Farm Bill Math Updated in New Congressional Budget Office Baseline

photo credit: PRO401(K) 2012 CC BY SA 2.0

John Newton, Ph.D.

Vice President of Public Policy and Economic Analysis

The Congressional Budget Office releases projections on expected spending for farm programs for the current budget year plus ten years, the ten-year baseline, up to three times a year. CBO’s June 2017 Baseline for Farm Programs was released on June 29, 2017. These projections identify expected outlays for farm bill program spending, assuming existing programs continue without changes, and will serve as an indicator of program spending available to Congress as crafting of the 2018 farm bill kicks into higher gear.

Farm bill math creates a few possible scenarios. Depending on negotiations between the budget and agricultural committees the next farm bill could be required to be budget neutral, meaning any increase in spending in one part of the bill would require a decrease in spending elsewhere in the bill, or it could be required to have a net reduction. Given these budget directives, scoring a bill (estimating the additional outlays and potential savings relative to the baseline) is one of the most critical components of farm bill development. From now through the farm bill’s passage, any change in policy will require an estimate of the budgetary impact. A farm bill written in 2017 would be scored against this baseline, and a bill written in 2018 would be scored against a spring 2018 baseline, or depending on progress in negotiations, could be scored against this June baseline.

Cost of Farm Programs is Higher for Some Commodities

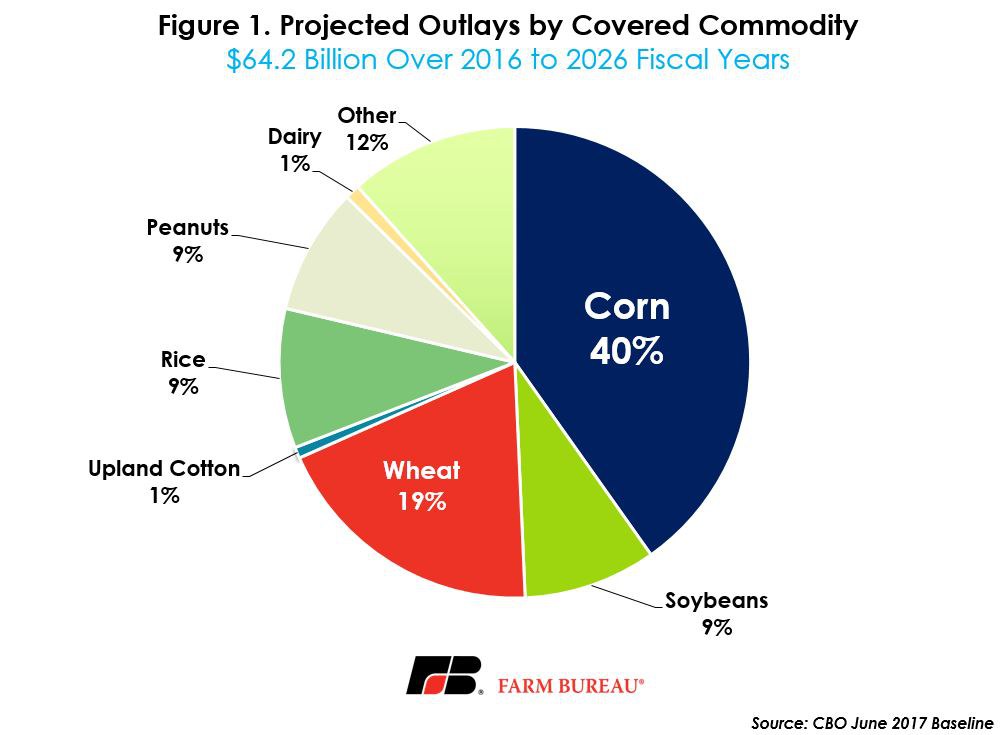

Many of the provisions of current farm programs move in opposite direction of commodity prices. Consequently, several years of lower prices have resulted in higher commodity support payments. Estimates of total farm program expenditures during the 2016 to 2026 fiscal years are now estimated at $64.2 billion dollars, up $3.5 billion over CBO’s March 2016 projections. Peanuts, cotton and soybeans saw their 10-year baselines decline, while corn, wheat, rice and dairy baselines increased in value.

