China Could Be Looking to Import More Corn

TOPICS

Trade

photo credit: Arkansas Farm Bureau, used with permission.

Shelby Myers

Former AFBF Economist

As of October 22, U.S. accumulated and outstanding corn sales to China total approximately 10.6 MMT, well above USDA’s projection for Chinese corn imports of 7 MMT and above the calendar year 7.2 MMT low-tariff-rate quota. Given this information, the potential for China to increase its low-tariff-rate quota for corn has spurred speculation about the Chinese buying millions of tons of additional U.S. corn in the new marketing year. Increased demand for corn in animal feed combined with a lower-than-anticipated domestic supply has pushed China to book more global corn purchases. Some analysts ultimately expect China to import as much as 17 MMT of corn.

The challenge, however, to this expectation is that the October World Agricultural Supply and Demand Estimates pegged Chinese corn imports for the 2020-21 marketing year at 7 MMT, just under the 7.2 MMT, 264.5 million bushels, low-tariff-rate quota in place now. As a result, many expect China to increase the TRQ to facilitate additional corn imports, at which point USDA would likely acknowledge higher U.S. corn exports and higher Chinese corn imports. Without a higher TRQ, China can still import more corn but could have to pay tariffs of up to 65% of the purchase price. Today’s article explores China’s TRQ corn dilemma and its options for increasing the TRQ to import more corn.

China’s Domestic Corn Situation

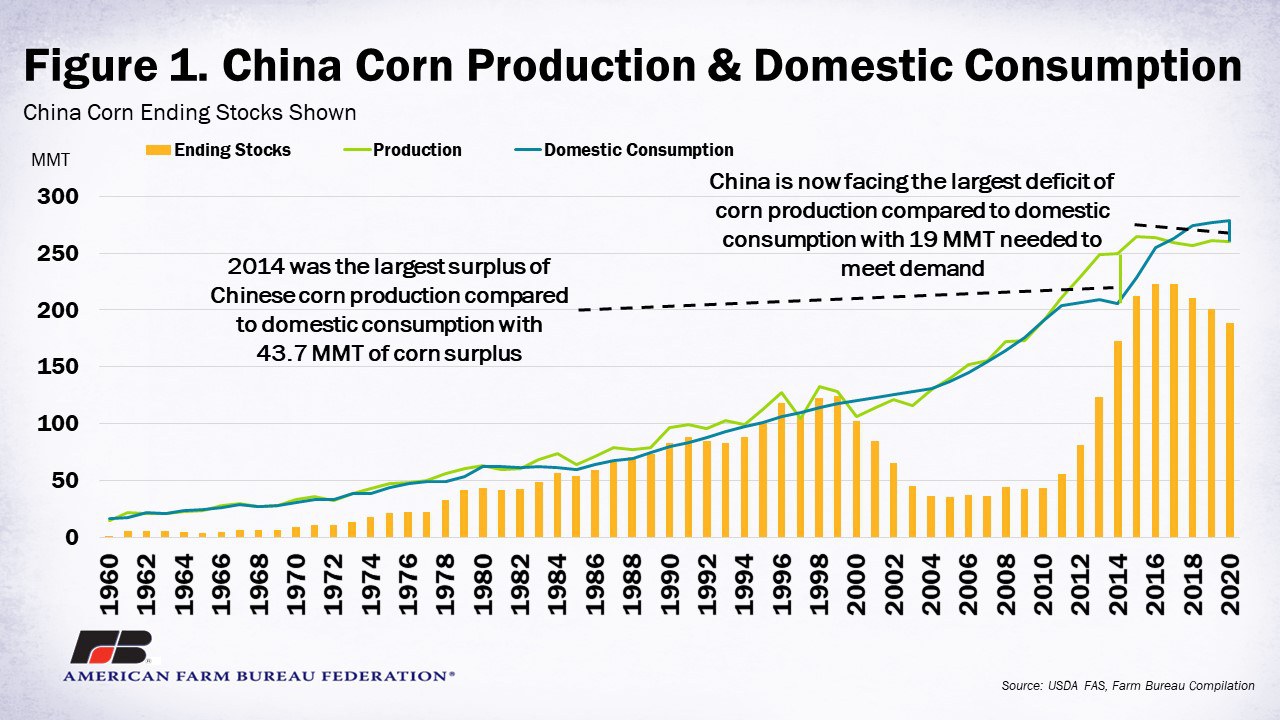

Due to the damage recently caused by typhoons and flooding, Chinese corn production is projected at 260 MMT, slightly above the five-year average of 259 MMT. However, there are also reports that their corn reserves are quickly dwindling with increased demand, particularly for livestock feed. USDA currently projects Chinese corn beginning supplies just under 201 MMT, about 7 MMT lower than projections first reported in May 2020. For years, China had been building reserves of corn in efforts to become more self-sufficient, as shown by a surplus of corn production compared to domestic corn consumption occurring between 2011 and 2017, when China held its largest surplus of corn production compared to domestic consumption of 43.7 MMT. While the Chinese stocks-to-use ratio rose to 93% in 2015, it was still less than the peak of 112% in 1996.

China's domestic corn consumption, as estimates stand now, is outpacing production by 19 MMT, which is the largest deficit on record for corn production compared to domestic consumption. Figure 1 displays Chinese domestic corn production and consumption since 1960, with corn ending stock reserves shown.

