Investing in the Future of Farming

Megan Nelson

Economic Analyst

photo credit: AFBF Photo, Morgan Walker

Megan Nelson

Economic Analyst

Over the past few decades, agricultural research and development has spurred tremendous leaps in farm and ranch productivity, efficiency and safety, as well as the decrease of costly inputs, like fertilizer and water for irrigation. According to USDA’s Economic Research Service, since 1948 these innovations have led to U.S. agriculture productivity growth of 170% while inputs have remained mostly unchanged and the use of labor has declined by 24%.

Once the global leader in agricultural R&D, the United States’ investment has been decreasing in comparison to private investment since 2010. The long-term effects of this shift have negative implications for the future of farming.

Investment in Agriculture R&D

U.S. public sector investment in agriculture R&D has historically positioned the U.S. to be a top contributor and the largest producer of cutting-edge agricultural technology in the world. Unlike other sectors of the U.S. economy, public investment, rather than private investment, in agriculture R&D, has been the main driver for the long-term development of industry-altering technology. However, since 2010, the share of U.S. public sector spending on food and agriculture R&D has decreased to less than 30% of total expenditures.

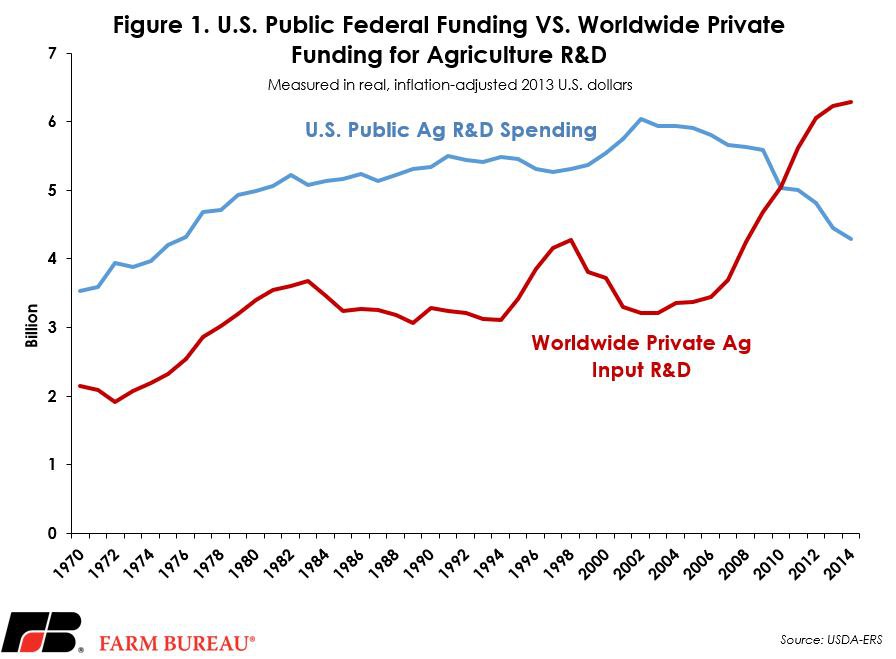

This shift in funding is the result of both a decrease in public funding and a dramatic surge in private funding in the biotechnology industry. The current funding trend in agriculture R&D may negatively impact the future of farming by focusing too heavily on short-term, consumer-driven developments. Figure 1 illustrates USDA-Economic Research Service data on trends of worldwide for-profit companies’ agricultural input R&D investments compared to U.S. public investment.

