ARC-County, A Bird in The Hand for Some in 2019

TOPICS

Soybeans

photo credit: Mark Stebnicki, North Carolina Farm Bureau

John Newton, Ph.D.

Vice President of Public Policy and Economic Analysis

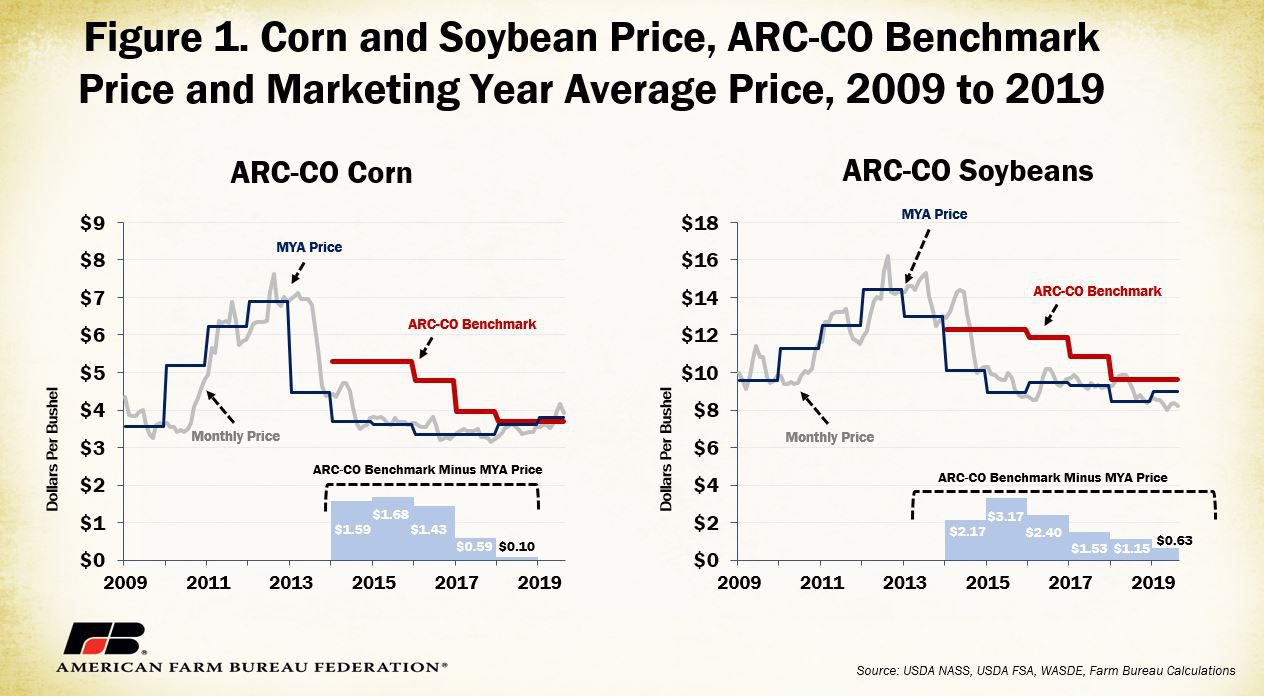

Following five consecutive years of lower corn and soybean prices, due in large part to ample supplies and reduced demand, the revenue support provided by Agriculture Risk Coverage-County Option is fading. The benchmark price for corn for 2018 ARC-CO coverage was $3.70 per bushel, down 30%, or $1.59 per bushel, from the coverage provided during the 2014 and 2015 marketing years. Similarly, the benchmark price for soybeans in 2018 was $9.63 per bushel, down 20%, or $2.63, from 2014 and 2015 levels.

The benchmark prices for corn and soybeans for the 2019 crop year are also $3.70 per bushel and $9.63 per bushel, respectively, Figure 1. Program payments for 2018 ARC-CO coverage will be issued this year and farmers are eligible to enroll for 2019 ARC-CO coverage through March 15, 2020. Today’s Market Intel reviews the 2018 ARC-CO payment rates and the revenue guarantee for the 2019 coverage year. Payments for 2019 ARC-CO coverage will be delivered in late 2020, after the close of the marketing year.

