December Cattle on Feed Report Shows Decline in Placements and Marketings

TOPICS

USDAMichael Nepveux

Former AFBF Economist

photo credit: AFBF

Michael Nepveux

Former AFBF Economist

USDA’s latest Cattle on Feed report, released December 18, shows the number of animals on feed as of December 1 is even with last year. The report provides monthly estimates of the number of cattle being fed for slaughter. For the report, USDA surveys feedlots of 1,000 head or more, as this represents 85% of all fed cattle. Cattle feeders provide data on inventory, placements, marketings and other disappearance.

November Cattle on Feed Report

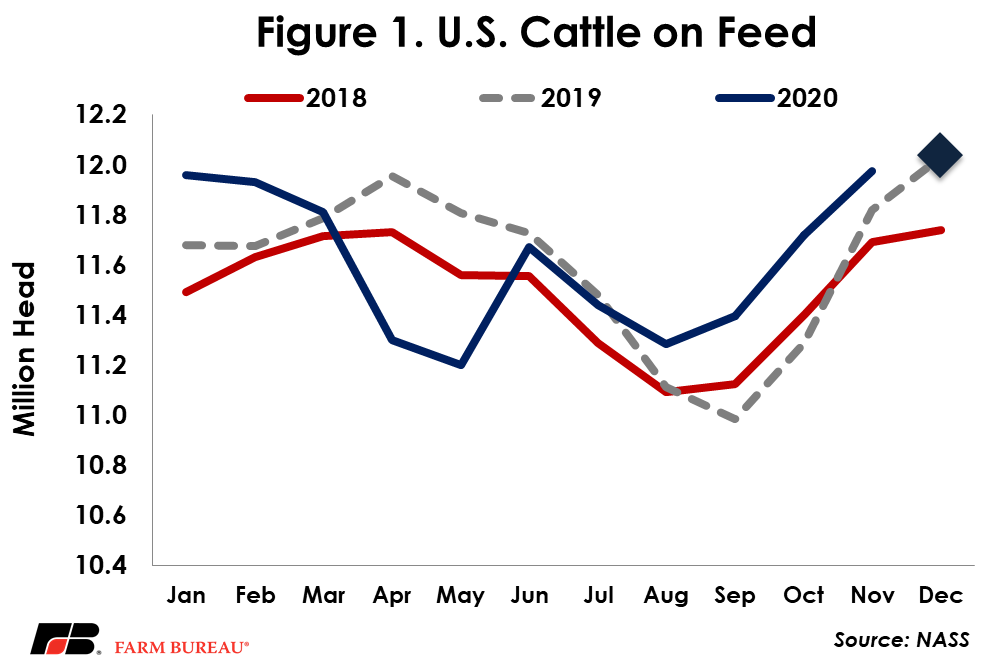

This report showed a total inventory of 12.036 million head for the United States on December 1, up from the same time in 2019 and from last month. This lack of a year-over-year change is right in line with analysts’ expectations of feedlot inventories holding steady relative to last year. Typically, December continues the fall buildup of animals after September lows, and it looks as if we are seeing this seasonality play out. After strong impacts from the pandemic in April and May, the number of cattle on feed has largely followed seasonal patterns, but since August has been running above recent years’ levels. This Cattle on Feed report marks a change in that pattern.

