The Verdict Is In: Farm Bankruptcies Up in 2019

photo credit: AFBF Photo, Mike Tomko

John Newton, Ph.D.

Vice President of Public Policy and Economic Analysis

While well below historical highs, Chapter 12 family farm bankruptcies in 2019 increased by nearly 20% from the previous year, according to recently released data from the U.S. Courts. Compared with figures from over the last decade, the 20% increase trails only 2010, the year following the Great Recession, when Chapter 12 bankruptcies rose 33%.

During the 2019 calendar year there were 595 Chapter 12 family farm bankruptcies, up nearly 100 filings from 2018 and the highest level since 2011’s 637 Chapter 12 filings. Given that there are slightly more than 2 million farms in the U.S., the 2019 bankruptcy data reveals a bankruptcy rate of approximately 2.95 bankruptcies per 10,000 farms, slightly below the rate of 2.99 filings per 10,000 farms in 2011.

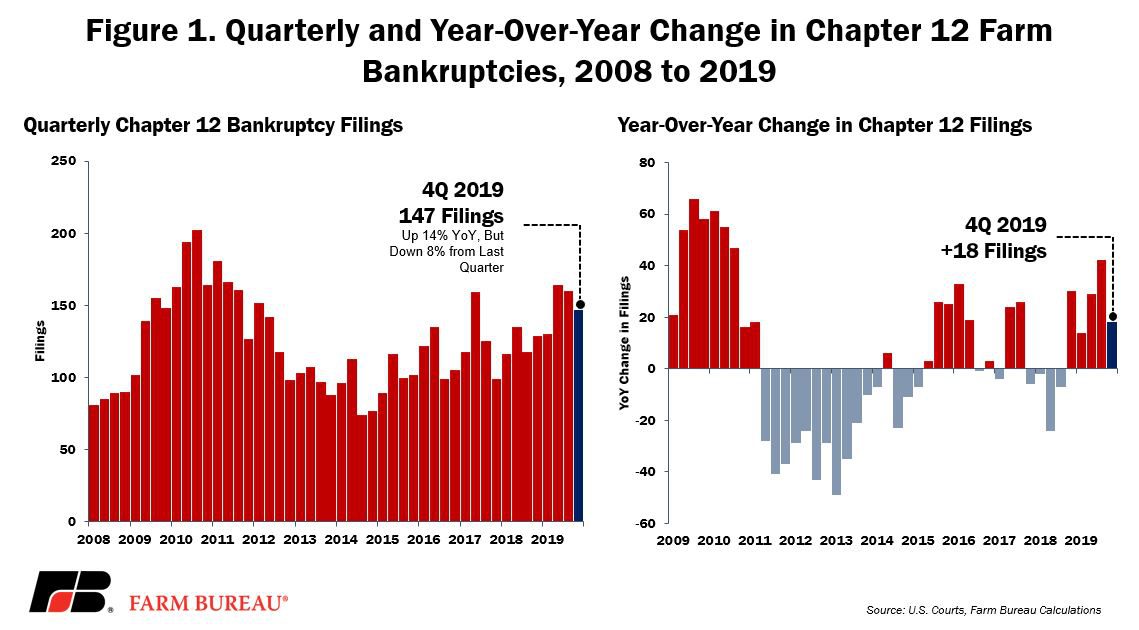

During the fourth quarter of 2019, there were 147 Chapter 12 bankruptcy filings, which was up 14% from the prior year but down 8% from the third quarter of 2019. On a year-over-year basis, Chapter 12 filings have increased for five consecutive quarters. The continued increase in Chapter 12 filings was not unanticipated given the multi-year downturn in the farm economy, record farm debt, headwinds on the trade front and recent changes to the bankruptcy rules in 2019’s Family Farmer Relief Act, which raised the debt ceiling to $10 million (What is Chapter 12 Family Farmer Bankruptcy?, Farm Bankruptcies Rise Again and Outlook Improves for 2019 Farm Economy, but Uncertainty Remains).

