In Survey-Based USDA Report, Farmers Indicate Lower Yields

TOPICS

USDA

photo credit: Arkansas Farm Bureau, used with permission.

Shelby Myers

Former AFBF Economist

USDA’s Crop Production Report, released on August 12, indicates corn yields will reach 174.6 bushels per acre and soybean yields will be 50 bushels per acre, despite weather concerns throughout the summer. The report provides the most recent update on U.S. commodity supplies since the June 30 Planted Acreage report.

The corn estimate of 174.6 bushels per acre is up 2.6 bushels per acre compared to 2020 but is 4.9 bushels per acre lower than last month’s USDA World Agricultural Supply and Demand Estimates (WASDE) report, which put corn at 179.5 bushels per acre. For soybean yields, USDA’s estimate of 50 bushels per acre in 2021 is down 0.2 bushels per acre compared to 2020 and 0.8 bushels per acre lower than where USDA pegged soybean yields in the July WASDE. Prior to the release of the crop production report and the August WASDE, analysts expected corn yields to be between 175.7 bushels per acre and 180 bushels per acre. They had estimated soybean yields would be between 49.3 bushels per acre and 51.3 bushels per acre. Keep in mind, crop production data from this report is based primarily on farmer surveys and satellite imagery. Field samples from USDA’s objective yield survey plots will not be available until September.

2021 Corn Yield

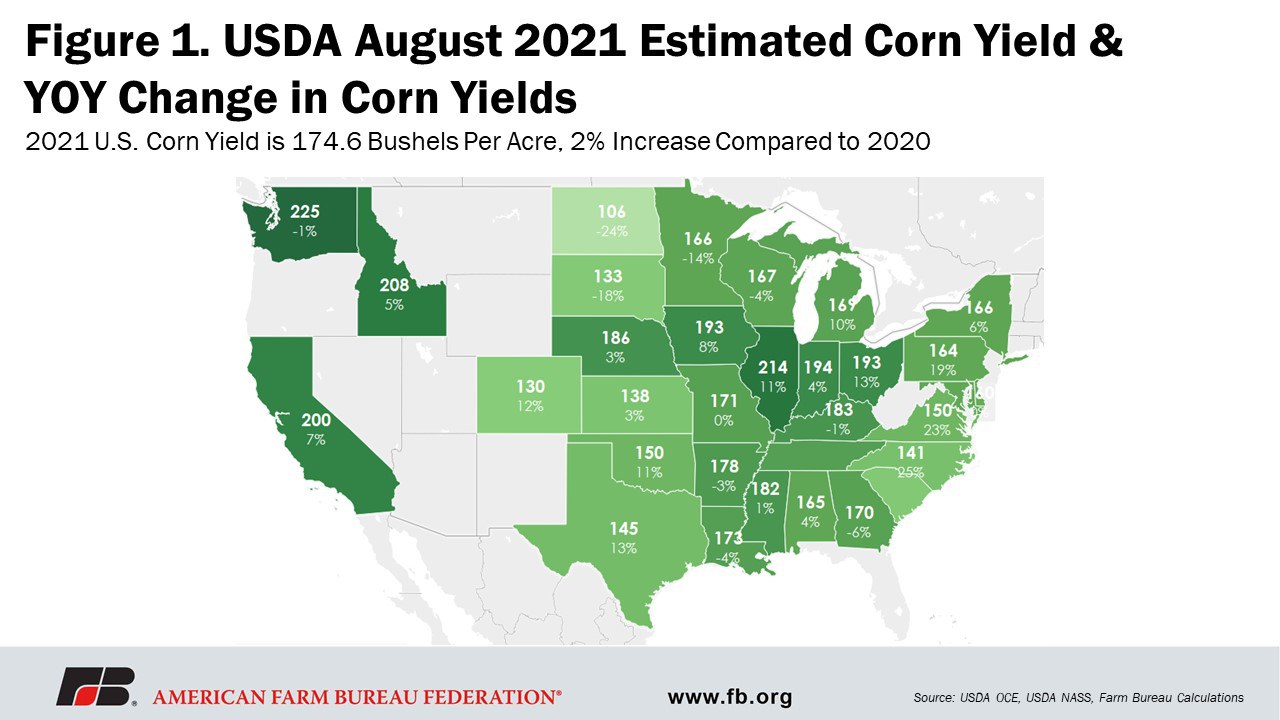

For non-irrigated corn, the highest yields start in Illinois where estimations put yields at 214 bushels per acre, an increase of 11% compared to 2020 when yields were 192 bushels per acre. Indiana follows with an estimated 194 bushels per acre, up 4% from 2020 when yields were 187 bushels per acre. Iowa is estimated to have the third-highest non-irrigated corn yield with 193 bushels per acre, up 8% from 2020. Washington leads irrigated corn yields with an estimated 225 bushels per acre, a decrease of 1% compared to 2020. Idaho is just behind with an estimated 208 bushels per acre of corn, up 5% from 2020. North Carolina is expected to have the largest year-over-year increase in corn yield, 25%, increasing from 113 bushels per acre to 141 bushels per acre.

