November WASDE Brings New Optimism for Corn and Soybean Markets

TOPICS

WASDE

photo credit: AFBF Photo, Right Eye Digital

Shelby Myers

Former AFBF Economist

USDA released its November World Agriculture Supply and Demand Estimates with amended supply and demand expectations for the 2020/21 marketing year. Largely in response to Chinese imports, U.S. corn exports increased this month compared to last. Corn and soybean supplies were lowered as expected yields were reduced for both crops. Anticipating higher export levels and lower yields, price expectations rose for the second month in a row. Today’s article reviews the November WASDE updates.

Some of the main highlights include big changes to U.S. corn export expectations, which grew by 325 million bushels, going from 2.3 billion bushels to 2.6 billion bushels. If these expectations are fulfilled, it would be the largest amount of corn the U.S. has exported on record. This bump in U.S. corn exports is largely driven by the increase of Chinese imports from 7 MMT to 13 MMT, some of which is expected to come from the U.S. If realized, it would be the largest amount of corn China has imported on record (i.e. China Could Be Looking to Import More Corn). USDA has stated that though there have not been any public statements regarding the Chinese corn import quota, shipment data for exporting countries through early November indicates China will exceed the current tariff-rate quota of 7.2 MMT. However, there are rumors China has increased the TRQ by 5 MMT through December. If the TRQ is not lifted, any additional corn China imports above the TRQ could be subject to a tariff of up to 65% of the purchase price.

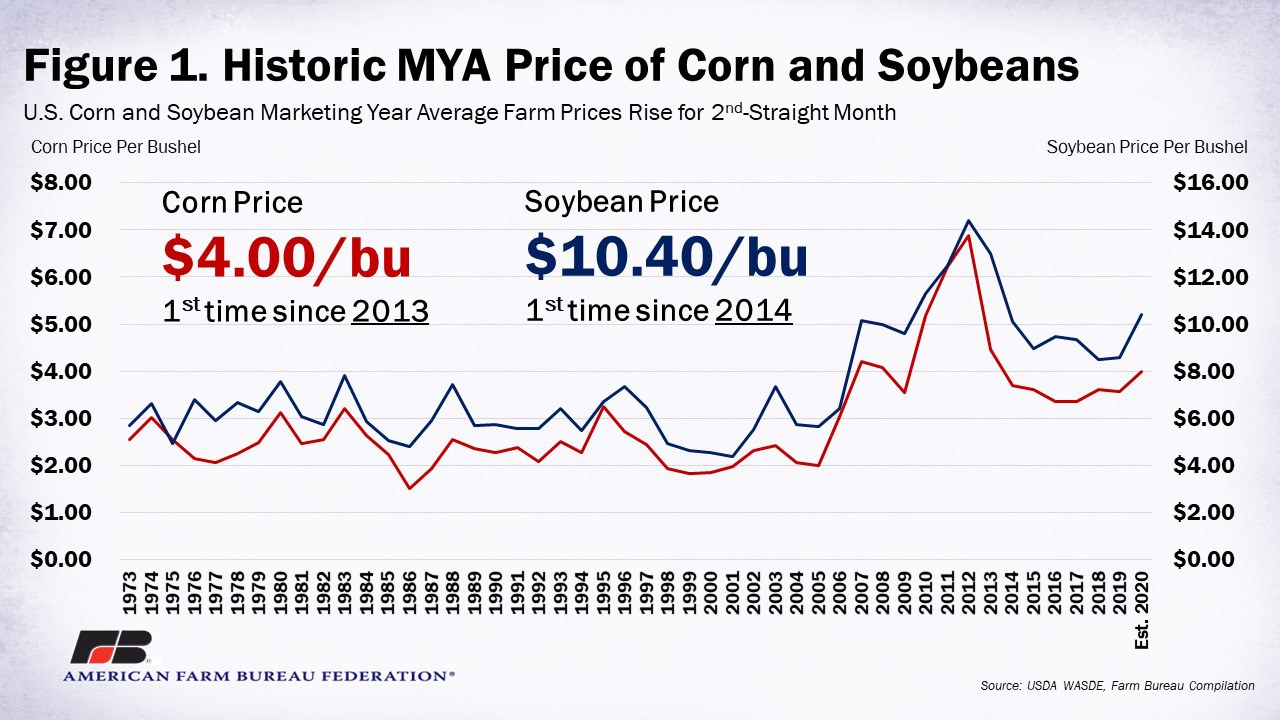

USDA put corn yield expectations lower, dropping from 178.4 bushels per acre to 175.8 bushels per acre. The two major changes to supply and demand for corn push ending stocks for the 2020/21 marketing year down to 1.7 billion bushels. Last month, the October WASDE had corn ending stocks above 2 billion bushels. With the adjustment, the average farm price rises from $3.60 per bushel to $4.00 per bushel, the highest price for corn since 2013, when the price was $4.46 per bushel.

Soybean highlights come from the changes USDA made in supply, reducing yield slightly from 51.9 bushels per acre to 50.7 bushels per acre and reducing overall 2020/21 soybean supply by 98 million bushels, going from 4.8 billion bushels to 4.7 billion bushels. The tightened supply decreases ending stocks from 290 million bushels to 190 million bushels, making it the lowest amount of soybean stocks on hand since 2013. With the tightening in supply and lower stocks, USDA raised the average farm price of soybeans from $9.80 per bushel to $10.40 per bushel, the highest price for soybeans since 2014, when the price was $10.10 per bushel.

Figure 1 displays the historic marketing year average farm prices for corn and soybeans.

Summary

Market analysts came into today’s WASDE release with expectations of increased demand and lower supplies in the current marketing year. The pre-report estimates leaned toward lowering corn yields by 0.7 bushels per acre to 177.7 bushels per acre and lowering soybean yields by 0.3 bushels per acre to 51.6 bushels per acre. Analysts’ yield estimates were higher than USDA’s for both crops. Additionally, analysts expected corn ending stocks would be lowered by only 135 million bushels to just above 2 billion bushels and soybean stocks would be lowered by only 55 million bushels to 235 million bushels. USDA cut corn and soybean stocks by nearly double those pre-report estimates.

USDA’s expectations for lower corn and soybean ending stocks for the 2020/21 marketing year improves the price outlook. All eyes will now turn to weekly consumption indicators from USDA’s Foreign Agricultural Service and the Energy Information Administration’s weekly ethanol production report to determine if the strong export commitments turn into actual export inspections and whether or not ethanol production will hold steady or improve given the rise of COVID-19 cases across the globe. Confirmation of demand strength at or above that needed for the WASDE to come to fruition will continue to support prices, while any slowdown in demand is likely to be accompanied by larger supplies and lower prices. Now is as good a time as any to review your marketing plans and put some risk management coverage in place…just in case.

Top Issues

VIEW ALL