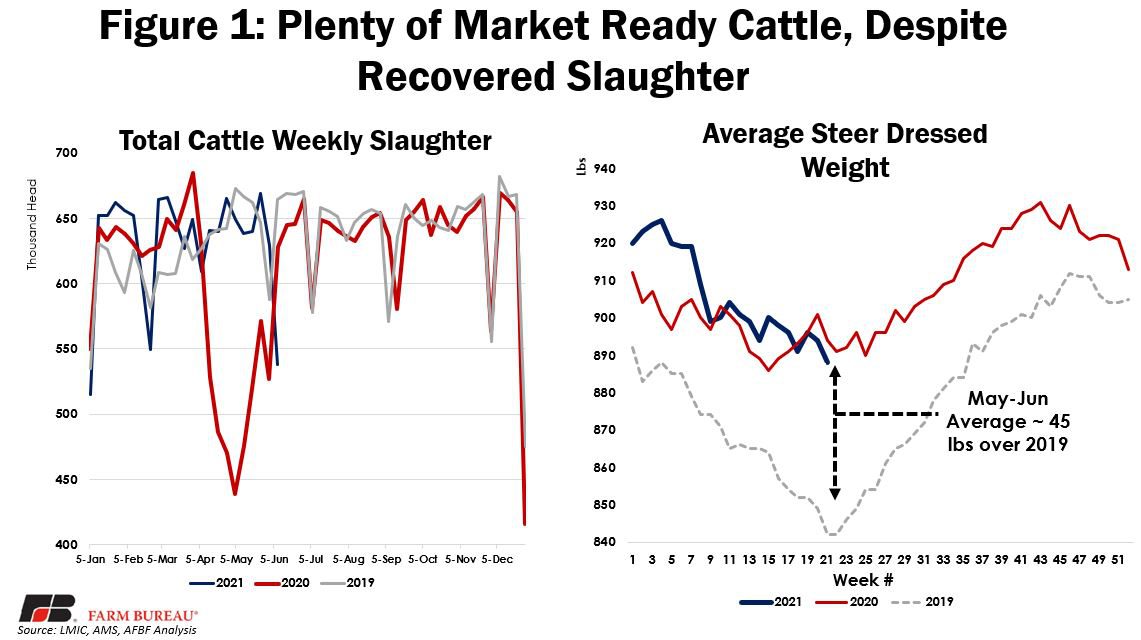

However, this is not a new issue that was created just by government stimulus during the pandemic; the difficulty of securing labor at packing plants has been an issue for years now. At the end of the day, working in a packing plant is an incredibly difficult job that requires a specialized set of skills -- two factors that will continue to place labor pressures on these employers even as they raise wages to attract workers. Figure 1 shows that in spite of these labor issues, total cattle slaughter has largely recovered from COVID-19 slowdowns and shutdowns and, except for a winter weather hiccup, has mostly remained above last year and above 2019. This figure also shows that dressed weights are not declining to the level that they usually would at this time of the year – an indicator of the backlog of cattle in the supply chain. This is likely a sign of cattle backing up in the system as we have more market ready cattle than current slaughter capacity available.

Perhaps a bigger story for cattle markets than the supply side is beef demand. So far, 2021 has been a story of rising beef prices supported by extremely healthy demand for beef. There are a variety of factors contributing to this, ranging from government stimulus to economies reopening. Grocery stores, food service and exporters are all competing for product. It certainly is true that this recession has been quite different than past recessions in that most analysts (including myself) were expecting a very difficult second half of 2020 for beef demand due to recessionary pressures. I am very happy to be proven wrong and report that we did not fully account for the ways in which this recession was different: many consumers remained employed while their spending decreased due to lockdowns, and government stimulus checks shored up the spending of those who did face employment difficulties. Another factor is that we are seeing much of the country move to reopening, which has prompted many food service establishments and restaurants to rush into the market to secure supplies for the pent-up demand that most are expecting. And finally, a potential wildcard is consumer preferences, meaning that consumers may have become much more comfortable with preparing a variety of cuts of meat without access to restaurants and we may see that preference lead to increased purchases. Simply put, due to changes in consumer preferences, we may even be in the early stages of witnessing a shift outward in the demand curve for red meat.

