Cage-Free Eggs Were Once Expected to Dominate the Egg Market

TOPICS

PoultryMichael Nepveux

Former AFBF Economist

photo credit: North Carolina Farm Bureau, Used with Permission

Michael Nepveux

Former AFBF Economist

California voters earlier this month approved proposition 12, a ballot measure mandating the dates by which all eggs sold in the state come from chickens living in cage-free production systems. A previously passed related measure took effect in 2015, but lacked specificity around the cage-size requirements and only applied to eggs produced within the state of California. Approval of this new measure means that even eggs produced in another state and imported into California are required to abide by this requirement. Proposition 12, a proposal that was heavily pushed by animal activist organizations, also included provisions on space requirements for veal and pork production.

Cage-Free Eggs in the U.S.

Cage-free has been a growing segment across the country for some time. Over the past several years, a significant share of retailers and restaurants have committed to going 100 percent cage-free, with many of them setting 2025 as the target year. A tipping point occurred in late 2015, when McDonald’s announced that the roughly 2 billion eggs it purchases annually would be transitioned to a cage-free supply. After that announcement, a flood of companies announced they were also going to move toward a cage-free standard.

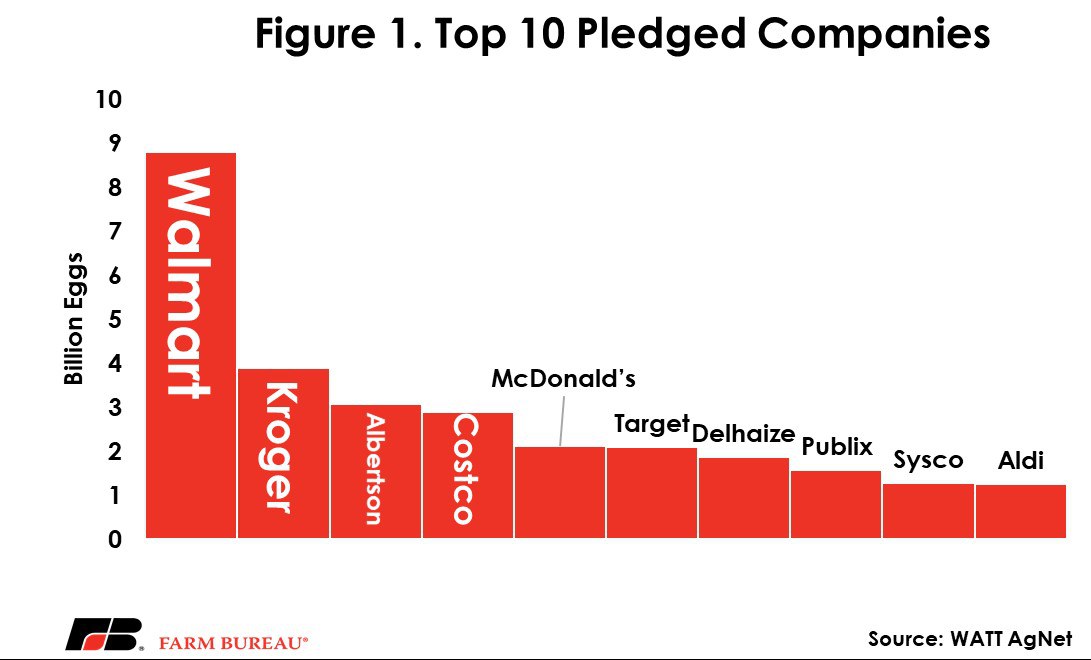

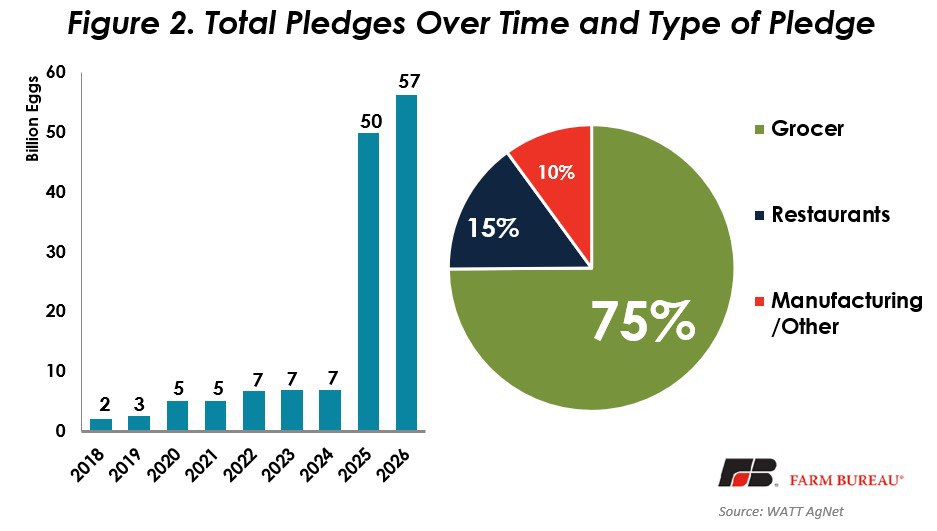

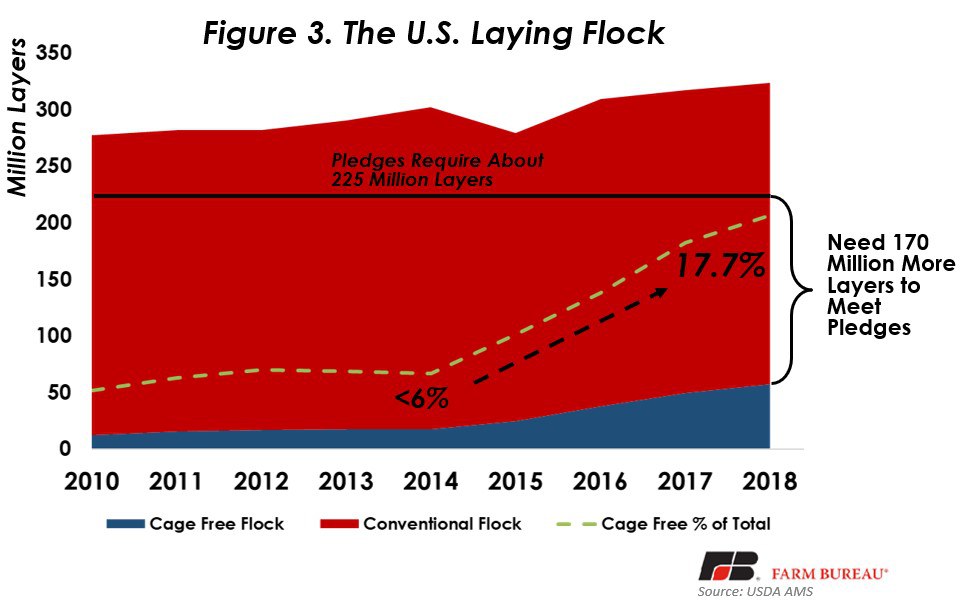

