Dairy Risk Management Tools Remain Vital Heading into 2022- Supplemental Dairy Margin Coverage Applications Open

TOPICS

USDA

photo credit: Mark Stebnicki, North Carolina Farm Bureau

Daniel Munch

Economist

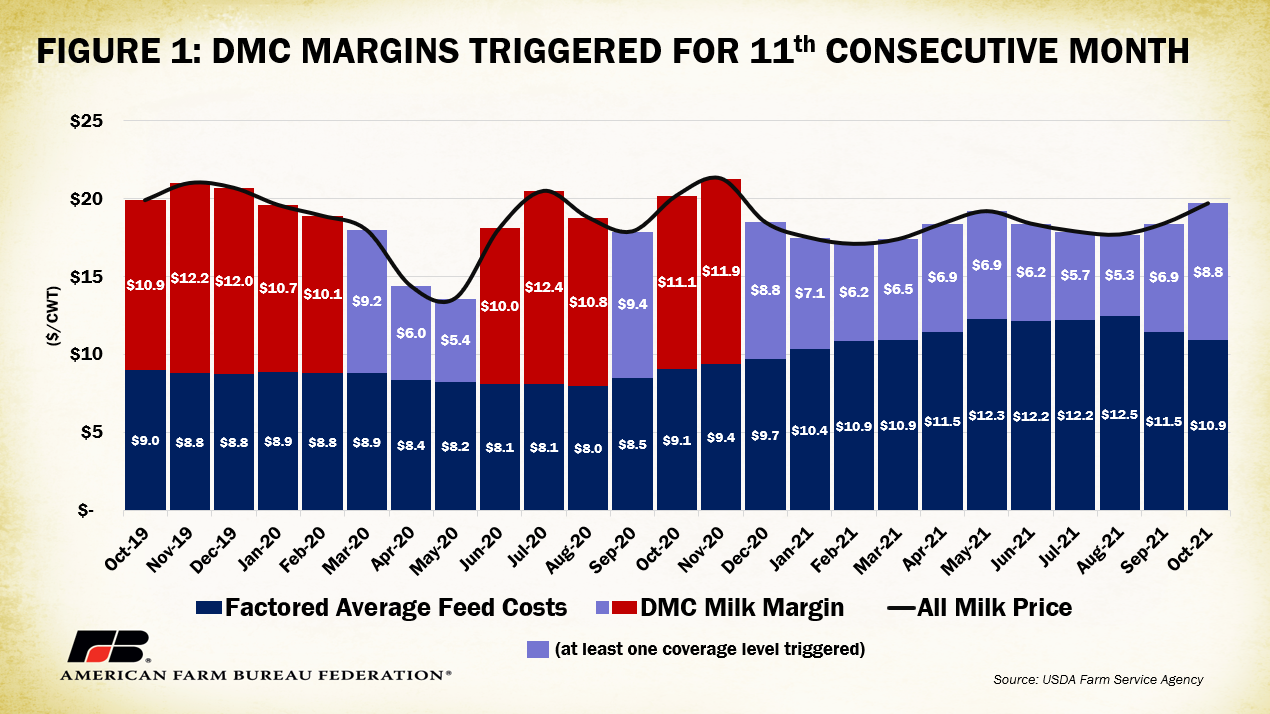

Ripple effects of the COVID-19 pandemic continue to impact dairy farmers. In a previous dairy article, we touched upon the network of pandemic-related market conditions that triggered Dairy Margin Coverage (DMC) payments for the seventh consecutive month. Unsurprisingly, shrunken margins primarily linked to high feed costs persist and have, yet again, triggered DMC payments for the eighth, ninth, 10th and 11th consecutive months, through this past October.

The Dairy Margin Coverage program provides a level of risk protection to dairy producers when milk prices are low and or feed costs, on average, are high. This voluntary program provides payments when the calculated national margin falls below a producer’s selected coverage trigger. The margin is the difference between the average price of feedstuffs (the price of hay, corn, and soybean meal) and the national all milk price.

