Diesel Prices Soar, Farmers Feel the Pain

photo credit: Getty

Veronica Nigh

Former AFBF Senior Economist

Soaring Prices

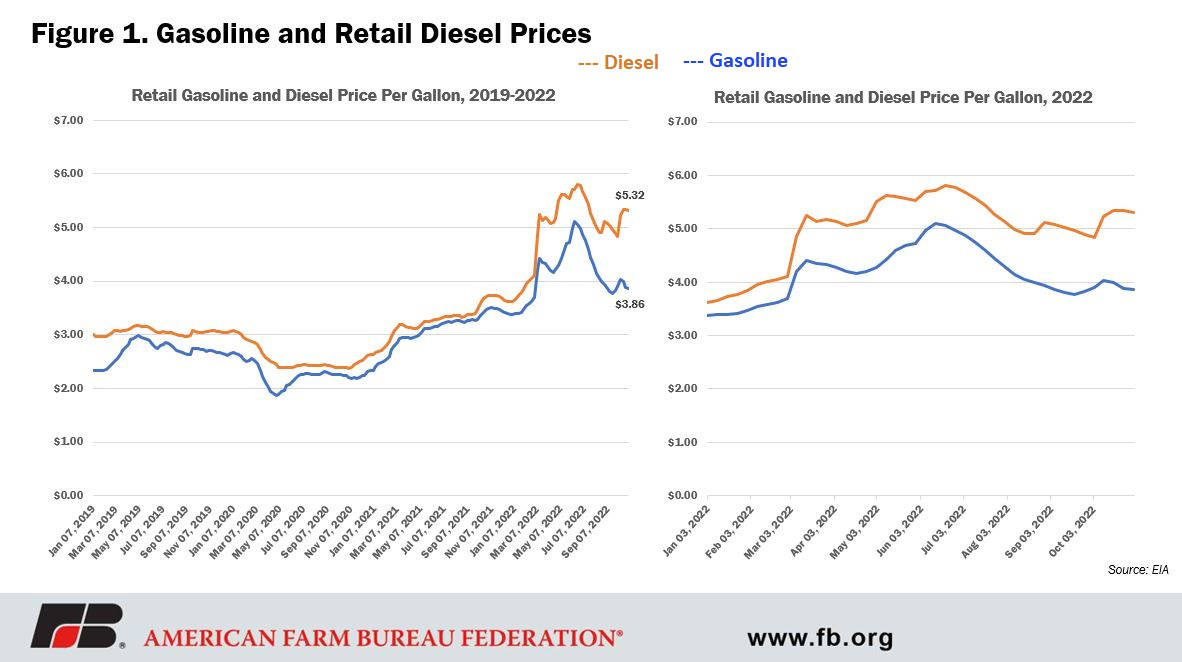

On Oct. 31, the average U.S. on-highway price of diesel was $5.32 per gallon. This is 49 cents per gallon below the June 20 peak, but still a whopping $1.59 above the same time last year. Meanwhile, the price of gasoline on Oct. 31 was $3.86, which is 38 cents above the same time last year, but down $1.25 from the 2022 peak, which was reached on June 13.

