Pork Market Insights for the Second Half of 2022

TOPICS

Pork

Bernt Nelson

Economist

Introduction

The first half of the year in pork markets has been a roller coaster filled with ups, downs, twists and turns. The year started out with futures approaching record levels and cash offerings doing the same. Futures prices are still well above forecasted break-even levels for 2022 but there are some indicators that a traditional high has occurred for the year. This Market Intel addresses the supply and demand factors, current world events and other issues influencing the wild ride that is the 2022 pork market outlook.

Prices

Lean hog futures have been volatile in the second quarter of 2022. The August lean hog contract showed an increase from $95.95/cwt in February to a high of $123.44/cwt on March 31. Since the highs in March, futures have been variable but have been moving upward in July, with the August contract settling at $109.30/cwt on July 11.

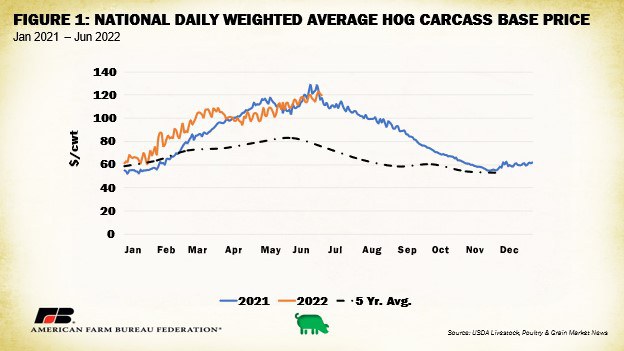

Cash prices have been strong in 2022 with the average carcass base prices well above the five-year average. Figure 1 illustrates the national weighted average hog carcass base price paid by processors between January 2021 and June 2022. Prices paid for carcasses in January were near the five-year average and have increased through the first half of 2022.

Supply - Quarterly Hogs & Pigs Report

USDA publishes a quarterly report called the Quarterly Hogs and Pigs report. This report provides a detailed inventory of breeding and market hogs for each of the 16 largest hog producing states, accounting for nearly 95% of the total U.S. inventory. In addition to these 16 states, the report also estimates the combined total for all other states.

The June 29th report fell in line with analyst polls and confirms that contraction is happening in the hog industry. The report estimated all U.S. hogs and pigs on June 1 at 72.5 million, down 1% from June 1, 2021, and down only slightly from March 30, 2022. Market hog inventory came in at 66.4 million head, down 1% since last year, and down only slightly from last quarter. The number of hogs retained for breeding was 6.17 million head, down 1% from last year but up 1% from the previous quarter. Breeding hog inventory increased in four states: Iowa, Missouri, South Dakota and Texas. Nine states had losses.

The March-May 2022 pig crop came in at 32.9 million, down 1% from 2021. Sows farrowing during this quarter were down 1% from 2021 at 2.99 million head. These sows represent 49% of the U.S. breeding herd. Average pigs per litter was 11 for the March-May period. This is up slightly compared to 10.95 last year.

Figure 2 illustrates the U.S. inventory of all hogs and pigs (million head) on June 1 between 2013 and 2022. The inventory of all hogs and pigs on June 1, 2022, has dropped nearly 7% since the record 77.6 million head in 2020. The decline in the breeding herd is especially important because it is responsible for hog supplies in the future.

The Pig Cycle

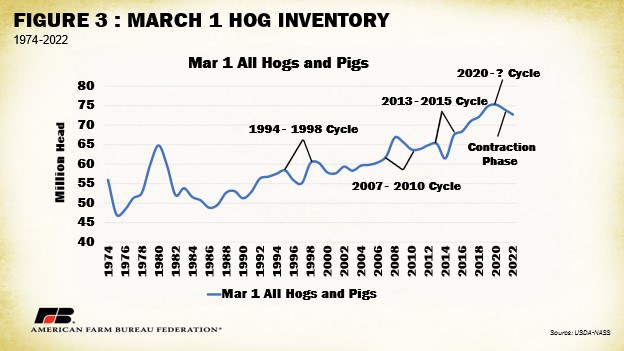

Much like the cattle cycle, production cycles also exist in the hog business. The pig cycle is the expansion and contraction of hog inventory in response to economic changes in the business. When pigs have been profitable for a while, farmers increase production and take advantage of better profitability. During expansion, farmers hold back young female hogs (gilts), which leads to an increase in the pig crop after farrowing. Eventually the supply from expansion causes prices to drop. When prices drop, farmers respond by either producing less or exiting the hog business. More female hogs go to slaughter, and the expansion phase of the pig cycle comes to an end. The shape of the inventory can help farmers see where we are in that cycle.

