What A Difference a Month Makes: April Jobs Report

TOPICS

MacroeconomyBob Young

President

photo credit: Getty Images

Bob Young

President

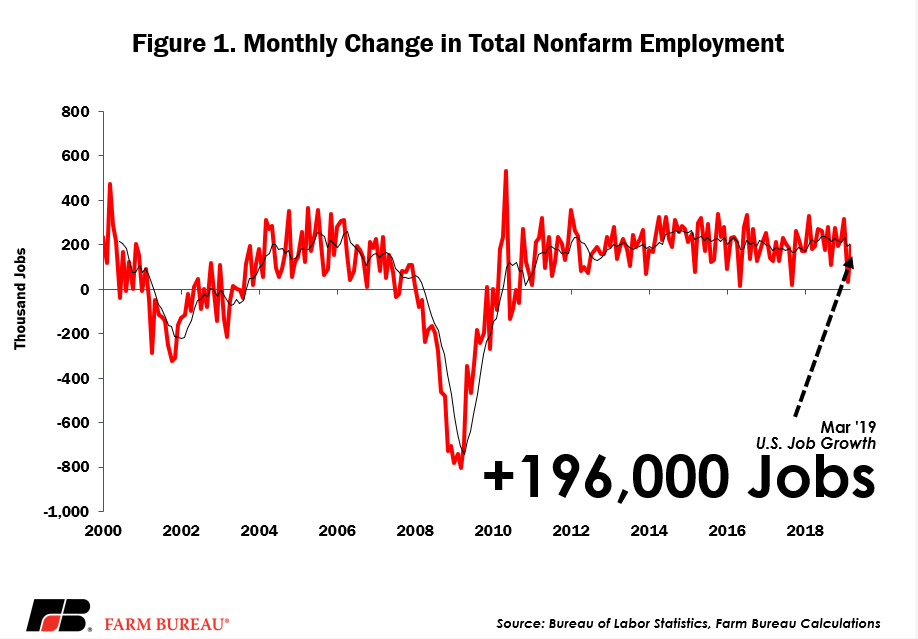

Taking a little poetic license to change Dinah Washington’s “What a Difference a Day Makes” to ‘”what a difference a month makes” and we have a spot-on theme for the April jobs report. Recall that the March report indicated the economy added a scant 20,000 jobs in February. This month, the report showed a 196,000-job gain, which is much more in line with the previous several months in which new jobs averaged over 250,000 per month. Even the 20,000 number for February increases was boosted in the first revision to 33,000. Still an outlier, but movement in the right direction.

While the headline number looks good, a dive inside raises an eyebrow or two. The overall goods-producing sectors – mining, construction and manufacturing – turned in a total of only 12,000 new jobs. Mining and logging jobs ticked up 2,000. Construction added 16,000, while manufacturing dipped by 6,000. All subsectors in manufacturing were changed by less than 5,000 slots, so in essence, the sector was static for March.

If overall numbers are up by nearly 200,000 and the goods sector added only 12,000, the arithmetic demands that the service sector stepped up in March. Walking down through the table the initial story was depressing. The trade, transport and utility mega-sector lost 5,000 jobs. Wholesale and retail trade combined dropped 14,000 slots. Department and general merchandise stores continue to slide, dropping 2,100 and 5,100 positions, respectively.

IT and financial sectors both added around 10,000 positions, with insurance carriers growing by 7,400 jobs. Professional and business services picked up 37,000 jobs. Computer systems design contributed 11,500 to that total.

Health care continues to add new jobs, particularly in ambulatory health care. Of 49,000 new health care-related jobs, 27,000 were in ambulatory care. These are doctor’s offices, dentists, outpatient care centers, testing laboratories and home health care. Hospitals and nursing care facilities combined picked up 22,100 new jobs.

One of the biggest changes between last month’s report and this report was in leisure and hospitality. While last month saw the sector lose 1,000 slots, it picked up 33,000 this month. As a reminder, January saw over 90,000 new jobs in this sector, suggesting at least some of that hiring was pulled forward. Food services and drinking establishments accounted for 27,300 of the sector’s additions.

While the federal government sloughed off 2,000 positions, state and local government increased hirings by 4,000 and 12,000, respectively.

Average weekly earnings were up by more than 3 percent, which is certainly better than the 2 percent level we ran from 2012 through much of 2017 but is well short of the 4 percent-plus we have historically seen when a growth period has grown this long in the tooth. And recognize that weekly earnings can increase due simply to adding a few more hours to the work week. It is not the same as wage growth. Average hourly earnings – which do reflect wage increases – were up by 3.3 percent, but that level is down from the 3.4- to 3.5-percent increases seen over the previous three months.

Data from the household survey, which is collected from individual employees, does not paint as bright a picture as the establishment data, which is collected from companies. While the household survey data showed essentially no change in the unemployment rate, it got to that bottom line by dropping 224,000 people out of the workforce and dropping 201,000 jobs. This was quite a change from the last quarter of 2018 when the household survey suggested we were adding 292,000 jobs a month. For the first three months of 2019, that same survey suggests we have been losing 68,000 jobs a month. There was also an – admittedly small – uptick in the number of people employed part-time who did not want to be part-time employees, i.e., these are employees who are not part-time employees by choice.

Many of these employment numbers suggest this growth period may be nearing a tipping point. Taken together with kinked yield curves, a downturn may not be imminent, but one of these days…

Top Issues

VIEW ALL