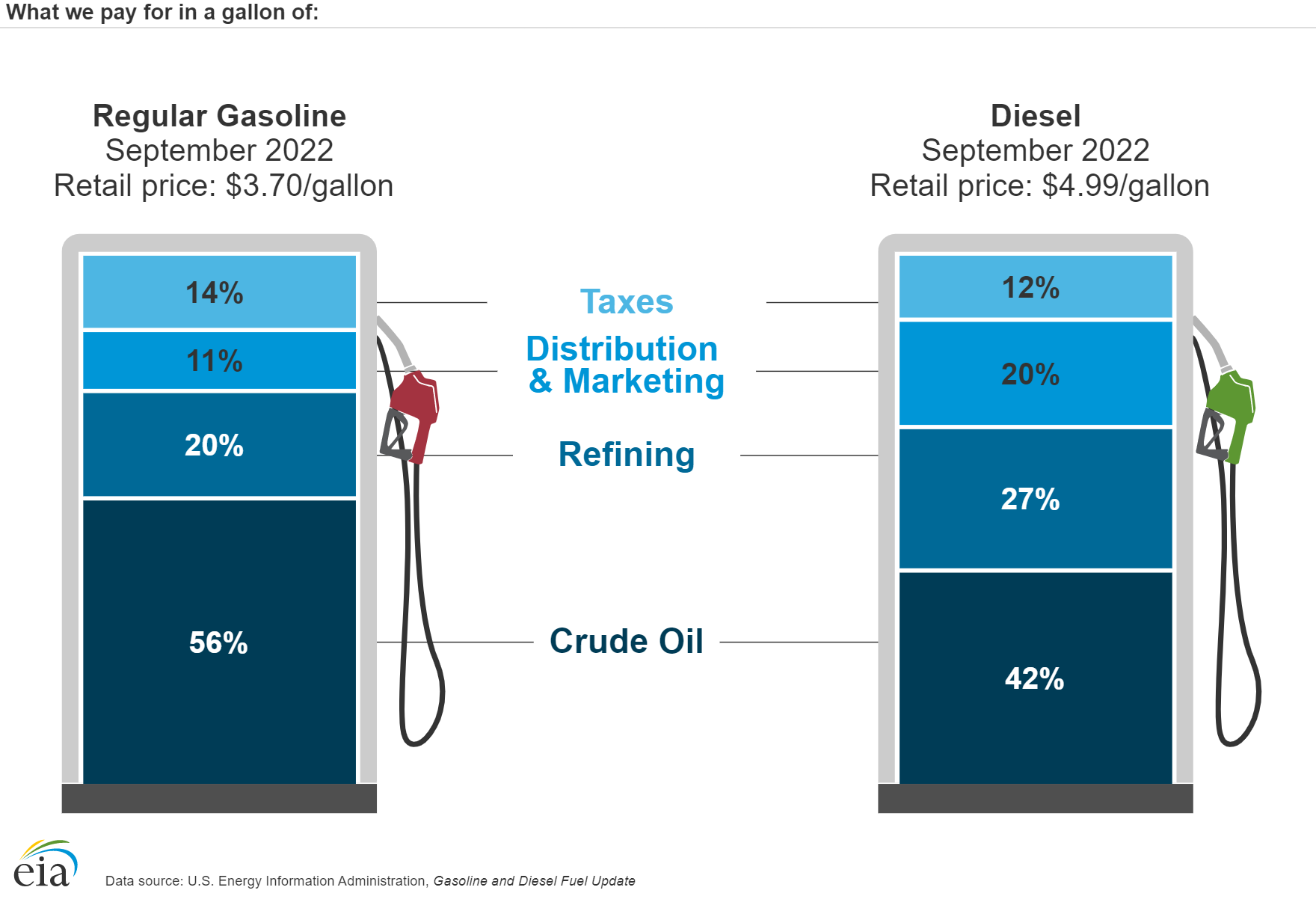

According to the U.S. Energy Information Administration, the price of crude oil is the main factor in the price of diesel fuel and gasoline, and fluctuations in the crude oil market greatly influence changes in prices. This is certainly true, but as shown in the EIA’s graphic comparing the September retail prices of gasoline and diesel, the price of crude oil is a larger share of the cost of gasoline than diesel, at 56% compared to 42%, respectively. The relative share of costs associated with refining are higher for diesel at 27% than gasoline at 20%. Additionally, the relative share of costs associated with distribution and marketing are higher for diesel at 20%, compared to gasoline’s 11%. These differences can help explain some of the spread between the retail prices of diesel and gasoline, but as we can see in Figure 1, the two fuels moved much closer together in price until 2022. What changed? As is often the case, both supply and demand forces are at play.

