What’s in the Inflation Reduction Act for Agriculture?

TOPICS

USDA

photo credit: AFBF Photo/Morgan Walker

Shelby Myers

Former AFBF Economist

Formerly known as the Build Back Better Act (BBBA), the budget reconciliation bill, after extensive negotiations and reworking, was finalized as the Inflation Reduction Act (IRA) of 2022, totaling roughly $770 billion. Since the budget reconciliation process was used, the bill only needed a simple majority in the Senate to pass, meaning it only needed 51 votes, rather that the 60 votes often needed to avoid procedural blocks. The Senate passed the bill on Sunday, Aug. 7, along a party-line 50-50 vote requiring Vice President Harris to cast the deciding, tie-breaking vote. The House passed the bill on Friday, Aug. 12, also along party lines, 220-207.

The final bill includes nearly $40 billion for agriculture, forestry and rural development. This includes nearly $20 billion in funding for the Agricultural Conservation Easement Program (ACEP), Conservation Stewardship Program (CSP), Environmental Quality Incentives Program (EQIP) and Regional Conservation Partnership Program (RCPP), plus technical assistance. In addition, it includes $14 billion for rural development to support the development of renewable energy and spending on biofuels infrastructure. The bill also provides $4 billion to mitigate the impacts of drought in the Western Reclamation states, with priority given to the Colorado River Basin and other basins experiencing comparable levels of long-term drought.

This Market Intel article reviews the agriculture-related provisions that are included in the bill.