Chapter 12 Bankruptcies by State

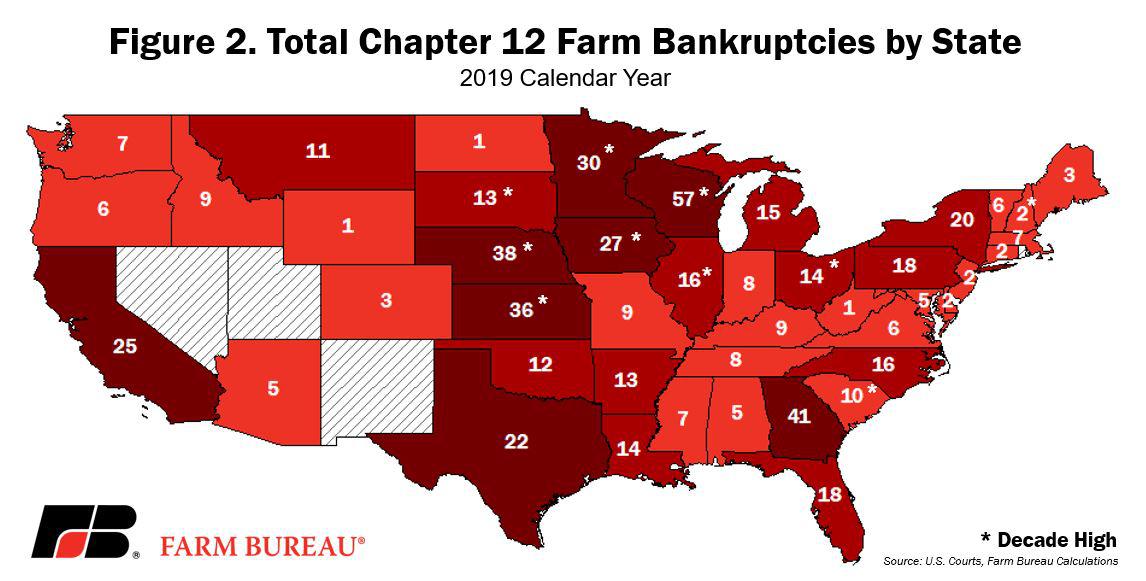

During the 2019 calendar year, Chapter 12 farm bankruptcies were the highest in Wisconsin at 57 filings. Wisconsin farm bankruptcies were up 8 filings from the prior year and were also at the highest level in a decade. Following Wisconsin, Georgia had 41 Chapter 12 filings in 2019, which was up 15 filings from 2018. Chapter 12 filings were at, tied with or above decade-high levels in 10 states: Iowa, Illinois, Kansas, Minnesota, Nebraska, New Hampshire, Ohio, South Carolina, South Dakota and Wisconsin, Figure 2.

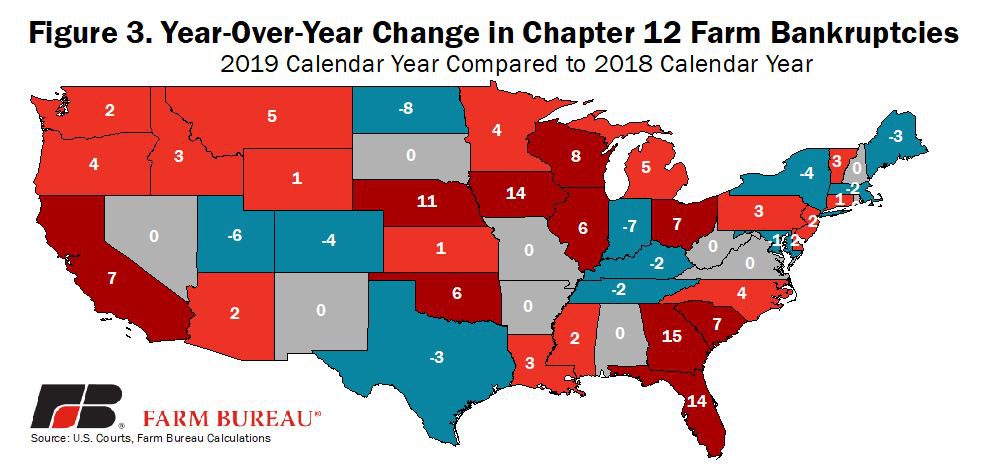

Chapter 12 farm bankruptcies rose in many states across the Midwest, West and Southeast. Georgia had the largest increase — 14 more filings than the prior year. Following Georgia were Iowa and Florida with 14 additional Chapter 12 bankruptcy filings and Nebraska with 11 additional filings, Figure 3.