Supply Side Considerations

The Russian in the Room (Or not in the Room)

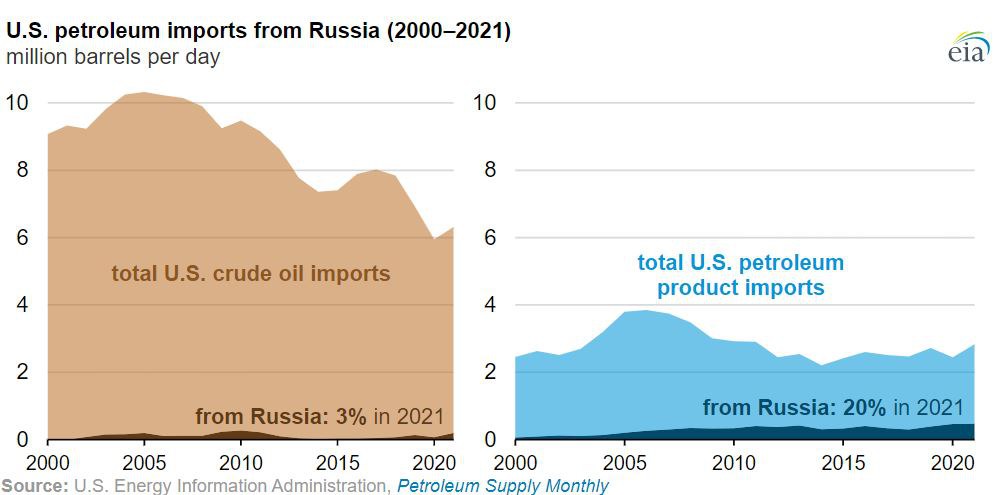

On March 8, President Biden announced a ban on U.S. imports of petroleum, coal and natural gas from Russia in response to Russia’s further invasion into Ukraine. The ban includes crude oil and petroleum products. It was well reported at the time that in 2021, imports from Russia only accounted for 3% of the U.S.’s crude oil imports. However, getting less discussion is that Russia accounted for a 20% share of U.S. imports of petroleum products in 2021. Petroleum products, namely unfinished oils and fuel oil, are used by the U.S. as a supplement to crude oil in the refining process. According to the EIA, a substantial share of the unfinished oils from Russia was used as a supplementary refinery input and has qualities similar to a heavier, relatively high-sulfur crude oil. These higher-sulfur oils are heavily used in the production of diesel fuels.