Agriculture Risk Coverage-County Option was introduced in the 2014 farm bill and reauthorized in the 2018 farm bill. ARC-CO is a county-based program that makes deficiency payments to farmers when the actual crop revenue for a marketing year, defined as the product of the county average yield and marketing year average price, falls below 86 percent of a benchmark revenue guarantee, defined as the product of the five-year Olympic moving average county yield and 5-year OMA crop price. The OMA is a five-year average that excludes the maximum and minimum from the calculation. For the 2019 coverage year, the OMA will average prices and yields for the five-year period beginning in 2013. This sample period was moved back administratively following the 2018 farm bill

ARC-CO Benefits for 2018

For the 2018/19 marketing year, the marketing year average price for corn was $3.61 per bushel, 9 cents below the benchmark price of $3.70 per bushel. Given these prices, a yield decline of 12% relative to the OMA yield was needed to trigger an ARC-CO payment for corn, i.e., -12%=(86%×3.70)÷3.61.

The national average corn yield in 2018 was 176.4 bushels per acre, in line with prior-year levels and above the national five-year OMA. It follows then that in many counties corn yields were above the county-level OMA. As a result, across many of the corn-producing areas of the U.S. the actual county revenue was greater than the revenue guarantee, resulting in no program payments from ARC-CO.

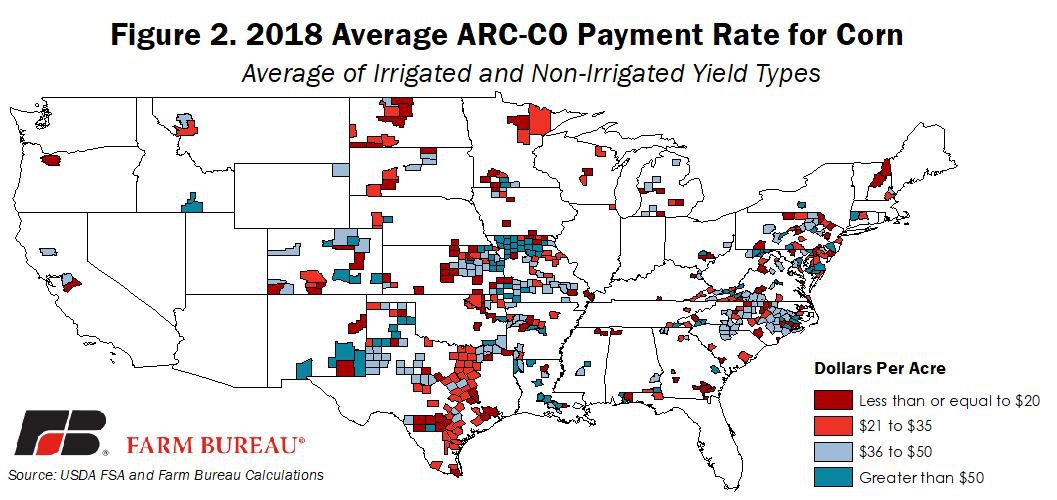

Nearly 500 counties triggered an ARC-CO payment for corn. In those counties, the average ARC-CO payment was $34 per acre and ranged from 46 cents per acre in Coos County, New Hampshire, to $89 per acre in Chaves County, New Mexico, where crop yield fell by 22% compared to the OMA. Figure 2 highlights average ARC-CO program payments for both irrigated and non-irrigated corn for the 2018 coverage year.

For the 2018/19 marketing year, the average price for soybeans was $8.48 per bushel, $1.15 cents below the benchmark price of $9.63 per bushel. Given these prices, a yield decline of 2% relative to the OMA yield was needed to trigger an ARC-CO payment for soybeans, i.e., -2%=(86%×9.63)÷8.48.

