First Look at the 2022/23 Marketing Year Amid Global Turmoil

TOPICS

Wheat

photo credit: AFBF Photo, Morgan Walker

Roger Cryan

Former AFBF Chief Economist

A review of the May WASDE with updates to the 2021/22 marketing year and a first look at the 2022/23 marketing year for select crops

The May World Agricultural Supply and Demand Estimates gives the first look at USDA’s supply and demand expectations for the newest marketing year since the USDA Agricultural Outlook Forum in February. This is the highlight of spring USDA reports as it incorporates farmer planting decisions from the March Prospective Plantings report and adapts supply estimates to reflect weekly planting progress reports. The run-up to this report has been dominated by concerns about global grain and oilseed supplies for this year and next, prompted by both growing demand and disruptions of Black Sea supplies due to the Russian war on Ukraine. This Market Intel dives into the May WASDE for updated estimates of the current 2021/22 marketing year crop and looks at what may be in store for the 2022/23 marketing year, which starts in September.

Corn

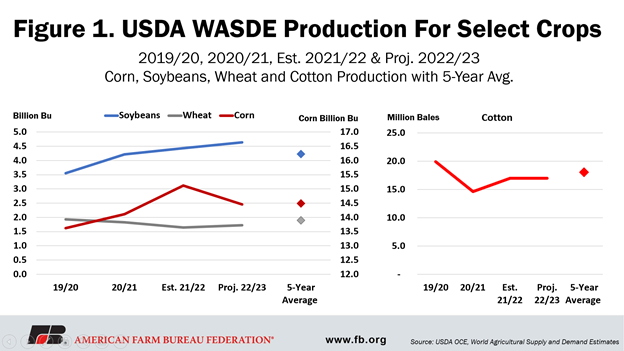

USDA estimates corn planted for the 2022/23 marketing year at 89.5 million acres, down 4.2% from 2021/22, when 93.4 million acres of corn were planted. USDA forecasts farmers will harvest 81.7 million acres of corn in 2022 at an unchanged yield rate of 177 bushels per acre. This projects to corn production in 2022 at 14.5 billion bushels, down from 2021’s near record 15.1 billion bushels. This would be 4% above the five-year average of 14.5 billion bushels.

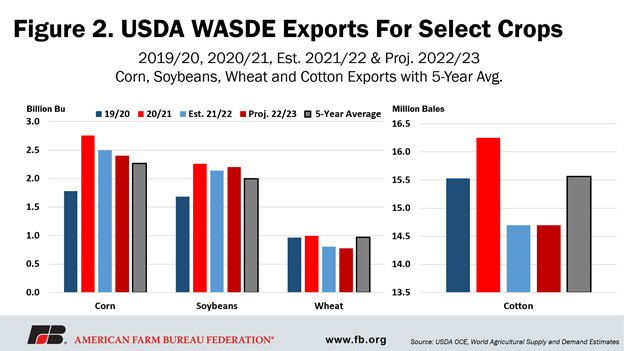

On the demand side, for the new 2022/23 marketing year, USDA estimates ethanol use will be unchanged from this year at 5.4 billion bushels. Corn export estimates for the newest marketing year are projected down 100 million bushels to 2.4 billion bushels, after an estimated 250-million-bushel decline this year from the highwater mark of 2.75 billion bushels in 2020/21.

Despite lower exports and steady ethanol use, next year’s projected production decline would lead to an 80-million-bushel reduction in ending stocks in September 2023, to 1.36 billion bushels. Of course, these early 2022/23 demand projections could change considerably over the next 15 months.

USDA estimates put the 2022/23 (ending) stocks-to-use ratio at 9.3%, down from the current year’s estimated 9.6%, and the second lowest since 2012. USDA projects the 2022/23 corn price at $6.75 per bushel, up 85 cents from this year’s estimated total; this would be the highest since $6.89 in 2012/13. USDA’s estimate for the corn price in 2021/22 is up a dime from last month, to $5.90.

Soybeans

Soybean farmers are expected to plant 91 million acres of soybeans in 2022/23, up 4.4% from 2021, when farmers planted 87.2 million acres. This was up nearly 19.6% from 2019. Soybean yields are projected at 51.5 bushels per acre for 2022/23 (up very slightly from the latest estimate for 2021/22) on 90.1 million acres harvested (also up 4.4%). As a result, U.S. soybean farmers are projected to produce 4.64 billion bushels in the new marketing year, 4.6% above the current year’s latest estimate of 4.44 billion bushels, and 5% above the five-year average.