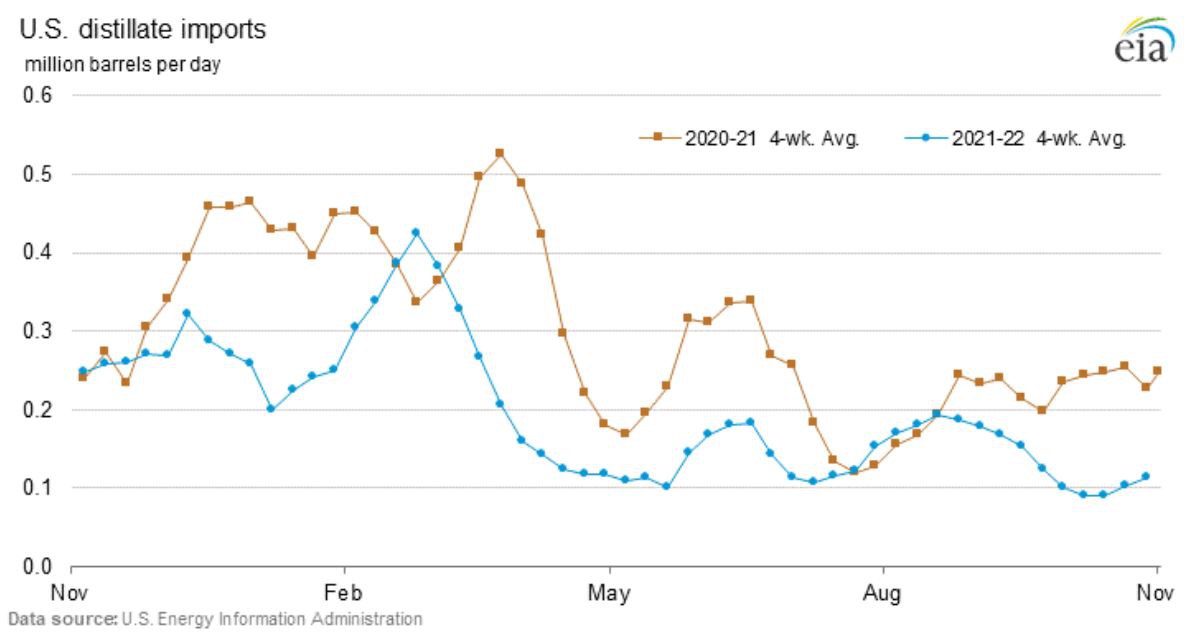

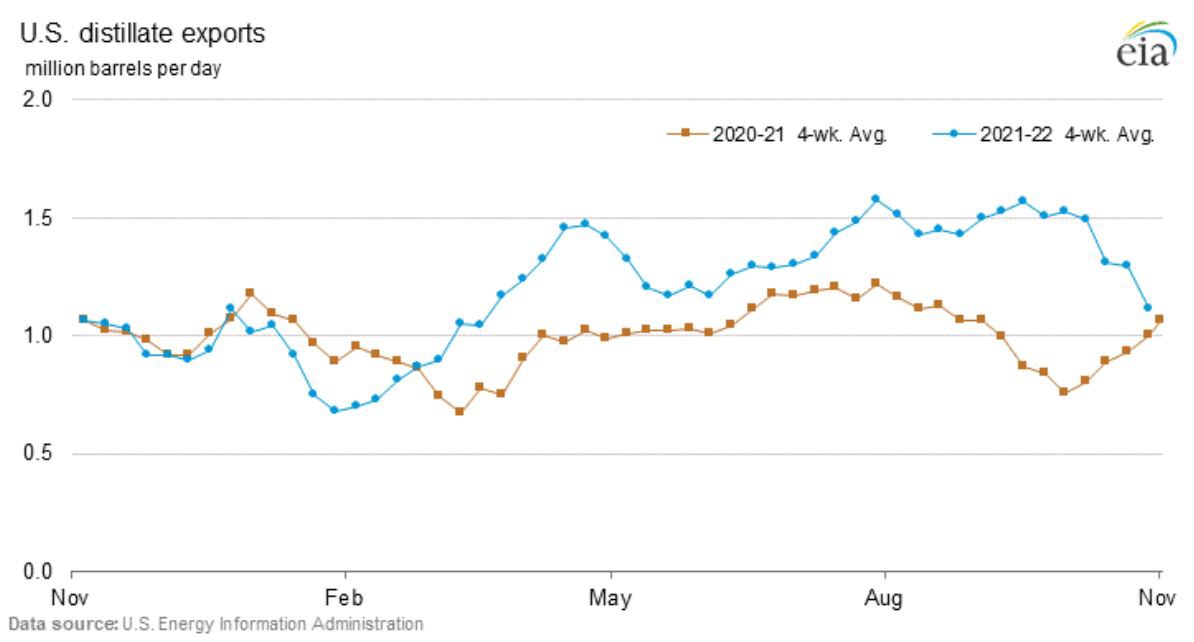

In EIA’s chart of U.S. distillate imports we observe lower imports in 2021-2022, relative to 2020-2021. Additionally, U.S. exports of distillates are higher in 2021-2022, relative to 2020-2021. (Distillate fuel oils are a general classification for one of the petroleum fractions produced in conventional distillation operations. It includes diesel fuels and fuel oils.) Russia’s invasion of Ukraine has had significant impacts on global markets for crude oil and petroleum products, not just U.S. markets. These disruptions have created unusual marketing opportunities for producers of oils and fuels and resulted in some unusual product flow. The result for the U.S. diesel market is a net decrease in distillate trade, further tightening U.S. supplies.