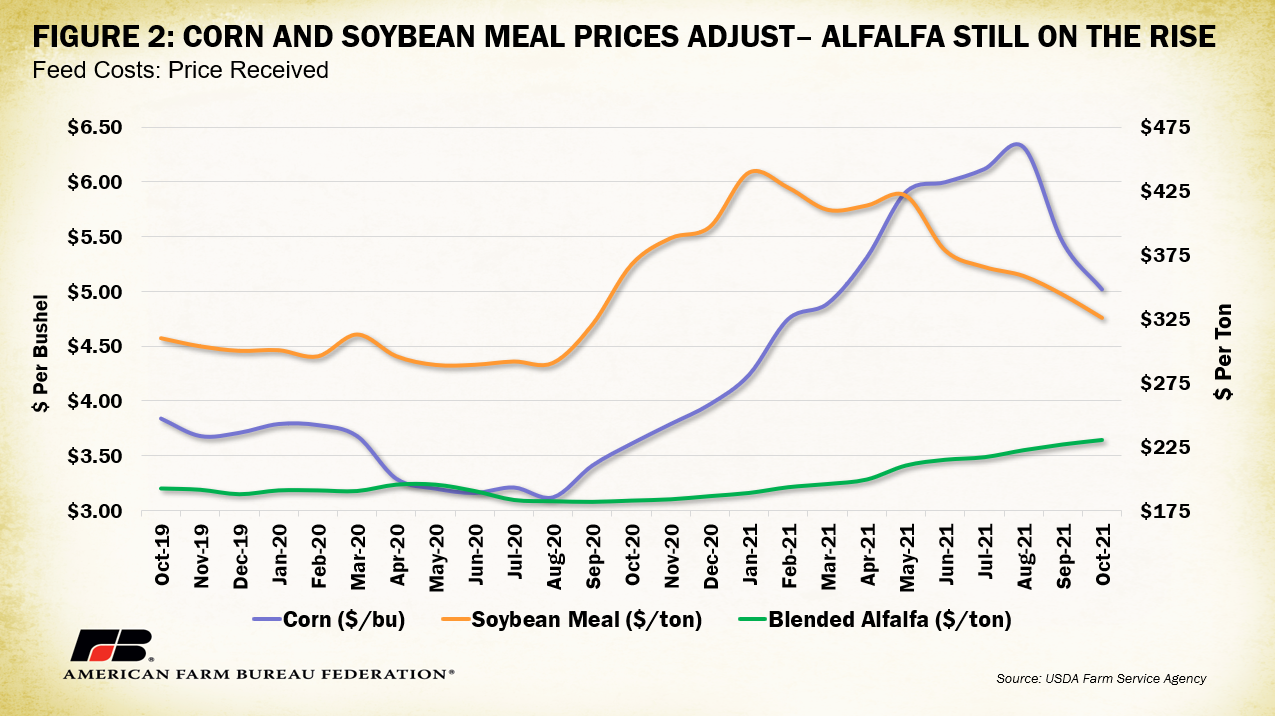

October’s DMC margin was $8.77 per hundredweight, $3.52 above August’s record-low of $5.25 and the largest margin since Nov 2020. A modest decline in corn and soybean meal prices over the past few months contributed to the lowest factored average feed cost ($10.93) since February. That said, corn and soybean meal costs remain above the previous five year average, partially linked to the widespread supply chain shortfalls ranging from labor shortages and increased input costs to delayed and costly transportation hurdles. Alfalfa prices have continued on an upward trend. Eight of the top 10 hay-producing states remain affected by widespread severe drought, with farmers reporting reduced crop yields ranging from 26% (New Mexico) to 64% (Montana) lower than last year.