The continuing increase in soybean production for 2022/23 follows rising crush demand to meet a rapidly increasing demand for soy-based diesel fuels. Though export demand dipped in 2021/22 to 2.14 billion bushels, it is projected to rise again in 2022/23 to 2.2 billion bushels, though both remain above the five-year average of 2.0 billion bushels. Demand for soybeans is expected to be up 108 million bushels for 2022/23.

The projected production increase in 2022/23 is expected to be offset by increased exports and increased crushings, but will still drive a projected 75-million-bushel increase in ending stocks to 310 million bushels. The stocks-to-use ratio for 2022/23 is projected to be 6.8%, above the estimated 5.3% ratio for 2021/22.

Rising demand and low stocks continue to push prices higher. For the 2021/22 marketing year, the average farm price for soybeans is still estimated at $13.25 per bushel (where it was for the last two months, but 60 cents lower than projected a year ago); and the price for 2022/23 is projected 9% higher, at $14.40.

Figure 1 displays U.S. crop production for corn, soybeans, wheat and cotton since the 2019/20 marketing year, including the new 2022/2023 projections and the five-year average.

Wheat

Wheat planted acres in 2022/2023 are estimated at 47.4 million acres, an increase of 1.5% from 2021/22’s 46.7 million acres. Yield is estimated to be 47 bushels per acre, which would generate wheat production of 1.729 billion bushels, a 5.0% increase from a poor 2021/2022 wheat crop, but would still be about 8.5% below the five-year average of 1.89 billion bushels.

Estimated wheat demand in 2021/22 is down 8.5% from 2020/21, and 2022/23 demand is expected to decline another 2.4%, to 1.885 billion bushels, largely as the result of reduced exports. Stocks at the end of 2022/23 are projected at 619 million bushels, down 5.5% from this year and down nearly 40% from the end of 2019/20. Feed use of wheat for 2021/22 is expected to decline by 20 million bushels in 2022/23 to 100 million bushels, while exports are anticipated to fall 30 million bushels to 775 bushels in 2022/23.

The resulting stocks-to-use ratio for wheat in 2022/23 is expected at 33%, its lowest level since 2014, while 2020/21 stocks-to-use sits at 34%.

USDA estimates the average farm price of wheat for the 2021/22 marketing year to be $7.70 per bushel, an 18% increase from USDA’s projection this time last year, when USDA expected the crop price to be $6.50 per bushel. Into the newest marketing year, USDA estimates the 2022/23 marketing year average price of wheat to be $10.75 per bushel, which would be the highest annual U.S. wheat price in history, $2.73 above the record of $8.02 in 2008.

Cotton

Cotton planting expectations for the 2022/23 marketing year are 12.23 million acres, 9% above this year’s estimate, but farmers are projected to harvest only 9.14 million acres, based on historical rates of abandonment and poor soil moisture in the Southwest. USDA anticipates a 6% yield bump to 867 pounds per acre for those acres, though, so the total harvest is expected to be 16.5 million 480-lb. bales, down 5.8% from the current year and about 13% below the five-year average.

Overall cotton use, which consists largely of exports, is projected at 17 million bales, down 300,000 bales from the estimated 2021/22 use. Exports are projected to be down 250,000 bales, to 14.5 million bales in 2022/23.

Cotton ending stocks for 2021/22 are estimated at 3.4 million bales and USDA projects that the lower production will be only partially offset by lower exports and domestic use, leaving ending stocks for 2022/23 at 2.9 million bales, down 15%. For 2021/22, USDA estimates have the cotton stocks-to-use ratio sitting at 19.7% and the 2022/23 stocks-to-use ratio at 17%, well below the five-year average.

Low stocks and a below-average crop are expected to support relatively high prices in 2022/23: USDA projects an average price of 90 cents per pound for upland cotton, just 2 cents below the estimated price for 2021/22 of 92 cents, which would be a record and would be 17 cents above the projection this time last year.

Figure 2 displays U.S. exports for corn, soybeans, wheat and cotton since the 2019/20 marketing year, including the new 2022/23 projections and the five-year average.

Conclusion

The May WASDE is the long-awaited first look at the upcoming marketing year for corn, soybeans, wheat and cotton. There is a lot of room for changes over the coming months. This May WASDE comes as the global grain and oilseed market faces tremendous demand growth for food, feed and fuel; great uncertainty about the impacts of the Russian invasion of Ukraine; and economic and political disruptions to critical farm inputs including fuel and fertilizer. Farmer planting decisions will not be updated by USDA until the June 30 acreage report, providing a better idea of supply expectations for the newest marketing year. High input costs could shift planted acreage and continued high prices could result in revised supply expectations throughout the 2022/23 marketing year. Stay tuned.

Top Issues

VIEW ALL