Refiner Production

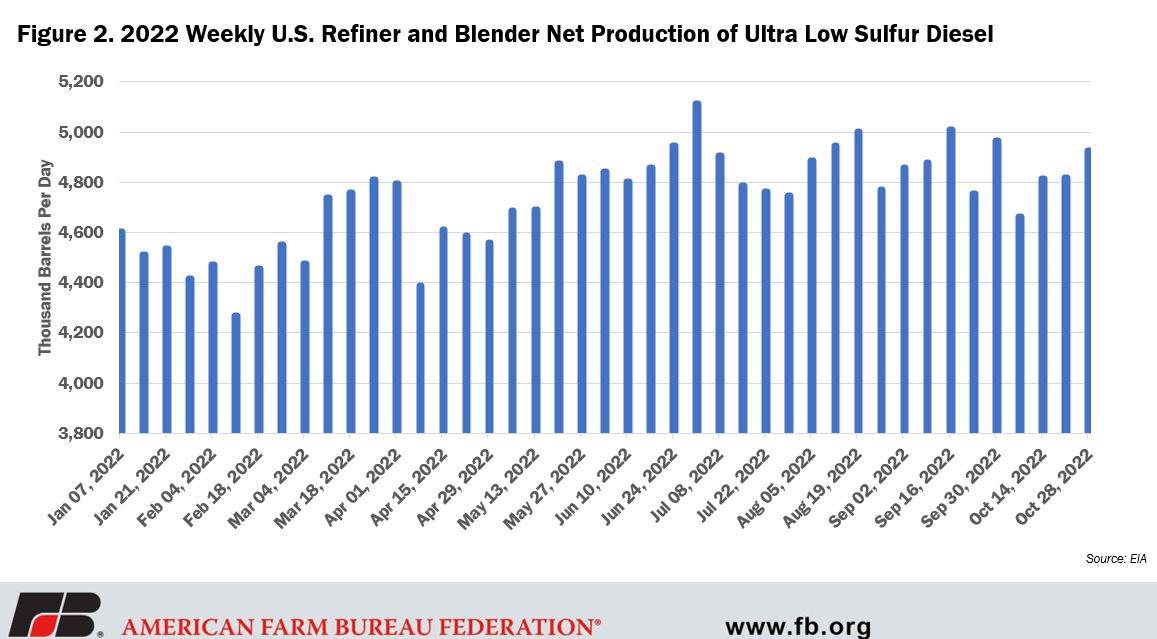

Beyond the impact of Russia, since 2019, diesel production capacity has dropped by about 180,000 barrels per day. This is equivalent to about 4% of current diesel production.

U.S. refining capacity has declined in the last two years, as plants shut during the outset of the coronavirus pandemic, causing prices to spike. Several plants that closed at the onset of the coronavirus pandemic are being converted to produce cleaner-burning renewable diesel, but those facilities are not yet online. Additionally, refiners have entered maintenance season, which further constrains availability. Data from October 28, does suggest that production has picked up somewhat over the last week, suggesting that some refiners have finished their maintenance, with their full production capability back online.

Demand Considerations

Overall, there are different seasonal price variations for the two fuels. Demand for gasoline tends to escalate in the summer as Americans hit the road on vacation. Meanwhile, demand for diesel rises in the fall and winter with increased demand from trucking, farming and heating. The increased demand in trucking is the result of increased product placement in advance of holiday shopping. Increased demand from agriculture is prompted by harvest as farmers’ demand increases dramatically. Additionally, this year, drought conditions throughout much of the country have led to low water levels on major waterways, such as the Mississippi River, diminishing the capacity of the waterway system, forcing more product into trucks for longer distances and increasing demand for diesel ever further. On the heating oil side, dropping temperatures, of course, increase use.