The distribution of farm program payments follows base acreage in the U.S. Corn, soybeans and wheat represent nearly 70 percent of all program payments, while rice and peanuts represent another 18 percent. Sorghum, upland cotton, dairy, and other smaller field crops represent the remaining 14 percent of outlays, Figure 1. These outlays come in the form of Price Loss Coverage or Agricultural Risk Coverage payments, marketing loan benefits, and margin protection program for dairy outlays.

The change in farm bill outlays is due to a variety of factors. First, price expectations for several covered commodities have changed due to different supply and demand conditions. For example, consider that record yields and larger domestic inventories have weakened corn prices in recent years and led to higher ARC-CO payments. CBO’s June 2017 projections are for marketing year average corn prices to remain below $4 per bushel over the next decade. These lower corn prices contribute to an additional $4.8 billion in ARC-CO and PLC outlays over the next 10 years.

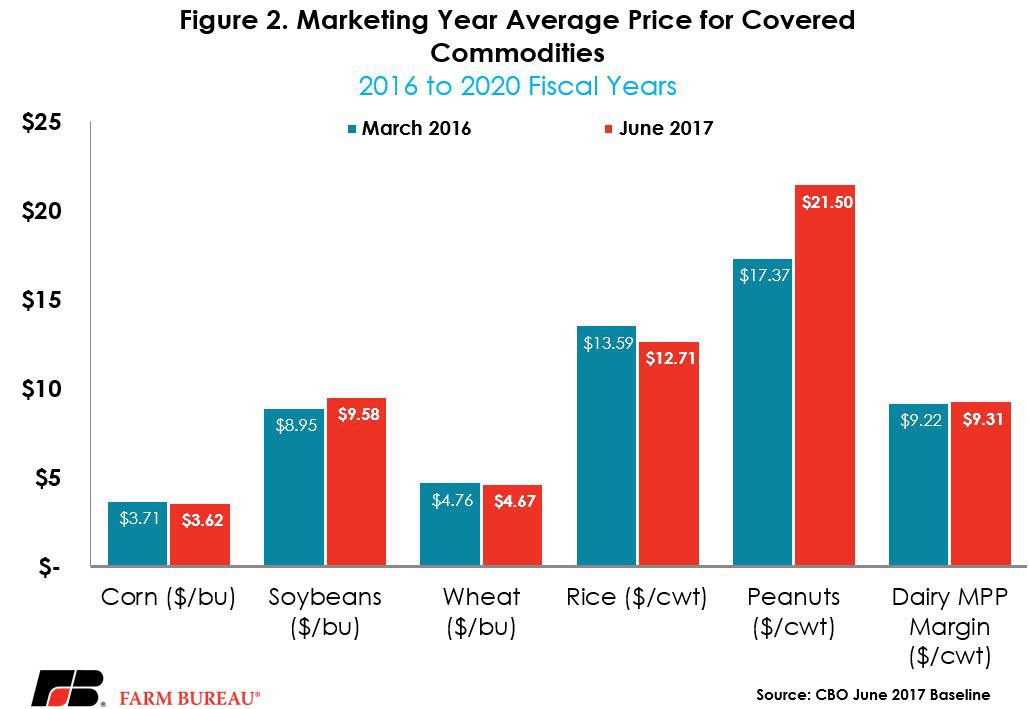

While government costs of the corn program have increased due to weaker prices, other commodities saw their outlays decrease due to higher market prices. For example, tighter supply conditions in peanut markets resulted in the CBO raising their price forecasts in nearby years. In March 2016, CBO estimated the five-year average peanut price at 17.4 cents, and in the most recent baseline, the five-year average price was 21.5 cents per pound, Figure 2. These higher peanut prices lowered forecasted PLC payments by $1.7 billion over 10 years. This reduction in baseline spending was expected as forward contracts to peanut producers have been reported in the range of $400 to $500 per ton.