Public Spending

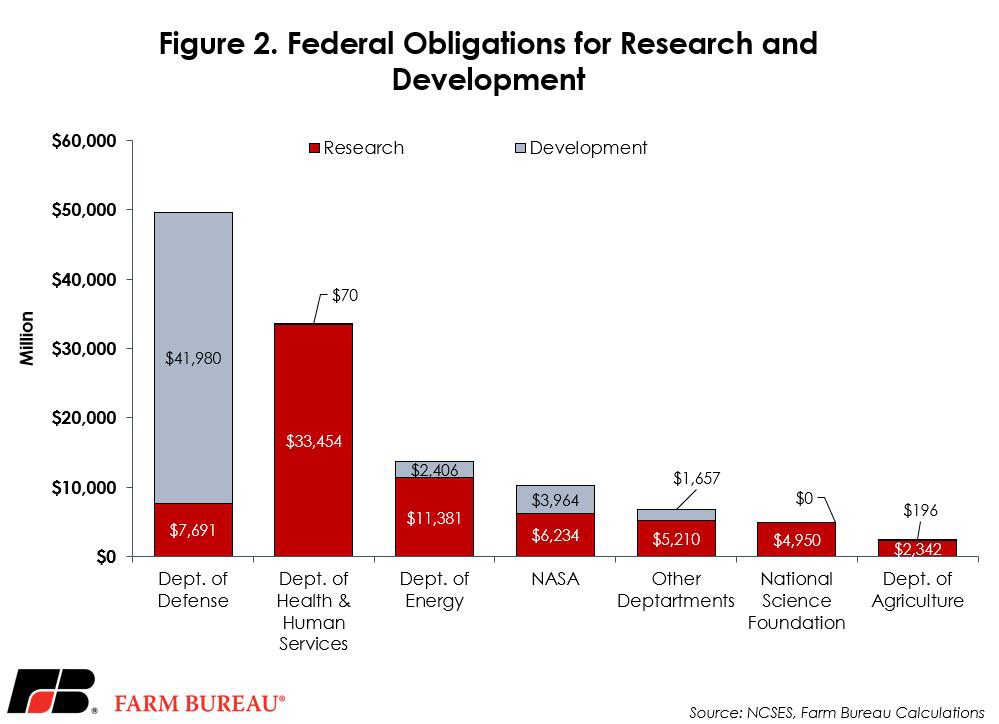

Federal obligations for total U.S. R&D expenditures increased to $121.5 billion for fiscal year 2018, up nearly 3% from fiscal year 2017. In fact, the Department of Agriculture financial obligations are the lowest among all other departments, and account for only 3.3% of the total federal obligations at $2.5 billion. Research obligations totaled $2.3 billion for fiscal year 2018 and were up 5.6% from prior year levels, while development-related obligation totaled $196 million and were down 3.1% from fiscal year 2017. Agriculture R&D funding is appropriated through the agriculture appropriations bill that funds USDA and is authorized in the farm bill.

The Senate Appropriations Committee’s fiscal year 2020 agriculture appropriations bill would provide $23.1 billion in discretionary funding, with $3.172 billion specifically for agriculture research programs. The House Appropriations Committee’s agriculture appropriations bill allocates $3.257 billion for agriculture research programs, with a total of $24.3 billion in discretionary funding. Both bills represent a decrease in agriculture research funding by over $100 million for 2020 compared to 2019 levels of $3.4 billion. Public funding for agriculture R&D is down over 30% from 10 years ago, leaving a gap in the potential for future developments.

Private Spending

One of the biggest differences between public and private funding is the target audience. While subject to regulations and application criteria, projects funded by public dollars typically focus on long-term, high-impact issues. In contrast, privately funded projects have a much narrower focus, with market value being the primary driver. The cost of trial and error, inherent with any R&D endeavor, limits companies from being able to take major risks.