China needs a significant amount of corn to feed its hog, dairy and poultry industries. And with its battle with African Swine Fever, which arrived in August 2018, China is looking to repopulate the hog herds lost to the disease. Before ASF, given the size of China’s herd, hog feed dominated the feed consumption market. Though the herd population and hog production are recovering faster than most expected, China has a production loss of almost 33% to make up for. Structural changes to the industry, which could be a result of a shift away from “backyard”-style farms toward larger commercial operations, could also change feed consumption.

These circumstances are causing Chinese corn prices to climb to record levels as demand increases and supply tightens, making lower-priced imported corn more appealing. Figure 2 highlights the daily closing prices of Chinese corn. Another incentive to import U.S. corn is China’s commitments made in the Phase 1 trade deal and the mad dash to meet them before the end of the calendar year.

More U.S. Corn Could Be Headed for China

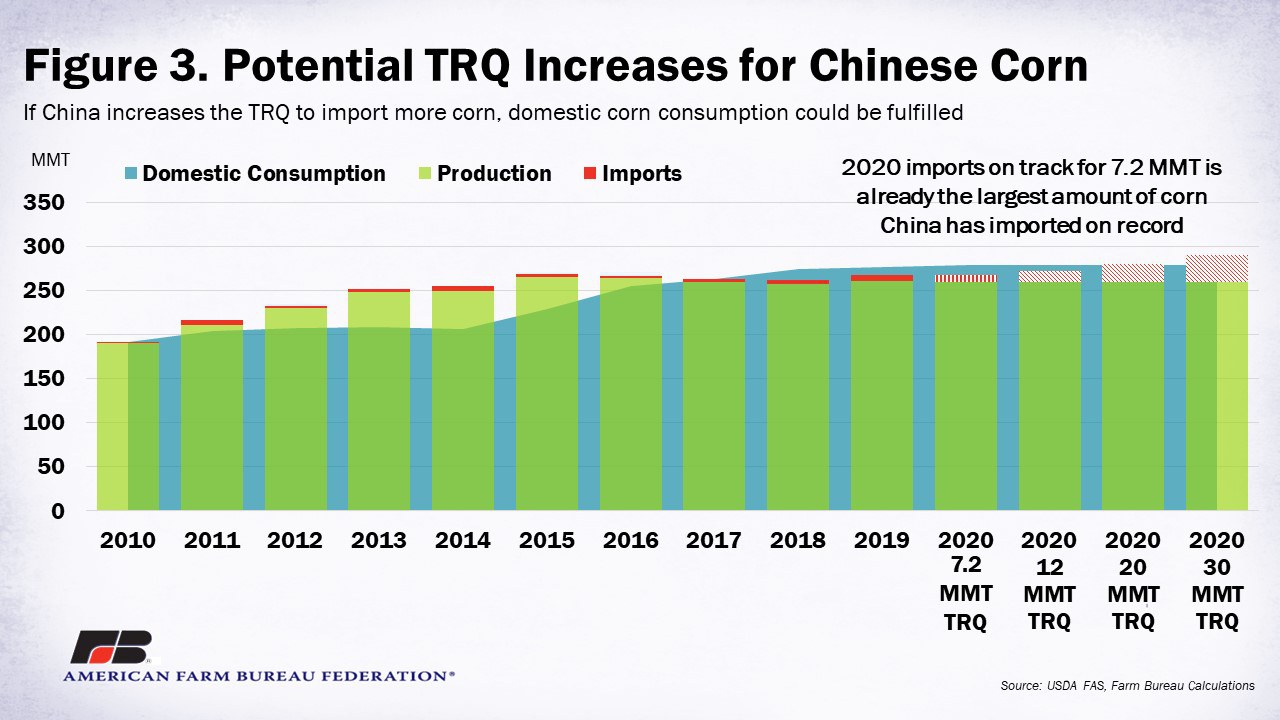

If rumors of China increasing the tariff-rate quota on corn come to fruition, it would expand the amount of imported corn China would allow for the new crop marketing year. Analysts estimate total Chinese corn imports from all trading partners between 12 MMT to 30 MMT. Chinese customs data shows 6.7 MMT of corn has already been imported for 2020, including September imports that reached just over 1 MMT. That leaves just above 500,000 MT, or just over 18 million bushels, left of the TRQ in the calendar year for China to import without making any adjustments. This would be the first time the country ever met the entirety of its import quota. To stay on track to meet domestic consumption without dipping too far into corn reserves or paying high domestic prices, China likely needs to find a way to import additional less expensive corn. China could potentially increase the low-tariff-rate quota from 7.2 MMT to 12 MMT, 20 MMT or even 30 MMT, which is the largest estimate circulating among market observers.

Figure 3 displays the three potential TRQ increases combined with current production estimates in order to meet domestic consumption.

Summary

China is on pace to import its largest amount of corn on record. With tightening supplies from weather impacts on production and rising demand as the country recovers from African Swine Fever, the pace at which China still needs corn is rising. Domestic corn prices are climbing to new highs, making global producers like the U.S. attractive alternatives for less expensive corn. There is an additional incentive to purchase U.S. corn to help meet commitments established in the Phase 1 agreements. As of October 22, accumulated exports of corn totaled 1.9 MMT, outstanding sales totaled 8.7 MMT, and total commitments stand at 10.6 MMT.

If China decides to raise its low-tariff-rate quota on corn imports, it will import its largest amount on record. China could still import more corn above the TRQ but will be required to pay tariffs of up to 65% of the purchase price. As more purchases are fulfilled, USDA will also need to increase its estimate of Chinese imports for the World Agricultural Supply and Demand Estimates, changing the U.S. and global landscape of new crop year corn supply, demand and prices.

Top Issues

VIEW ALL