First Quarter 2021 Gross Domestic Product In Technical Terms – ‘Pert Darn Good’

TOPICS

TradeBob Young

President

photo credit: Unsplash CC0

Bob Young

President

The overall economy grew at an annualized rate of 6.4% in the first quarter of the year. Any time other than a pandemic recovery, we would have all said, ”Wow!” However, given where we’re coming from, it is more of a ”what-did-you-expect” outcome.

Total gross domestic product for the first quarter was $22.04 trillion on an annualized basis. This compares to $21.49 trillion for the fourth quarter of 2020 and $21.56 trillion in the first quarter of 2020. The highest figure before the pandemic set in was $21.75 trillion in the fourth quarter of 2019. So, we are back to the strong overall economy of 2019, but some sectors continue to struggle.

Personal consumption expenditures rose by more than $500 billion, effectively driving the rise in GDP. Spending on goods grew by $331 billion, halved roughly between durable and non-durable goods. All the discussion about a chip shortage slowing down car purchases hasn’t shown up in the aggregate numbers so far as motor vehicle expenditures grew by almost 10%. Foodservice jumped by $49 billion. People are showing a willingness to eat out. But while $865 billion on food service is a considerable number, it is still well below the $1.01 trillion spent in the last quarter of 2019. This component and other leisure and hospitality factors will continue to add to overall economic growth as we reopen from various lockdowns, but there is an upper limit. We were pretty close to full bore in the food service and other leisure and hospitality areas before the pandemic. There may be another $200 billion or so in activity there, but is there much more?

Gross private domestic investment is the next major account in GDP. These investments in structures and fixed equipment declined by $24 billion from last quarter, although businesses boosted spending on equipment and intellectual property products by a combined $74 billion over fourth quarter 2020. Even investments in residential properties rose by over $50 billion. The drag on this account comes from the third portion, change in assets. Inventories dropped by $90 billion in the first quarter, after rising by $60 billion in the fourth quarter. This translates to a $150 billion charge to the negative from inventories alone. This swing in inventories is something of a good-with-the-bad situation. While the drop in inventories lowers this quarter’s GDP, we will need to rebuild sooner or later. When we do rebuild, it will then count as a plus for GDP.

Exports are back in the $2.3 trillion range, up by $95 billion from the previous quarter. Most of this was in goods as exports of services grew by only $7 billion. Imports, however, also increased – by $138 billion, swamping the export figure. Here again, it was imports of physical goods that dominated. Goods imports rose by $128 billion.

Federal government expenditures that contribute to the GDP rose by $64 billion this quarter, with the large majority of that figure - $62 billion – in non-defense spending. State and local governments also boosted spending by $54 billion.

So other than a few minor drags from inventory changes and a rise in imports, everything moved in the right direction. And the two downers are essentially indicators of solid demand that current production capacity can’t keep up with, drawing down inventories and boosting imports.

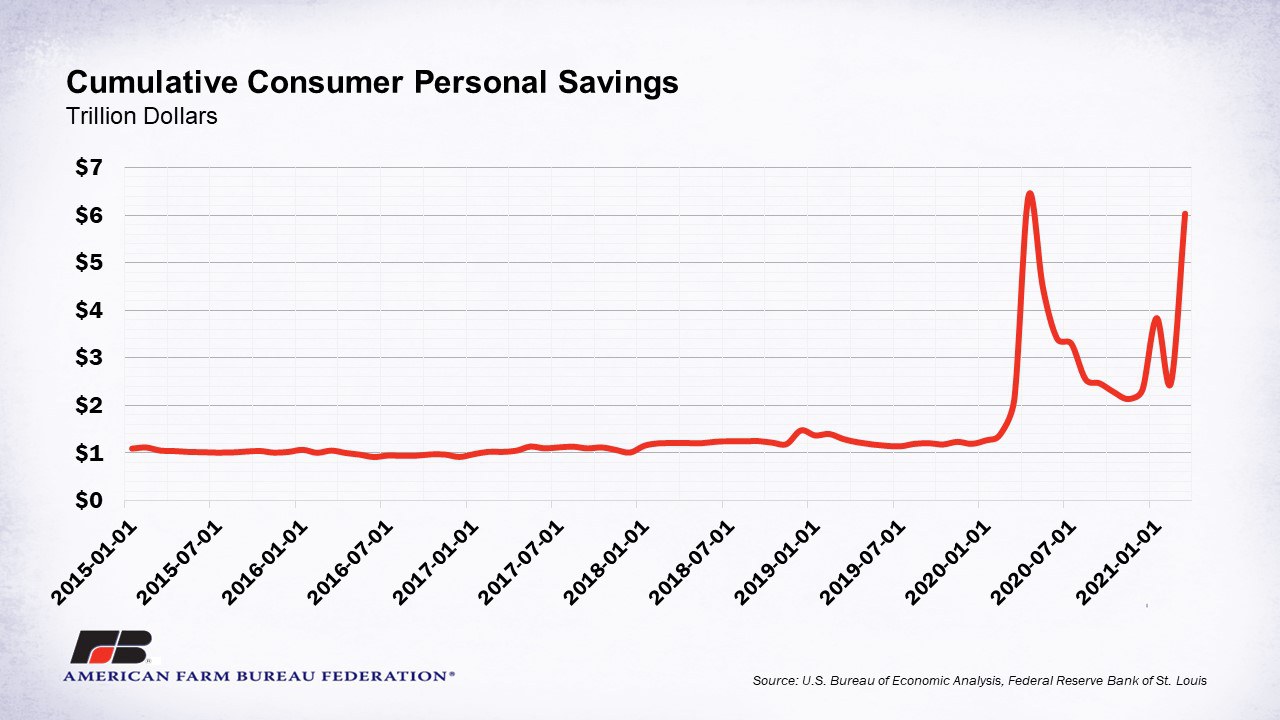

A lot of press over the past few weeks has focused on inflation. With the growth indicated by this GDP report, taken with an expectation of further economic opening over the next few months, one could understand concerns about an overheating economy. Consumers have a lot of savings backed up between earlier reduced consumption and the stimulus checks; personal savings that typically run around a trillion dollars now sit over $6 trillion.

Two of the more volatile components of the consumer price index, energy and food costs, were both up substantially in March. Food was up 3.5% over year-earlier figures and overall energy costs were up 13.2%. Wages and salaries have been rising at a 3% rate as well for the past few months. When we get broad sectors of the economy showing substantive price increases, like energy or labor, you have to worry about overall inflation.

As we come out of the pandemic, supply chain backups will only continue to get more pronounced. Whether it be computer chips, plywood or chicken, a new example shows up in the press almost daily. And labor is frequently the driving factor.

So, the economy is doing pretty well -- maybe too well – for the past few months.

Top Issues

VIEW ALL