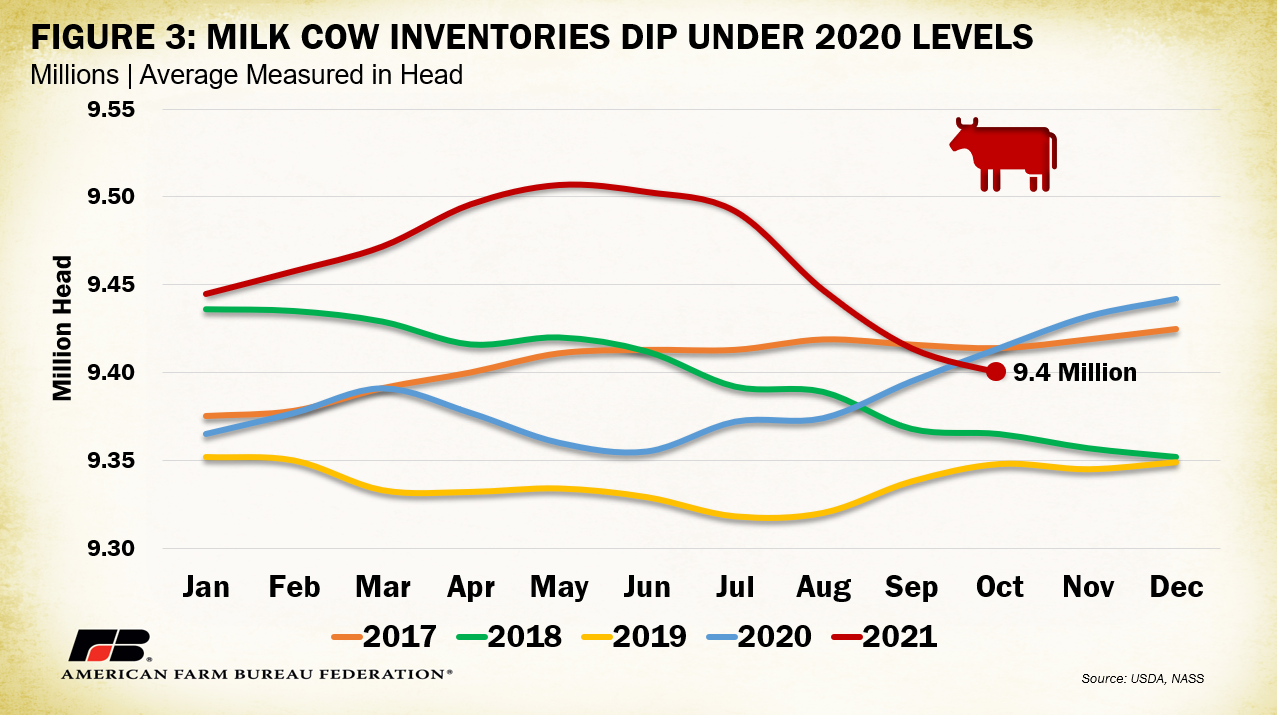

2021 milk cow inventories dropped below 2020 levels for the first time in October (Figure 3). The 14,000-head reduction from October 2020 resulted in an 88,000-pound (0.5%) drop in milk production during the same timeframe. This 14,000-head year-over-year decrease is equivalent to the decrease from last month and combines into a total 107,000-head decline since the May 2021 peak - the largest recorded national herd size in over 20 years. Notably, the latest milk production report put milk production per cow at 1,970 pounds in October 2021, a 6-pound decrease from October 2021. Even with a slight tightening of supply, DMC milk margins triggered payments for producers with the highest coverage level elections. A continued decline in milk supply could push prices upward in 2022, though producer-level expenses remain inflated, constraining expectations for better margins. The recent World Agricultural Supply and Demand Estimates increased forecasted 2021 average Class III milk prices by 10 cents to $17.05 per hundredweight (cwt), the average 2021 Class IV price by 5 cents to $16.05 per cwt and the 2021 all milk price 10 cents to $18.60 per cwt. 2022 forecasted Class III and IV prices were also raised 30-40 cents to $18.15 and $19.00/cwt, respectively. DMC remains a widely used safety net by over 75% of dairy farmers across the nation given its protection from price uncertainty.

A recent USDA news release announced that applications for the Supplemental Dairy Margin Coverage (SDMC) Program would be accepted Dec. 13 through Feb. 18. Last December, under the Consolidated Appropriations Act of 2020, SDMC based on 75% of the difference between 2019 marketings and the old base calculation (2011-2013 milk marketings) number was passed into law. The new policy allows operations to option for higher milk production coverage if changes to herd size were made since the 2011-2013 basis years (within the 5-million-pound limitation). For this expansion of coverage, $580 million has been set aside. It will apply to the 2021 (retroactively), 2022 and 2023 calendar years. After making any revisions to production history under SDMC, producers can apply for 2022 traditional DMC coverage. This means future DMC contracts will include the updated production history figures that account for 2019 marketings.

