Second Round of Trade Assistance Coming Soon

TOPICS

Trade War

photo credit: Sgt. Mikki Sprenkle/Public Domain

John Newton, Ph.D.

Vice President of Public Policy and Economic Analysis

Following nearly two years of unfair retaliatory tariffs that have roiled U.S. commodity markets and disrupted supply chains, USDA recently signaled that the second of three rounds of Market Facilitation Program payments, i.e., payments that were tentative to be paid in November 2019, will be available to producers in late November or early December. The first round of trade assistance, announced in July 2019, authorized up to $14.5 billion in direct payments to farmers who had been impacted by the tariffs (USDA Announces Details Behind the New Trade Aid Package). USDA data suggests that, so far, the department has sent $6.8 billion in payments to farmers.

County-Level Trade Assistance

The second round of trade assistance provided direct payments to growers based on planted acres (2018’s assistance was based on actual production with commodity-specific payment rates). For non-specialty crops, payments were announced at the county-level and ranged from a low of $15 per acre to a high of $150 per acre. Cover crops planted on acres prevented from being planted were also eligible for an MFP payment of $15 per acre, in addition to top-up payments on prevent plant indemnities.

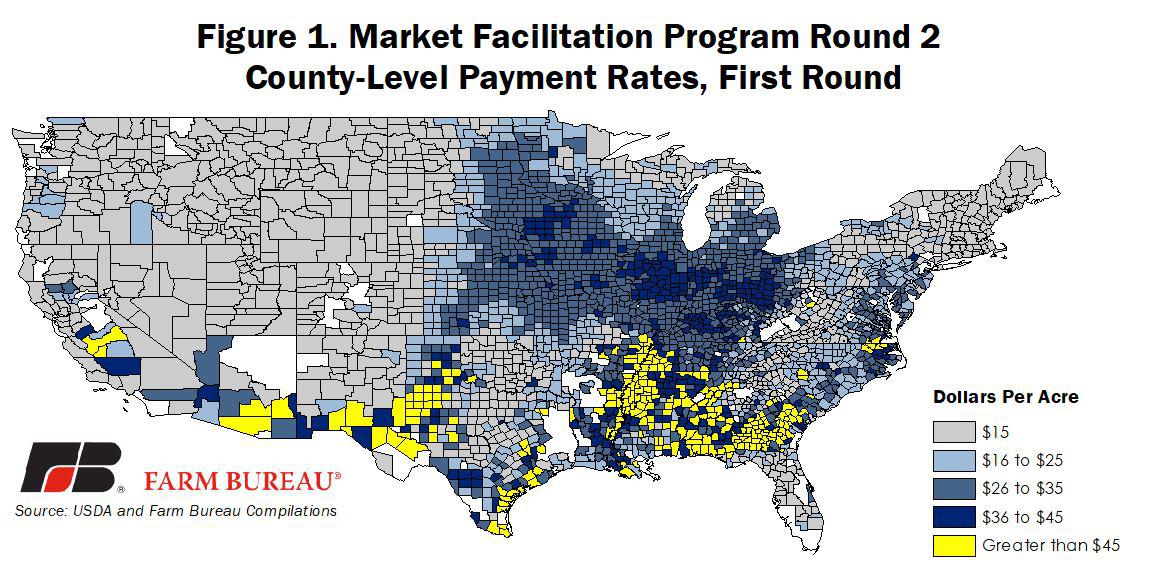

The first round of MFP payments was the higher of one-half of the county-level payment rate or $15 per acre. For example, a farmer with a $25 per-acre county-level payment rate would receive a first payment equal to $15 per planted acre. Figure 1 identifies the first round MFP payment rates by county. Non-specialty crops eligible for payment include alfalfa hay, barley, canola, corn, crambe, dried beans, dry peas, extra-long-staple cotton, flaxseed, lentils, long grain and medium grain rice, millet, mustard seed, oats, peanuts, rapeseed, rye, safflower, sesame seed, small and large chickpeas, sorghum, soybeans, sunflower seed, temperate japonica rice, triticale, upland cotton and wheat.

