Higher June Lamb Exports, Not the Cause of Higher Priced Lambs

AFBF Staff

photo credit: Alabama Farmers Federation, Used with Permission

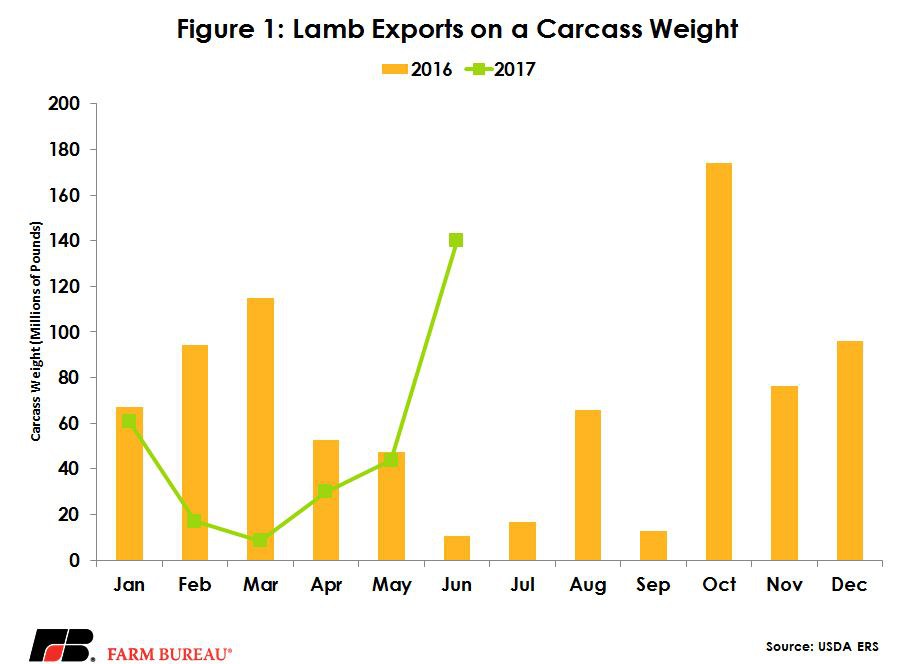

Lamb is a very small portion of the U.S. meat export portfolio, surpassed by all the major categories including mutton. Most months of the year lamb exports remain under 100,000 pounds. However, this June saw numbers hit 140,000 pounds, compared to June numbers last year of only 10,000 pounds. Mexico is one of the more consistent buyers of U.S. lamb, and their purchases grew by 39,000 pounds compared to last year. The Dominican Republic and Honduras were two other large buyers jumping in this month. Honduras purchased 65,000 pounds, while the Dominican Republic bought 23,000 pounds.

Most of the lamb raised in the U.S. is consumed domestically, as along with fairly high levels of imported lamb. Last year the U.S. imported 188 million pounds of lamb on a carcass weight, compared to exporting only 828,000 pounds. While the June numbers were good, year-to-date lamb exports are actually running below a year ago by 87,000 pounds, about 23 percent. Lamb exports vary throughout the year. The June 2017 export volume is the largest total since October 2016, see Figure 1.

Although exports were up in June and total exports on the year are down, per capita consumption is expected to be down slightly for sheep and lamb, hovering around that one pound per person per year. Even with these less than stellar demand issues, domestic lamb prices have gained ground. The second quarter of 2017 showed prices up 19 percent for slaughter-weight lambs with similar gains seen in feeder lambs. So why have prices seen gains in the first half of 2017?

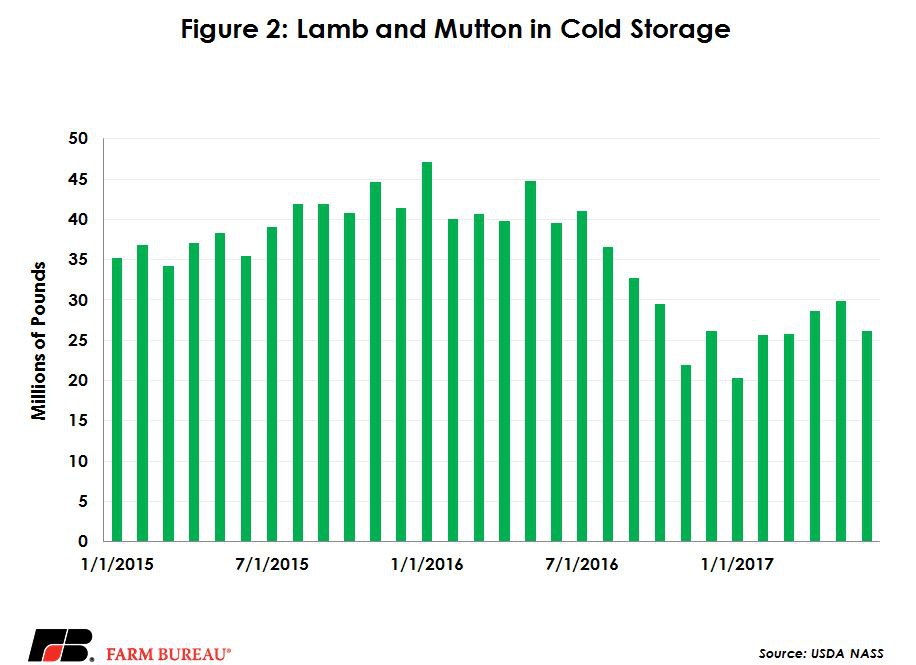

It’s largely been a supply story in 2017. January’s Sheep and Lamb Inventory report estimated the sheep herd was down 2 percent or 100,000 head. A resulting smaller lamb crop has been reflected in lower slaughter levels. Weekly slaughter for lambs and yearlings is down nearly 5 percent and is coupled with lower dressed weights which are down a full 2 percent year-to-date. Further adding to the tightness is a slow decline in stock inventories that had built up last year. June inventories are 34 percent below a year ago, continuing the slide shown in Figure 2.