Additionally, the Farm Service Agency (FSA) has adjusted the calculation of alfalfa within the factored average feed costs figure using 100% premium alfalfa hay rather than 50% in hopes of making future DMC payments more reflective of dairy expenses. This change reduced DMC milk margins by an average of $0.22/cwt a month linked to an average $15.95/ton increase in alfalfa prices under the updated formula for 2021. For example, in October, the DMC margin dropped from $8.77/cwt to $8.54/cwt under the adjustment. This will allow enrolled producers to retroactively recoup payments they would have qualified for under the feed cost formula change – if the difference was large enough to trigger a higher payment level covered under their plan. FSA estimates that the formula change will result in additional payouts of $108.47 million for the January 2020 through September 2020 payment period. A three-fiscal year (2021 through 2023) payment estimate is $335.43 million and the 10-fiscal year (2021 through 2030) payment estimate is $705.32 million. FSA will use the adjusted alfalfa prices when calculating future SDMC and DMC payments and will reimburse producers retroactively through January 2020.

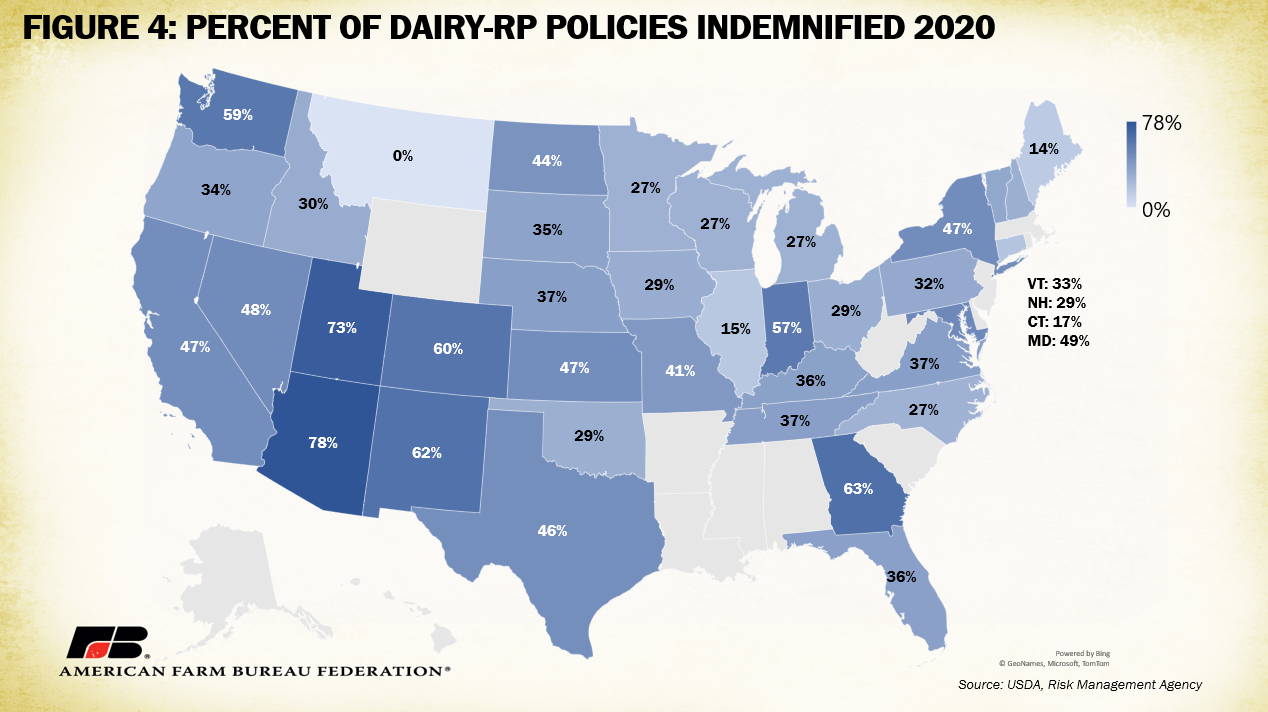

On the Dairy Revenue Protection (DRP) side, indemnity payments are down from 2020 while program participation is up. DRP is an area-based federal crop insurance product that provides quarterly revenue coverage for dairy farmers. The quarters available for coverage correspond to the quarters of the calendar year, i.e., January to March, October to December. Under DRP, an indemnity is paid to a dairy farmer if actual milk revenue falls below a previously established final revenue guarantee.