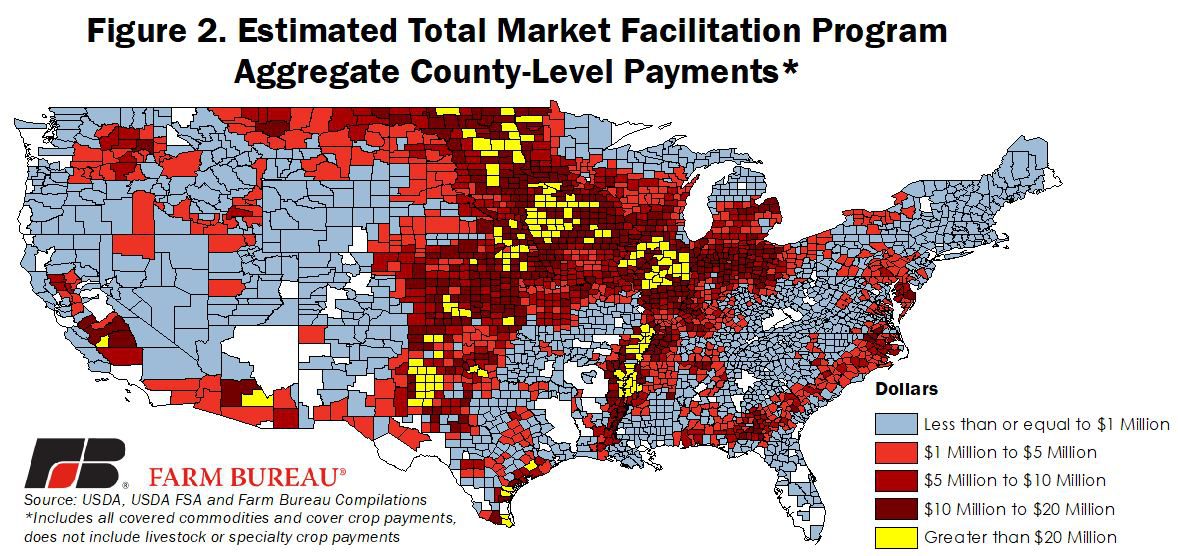

While county-level per-acre payment rates are higher in portions of the South, most of the acreage planted to crops eligible for MFP payments are found across the Corn Belt, along the Mississippi River and into portions of the Upper Midwest. Thus, when multiplying the total county-level payment rate by Farm Service Agency crop acreage data for eligible crops and cover crops, the financial support provided by MFP shifts from the South to the Midwest, Figure 2.

Actual Trade Assistance Payments

Data from USDA FSA reveals that as of Nov. 12, $6.8 billion in trade assistance has been provided for non-specialty crops, livestock and specialty crops. This total represents approximately 47% of the $14.5 billion in trade assistance planned by the administration.