Figure 3 illustrates the U.S. inventory of all hogs and pigs on March 1 from 1974 to 2022, including some examples of the pig cycle. The length of a cycle varies but typically takes three to five years. This is due to a couple of factors. First, the farmer needs a reason to change production. Usually this comes from a change in profitability. Second, the life cycle of a market pig is nine to 10 months. This is the amount of time it takes from conception to when new pigs reach market weight (280 lbs.). When profitability was low in 2019, farmers made the decision to cut back on production. This decision increased sow slaughter by 10.2% in 2020. Piglets from the reduced breeding herd reached market weight nine to 10 months later, resulting in a smaller hog inventory. This contraction phase of the cycle has been in place since the record 77.6 million head inventory in 2020.

Slaughter

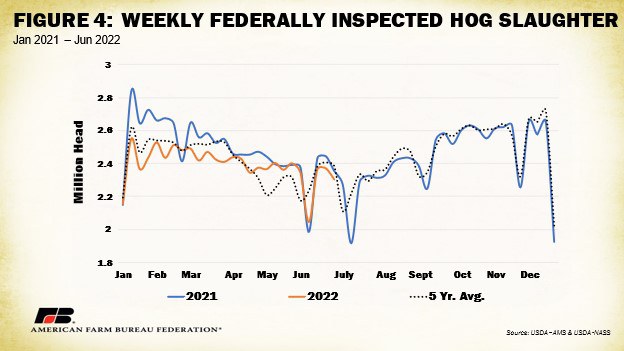

Hog slaughter has been below 2021 levels for most of 2022. Figure 4 illustrates weekly slaughter of federally inspected hogs for 2021, 2022 and the five-year average. Slaughter has also been below the five-year average for much of the year. Slaughter for the week ending July 8 came in at 1.98 million hogs. This is 67,000 more than this time last year.

Demand

Demand for pork on both the global and domestic fronts is facing obstacles but continues to show strength. The cost of food is increasing for U.S. consumers and USDA forecasts U.S. per capita meat consumption will decrease modestly for 2022.

The USDA Cold Storage survey is a measure of reserve food supplies held in commercial and public warehouse buildings. The report estimated that total red meat in cold storage on May 31 was 1.087 billion pounds, down slightly from April, but 20% greater than last year. Pork accounted for 543.07 million pounds, down only 2% from last month but up 17% from last year. The change from month to month is only slight and reflects a seasonal decline from the peak grilling season demand. For more information, see the latest Market Intel on cold storage.

Global Events -- ASF

The first case of African Swine Fever (ASF) in China was documented on August 3, 2018. ASF has now been detected in commercial hog herds in Germany and Northern Italy and is getting closer to France and Netherlands. Since 2014, the disease has been detected in 16 European countries and has crippled exports coming out of Europe. Prices of pork have increased alongside costs of production, which have been exacerbated by the Russian invasion of Ukraine. This creates incentive for many countries, especially in Europe, to look for alternative pork supplies.

ASF has also been detected in the Dominican Republic and Haiti, just 85 miles from the Commonwealth of Puerto Rico. The USDA Animal and Plant Health Inspection Service, is committed to keeping this disease out of the U.S. Recently, USDA’s Agricultural Research Service announced that a vaccine is one step closer to approval for commercial distribution.

The discovery of ASF on U.S. soil would be devastating. The arrival of the virus would initially shut down pork trade between the U.S. and other countries. History suggests that regionalization, evaluating animal disease status in a specified zone and controlling the products that enter or exit the zone, would not allow the U.S. to export until after USDA had been able to prove its measures effective in controlling the spread of the virus. Two of the most likely sources to bring this disease to the Unites States are animal feed and human food grown or produced in areas where ASF is present. ASF is a very resilient virus and can survive in feed or food products for up to 30 days. The U.S. is home to over 6 million feral hogs, an unfortunately convenient way for the virus to spread.

Exports

Global pork prices have been a spotlight item, adding questions to the pork market. Higher domestic prices have made it appealing for countries to look elsewhere for pork. All major exporters of pork other than Brazil are forecast to reduce hog inventory by the end of 2022.

