A Tale of Two Farm Incomes

TOPICS

Trade Assistance

photo credit: Getty Images

John Newton, Ph.D.

Vice President of Public Policy and Economic Analysis

USDA’s most recent Farm Income Forecast, released Feb. 5, predicted farm income to decline in 2020. USDA’s Farm Income Forecast also predicted farm income to increase in 2020. You read that right, USDA is projecting farm income in 2020 to both rise and fall.

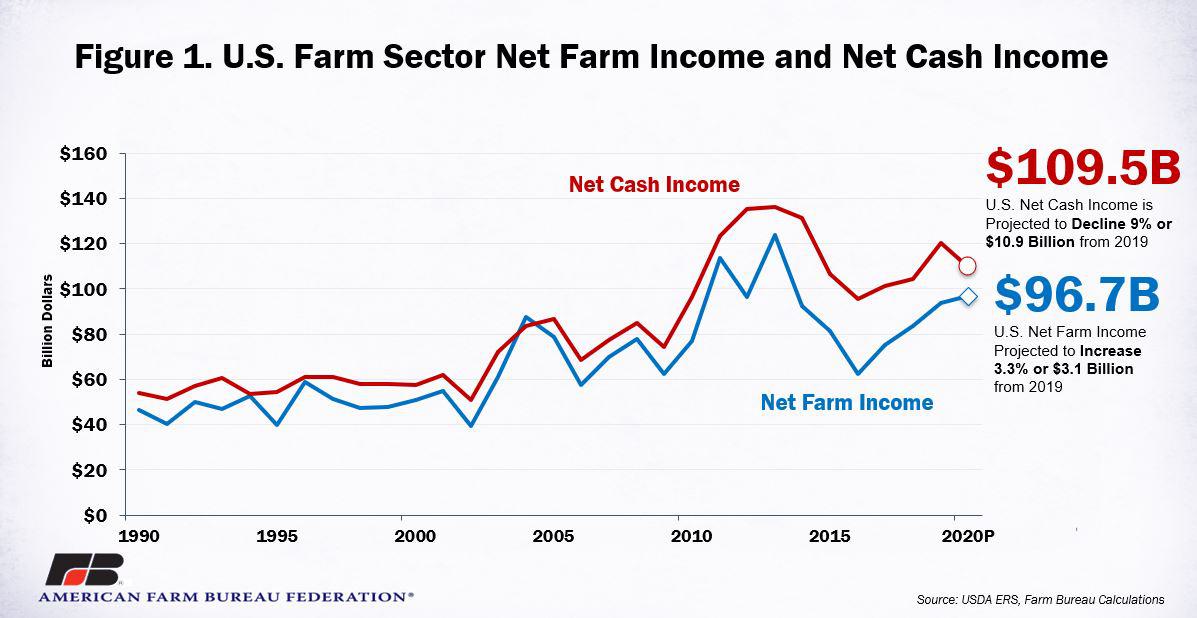

U.S. net farm income, a broad measure of farm profitability, is currently forecast at $96.7 billion, up 3.3%, or $3.1 billion, from the prior year. If realized, net farm income in 2020 would represent the fourth consecutive year of higher net farm income and would be 55% higher than the decade low of $62 billion in 2016. However, it would remain 22% below 2013’s high and would be only slightly higher than the 20-year inflation-adjusted average of $93 billion.

U.S. net cash income, which does not include adjustments such as depreciation, non-money income related to farm-level consumption of the farm’s own production or inventory adjustments that transfer the value of inventory across tax years, is currently forecast at $109.5 billion, down 9%, or $10.9 billion, from 2019. Figure 1 highlights U.S. farm sector net cash income and net farm income.

The divergence of the two measures does not happen often – twice in the last 20 years – but it is primarily related to how sales of inventory are treated. For example, during the short crop year of 2019, farmers likely sold products from the prior year’s inventories. Since net cash income is based on the year in which the sales occur and net farm income is based on the year the production occurred, the inventory adjustment changes total gross income and net farm income for the production year. The inventory adjustment during 2019 totaled -$14.5 billion – the largest since 2012’s -$20 billion -- and in 2020 is forecast at $350 million.