An important note is the year-over-year decrease in expected corn yield for North Dakota, South Dakota and Minnesota, which have all been significantly impacted by drought. North Dakota is expected to have a decrease of 24% in corn yield, going from 139 bushels per acre in 2020 down to 106 bushels per acre in 2021. South Dakota is expecting an 18% decrease in corn yield, going from 162 bushels per acre in 2020 to 133 bushels per acre in 2021. Minnesota reports an expected decrease of 14% in corn yield, going from 192 bushels per acre to 166 bushels per acre.

{kind=link}

Figure 1 maps USDA’s August 2021 corn yield estimates and displays the year-over-year change from 2020.

Corn Supply and Demand Expectations

Given the 174.6 bushel per acre estimate for corn yield, USDA lowers production by 415 million bushels in the August WASDE, dropping from 15.16 billion bushels in July to 14.75 billion bushels, which would be a 4% increase compared to 2020. Supply for the 2021/22 corn marketing year will also be increased 35 million bushels due to adjustments made in the 2020/21 marketing year. Ethanol use for 2020/21 was increased by 25 million bushels to 5.075 billion bushels and another 15 million bushels were added in the food, seed and industrial use category to reach 6.5 billion bushels. Exports for the 2020/21 marketing year were reduced by 75 million bushels, going from 2.85 billion bushels to 2.77 billion bushels. The net result is an increase to ending stocks of 35 million bushels, moving from 1.08 billion bushels to 1.11 billion bushels of current marketing year corn that will be carried into the 2021/22 marketing year. The stocks-to-use ratio for the current marketing year moves up slightly to 7.4%, the lowest level since 2012, while the corn price for the current marketing year remains at $4.40 per bushel.

In addition to demand adjustments in 2020/21, USDA adjusted corn demand for the new marketing year (2021/22) by reducing feed and residual use by 100 million bushels to 5.6 billion bushels, but increased food, seed and industrial use by 10 million bushels for non-ethanol use, bumping it up to 6.6 billion bushels. Exports for 2021/22 corn were also reduced by 100 million bushels, going from 2.5 billion bushels to 2.4 billion bushels. The overall impact reduces expected corn ending stocks for the new marketing year from 1.4 billion bushels to 1.2 billion bushels. The stocks-to-use ratio decreased from 9.6% in July to 8.5% in August, while the corn price increased from $5.60 per bushel to $5.75 per bushel, the highest since 2013.