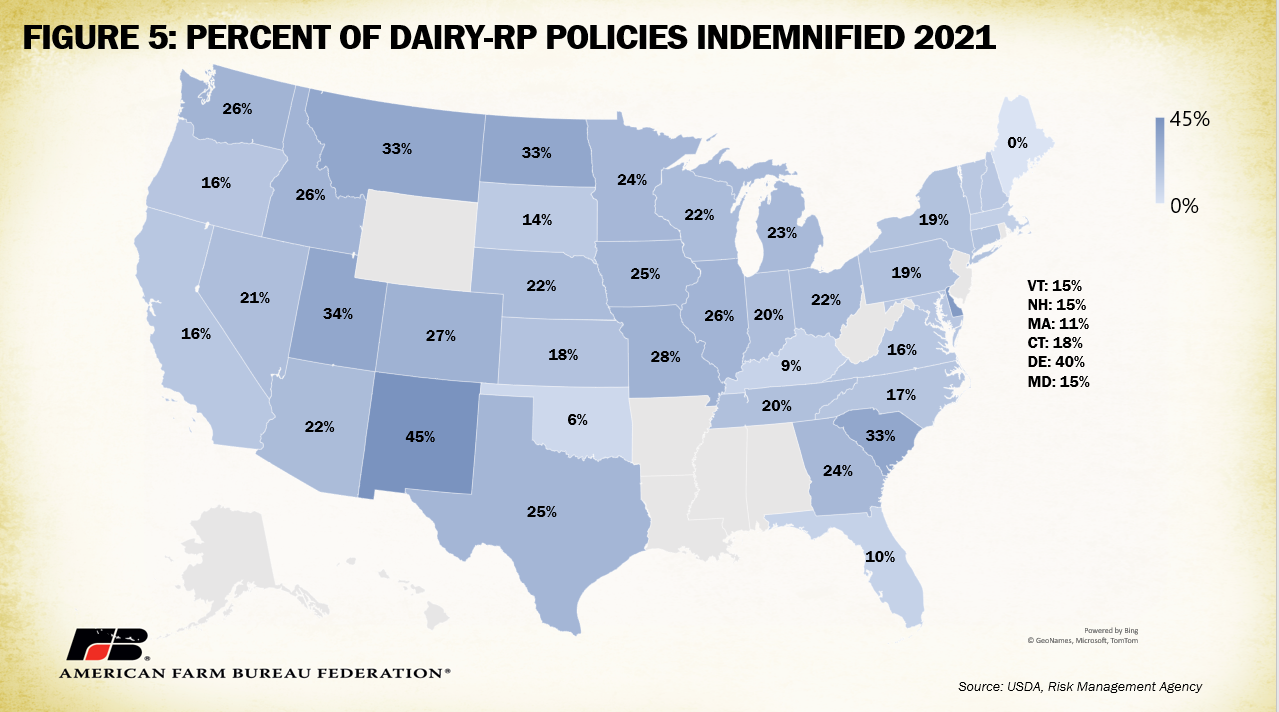

As of Nov. 22, in 2021, 18,773 DRP policy endorsements were sold, compared to the total 15,022 policy endorsements sold in all of 2020. This is a 3,751 jump in sold endorsements, with the largest jumps in New York (+1,053), Pennsylvania (+642) and California (+445). With 3,980, or 19%, of 2021 endorsements indemnified, $95 million in payments have been made. Figures 4 and 5 display the percent of endorsements indemnified in each state for 2020 and 2021, respectively. Though milk prices have experienced volatility throughout 2021, it has not compared to the peaks and trenches of 2020, which resulted in more extreme payouts. Notably, average Base Class I prices have remained on a marginal upward trend, starting at $15.14/cwt in January 2021 and most recently $19.17/cwt for December, reducing the likelihood of DRP payouts.