Another factor driving additional outlays is CBO expecting Congress to provide farmers with the option of re-enrolling in ARC-CO or PLC in the next farm bill. This would allow farmers to change program participation for the 2019/20 growing season and would impact program payments beginning in the 2021 fiscal year. For the 2014 farm bill, 96 percent of corn base acres, 91 percent of soybean base acres, and 66 percent of wheat base acres were in the revenue-based ARC-CO safety net.

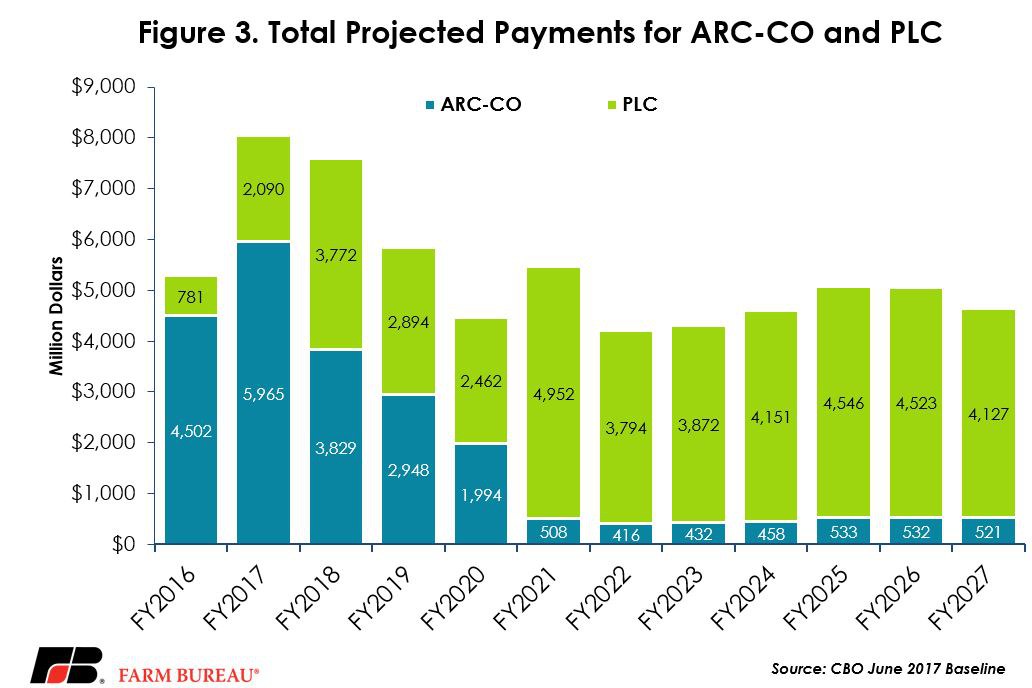

Expectations for lower corn and wheat prices are likely to make PLC the more attractive safety net option beginning with the 2019 crop year – and thus CBO is projecting that 82 percent of the corn and wheat base acres will choose PLC over ARC-CO. Due to this shift in program participation, CBO is projecting PLC outlays to increase by nearly $10 billion over 10 years to $37.8 billion. ARC-CO payments are projected to be $3.5 billion lower over 10 years and is now estimated to cost $28 billion over 10 years. Figure 3 shows expected outlays under ARC-CO and PLC by fiscal year, and highlights the impact of the re-enrollment decision beginning with 2021 fiscal year outlays.

The final factor impacting the change in outlays is budget sequestration. The March 2016 baseline adjusted for budget sequestration for the 2015 to 2026 fiscal years. The most recent June 2017 baseline only adjusts for sequestration through the 2018 fiscal year. The Office of Management and Budget is responsible for the official determination of sequestration reductions based on their estimates of federal spending. If additional sequestration is authorized, farm program outlays would most likely be lower beginning with the 2019 fiscal year and when the next baseline is released.

Implications

This most recent CBO baseline on farm program outlays is an important indicator of the budget outlook going into the next farm bill debate. Underpinning these budget forecasts are important estimates of commodity supply and use. Lower than forecasted commodity prices would be expected to result in higher outlays by the spring 2018 baseline. Similarly, improvements in commodity prices would result in lower projected outlays for farm programs. These market fundamentals will be important to monitor as they will ultimately impact the budget and development of the next farm bill.

Top Issues

VIEW ALL