Conservation Funding for Working Lands

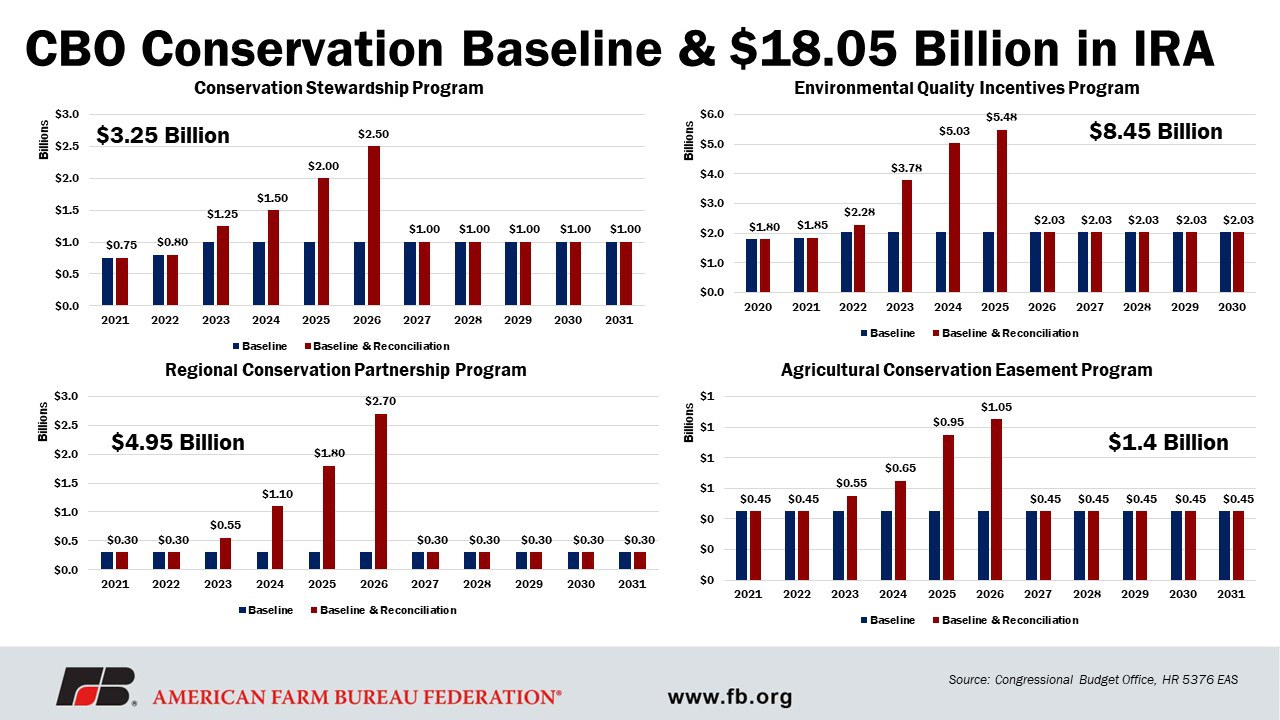

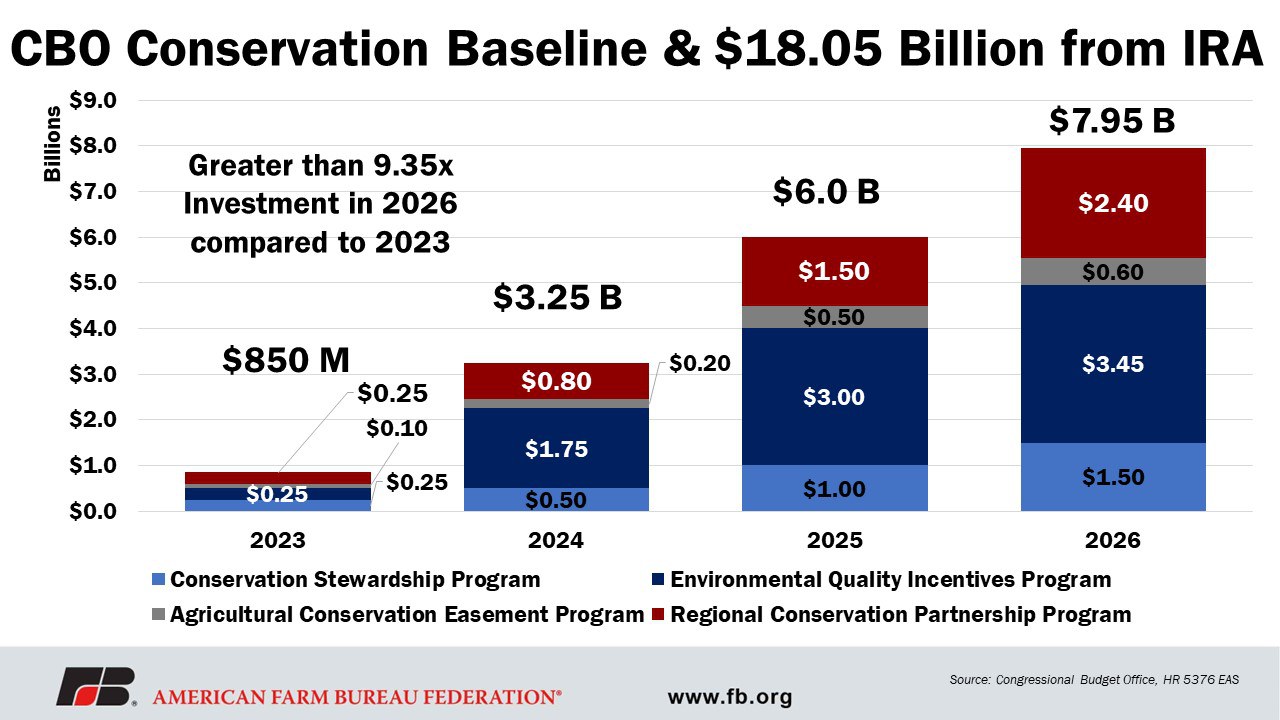

The IRA would provide a total of approximately $19.5 billion for agricultural conservation efforts. The bill will add about $18.05 billion in additional funding for existing farm bill working lands conservation programs through fiscal year 2026 and extend the programs’ authorities through fiscal year 2031. The expectation is that USDA could spend the additional money included in the IRA beyond fiscal year 2026 but not beyond fiscal year 2031. This will likely be a factor in conversations about the 2023 farm bill as the IRA language related to these four programs would extend their authorizations through 2031, as well as extend authorization of the Conservation Reserve Program, though it was not provided additional funding in the bill.

In total, EQIP was appropriated $8.45 billion, RCPP was appropriated $4.95 billion, CSP was appropriated $3.25 billion and ACEP was appropriated $1.40 billion. Over the next four years, the IRA invests 9.35 times the amount of funding previously included in the 2018 farm bill for the four working lands programs.

In addition to the funding added to these programs that provide financial and technical assistance for voluntary adoption of conservation practices on agricultural lands, IRA also includes an additional $1 billion in funding for conservation technical assistance, $300 million for a carbon sequestration and greenhouse gas emissions quantification program, and $100 million in funding for administrative expenses.

Forestry

The IRA provided a cumulative total of $5 billion for forest management, planning and restoration activities for federal and nonfederal forests. Broken down, there is $2.15 billion for management activities of the National Forest System. Activities include funding for hazardous fuel reduction or vegetation management projects on National Forest System lands, for inventorying and protecting old-growth and mature forests on National Forest System lands, and for improving environmental reviews. The other $2.75 billion is for grants and financial assistance to be used for nonfederal forest management activities.

Extension of the Biodiesel Income Tax Credit

While the previous Build Back Better legislation proposed an extension of the biodiesel and renewable diesel blenders tax credit through 2031, IRA extends biodiesel, alternative fuel and second-generation biofuel tax credits only through the end of 2024. The current tax credit is a $1-per-gallon biodiesel tax credit for producers or blenders of pure biodiesel and a $1-per-gallon renewable diesel tax credit for producers or blenders of biomass-based diesel or diesel/renewable diesel blends.

Renewable Energy

The IRA provides a total of $3 billion for renewable energy projects in rural areas. This includes about $1 billion for electric loans for renewable energy under the Rural Electrification Act with the option for USDA to use the funding to make loans for electric generation from renewable energy resources, including for projects that store electricity. There is also $1.7 billion for eligible projects under the popular farm bill program known as the Rural Energy for America Program (REAP). Another $304 million is for grants and loans for underutilized renewable energy technologies, along with technical assistance for previously mentioned REAP projects. Additional spending of $500 million is for grants intended to increase the sale and use of agricultural commodity-based fuels through infrastructure improvements for blending, storing, supplying or distributing biofuels.

