Drop in Soybean Exports Coincides with Steely Announcements on Trade

TOPICS

Trade

photo credit: North Carolina Farm Bureau, Used with Permission

Veronica Nigh

Former AFBF Senior Economist

Over the last few weeks we have written that soybean exports in the 2017/18 marketing year are projected lower than last year. We’ve also written about the impact the administration’s announcements, actions and even potential announcements or actions have had on exports of U.S. grain sorghum to China. This article combines those two thoughts. Is the U.S. soybean sector set to follow a similar path as sorghum when it comes to China? USDA weekly export sales data suggests we should be on alert.

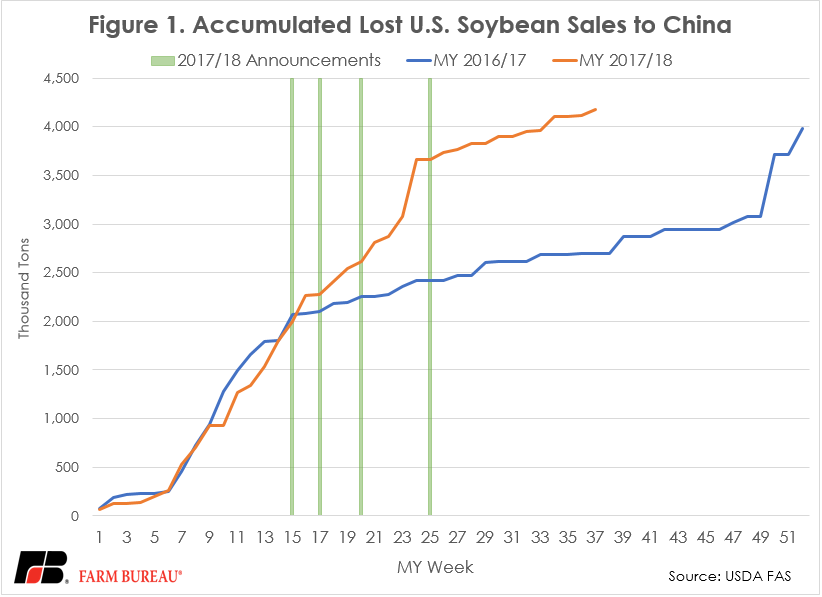

Clearly there are lots of factors that influence sales, and to truly isolate the impact of the administration’s verbiage on the soybean market would take robust economic analysis. However, by lining up the dates of different announcements related to steel and aluminum tariffs with data from USDA’s weekly Bell Report on exports, we begin to see a relationship between the two. Below we describe each “event” represented by a green line in Figure 1. It is important to remember that USDA’s sales reporting reflects sales activity from the week previous.

The first event occurred on Dec. 5, 2017, when the U.S. Department of Commerce announced a preliminary affirmative ruling that imports of certain steel and steel products imported from Vietnam but produced from substrate originating in China, were circumventing anti-dumping and countervailing duty (AD/CVD) orders that were in place against those products imported from China. In short, the Commerce Department found that China was transshipping certain steel products through Vietnam to avoid existing AD and CVD duties.

The ruling came with sizable tariffs against the products in question. Duties of more than 200 percent were applied to corrosion-resistant steel and 500 percent on certain cold-rolled steel flat products produced from substrate originating in China and imported from Vietnam. Additionally, the ruling pronounced that the duties would apply to all shipments entering the U.S. on or after Nov. 4, 2016, the day the circumvention inquiries were initiated. The precedent of retroactively applying tariffs was perhaps more significant than the action itself. The ruling came in week 15 of the soybean marketing year.

The second market impact was felt on Dec. 19, 2017, after an administration official was extensively quoted discussing a new strategy document that detailed potential steel and aluminum tariffs. China and Russia, to no one’s surprise, were specifically named as potential targets of those tariffs. The impact of these comments began to be reflected in week 17 of the marketing year.

The third market impact occurred on Jan. 11, when the Commerce Department announced that President Donald Trump had the results of its probe into whether steel imports threaten U.S. national security, but declined to reveal any details. Given previous official and unofficial statements from the administration, it was widely assumed that Commerce Department would recommend that duties should be applied. The date of the Commerce report coincides with the week 20 Bell Report.

Finally, the fourth market observation came in week 25 when the results of the investigation on steel and aluminum imports were announced. On Feb. 16, the report declared that imports of steel and aluminum from China and other countries were a threat to national security and, as such, tariffs of 25 and 10 percent, respectively, would be applied.

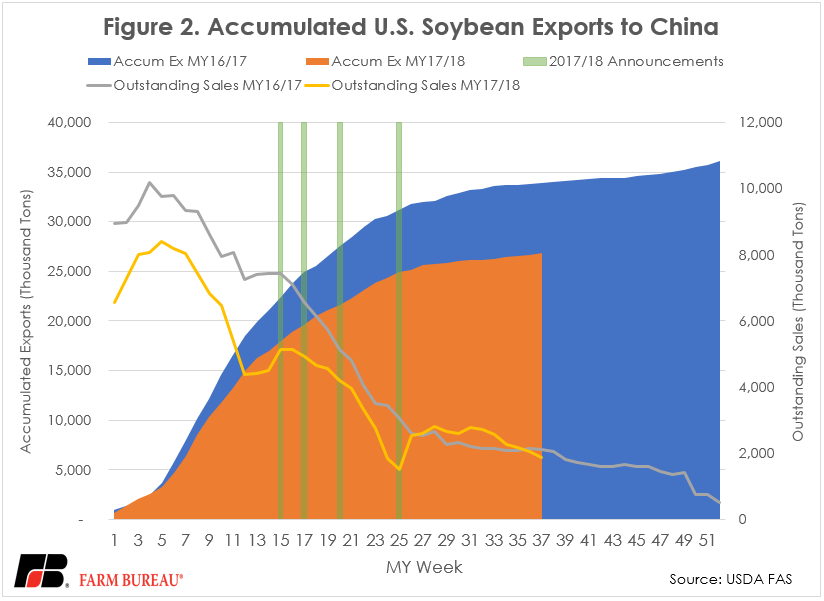

As of this article’s posting, the soybean marketing year, in its 37th week, is only 70 percent over. Yet, accumulated lost sales (cancellations, foreign purchases and destination changes) of U.S. soybeans to China have already exceeded the total accumulation of lost sales during the entire 2016/2017 marketing year. In fact, we exceeded that level two weeks ago. Cancelled sales began to get media attention when the May 3 Bell Report showed nearly 142,000 metric tons in lost sales during that week. The attention over this has died down in the last few weeks, when no additional cancellations were noted in the May 10 report. Hopefully, lost sales have come to an end. If 2017/18 follows 2016/17, the next 10 weeks will be quiet. However, Figure 2 clearly highlights some of what we already knew – exports are down and there doesn’t seem to be a large volume of sales waiting to be exported.

Top Issues

VIEW ALL