Stocks and Prices – The End Result

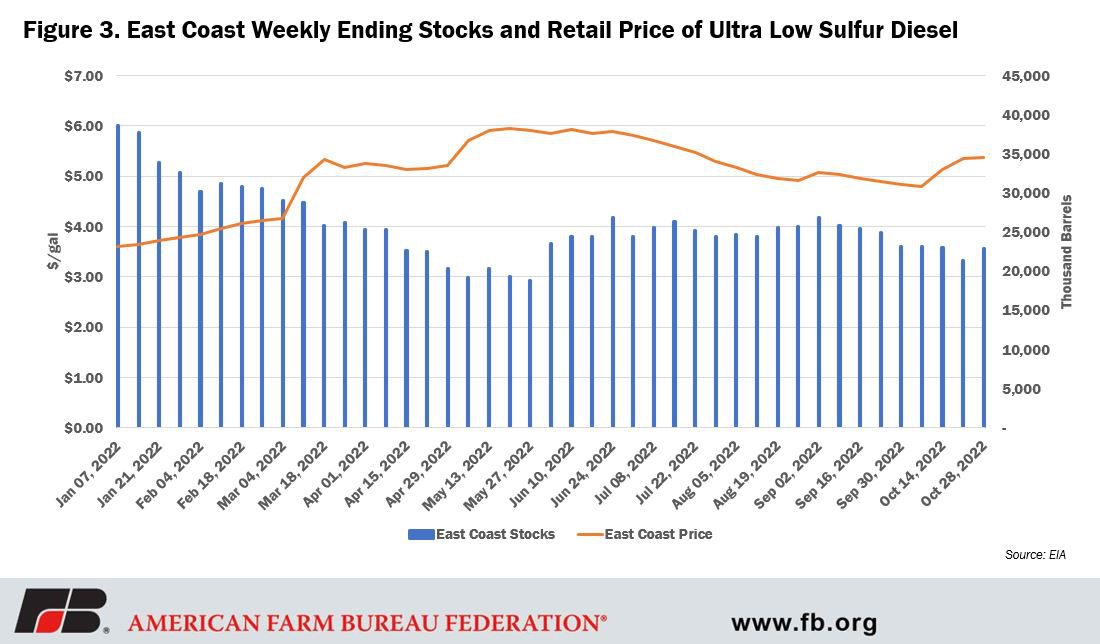

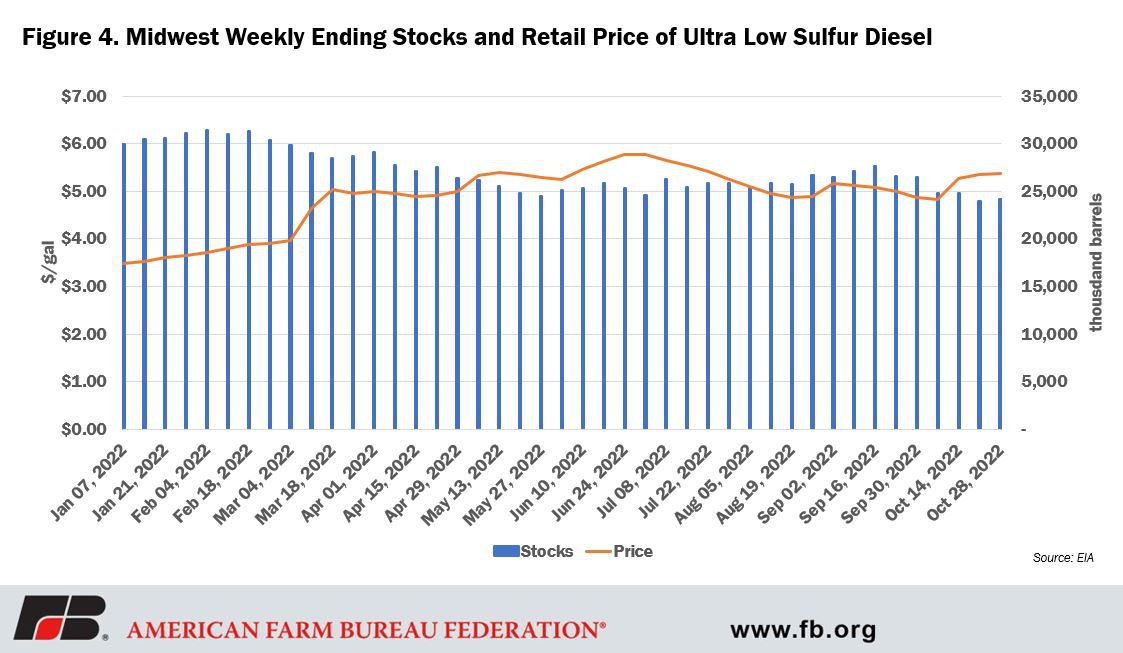

Despite a small uptick in production, industry experts have pointed out that the high price situation has created what is known as market backwardation — where prompt deliveries are priced at a premium over future deliveries — which makes building inventory extremely costly, feeding into a vicious cycle of tight supplies and price spikes. Stocks of diesel fuel are currently down 17% relative to a year ago.

