Return To The Alphabet Lesson For the Economy’s Recovery

TOPICS

MacroeconomyBob Young

President

Bob Young

President

A few months back, we discussed the potential shape of the recovery. Would it be a “V,” an inverse “J,” or a “W”? Another potential letter has appeared in the last month or so, a “K.”

A K recovery reflects that some sectors of the economy have already bounced back and are, in some respects, stronger than before the pandemic. Equities markets are probably the best example of this: The S&P 500 set a then-high of 3,386 on Feb. 19. The index climbed further to 3,581 on Sept. 2.

There have been several reports of billionaires increasing their net worth by billions of dollars during the pandemic. This goes hand in glove with the idea of the equities markets setting new highs, particularly as the tech sector has been on such a tear.

These economic gains reflect the top side of the K. They apply not just to the top .1% of the economic ladder, but to larger sectors as well.

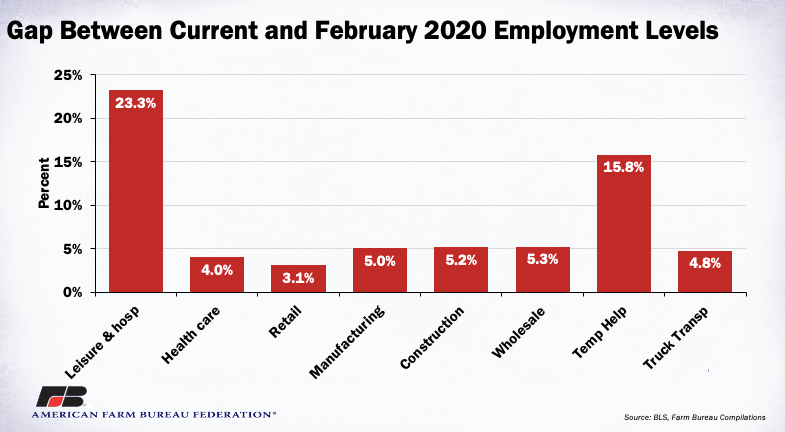

Overall, the economy employed 152,463,000 people in February 2020. This was the employment peak before the pandemic shutdown. After the latest jobs report, we are still shy of this number by 10,743,000. If you are in that figure, you represent the bottom side of the K.

The eight categories of employment shown in the graphic account for 53% of the total number of jobs in the United States. At 16.5 million slots each, leisure and hospitality and health care are essentially the same size. Together they clearly show the K-shaped recovery. We are still down 3.8 million jobs in leisure and hospitality from the February peak. Restaurant closings, Disney layoffs and second waves of COVID-19 infections all contribute to keeping this sector in a confused state. How do you bring all the staff back when the place can only operate at 25% capacity? Conversely, look at the retail sector. The gap there compared to February levels is only 3%, nearly restored.

But the sector levels hide that same K structure. If you are involved in automotive work, whether it be selling new cars, car parts or tires, you are pretty much back to pre-pandemic levels. If you are in the hardware business, there are more jobs today than were around in February. Same story for food and beverage.

Clothing stores are another story. After hitting 1.28 million slots in February, jobs at clothing and accessory stores dipped to 492,000, but have climbed back to 962,000, still off a third from earlier levels. Somewhat surprisingly, even department store employment is nearly back to pre-COVID-19 levels. Jobs at sales clubs are up over 200,000 slots. While not a large category, jobs at bookstores are down to 45,000 positions from 73,000 in February, nearly a 40% hit.

Do we need another stimulus? Mr. Powell, chairman of the Federal Reserve, has testified that we do. If you are in the bottom side of the K, you could use one. If you are in the top part, you would probably complain about the deficit.

A couple of data points suggest the economy could be ready to go once the restrictions are lifted. One of these is the personal savings rate. Historically, the personal savings rate has hovered in the 7% range. Between January 2014 and January 2019, the monthly data stayed between 6% and 8% for all but one month. The stimulus package and the hospitality and leisure sector closure boosted personal savings to a record 34% in April of this year. The figure has retreated to only 14% in August, but this remains well above historical precedent.

Another data point is the proportion of disposable income people spend on debt service. This data is only available quarterly, with third-quarter data not available at the time of writing. Unlike the savings rate, this proportion shows more variability. In the early stages of the 2007/08 recession, the share spent on debt service rose to a high of 13% but has been relatively steady in the 9-10% range since 2011. The second quarter this year showed a decline to 8.7%. In other words, the consumer could take on more debt without budgetary strain. This gives the consumer substantial running room when convinced the economy is back on the mend, particularly if they’re on the top side of the K.

Targeted stimulus would be appreciated by those on the lower side of the K, like those in the leisure and hospitality sector, which still has a long way to go. Such a package would require careful crafting to avoid sending money where it’s not needed.

Top Issues

VIEW ALL