Chapter 12 Bankruptcies by Region

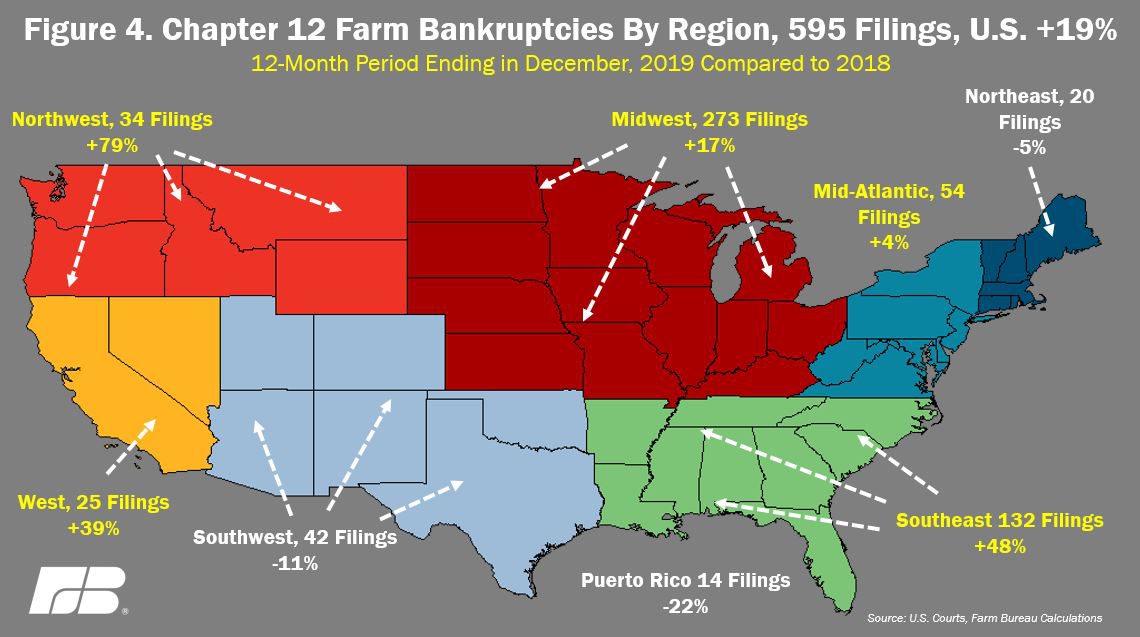

All but three regions of the U.S. experienced higher bankruptcy rates in 2019 compared to 2018. Nearly 46% of the Chapter 12 filings were in the 13-state Midwest region, followed by 22% in the Southeast. The Midwest had 273 Chapter 12 filings, up from 234 filings in 2018, while the Southeast had 132 filings, up from 89 filings the previous year. Figure 4 highlights Chapter 12 bankruptcy filings by region and the year-over-year change.