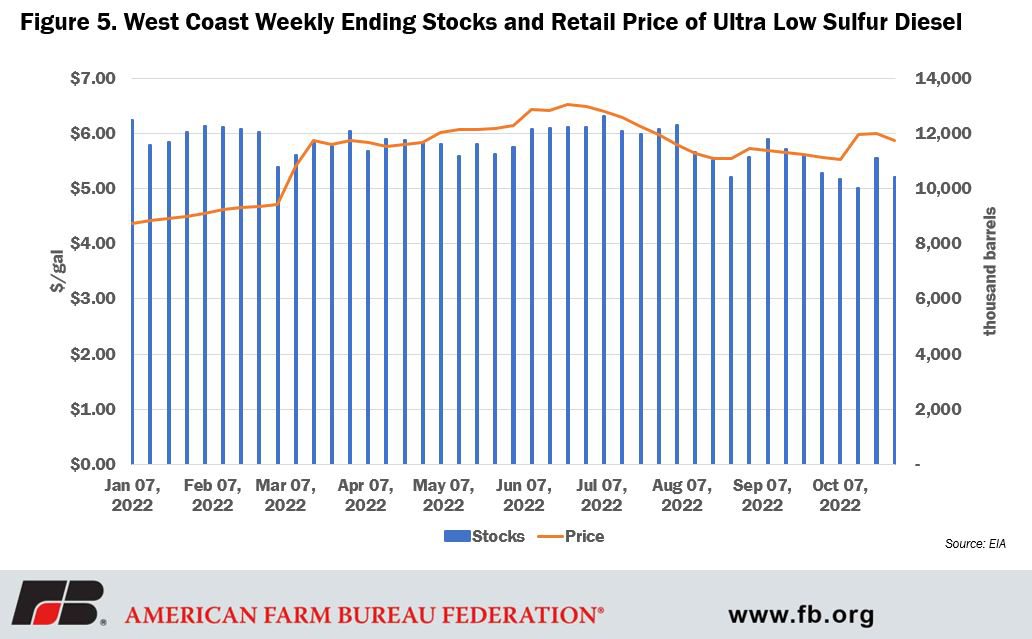

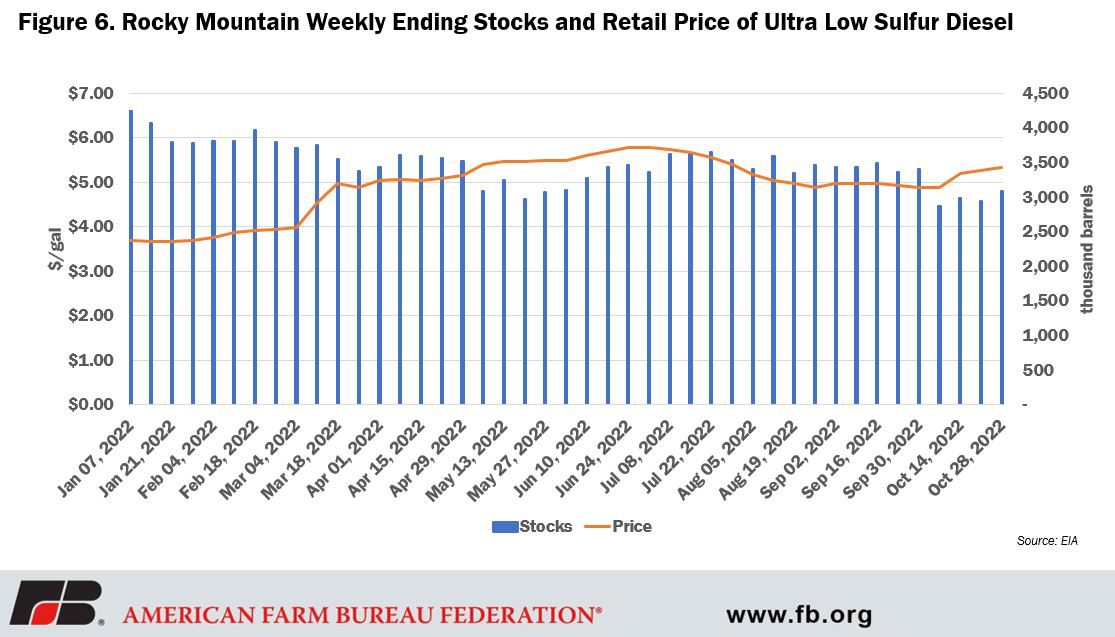

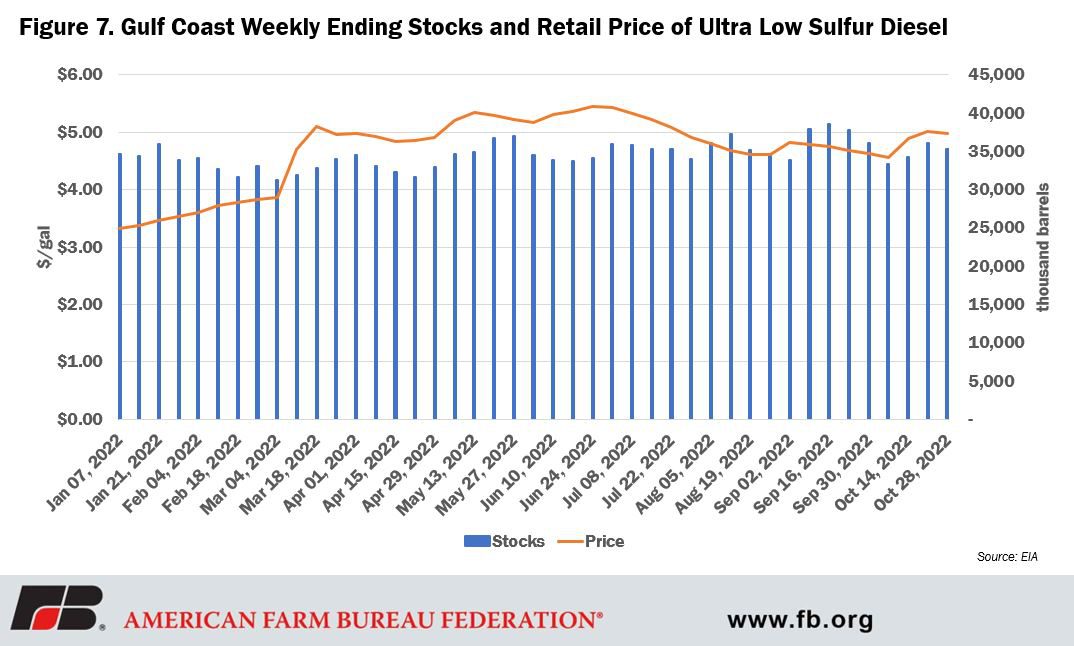

A regional analysis reveals that the decline in diesel stocks is more pronounced in some parts of the country than others. The East Coast leads the pack, with stocks down 37% compared to last year. The Midwest is down 15%, while the West Coast and Rocky Mountain regions are down 11% and 9%, respectively. The Gulf Coast region is up 1% relative to the same time last year. The East Coast tends to have the highest usage of heating oil as a heat source, which adds additional demand.

The EIA projects national diesel prices to average $4.86 per gallon in fourth quarter 2022 and $4.29 per gallon in 2023. We’re going to have to hurry to see prices reach these levels.

Conclusion

The diesel market is tight and will likely remain so throughout the end of 2022. The underlying increase in demand shows no sign of letting up, while it’s anyone’s guess when Russia’s actions in Ukraine will come to an end and bring some sense of normalcy back to the oil markets. Because of these combined factors, divergence between diesel and gasoline prices is likely to remain high, at least in the short to medium term. Diesel prices have largely exceeded gasoline prices since at least 2010, but in the period of 2010 through 2021 the average price premium of diesel was about 25 cents, a far cry from 2022’s average of 84 cents and Oct. 31’s $1.46 spread. In the long term, diesel prices will likely remain above gasoline prices, though with a smaller gap than we see today. Market and policy support for renewable diesel production could help shrink that gap further and help make the U.S. diesel market more energy independent.

Top Issues

VIEW ALL