In evaluating and comparing poultry production management systems, there are a range of competing factors to consider, making it difficult to identify one system as “better” than another. People and organizations weigh the various factors differently. While one individual may place greater weight on cage size, another may put a higher value on environmental impact, worker safety, or overall animal health. Additionally, while all systems have benefits and tradeoffs, cage-free as a marketing term is easier for consumers to understand, and so the pledges continued. Altogether, the total pledges would require an estimated 57 billion eggs to be produced using cage-free production systems, which would require a laying flock of roughly 225 million hens, or over 70 percent of the U.S. flock. Many of the country’s most popular brands have made the pledge (Figure 1), with retailers/grocery stores accounting for the majority of the volume of eggs pledged.

Uncertainty Over How Companies Can Follow Through

On the production side, there is still substantial work to do to meet the tight deadline required by many of the company pledges. According to the most recent data, the current cage-free layer flock sits at just over 57 million hens, accounting for approximately 17 percent of the national layer flock. With the total number of pledges due by 2025 requiring over 200 million layers, this means the current cage-free flock would have to more than triple in the next seven years. The current cage-free flock has increased from just under 24 million layers at the beginning of 2016 to nearly 60 million hens now, but more than tripling this number in just seven years is a tall order.

Many of the retailers gave themselves some wiggle room in their pledge, allowing for adequate supply and consumer acceptance to be contributing factors.

“By 2025, our goal is to transition to a 100 percent cage-free egg supply chain, subject to regulatory changes and based on available supply, affordability and customer demand.”