The IRA specifically provides $9.7 billion to rural cooperatives for assistance for rural electric systems to purchase renewable energy, renewable energy systems, zero-emission systems, carbon capture and storage systems, and others.

One more energy provision in the IRA that impacts agriculture is $5 million provided to the EPA to carry out the Renewable Fuel Standard program, in part, for data collection and analyses of lifecycle greenhouse gas emissions of a fuel and $10 million for new grants to support advanced biofuels.

Western Drought Mitigation

Included in the IRA are provisions that provide $4 billion in fiscal year 2022 through fiscal year 2026 for grants, contracts or financial assistance agreements to mitigate the impacts of drought in the Reclamation states, with priority given to the Colorado River Basin and other basins that are experiencing comparable levels of long-term drought. The funding may go toward compensation for a temporary or multiyear voluntary reduction in diversion of water or consumptive water use, voluntary system conservation projects or ecosystem and habitat restoration projects to address issues directly caused by drought in a river basin or inland water body.

Agricultural Credit and USDA Agency Provisions

Included in the IRA is debt relief for distressed borrowers of direct or guaranteed loans administered by the Farm Service Agency and assistance for underserved farmers and ranchers. This funding replaces provisions first included in the American Rescue Plan Act of 2021. This includes $3.1 billion to provide payments for the cost of loans or loan modifications. About $125 million is provided for USDA technical assistance and customer service support for underserved farmers, ranchers and foresters. In the credit provisions, an additional $250 million is provided in grants and loans for eligible entities to improve land access for underserved farmers, ranchers and forest landowners, including veterans, limited resource producers, beginning farmers and ranchers, and farmers, ranchers and forest landowners living in high poverty areas. USDA is called upon to create an equity commission and is appropriated a budget of $10 million. An appropriated amount of $2.2 billion is included for financial assistance to farmers, ranchers or forestland owners determined to have experienced discrimination in a USDA lending program before Jan. 1, 2021. An appropriation of $24 million was also included for administrative costs associated with carrying out this section of the bill.

In addition, USDA is appropriated $250 million to support and supplement agricultural research, education and Extension. This can be used in the form of scholarships, internships and pathways to the agricultural sector or federal employment.

Sustainable Aviation Fuel Standards

The IRA establishes a new sustainable aviation fuel credit through fiscal year 2024 that multiplies the number of gallons of sustainable aviation fuel by the sum of $1.25 plus an applicable supplementary amount. That applicable supplementary amount is the amount equal to 1 cent for each percentage point by which the lifecycle greenhouse gas emission reduction percentage for such fuel exceeds 50%. However, the applicable supplementary amount cannot exceed 50 cents.

SAF Credit = $1.25 x (# of gallons of SAF) + [($0.01 x (Percentage Point >= 50% lifecycle GHG emissions reduction)) < $0.50]

For agriculture, the term “sustainable aviation fuel” means liquid fuel that meets the ASTM International Standard D7566 or the Fischer Tropsch provisions of ASTM International Standard D1655, Annex A1. In the latter provisions, feedstocks can be included in the blending of alternative jet fuels that would be considered sustainable aviation fuel in this bill.

Offsets

Farmers and ranchers were effective in the campaign to prevent the inclusion of tax provisions that would have been harmful to agriculture – such as the repeal of stepped-up basis, a higher tax rate on capital gains, and the repeal of the enhanced estate tax threshold. The majority of the revenue for the bill was raised by reforming the Medicare prescription drug program and instituting a corporate book minimum tax for companies that make more than $1 billion. However, at the last minute, to make up revenue that was lost because of changes made to the bill during debate, the last amendment adopted, offered by Sen. Mark Warner (D-Va.), swapped out a one-year extension of the state and local tax deduction cap instituted by the Tax Cuts and Jobs Act of 2017 for a two-year extension of the excess business loss limitation provision for 2027 and 2028. Without the extensions of other important provisions affecting small businesses, like the lower individual rates and 199A business income deduction, the extension of the excess business loss limitation amounts to a $50 billion tax increase on pass-through businesses.

Also included in the bill is $80 billion dollars in additional funding for the Internal Revenue Service over the next decade with the intention to help raise an additional $200 billion in revenue through enhanced compliance, i.e., audits.

Summary

On Aug. 12, the House passed, on a party-line vote, the $750 billion Inflation Reduction Act after the Senate also voted along party lines to pass the bill on Aug. 7. The bill includes provisions to use fiscal year 2022 reconciliation instructions to raise revenue and the bill’s stated goal is to lower prescription drug costs, fund new energy, climate, and health care initiatives and reduce budget deficits.

Provisions specific to agriculture include nearly $40 billion for spending on programs and initiatives ranging from farm bill working lands conservation and technical assistance to renewable energy and biofuels. There are also funds provided for rural development and drought mitigation. As Congress moves on from this bill, questions are being raised about provisions that impact farm bill programs and whether or not it changes the policy conversations and/or political landscape for the 2023 farm bill.

Top Issues

VIEW ALL