Trade Aid Leaves a Big Hole in Farm Income

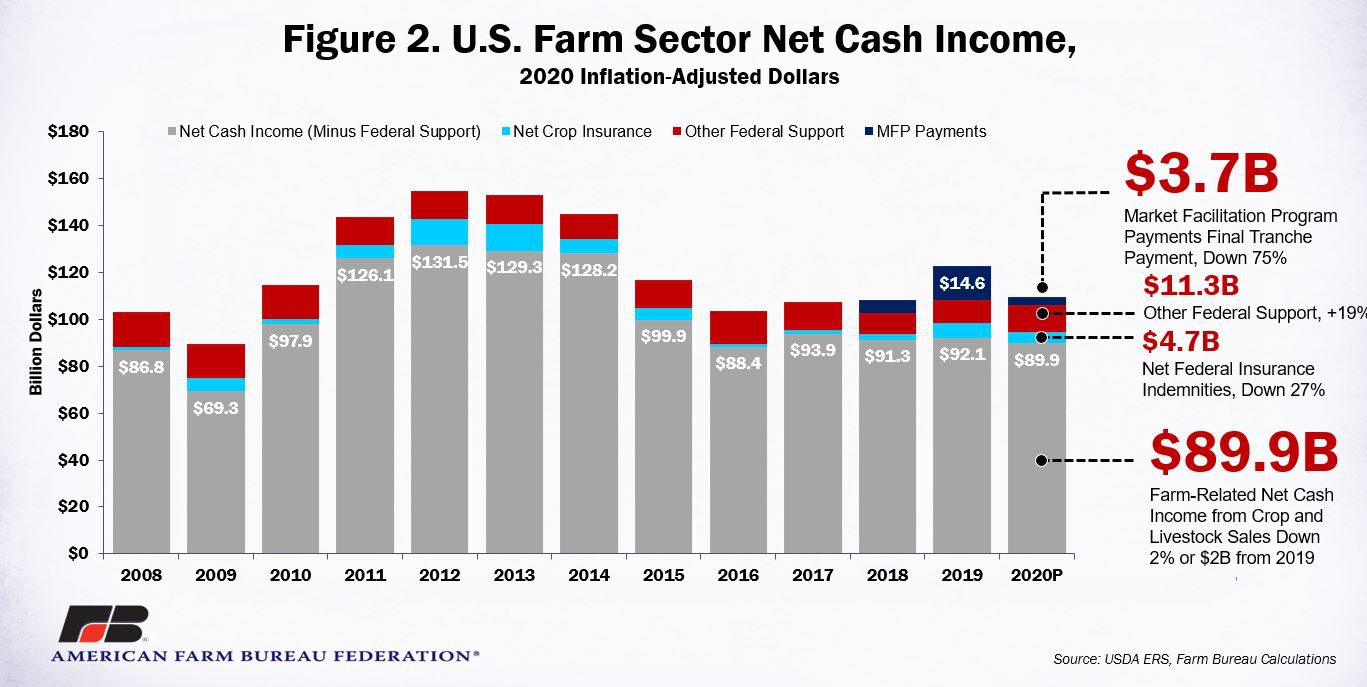

During 2020, cash receipts from crop and livestock sales are projected at $384.4 billion, up 2.7%, or $10.1 billion, from 2019. A majority of the increase in cash receipts is driven by higher livestock sales, which at $185.8 billion are up 5%, or $8.2 billion, from 2019. Cash receipts from crops are forecast at $198.6 billion, up $1.9 billion, or 1%, from the prior year. The higher crop and livestock cash receipts do not fully offset the loss in federal government payments. During 2019, the federal government paid $14.6 billion, in inflation-adjusted dollars, to farmers impacted by retaliatory tariffs, according to USDA’s Economic Research Service. The final tranche of Market Facilitation Program payments (China and MFP Tranche 3) was distributed in February 2020 and is forecast at $3.7 billion, down 75%, or nearly $11 billion, from 2019. Combined, gross cash income in 2020 is forecast at $430.9 billion, down $1.3 billion, or one-third of 1%, from 2019.