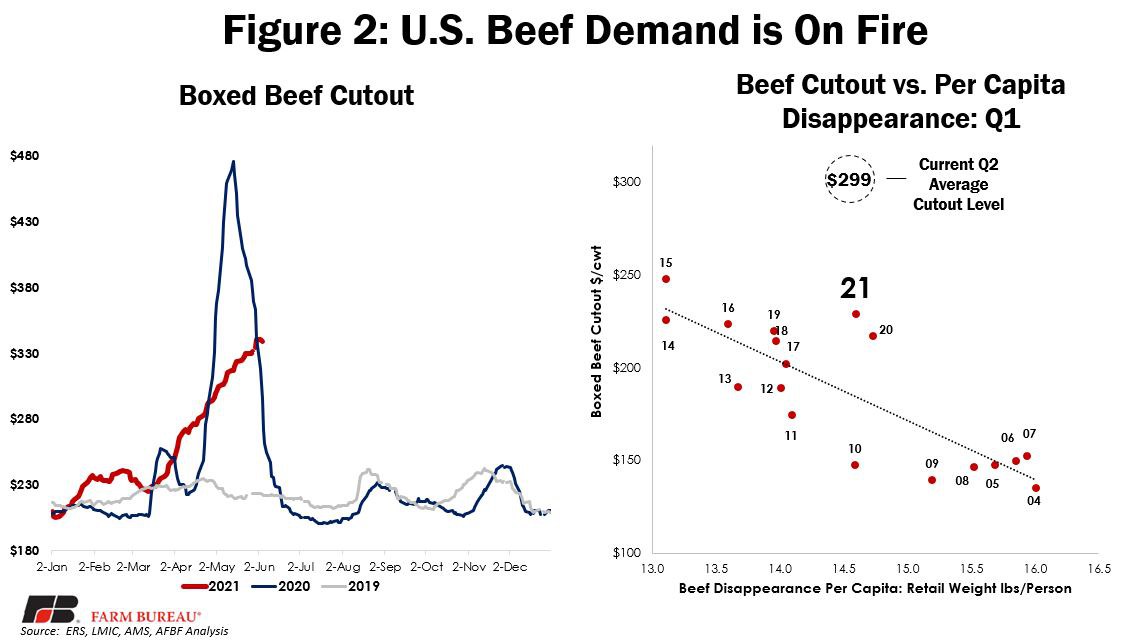

Figure 2 shows the historic (non-COVID-19) climb of the beef cutout as well as a comparison of beef disappearance per capita and the cutout. A simple way to interpret the scatterplot is that we experience a stronger beef market as we move upwards and to the right on the graph. This means that we are both consuming more beef per person and paying more for that beef. This particular graph is only looking at January-March averages of each variable for each year, but we seem to have had both high consumption and high prices in the first quarter of 2021, along with 2020. If we were to look at April-June cutout levels to date (we do not have disappearance data just yet), we can clearly see that regardless of where that disappearance number falls, we are on a completely new level when comparing to first quarter data. As we move throughout most of the summer, we can largely expect elevated prices to continue.

Pork

Similar to beef markets, demand for pork has been exceedingly healthy. The pork cutout has been steadily marching upward to historic highs and is now at levels not seen since the supply crunch of 2014 that was caused by PEDv. Many of the same reasons for the increase in beef demand apply to pork: food service sector restocking, economies reopening and higher levels of consumer savings/government support. High beef prices also can be supportive of pork prices, particularly in terms of retail demand. Pork has also experienced favorable exposure to export demand; however, that goes back some time and has less to do with COVID-19 and more to do with Southeast Asia’s protein deficit.