2021 Soybean Yield

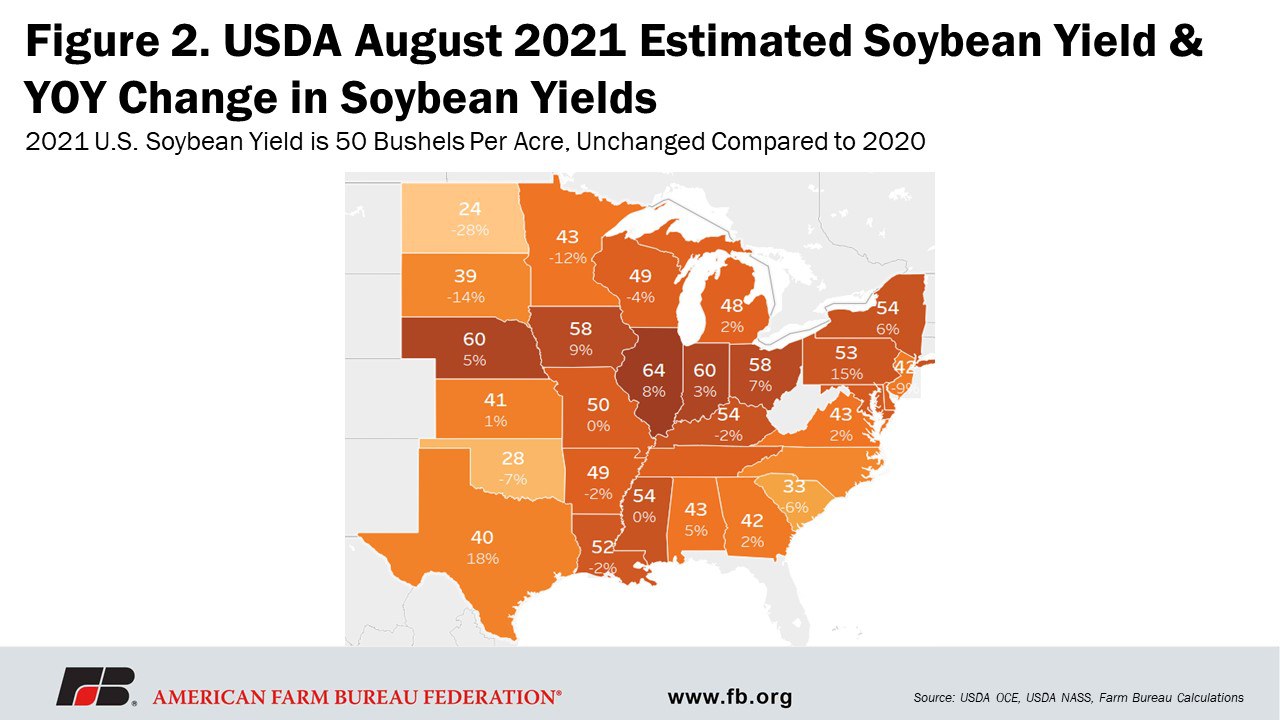

Illinois leads the country in estimated soybean yield with 64 bushels per acre, an increase of 8% compared to 2020 when soybean yield was 59 bushels per acre. Nebraska is just behind with an estimated soybean yield of 60 bushels per acre, up 5% from 2020 when soybean yield was 57 bushels per acre. Indiana is also expecting 60 bushels per acre of soybeans, which is up 3% from 2020 when soybean yield was 58 bushels per acre. Texas leads the way with the largest year-over-year increase in estimated soybean yield, 18%, with soybean yields estimated to be 40 bushels per acre, up from 34 bushels per acre in 2020.

Looking at a few of the drought-stricken states, North Dakota is expecting the largest year-over-year reduction in soybean yields across all soybean producing states, decreasing 28% from 33.5 bushels per acre in 2020 to, 24 bushels per acre in 2021. South Dakota is expecting the second-largest decrease, 14%, going from 45.5 bushels per acre in 2020 to 39 bushels per acre in 2021. Minnesota expects a 12% reduction in soybean yields, moving from 49 bushels per acre in 2020 to 43 bushels per acre in 2021.

Figure 2 maps USDA’s August 2021 soybean yield estimates and displays the year-over-year change from 2020.

Soybean Supply and Demand Expectations

USDA’s soybean yield estimate of 50 bushels per acre lowers the estimate for 2021/22 soybean production by 66 million bushels, declining from 4.4 billion bushels estimated in the July WASDE to 4.34 billion bushels; but it would be a 5% increase in production compared to 2020 when 4.13 billion bushels of soybeans were produced. Soybean supply in 2021/22 is increased by 25 million bushels of additional stocks carried over from the current marketing year. USDA estimates for 2020/21 that crushing will be reduced by 15 million bushels to 2.15 billion bushels compared to July estimates. Exports were also reduced by 10 million bushels to 2.26 billion bushels, resulting in a 25-million-bushel carry-over. The stocks-to-use ratio for the 2020/21 marketing year increases to 3.5% from 3% last month and the soybean price for the 2020/21 marketing year was reduced from $11.05 per bushel in July to $10.90 per bushel in August.

USDA made similar soybean demand adjustments in the 2021/22 marketing year, decreasing crushing estimates by 20 million bushels to 2.2 billion bushels and decreasing export estimates by 20 million bushels to 2.05 billion bushels, as well. The supply and demand adjustments made in this August WASDE report offset each other so that soybean ending stocks for the 2021/22 marketing year remain at the 155 million bushels with a stocks-to-use ratio of 3.5% and soybean price of $13.70 per bushel.

Summary

In the survey-based August Crop Production Report, USDA estimates corn yield to be 174.6 bushels per acre, up 2.6 bushels per acre compared to 2020, and soybean yield to be 50 bushels per acre, very close to 2020 yield results. Yield estimates will be updated in the September report, which will include the objective yield plots as part of the production estimates for the first time this year. These survey results are early evidence of drought impacts to crops in drought-stricken states, with more updates to supply likely to come in the September report. On the demand side, grain marketers will be monitoring U.S. corn exports increasing due to Brazil's decline in corn production, China’s imports of U.S. corn in anticipation of a potential repeat of 2020 and U.S. soybean export destinations, all with the potential to tighten crop supply margins further and increase commodity prices.

Top Issues

VIEW ALL