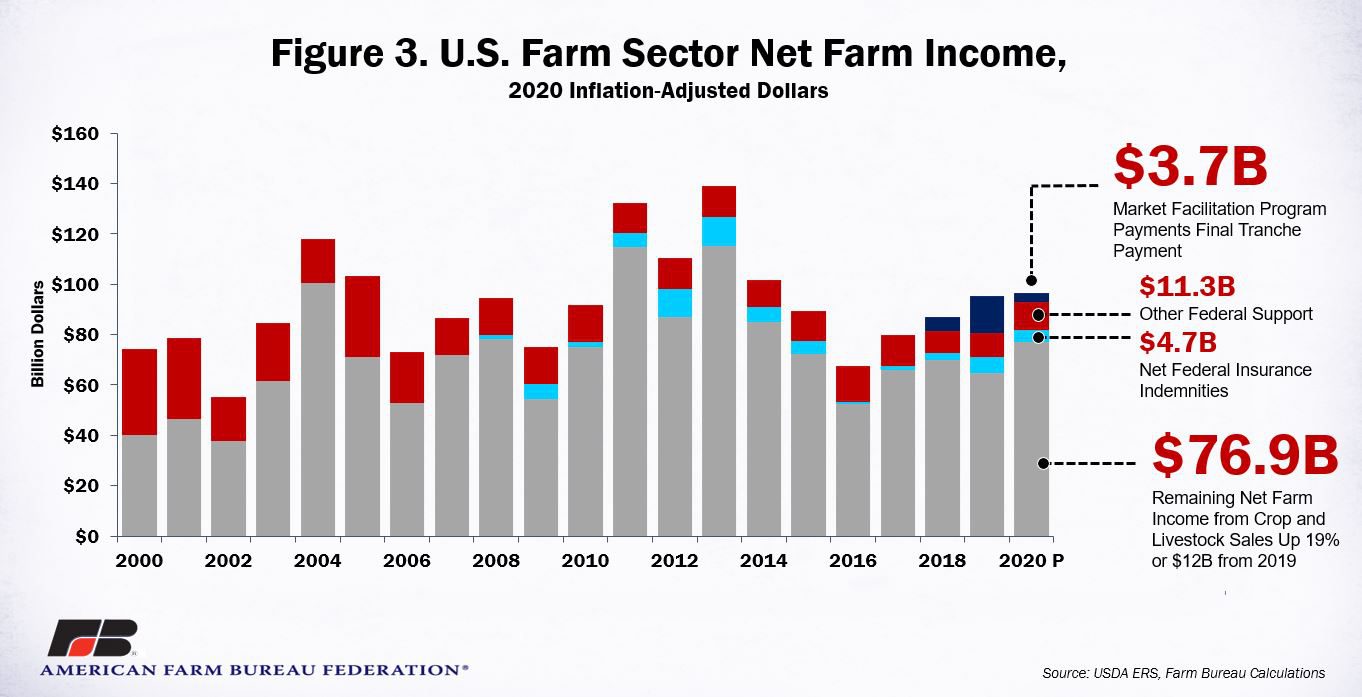

When removing trade support, net federal crop insurance indemnities and other federal support, i.e., farm program risk management and conservation programs, the remaining net cash income totaled $89.9 billion, down 2%, or $2 billion, from 2019. If realized, the remaining net cash income would be the second lowest over the last decade, behind only 2016’s $88.4 billion and $18 billion below the 10-year average. Similarly, after factoring in the smaller inventory adjustment for 2020, the remaining net farm income value was $76.9 billion, up 19% percent, or $12.2 billion, from the prior year in inflation-adjusted dollars. Figures 2 and 3 highlight farm profitability indicators along with other sources of income.

