Transfer Tax Could Impact a Huge Portion of US Farm Production

TOPICS

Taxes

photo credit: Getty Images

Veronica Nigh

Former AFBF Senior Economist

Potential changes to capital gains taxation at death for family farms has been a hot topic in agricultural circles over the last six months. Capital gains-related studies from EY, Texas A&M, University of Kentucky and Iowa State University released over the spring and summer illustrate the potential impacts to U.S. farmers and ranchers. Last week, USDA’s Economic Research Service released an analysis of the American Families Plan, which proposes to eliminate stepped-up basis for inherited assets greater than $1 million for individuals’ estates and $2 million for married couples’ estates while deferring capital gains tax liability on business assets as long as the business remains family-operated. The results echo many of the points that have been made by economists and tax professionals throughout the ongoing discussion.

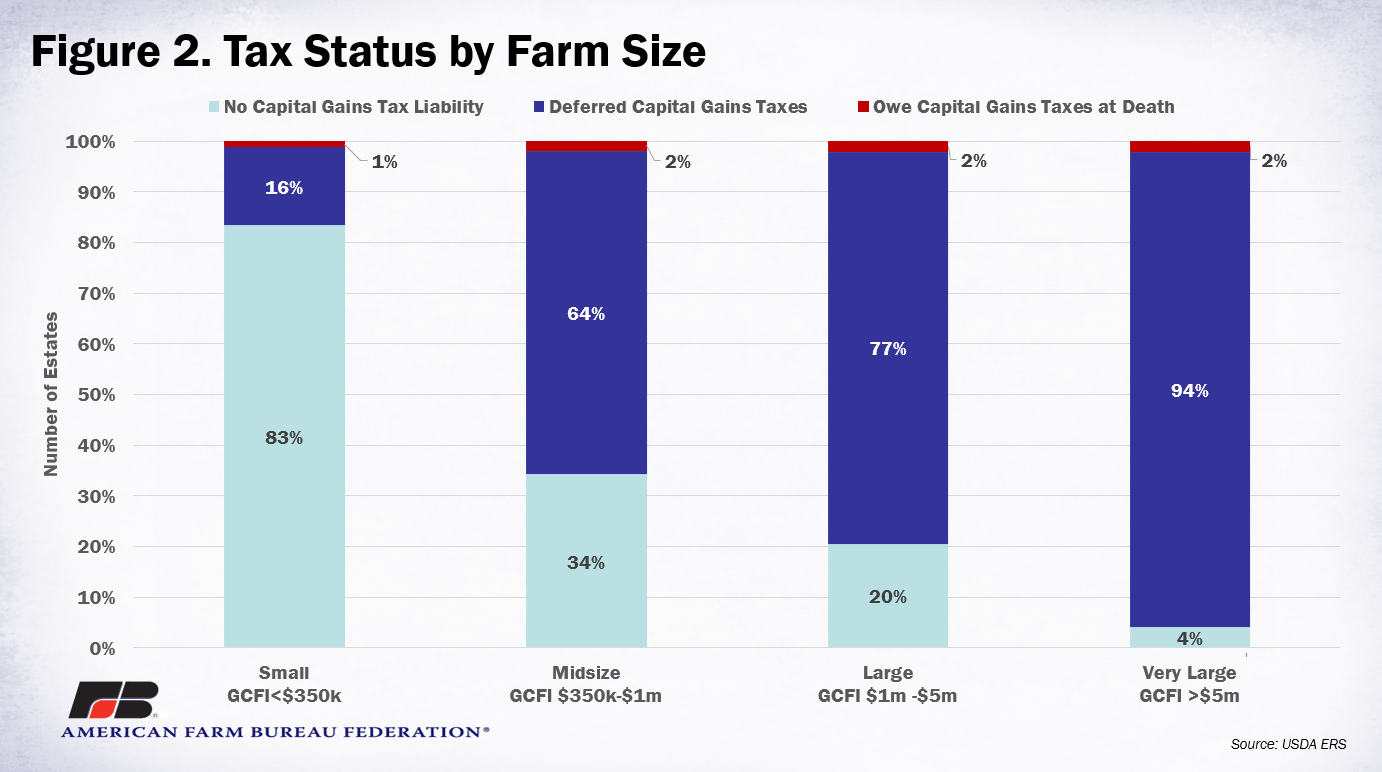

Much of the debate around the AFP proposal has centered around the “exemption” or more accurately, the deferral of capital gains liability for farms that continue to be family-operated after the inter-generational transfer. Some analysts equate the deferral to no impact. In their view, there is either capital gains tax owed at the time of death or there is not. ERS’ model, which indicates that under the proposed plan only 1.1% of created estates would owe a capital gains tax at death, seems to support this view of the AFP. Looking at it through this lens, 98.9% of farms are not impacted by the changes.

However, other analysts, including many economists, tax practitioners and the American Farm Bureau Federation, argue that deferred capital gains taxes can have significant implications for a farm, even if it continues to be operated by the family. This is because it’s easy to say that taxes will be deferred, but it’s hard to write that deferral into law in a way that matches intent, and even harder for the farm’s operators to maintain that