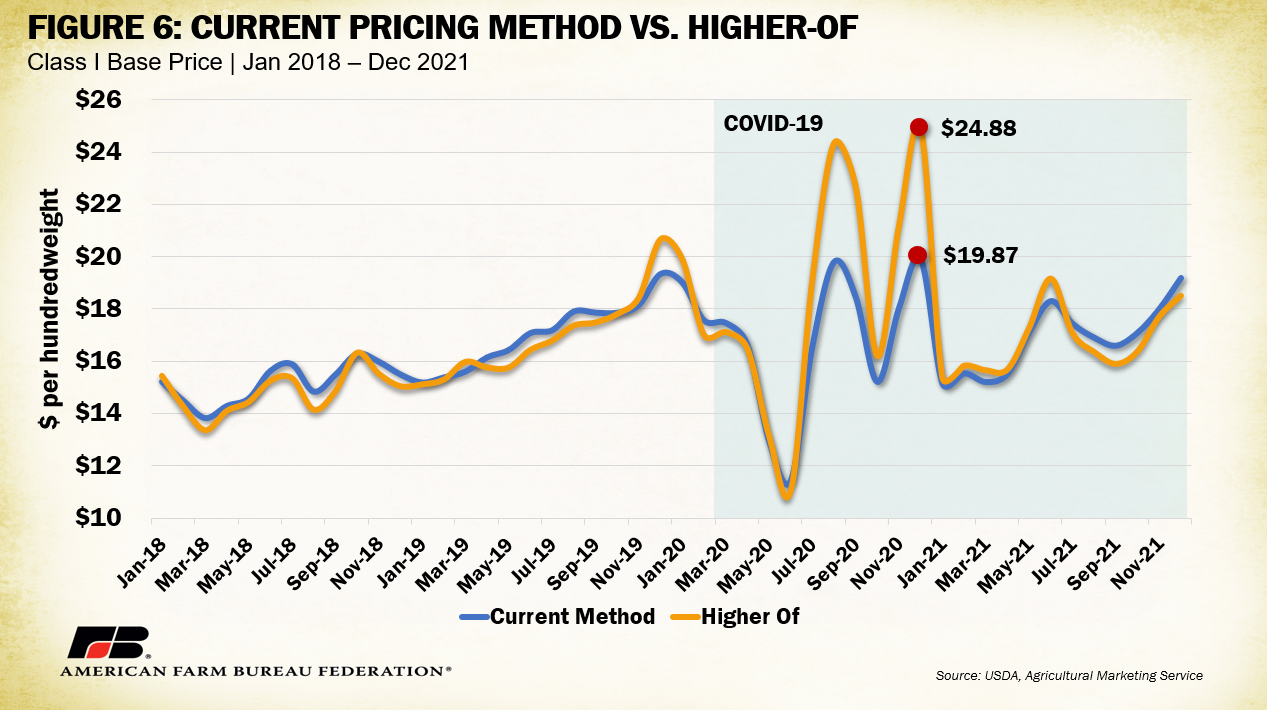

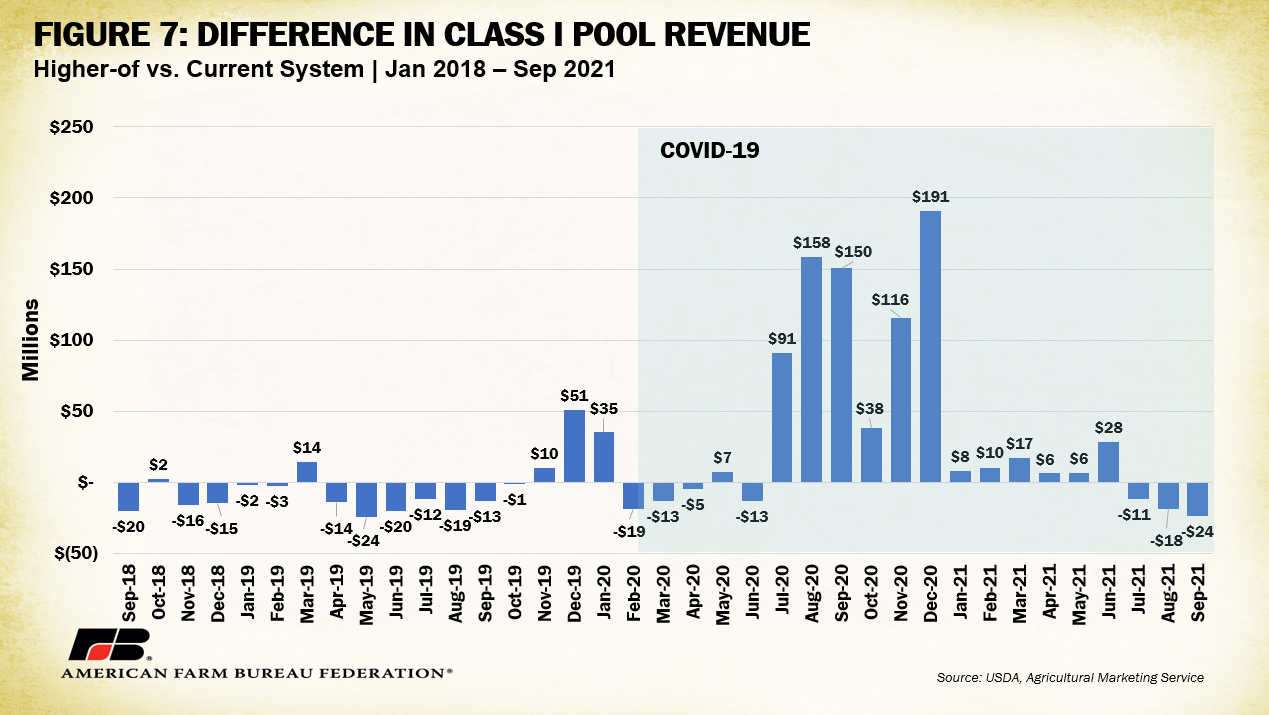

Speaking of Class I prices, farmers recovering from lopsided Class I revenue have tempered optimism about USDA’s new Pandemic Market Volatility Assistance Program (PMVAP) and its ability to fill gaps left by last year’s de-pooling. Since the 2018 farm bill, the price for Class I milk, i.e., milk used to produce beverage milk products, has been calculated using the simple average of advanced Class III (cheese) and Class IV (milk powders) skim milk prices plus 74 cents. In years prior, the formula was the higher of advanced Class III and Class IV skim milk prices. As illustrated in Figures 5 and 6, during 2020, this Class I formula change, combined with pandemic-induced price volatility, resulted in a massive price reduction from what would have occurred under the old formula: the formula change resulted in $736 million less in the federal order pool in 2020, causing widespread negative producer price differentials.

To address these perceived losses, on Aug. 19, USDA announced PMVAP, which is expected to provide $350 million in pandemic assistance payments to dairy farmers who received lower value for their milk (primarily Class I suppliers) due to market abnormalities (widespread de-pooling) caused by the pandemic. Program payments will “reimburse qualified dairy farmers for 80% of the revenue difference per month based on an annual production of up to 5 million pounds of milk marketed and on fluid milk sales from July through December 2020.” USDA is currently working with individual handlers to come up with a unique payment plan for impacted producers. Eligible handlers are said to be any handler that paid producers that had pooled milk during 2020. USDA has chosen to funnel payments through handlers and to producers to reduce administrative burdens on the