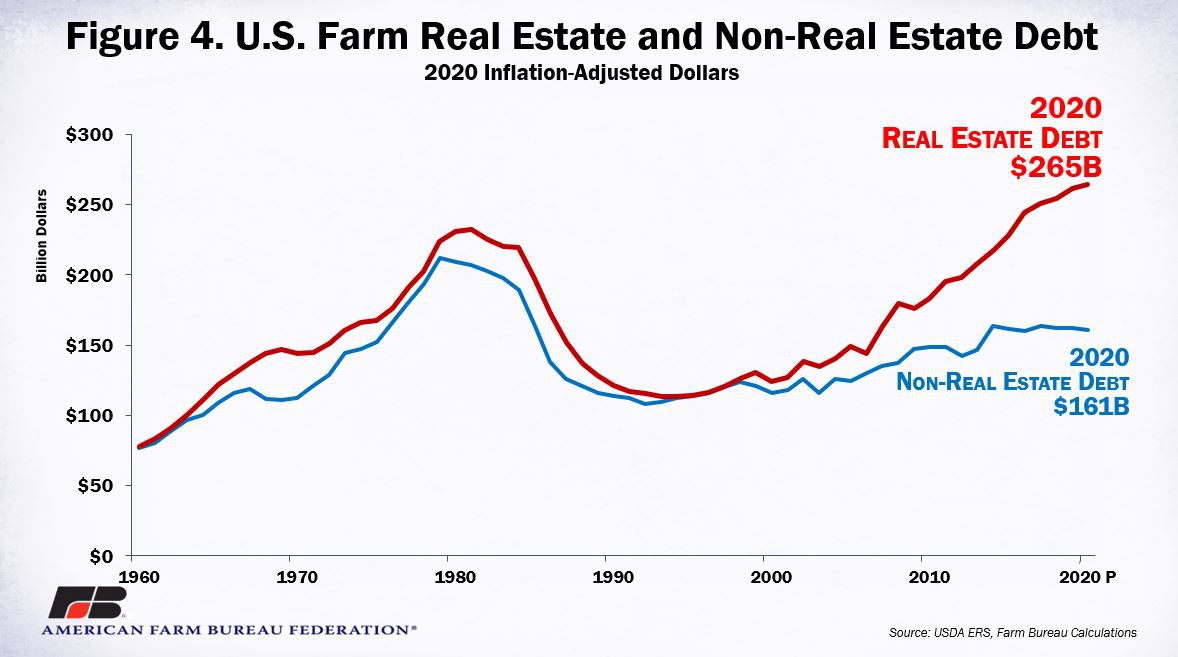

Record-High Farm Real Estate Debt

For 2020, USDA is forecasting farm debt to reach $425 billion – a record in nominal dollars. If realized, farm debt in 2020 would be up 2.3%, or $9.7 billion, from prior-year levels. In inflation-adjusted dollars, total farm debt would be $15 billion shy of the $440 billion record, set in 1980. While total farm debt remains below inflation-adjusted highs, real estate debt in 2020 is forecast at $265 billion, an all-time high in both nominal and real terms. That’s $33 billion higher than 1981’s $232 billion and up $8 billion, or 3%, relative to 2019 in nominal terms. Non-real estate debt is forecast at $161 billion, up $1.6 billion, or 1%, from 2019. In inflation-adjusted dollars, non-real estate debt actually declined from 2019 by $1.3 billion, or 1%.

One interesting trend that emerged in 2014 is a plateauing of non-real estate debt, in inflation-adjusted dollars, and a rapid increase in real estate debt. Since 2014, real-estate debt, in inflation-adjusted dollars, climbed 22%, while non-real estate debt fell by 2%. One likely cause of the rising real estate debt and flat non-real estate debt, other than rising agricultural land values, is the prevalence of farmers refinancing short-term and higher-interest loans or dealer financing into long-term debt, i.e., farm real estate. Of course, there is a risk that the underlying asset, i.e., farmland, could be liquidated, should the farmer default on the debt. Figure 4 highlights farm real estate and non-real estate debt.

Summary

USDA’s recent farm income forecasts farm sector profitability to both rise and fall in 2020. Cash receipts for crops and livestock are expected to increase in 2020 to $384.4 billion, but their increase does not fully offset the $11-billion decline in Market Facilitation Program benefits. Net cash income is projected at $109.5 billion, down 9%, or $10.9 billion, from the prior year. Meanwhile, net farm income, a broader measure of farm profitability that includes factors such as optional inventory adjustments, is forecast at $96.7 billion, up $3.1 billion, or 3.3%, from 2019. The divergence of the two profitability measures is due to a $14 billion adjustment in inventory made during 2019.

While farm profitability is mixed, farm debt is not. At $265 billion, farm real estate debt is projected to reach a record high in 2020 and total farm debt is forecast at $425 billion. A portion of the rising real estate debt may be attributable to farmers rolling short-term debt into longer-term debt, thereby increasing total real estate debt.

No matter which farm income forecast you follow, one thing is certain: these numbers will change. The February 2020 Farm Income Forecast is based on supply and utilization data from a variety of sources including the January World Agricultural Supply and Demand Estimates and USDA analysts’ expectations of acreage, yields and prices in 2020. Farm income would likely improve if additional sales materialize as a result of improved trade with Canada, Mexico, China and Japan, among others. Farm income could face more pressure, however, if those sales do not materialize as expected in the face of increased crop acreage and production.

Top Issues

VIEW ALL