deferral. There are many ways that “continues to be operated by the family” could go afoul, including how “family” is defined by the IRS versus how USDA defines it, changes to family status, the rules around recapture, and changes to the rules around material participation, just to name a few. So, while the intent of deferring taxes may be good, those deferred taxes can hang over an operation like a dark cloud. Deferred taxes can impact a farmer’s ability to secure operating loans, make organization changes and generally run the farm or ranch optimally. Importantly, ERS’ model shows that under the proposed plan, 18.2% of created estates would owe no tax at death but could potentially have a deferred tax on farm gains.

When deferred taxes are not considered the same as no taxes, the importance of the data source utilized by ERS in this study, USDA's Agricultural Resource Management Survey, becomes more evident. ARMS is the only national survey that provides observations of the economics of farm businesses, including income statements, balance sheets and financial indicators and the demographics of the American farm household—all designed to be statistically representative of all types of farm households and farm regions of the country. Jointly sponsored by ERS and the USDA’s National Agricultural Statistics Service, ARMS has been conducted annually since 1996.

For this study, ARMS data was examined across farm size; small farms have gross cash farm income (GCFI) less than $350,000, midsize farms have GCFI between $350,000 and $1 million, large farms have GCFI between $1 million and $5 million, and very large farms have GCFI greater than $5 million. As a reminder, GCFI is annual income before expenses and includes cash receipts, farm-related income and government farm program payments. It is important to note the significant difference between GCFI and actual return to operators – the inclusion of expenses. Over the last decade, returns to operators have averaged just 17% of GCFI. So please keep this in mind while thinking about the size of farms.