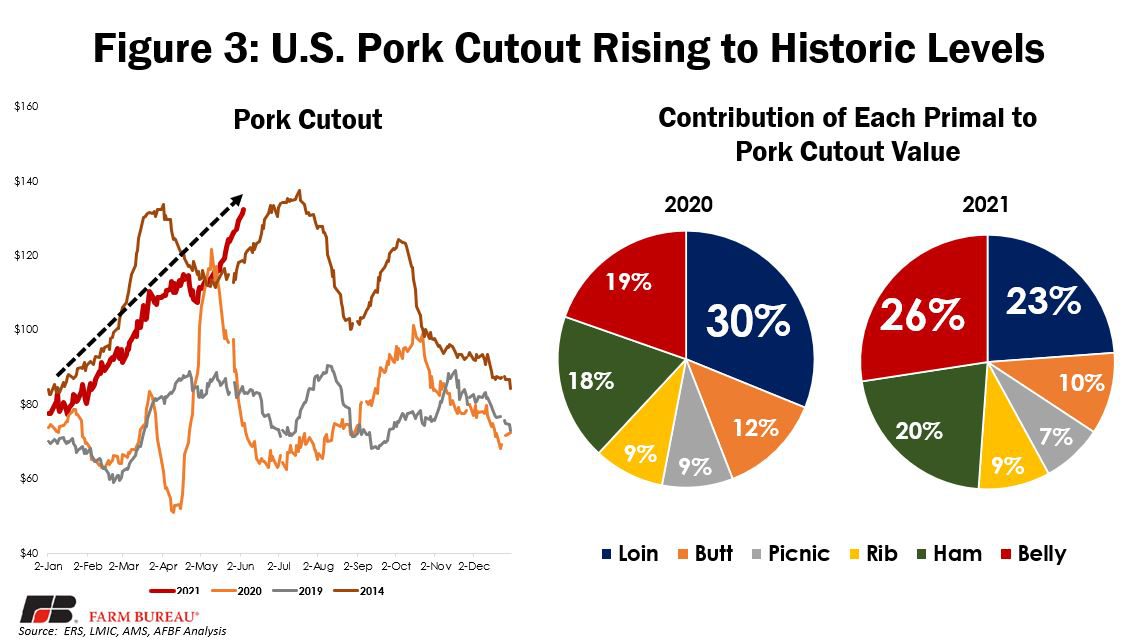

In addition to showing historic pork cutout levels, Figure 3 also shows the shift in the contribution to the cutout value by each of the primals for January-June. The story here mostly centers around a recovery in pork bellies and the share attributed to the loin primal. The share of the overall pork cutout that comes from bellies has increased from 19% in 2020 to 26% in 2021. After a two-three-week gully in late April-early May, pork bellies are largely back to their more robust levels. Granted, this time period comparison also includes the COVID-19-induced disruptions that resulted in a collapse in the belly market for the first half of April 2020. This shift in value toward the belly has largely come at the expense of the loin. Regardless of the share that each contributes to the cutout, levels have risen for all the major cuts throughout the first half of 2021.