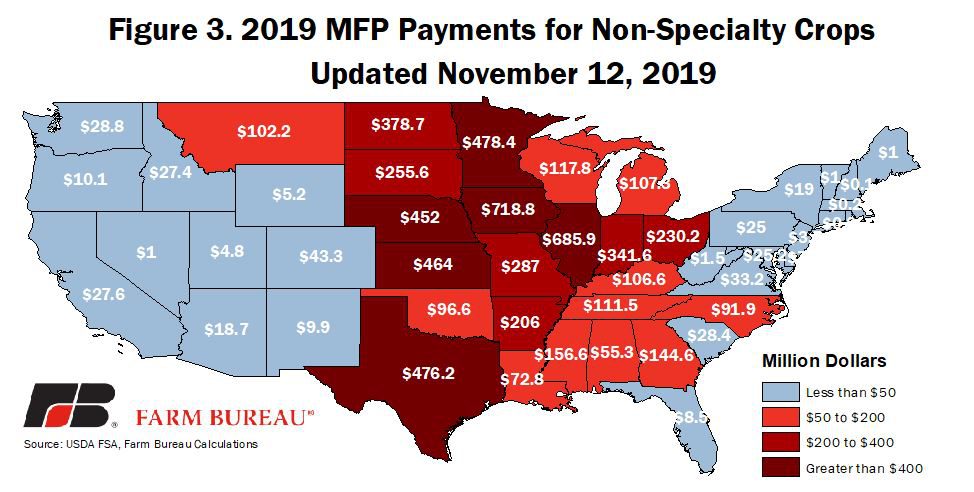

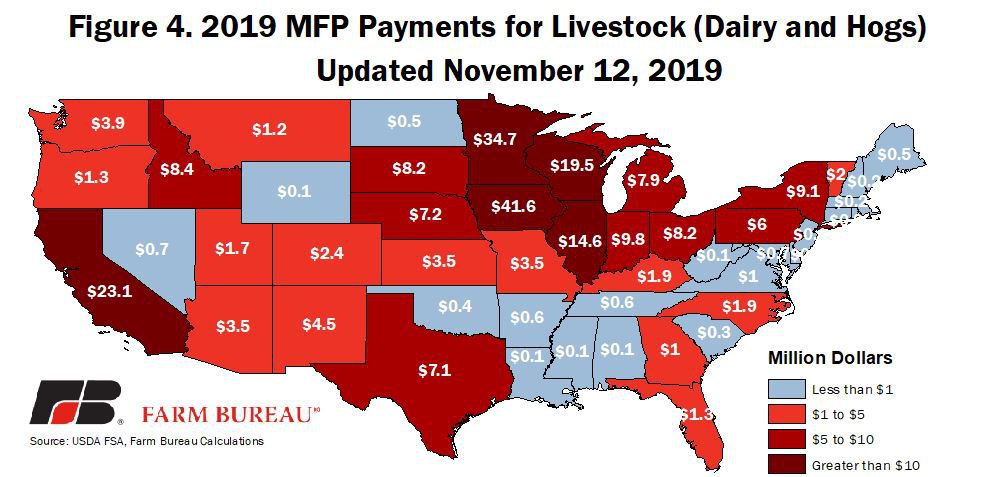

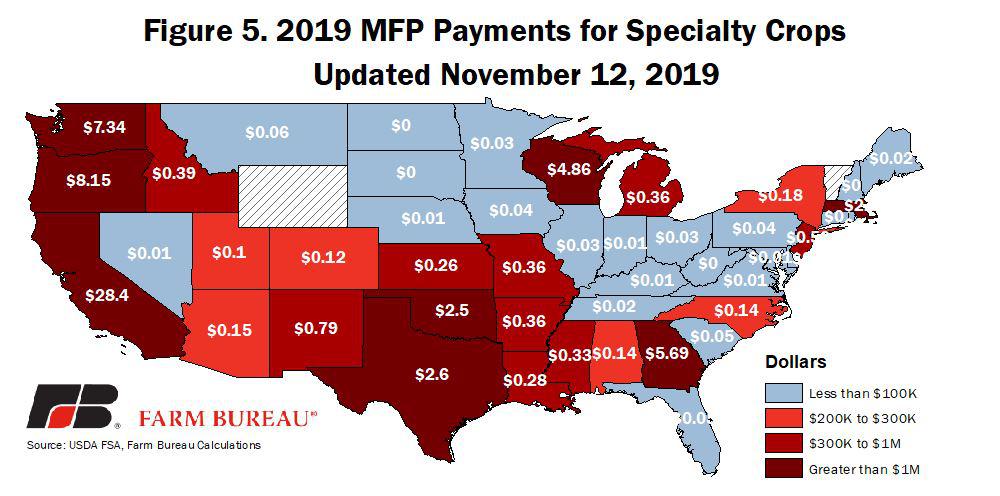

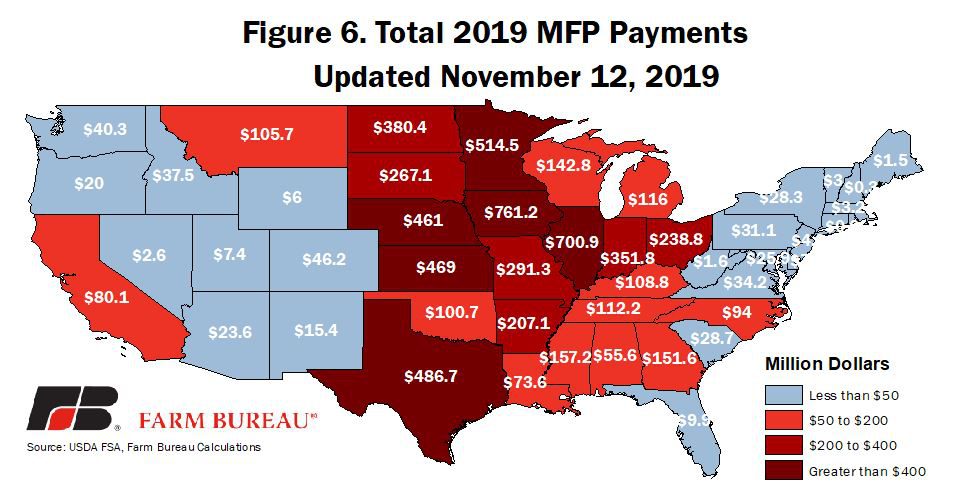

Non-specialty crop producers have received $6.5 billion; dairy and hog producers have received $246 million in support; and specialty crop growers have received $67 million in support. Specialty crops eligible for support include almonds, cranberries, cultivated ginseng, fresh grapes, fresh sweet cherries, hazelnuts, macadamia nuts, pecans, pistachios and walnuts. Figures 3 through 6 identify total first-round MFP payments for non-specialty crops, livestock, specialty crops and total payments by state as of Nov. 12. As evidenced, aggregate payments are concentrated in Midwest states such as Iowa, Illinois, Minnesota, Kansas and Nebraska. Texas, the nation’s largest cotton producer, ranks 4th in total MFP payments delivered through Nov. 12.

Summary

Many farmers have been impacted by unfair trade practices and the administration has responded by providing financial support in both 2018 and 2019. Currently, USDA has provided $6.8 billion in support in 2019, and more than $8.5 billion was provided in 2018. USDA recently signaled that the second round of 2019 trade assistance payments will be distributed in late November or December.