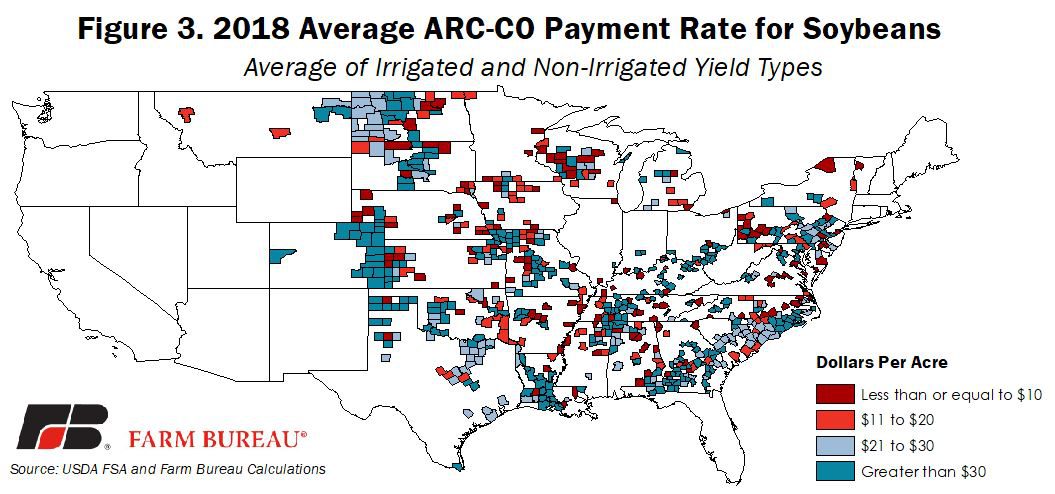

Like corn, the national average soybean yield was in line with prior-year levels, and in many counties the soybean yield was above the five-year OMA yield, resulting in slightly more than 650 counties triggering an ARC-CO payment for soybeans. Payments ranged from a low of 16 cents per acre in portions of Missouri and Pennsylvania to more than $50 an acre in portions of Kansas, Texas and Nebraska, among others, Figure 3.

What to Expect in 2019?

The OMA prices for corn and soybeans in 2019 remain unchanged from 2018 due to an administrative tweak to shift the averaging period following the 2018 farm bill. Current projections are for a MYA corn price of $3.80 per bushel, above the benchmark price of $3.70, and for an MYA soybean price of $9.00 per bushel, below the benchmark price of $9.63 per bushel.

While benchmark prices remain unchanged, modifications to the yields used to determine the revenue guarantee (What’s in Title I of the 2018 Farm Bill for Field Crops?) will enhance the revenue support provided by ARC-CO in 2019.