Bankruptcies Over the Last Decade

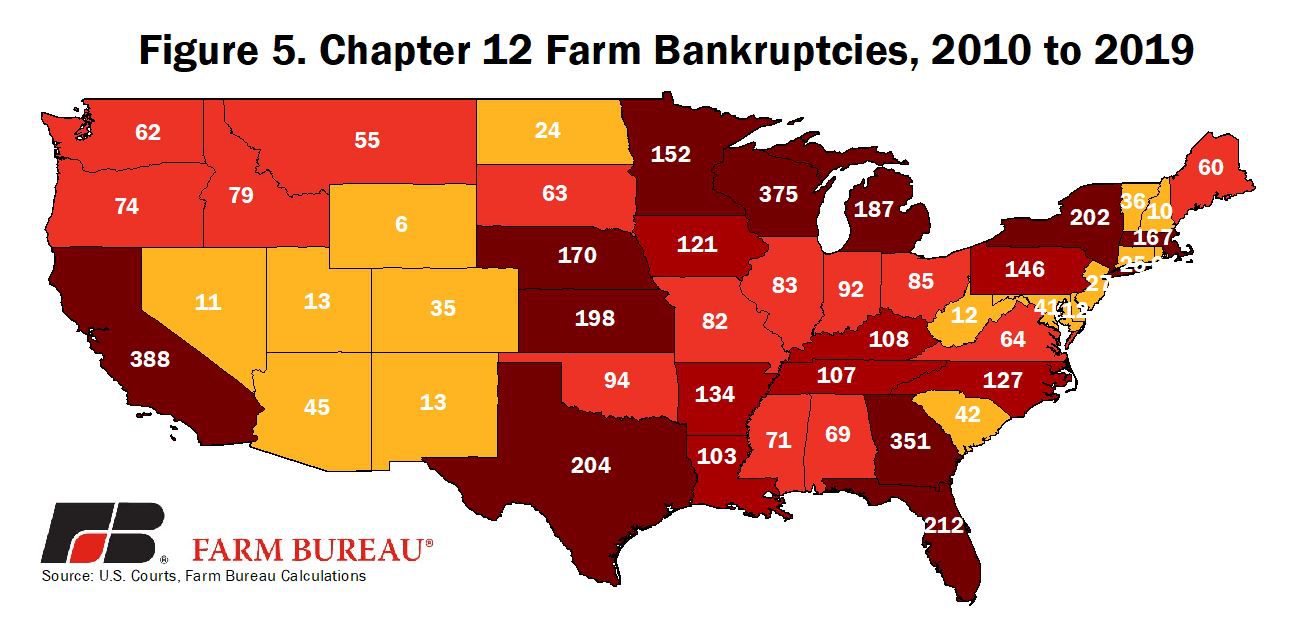

Over the last decade, there have been more than 5,000 Chapter 12 farm bankruptcies across the U.S., representing approximately a quarter of 1% of all farm operations during this time period. At 388 filings, Chapter 12 filings over the last decade were the highest in California, followed by Wisconsin at 375 filings and Georgia at 351 filings. Figure 5 highlights Chapter 12 farm bankruptcies over the last decade.

Summary

Depending on perspective, net farm income in 2019 inflation-adjusted dollars is either down 33% from a record high or up nearly 40% from the decade low set in 2016. Regardless of perspective, net farm income in 2019 is slightly above the 20-year average but was supported in large part by the Trump administration’s efforts to financially shield farmers from unfair retaliatory tariffs.

Without this support, farm-related income from crop and livestock sales in 2019 inflation-adjusted dollars would have been at the second-lowest level in the last decade at $63.6 billion. The corollary to this is that farm bankruptcies could have been worse considering the record-high farm debt of $415 billion (in nominal terms) and the likely difficulties servicing this debt without the revenue from the Market Facilitation Program.

The Trump administration is not expected to announce a third round of trade assistance given the welcome trade news with respect to Japan, USMCA and a China Phase 1 deal. As a result, farm financial conditions in 2020 will come down to – notwithstanding any other black swans -- a race between the additional grain and oilseed supplies likely to come online following a record prevented planting year and any demand boosts for U.S. agriculture that results from these new and enhanced trading opportunities.

Farm Bureau has been invited to participate in USDA’s 96th annual Agricultural Outlook Forum. Your participation in this short and informal survey will help Farm Bureau staff communicate the general sentiment of the industry and our membership on the health and outlook for the U.S. farm economy.

Take the survey now at www.fb.org/farmeconomy

Top Issues

VIEW ALL