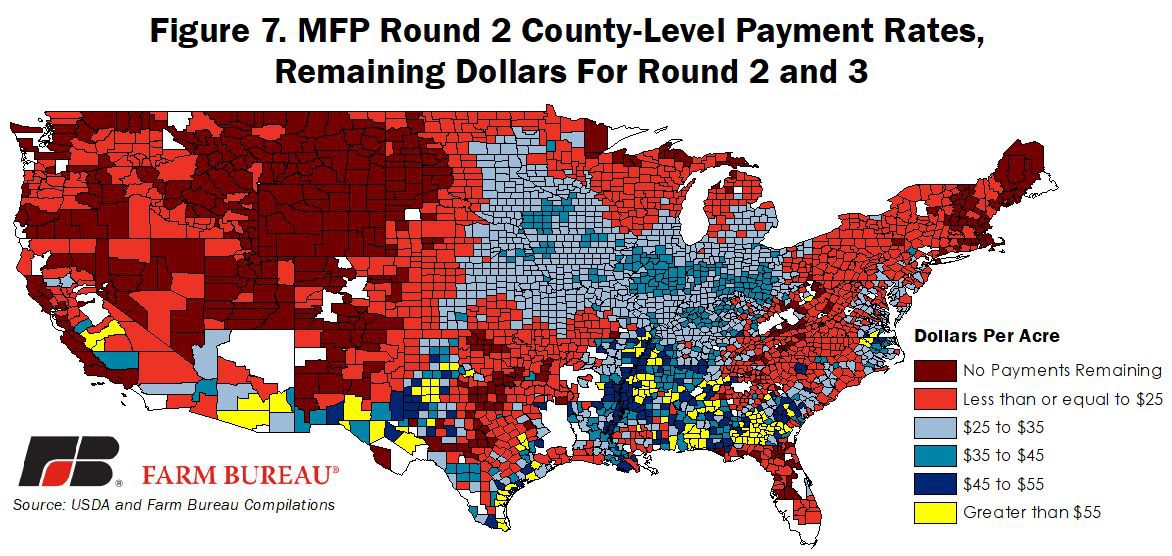

Details of the second round of trade assistance have yet to be announced, but any producer in a county with a county-average payment rate of $15 per acre will not receive a second or third round of payments. Also unknown is what percentage of the remaining county-level payments will be distributed in the second or even third round of support. Figure 7 identifies the amount of county-level support available for the second and potentially third round of MFP support.

Importantly, while up to $14.5 billion will be delivered to help agricultural producers offset losses due to multiple years of unfair retaliatory tariffs, little of this support will likely remain on the farm. With a projected $416 billion in farm debt, bankruptcies rising and loan repayment terms increasing, a large portion of the trade assistance dollars will probably be used to meet immediate financial needs, paying down debt and paying creditors.

Top Issues

VIEW ALL