Walmart

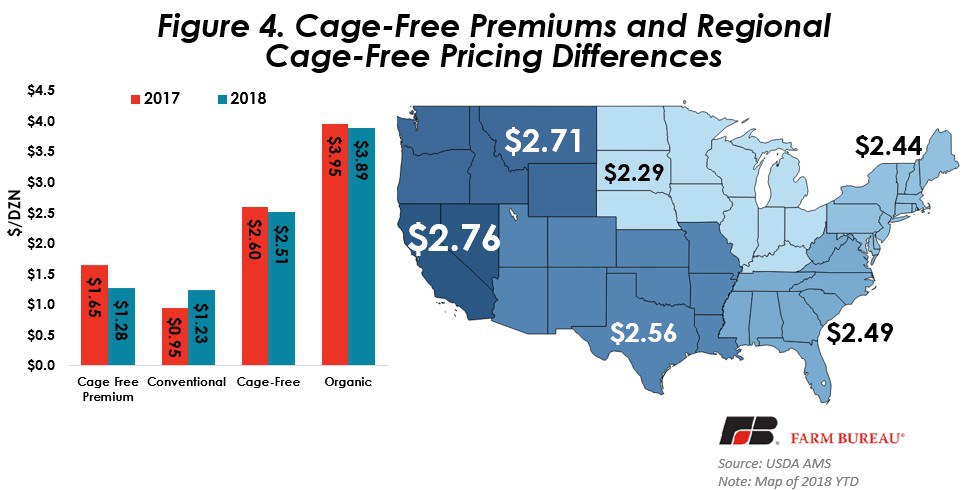

Customer demand is key because so far, consumers aren’t making the switch to cage-free nearly as quickly as most predicted. This is particularly true in a retail environment where the consumer has the option to make a choice between the cage-free variety and the more affordable conventional eggs, oftentimes with the different egg varieties placed right next to each other on the shelf. Several years ago, egg prices increased substantially because of flock decimation due to avian influenza, and the premium between cage-free eggs and conventional eggs shrunk. Retailers saw that consumers were purchasing more cage-free eggs, but with the rebound in egg production and the subsequent price decline, that premium has widened once again.

At the crux of the disparity between what consumers say they want and the decisions they make at the grocery story is the leading question retailers and researchers are asking consumers. If you ask consumers if they want cage-free eggs, many will answer yes. The real question though, is whether they are willing to pay more than $1.00/dozen extra for the cage-free variety. So far most customers are balking at the premium. According to USDA-Agricultural Marketing Service data, while the premium is lower than last year, it is still $1.28 cents for 2018 so far. Producing eggs in a cage-free system costs an estimated 36 percent more than in a conventional production system, and it will likely always cost more, even with economies of scale and increasing competition from expanding production.

The original policy change in California lowered production within the state by 35 percent and increased the average price of eggs by 22 percent. While many consumers have expressed a willingness to pay for cage-free eggs, the premium that they are willing to pay is much lower than current premiums. Recent research suggests that almost 60 percent of consumers have a willingness to pay for cage-free egg premiums less than $0.40/dozen, a full $0.88/dozen short of the 2018 premium.

In order to meet company pledges, the industry could have to invest as much as $10 billion to convert housing systems in the U.S. to cage-free. After the flood of cage-free commitments were announced by restaurants, companies greatly invested in expanding their cage-free operations to meet the expected increase in demand. As a result of the lackluster consumer response, producers have scaled back investment in cage-free systems. At this point, there is a great amount of uncertainty whether the industry will actually make the move to cage-free. It is almost a game of chicken between producers and consumers; producers need time to expand their cage-free capacity but won’t do so unless there is adequate demand from consumers. Consumers say they like the idea of cage-free eggs but aren’t willing to pay the premium associated with them.

Will we See the Market Move to 100-Percent Cage-Free Eggs?

This depends on the market segment. It is certainly conceivable that food service and restaurant establishments who made the pledge could move all the way to cage-free eggs as they have room to disguise the cost increase in the entire cost of the meal. A similar argument can be made for institutional buyers and food manufacturers. However, it is probably unlikely that retailers will make the switch completely, even if they made a pledge to do so. So many of the commitments contained caveats about availability of supply and consumer demand, and the consumers just aren’t buying the eggs. It is likely the only way the switch would happen at this point is if retailers were to take away the option of the conventional eggs, forcing consumers to switch. This is unlikely as retailers would not want to turn away their more price-conscious consumers and would not want to be seen as making it more difficult for working families to afford food staples. Whether or not these pledges are met ultimately depends on how many of these retailers take away the more affordable option and put the chicken before the egg.

Top Issues

VIEW ALL