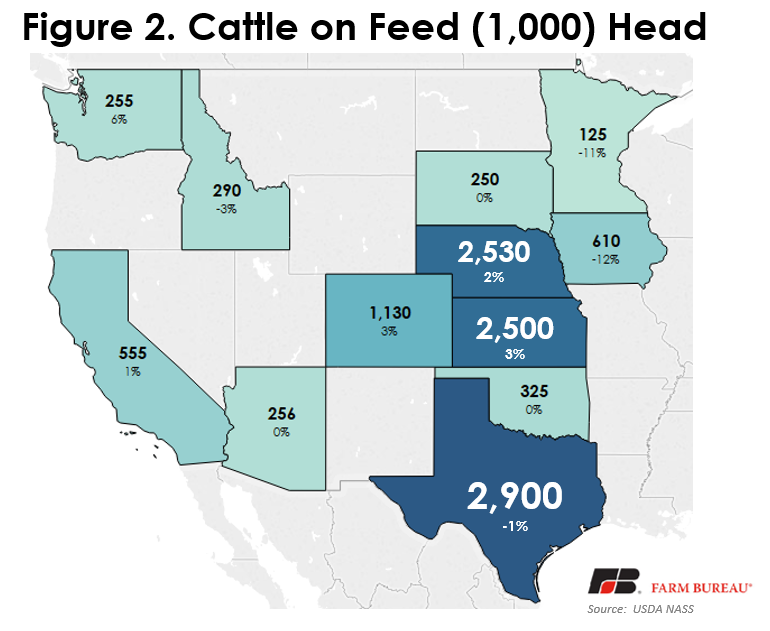

As usual, Texas, Kansas and Nebraska led the way in total fed cattle numbers, accounting for over 7.9 million head, or approximately 66% of the total on-feed inventory in the country. Texas ended its year-over-year gain, dropping 1% relative to 2019. Kansas and Nebraska posted moderate gains, adding 3% and 2%, respectively.

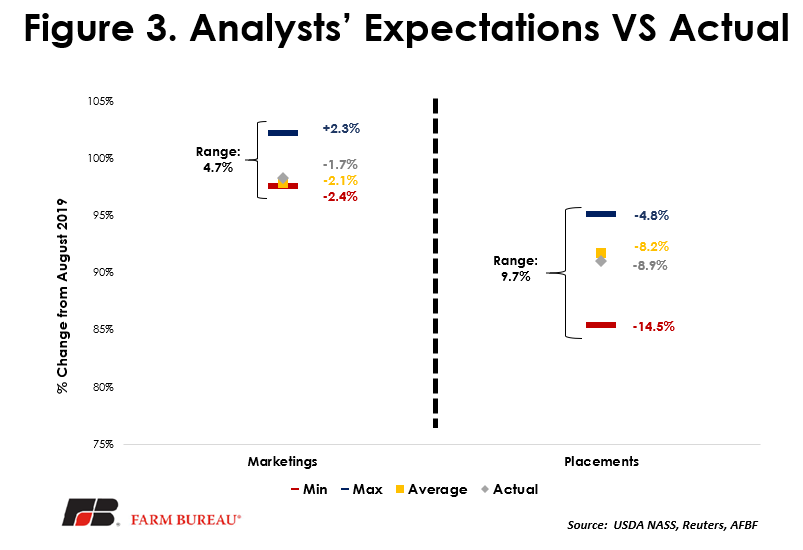

While total inventories are an important component of the report, other key factors include placements (new animals being placed on feed) and marketings (animals being taken off feed and sold for slaughter). Coming in at 8.9% under 2019, placements in November came in under the average analyst expectation of an 8.2% decrease. The relatively wide range of forecasts for placements – approximately 10% -- highlights the uncertainty that can exist in forecasting this specific variable. Imports of feeder cattle from Mexico have been sluggish, driving some of this pullback in placements. After recovering from declines in April and May at the height of the pandemic, placements had been running ahead of year-ago levels –– until October, when they dropped by 270 million animals. In November, placements clocked in at 1.906 million head, 187,000 head below a year ago and continuing the previous months’ year-over-year declines. With the decline in placements and overall cattle on feed numbers working their way back down, feedlots may be mostly current. Two consecutive months of declining placements are setting up for reduced fed cattle supplies, and likely higher prices, in the April/May timeframe. Lower placements may continue as long as cost of feeding remains elevated and feeders try to keep animals off feed to an extent. Marketings came in at 1.782 million head, or 1.7% below last year. This is slightly above analysts’ expectations of 2.1% below year-ago levels, with November experiencing lower marketings, even with the same number of slaughter days as a year ago.

Summary

This December Cattle on Feed report is considered relatively neutral to bullish. While a 9% decline in placements is bullish for future supplies of fed cattle, the industry expected a decline to a decent degree. The overall supply of cattle on feed is almost exactly in line with December 2019, and the number of animals marketed throughout November is below a year ago.

Looking forward, the big question is the level of resurgence in COVID-19 cases throughout the winter. We have already had several reports of packing plants closing due to outbreaks, but so far have we have not seen the significant price movements that would indicate a serious concern about supply. This could also be partly due to the meat pipeline having its needs met for now, with additional winter closures of restaurants potentially further reducing demand in that sector. After we clear the winter, this report indicates we should be looking at tighter market-ready cattle supplies in the late spring, a possibility supported by the April live cattle futures contract topping $118/cwt the last two days.

Top Issues

VIEW ALL