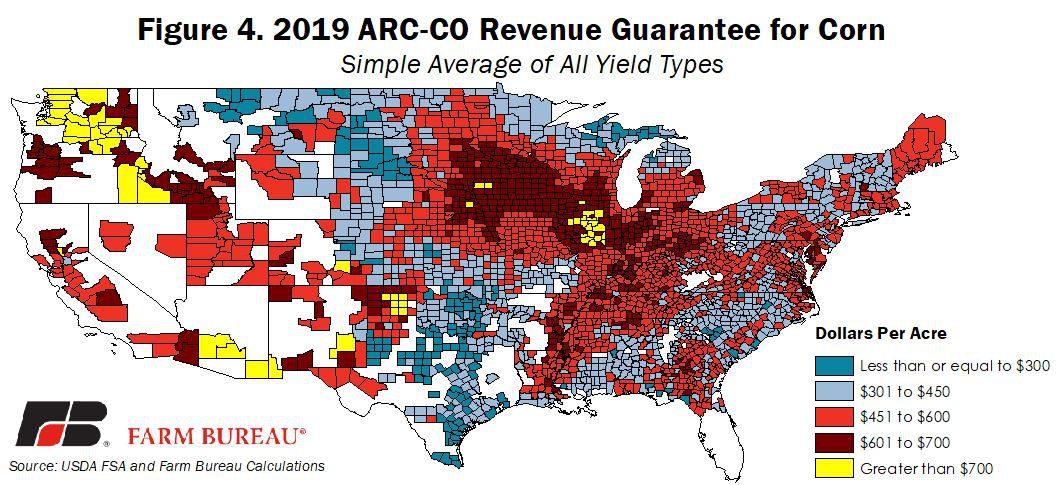

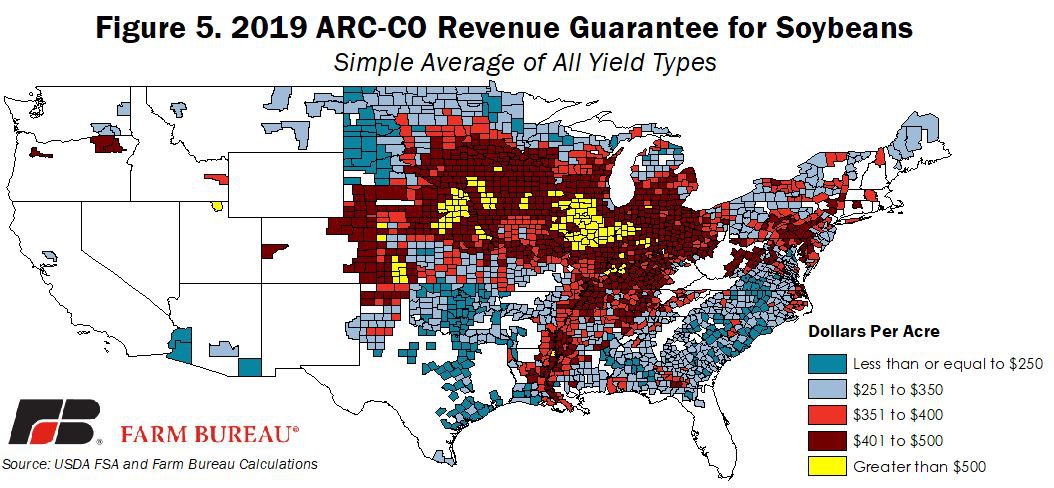

USDA Farm Service Agency data reveals that for corn the average revenue guarantee, i.e., 86% multiplied by the benchmark revenue, ranges from less than $300 per acre outside the Corn Belt to more than $700 per acre in portions of Illinois and in areas with a large percentage of irrigated cropland. Like corn, soybean revenue guarantees are lower outside the Corn Belt, but they exceed $500 per acre across portions of Indiana, Illinois, Kansas and in Nebraska.

Summary

Given that 2019 crop prices are projected to be higher than in 2018, the yield declines needed to trigger ARC-CO will need to be more substantial. For corn, the yield decline relative to the OMA needed to trigger ARC-CO is 16%, and for soybeans, the yield decline is 8%. Given the historical delays in planting, record rainfall this spring and adverse weather during harvest, yields are expected to be lower, increasing the probability of an ARC-CO payment, if current price expectations hold.

Farmers are eligible to enroll for 2019 ARC-CO coverage through March 15, 2020, and must also evaluate the benefits of the Price Loss Coverage program. PLC makes a deficiency payment when MYA prices fall below a statutory reference price. The decision made in 2019 is binding for both the 2019 and 2020 crop years, after which farmers will be able to elect annually between ARC-CO and PLC for the remainder of the life of the 2018 farm bill.

Current projections for corn and soybean prices are above PLC-triggering levels of $3.70 per bushel and $8.40 per bushel, respectively. Meanwhile, many counties in the U.S. that experienced adverse growing and harvesting conditions could see county-average yields low enough to trigger ARC-CO. However, county-average yields may not be published by USDA prior to the enrollment deadline, making the ARC-CO or PLC decision more complicated.

Moreover, while PLC is unlikely to trigger in 2019 for corn or soybeans, 2020 holds more uncertainty. Growers that elect ARC-CO in 2019 may not see any program payments in 2020 if yields and crop revenues increase. However, growers that elect PLC in 2019 are unlikely to see benefits this year – based on current supply, demand and price projections -- but could see program benefits if prices fall from their current levels next crop year. The phrase: “A bird in the hand is worth two in the bush,” comes to mind.

Today’s Market Intel has identified benefits of 2018 ARC-CO coverage and reviews the protection of ARC-CO for 2019. To assist farmers in making their decisions about ARC-CO and PLC, a future Market Intel, published closer to the enrollment deadline, will evaluate the probability of grain and oilseed prices falling below ARC-CO and PLC threshold levels. These price distributions will help agricultural producers make more informed risk management decisions for the 2019 and 2020 coverage years.

Top Issues

VIEW ALL