JBS Hack Aftermath

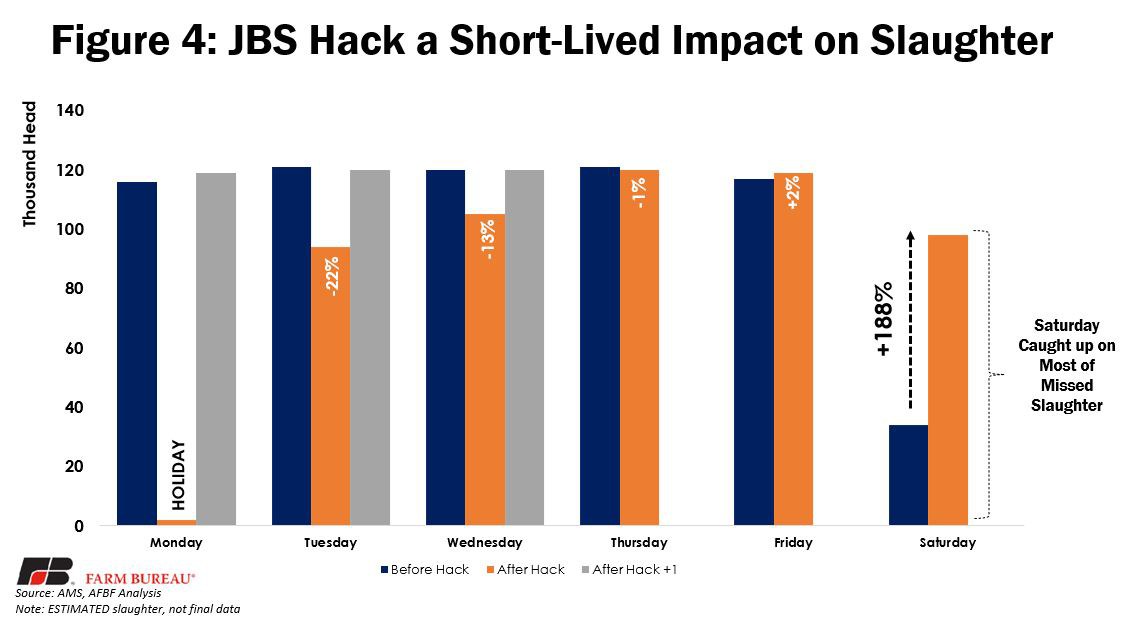

Anyone who glanced at a screen last week is probably aware of the fact that JBS, the largest beef packer and second-largest pork packer in the U.S., experienced a highly publicized hack. An immediate concern for most of the country was what the impact of this event would be on our supply of animal protein. News stories warning of an imminent meat shortage began to pop up and some worried about potential panic-buying, similar to the recent run on gas stations. While the company reportedly paid the hackers over $10 million in ransom, the impact to their slaughter plants was mostly short-lived. Figure 4 shows the national slaughter estimates for the week before, the week of and the week following the hack (for the days with data available). It is very important to note at this point that these numbers are estimates, and soon USDA will have the officially reported slaughter data.

It should first be noted that the Monday following the hack was a holiday, which makes doing any weekly comparisons unhelpful. Here we will need to examine the daily slaughter estimates to have a better idea of the impacts of the hack. The Tuesday following the hack, total U.S. slaughter estimates were showing a 22% decline when compared to the previous week. Industry estimates place JBS market share of U.S. slaughter capacity at 23%, which could imply that the hack did indeed take out all of JBS’ cattle slaughter plants. On Wednesday, the company indicated in a press release that it was working toward getting back online and that many (not all) of its plants were going to be operating at some capacity. This is supported by the national slaughter estimates, as slaughter levels increased on Wednesday, coming in at 13% below the previous week. Slaughter largely returned to normal on Thursday, with a 1% decline from the previous week, only to climb to a 2% increase on Friday. The national slaughter numbers dramatically increased on Saturday, more than just JBS could make up for. This is likely a response by packers to both the holiday on Monday as well as decreases in levels from the computer system hack. I suspect when we look back at this hack, we will see it as a short detour on the road to exceptional red meat demand throughout this summer.

Summary

The big takeaway from this Market Intel article is that beef and pork markets are hot this summer. When we saw the beef and pork cutouts spike last year as a result of COVID-19, many assumed it would be a long time before we saw beef and pork prices at those levels again. Fast forward just 12 months and we are seeing historic levels for both the beef and pork cutouts, except this time it is without the pandemic-induced decline in slaughter numbers. Normally I might be concerned about the impact that a surging cutout price has on consumers’ willingness to pay for the product, but the saving grace is prices for all proteins seem to be increasing, which may prevent one protein from gaining substantially at the expense of another. However, it is certainly worth asking if these prices are sustainable for the industry.

Top Issues

VIEW ALL