This tightening on the supply side has led to stronger prices. The 3-market feeder lamb price hit an all-time high earlier this year topping $260 per hundredweight. The previous record was $244.75 per hundredweight set back in May of 2011. Prices remained over $200 per hundredweight for the second quarter and have since eased off to the $180s in recent weeks, closer to last year’s prices. Fed lamb prices peaked in the second quarter and have been trailing ever since.

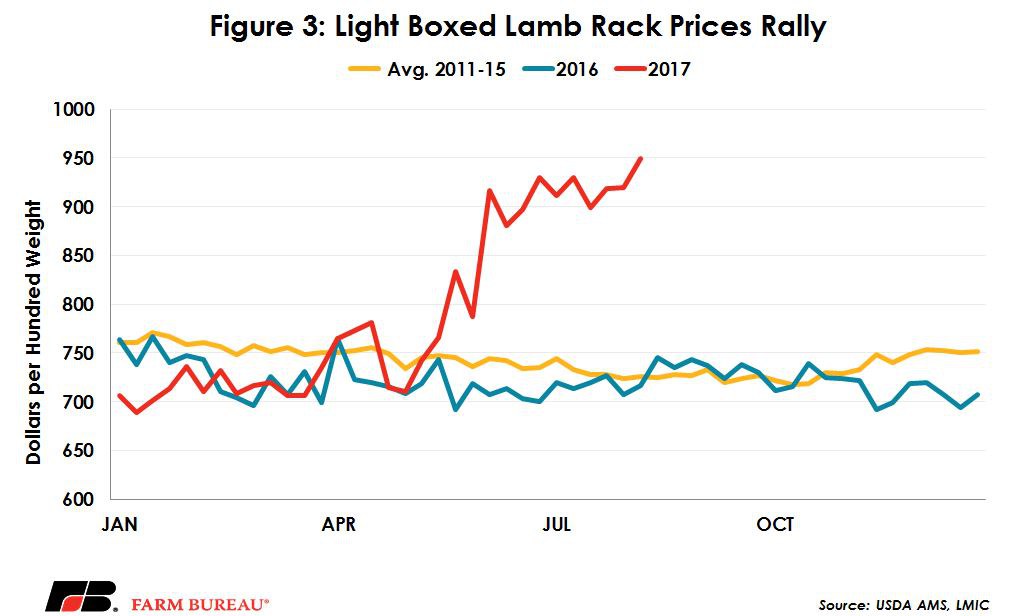

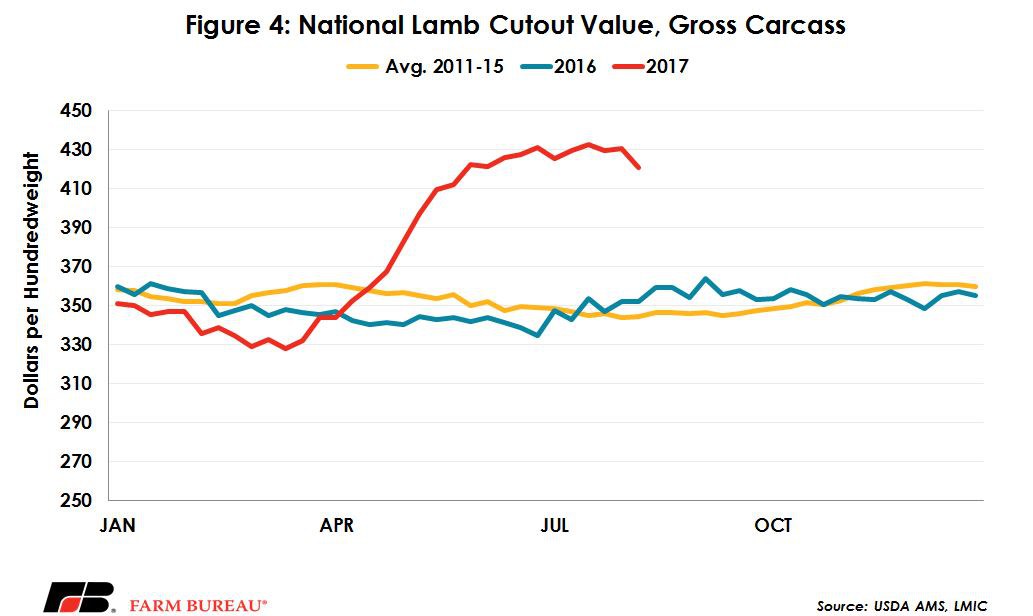

Higher lamb prices have translated into higher meat prices across the lamb complex. The lamb cutout has hit lofty highs on a weekly basis and seen some tremendous strength. Weekly cutout values took off starting in April 2017 and have gained $80 per hundredweight since, reaching well over 20 percent above a year ago for the last 11 weeks. Racks, loins, shoulders and legs have also shown great gains from a year ago and have not eased off the same way live prices for fed and feeder lambs have. Figures 3 and 4 show the climb in racks and cutout values.

Livestock Marketing Information Center is one of the few groups independently forecasting lamb production and prices. They expect robust prices to continue in feeder lambs, averaging over $210 per hundredweight for 2017, or 14 percent higher than 2016. Slaughter weight lambs are also expected to close 2017 with higher prices, averaging just over $300 per hundredweight or 7 percent higher. Looking beyond 2017, LMIC forecasts production increasing and on balance a slight slip in prices, about 1-2 percent down in feeders and slaughter lambs. Lamb consumption is expected to hold relatively steady at one pound per person per year.

Top Issues

VIEW ALL