USDA forecasts U.S. pork exports to decrease by 4.3% to 6,750 billion pounds in 2022, still 6.7% higher than 2019 levels. A July 8 export sales report from USDA’s Foreign Agricultural Service put total weekly U.S. exports of pork muscle cuts at 192,400 metric tons, 7% lower than this time last year. Mexico was the leading importer at 486,000 metric tons, followed by Canada at 403,000 metric tons and Japan at 253,000 metric tons. Exports will have to improve to meet USDA’s estimate. China has largely stopped buying U.S. pork so far in 2022.

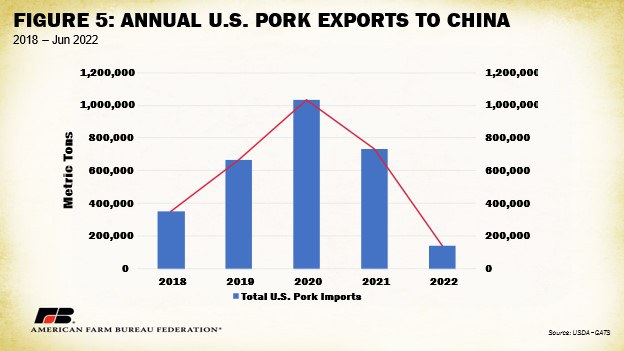

When China’s herd was devastated by ASF in 2018, they imported more U.S. pork. When China’s hog herd began recovering, imports kept flowing into the country. Figure 5 illustrates total Chinese imports of U.S. pork between 2018 and 2022. Figure 5 illustrates the astounding 193% increase in imports of U.S. pork between 2018 and 2020, causing an apparent oversupply of pork in China. As a result, hog prices dropped in late 2021 and China slowed imports to help raise their domestic hog prices. China further addressed this issue by increasing tariffs on U.S. pork from 8% to 12% in January 2022. China does not provide detailed data, but sources indicate that hog prices have come back up, suggesting increased demand. If this rise in prices continues, China may become a player in the export market in the fall of 2022.

Input Costs & The Bottom Line

Cash hog prices are up and so are production costs. Inflation is playing a big role in the current pork outlook, especially to the producer’s break-even prices and the consumer’s grocery bill. Bellies and hams are currently seeing the greatest increases in value.

Break-even price is the price a farmer or rancher must receive for his or her product that covers their cost of production. Input costs, feed- and non-feed-related, are driving up breakeven. Feed costs include corn, soybeans, dried distillers grains, and other feed and feed ingredients used to feed commercial hogs. Non-feed costs include items like operating interest and overhead. The result is that the hog farmer’s bottom line has not risen with the current prices.

Summary

The first half of the year for pork has come with higher prices and record-high cash offerings. Futures have been volatile, falling after mid-June, but showing some recovery in July. Strong cash and declining futures prices indicate that a traditional seasonal high has been established.

Domestically, higher food prices have consumers eating less meat. On the global front, U.S. pork exports to Mexico and Canada are booming. At the same time, China has re-built its hog numbers and is not importing as much pork in 2022. The combination of these factors has resulted in more meat in cold storage.

The USDA Quarterly Hogs and Pigs report confirmed further contraction in the pork industry. This means that farmers have increased the number of sows being slaughtered and the pig crop is likely to decline in days ahead.

ASF has begun popping up in Germany and continues to be a threat to hog herds worldwide, including in the Dominican Republic and Haiti, which are too close for comfort to the Commonwealth of Puerto Rico. Various USDA agencies are working to keep ASF from entering the United States.

Exports overall have been below 2021 levels but as pork prices rise globally, countries such as Mexico have been looking to other sources. Mexico and Canada have taken the lead in U.S. pork exports over China, the leading importer of U.S. pork in 2021. China faced problems with industry contraction and low hog prices due to an oversupply of pork, prompting them to elevate tariffs on U.S. pork to 12% in January 2022. Sources indicate that hog prices have begun to climb but the question of whether China will become a buyer of U.S. pork later in the year remains. China entering the market would mean increased demand for U.S. pork.

Conclusions

The 2022 pork market is a wild ride. The good news is the market started off the year strong and has maintained profitability through the first half of the year, even with increased feed costs. USDA’s Quarterly Hogs and Pigs report estimates the June 1 inventory of all hogs and pigs down 1%. Inventory has been declining since its peak in 2020. This is an indicator that the U.S. is in the contraction phase of the pig cycle. The spread of ASF in Europe is crippling their exports, and there is potential for China to become a buyer of U.S. pork again later in the fall. These two events happening at the same time as contraction in the U.S. hog industry could both help drive hog prices higher in the fall.

Top Issues

VIEW ALL