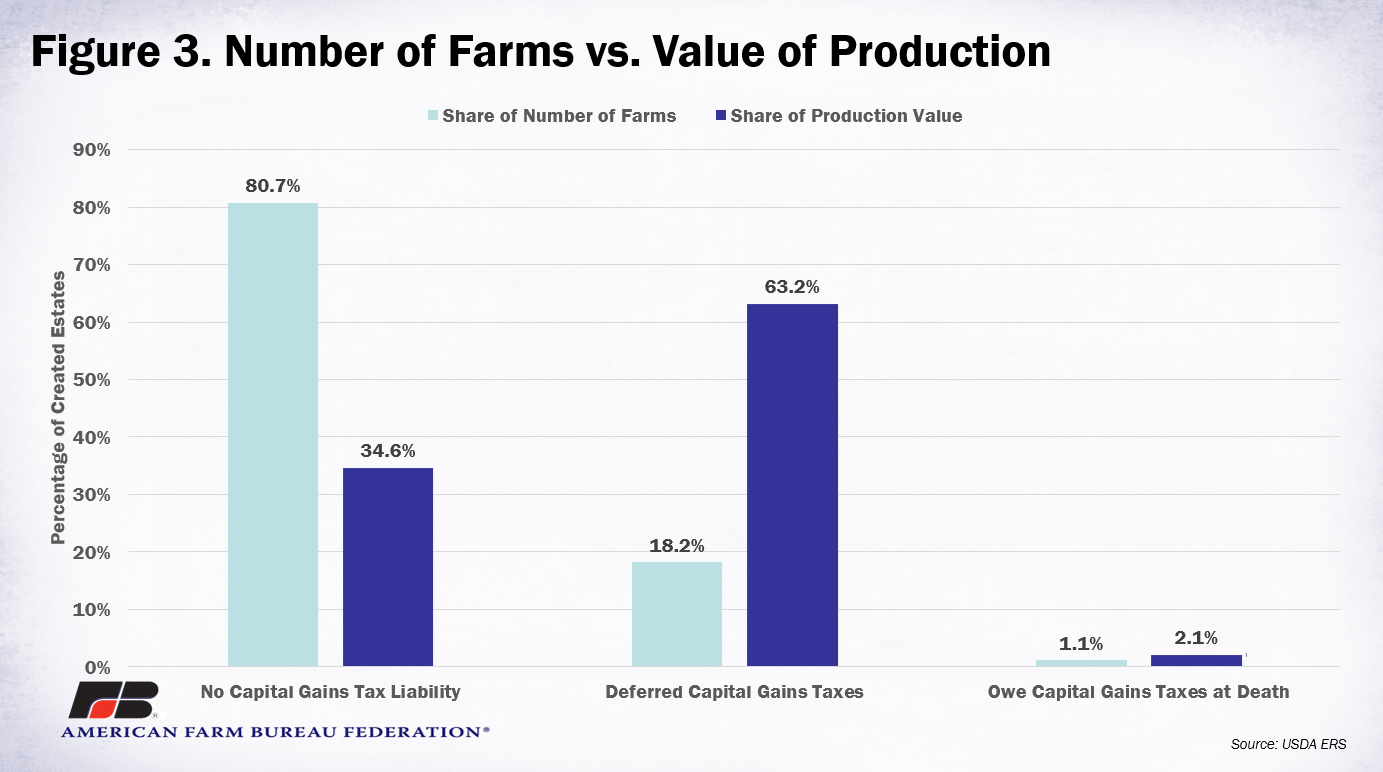

When grouped all together, the ERS study found that 1.1 % of farms would owe capital gains taxes at death, 18.2% would not owe capital gains taxes at death but could have deferred tax liability if the farm assets do not remain family-owned and operated, and 80.7% would have no change to their capital gains tax liability. However, when the impact of the AFP proposal is viewed through the lens of farm size, we learn more about the types of farms that would be impacted. The study found that among small farms with GCFI less than $350,000, 83% would have no capital gains liability, 16% would have deferred liability and 1% would owe capital gains taxes upon death. Perhaps not surprisingly, the results change significantly as farm size increases. As depicted in Figure 2, 64% of mid-size farms, 77% of large farms and 94% of very large farms would have deferred capital gains tax liability as a result of AFP.

Another interesting lens through which to view the results is the value of production for impacted estates. With this in mind, the 18.2% of created estates that would not owe capital gains taxes at death but could have deferred tax liability accounted for the vast majority - 63.2% - of the value of production of created estates. The 80.7% of created estates that would not owe capital gains taxes at death accounted for a little over a third – 34.6% - of the value of production of created estates. The 1.1% of created estates that would owe capital gains taxes at death only accounted for 2.1% of the value of production of created estates.

Conclusion

ERS’ The Effect on Family Farms of Changing Capital Gains Taxation at Death is an important contribution to the debate on changes to capital gains taxation. The utilization of ARMS data helps to specify the share of created estates that could potentially have deferred capital gains taxation hanging over inter-generational farms. The usage of ARMS data also adds important context in highlighting that these are the very farms producing the vast majority of the nation’s food, feed and fiber.

Top Issues

VIEW ALL