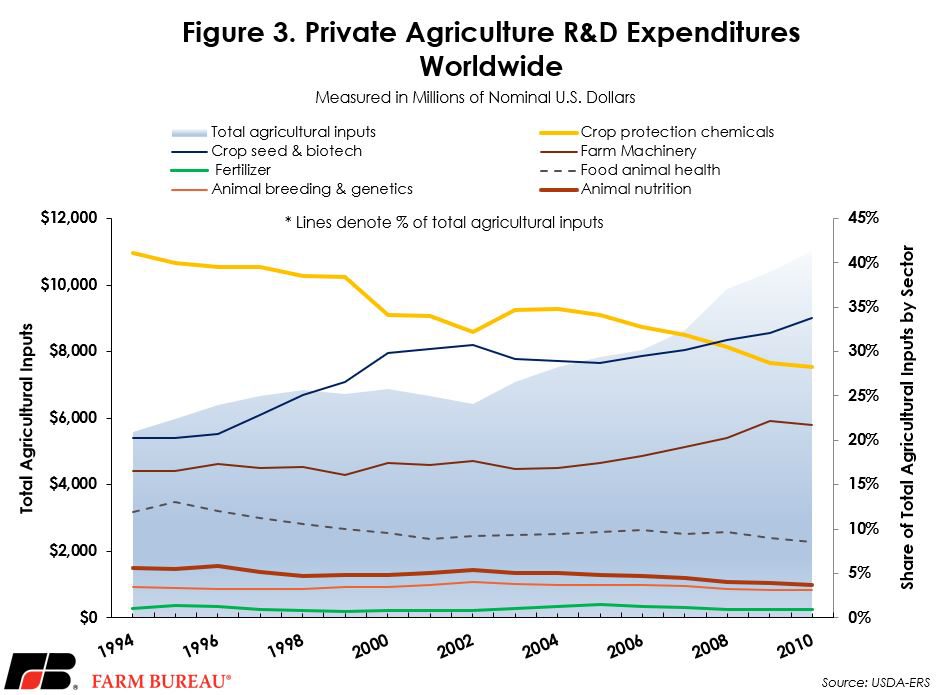

However, as the market for new biotechnology in the agriculture industry has increased, so has the ability of companies to invest. Private investment in various agricultural input sectors has increased steadily over the past 20 years, reaching an estimated $11.026 billion in 2010. More than doubling since 2000 and 2010, private investment in crop seed and biotechnology inputs represents over one-third of total agricultural inputs, Figure 3.

Global Comparison

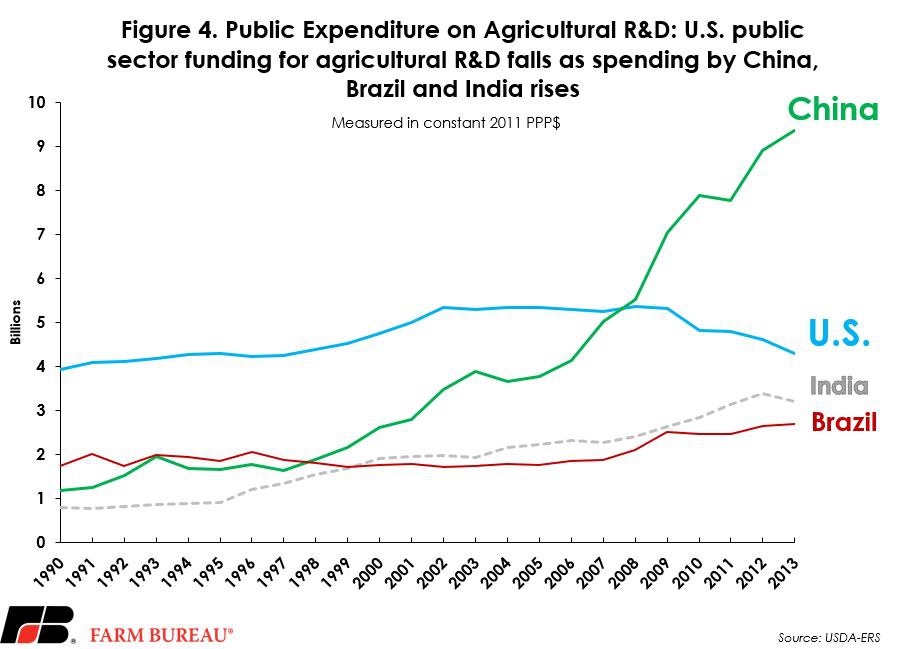

The average rate of return for high-income countries on their investments in agriculture R&D is 35%. However, U.S. public investment in agriculture R&D has decreased steadily since 2002. Once a global leader of public agricultural R&D, with 20% to 23% of the global share between 1990 to 2006, the U.S. declined to only 13% of the global share by 2013. By 2008, China surpassed U.S. total public expenditures on agriculture R&D, and China has only upped its funding, while U.S. public investments continue to decline. Other global competitors, like Brazil, have increased public spending by over $600 million from 2008 levels to 2013 levels, while the U.S. has decreased funding by over $1 billion over the same time period. Figure 4 outlines the public expenditure on agriculture R&D measured in constant 2011 purchasing power parity dollars from 1990 to 2013.

Summary

The U.S. still holds the top spot for the most productive agriculture research system in the world. However, if private-sector investments continue to outpace public spending, the future of U.S. agriculture innovations may look very different than the large-scale, impactful gains we enjoy today.

Research endeavors not burdened by the need to recoup expensive R&D costs provide a unique opportunity for exploration and innovations. While private-sector investment in agriculture R&D - in terms of dollar amount - has more than made up for the decline in public-sector investment, the former is not a substitute for the latter. Instead, private and public efforts should complement each other to produce agriculture innovations that will feed growing populations under all climate circumstances.

Top Issues

VIEW ALL