USDA and take advantage of prior payment processes already utilized by the handler. The exact method handlers will use to disseminate payments will depend on the particular methods used to pool, blend and pay farmers during the pandemic. Given concerns over transparency, USDA has assured a full auditing process will be in place to ensure that farmers receive their payments and that handlers do not retain any of the funds, other than the limited allowance for farmer education. PMVAP has garnered initial criticism from farmers over its 5-million-pound limitation and adjusted gross income limitations. Others have praised it for its educational requirement that includes funding for farmer training related to better understanding the Federal Order system, risk management options, conservation and other relevant dairy topics. Above all, PMVAP is an attempt to lift some of the burden of pandemic-linked market disparities.

Conclusion

Risk management programs remain a vital safety net for dairy farmers still reeling from pandemic-induced market conditions. Higher-than-average feed prices linked to widespread supply chain challenges will continue to pressure milk margins, making 2022 Dairy Margin Coverage an advisable purchase for most farmers entering the new year. Regardless of fewer indemnity payouts in 2021, uncertainty surrounding milk prices will also keep Dairy Revenue Protection relevant to farmers looking to protect against unexpected price drops. Additionally, the Pandemic Market Volatility Assistance Program, although outside the scope of any risk management program, will attempt to fill gaps left by de-pooling and negative producer price differentials in 2020. Moving forward, farmers are keeping risk management options top of mind, with special interest in opportunities that may protect against COVID-19-like events.

Top Issues

VIEW ALL