Tensions With China Take A Bite Out of U.S. Soybean Acreage

TOPICS

Wheat

photo credit: Sgt. Mikki Sprenkle/Public Domain

John Newton, Ph.D.

Vice President of Public Policy and Economic Analysis

USDA recently released several tables previewing the annual long-term Agricultural Projections to 2028 (the complete projections will be released in February 2019). These early-release tables provide USDA’s estimates on the supply and demand for agricultural commodities for the next 10 years and take into consideration macroeconomic conditions, gross domestic product growth, population growth and farm policy, among other factors.

Given the current U.S.-China trade environment -- U.S. Soybean Exports to China Fall Sharply -- a key takeaway from these projections was the impact on soybean and other field crop acreage, soybean exports, soybean ending stocks and, finally, prices.

For the 2019 crop year, USDA projects soybean planted acreage will decline by 6.6 million acres, dropping from a record 89.1 million acres planted in 2018 to 82.5 million acres. If realized, this would be the third-largest acreage decline of all time and the largest year-over-year decline in soybean plantings since the beginning of the Renewable Fuels era in 2007. The decline in soybean acreage is anticipated given the slow pace of soybean exports, the dramatic decline in Chinese purchases, expectations for a nearly billion-bushel-carryout and projections for decade-low soybean marketing year average prices.

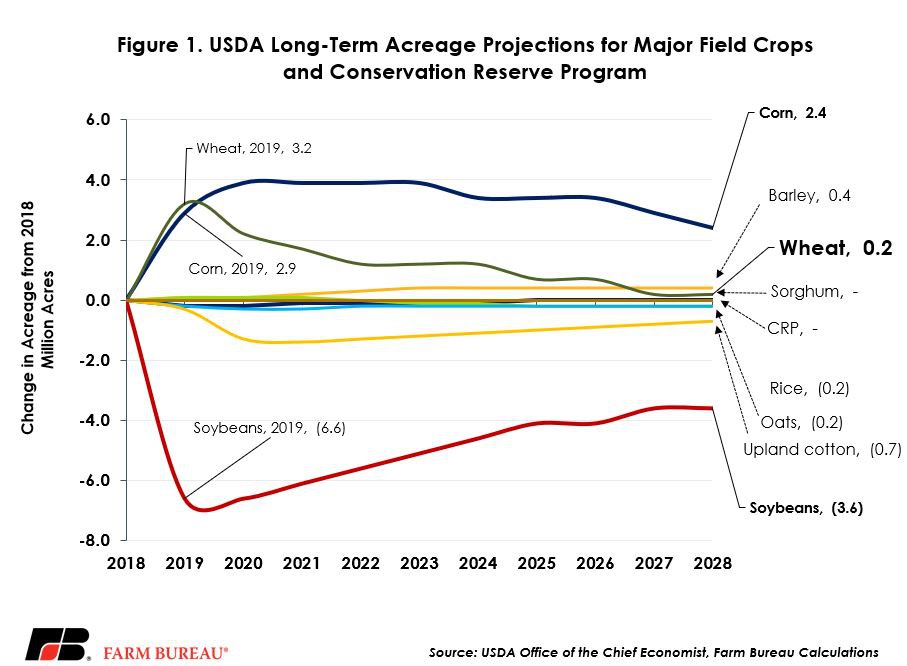

With acreage moving out of soybeans, growers are expected to plant 92 million acres of corn in 2019, up 2.9 million acres, and 51 million acres of wheat, up 3.2 million acres. Barley and oats are expected to see 100,00 additional acres planted in 2019. Upland cotton planted area is expected to decline 300,000 acres to 13.5 million acres, and rice acreage is expected to decline 200,000 acres to 2.7 million acres. Sorghum acres are also expected to decline by 200,000 acres, landing at 5.6 million acres. For the eight major crops and Conservation Reserve Program acreage, planted acreage plus CRP acreage is expected to decline 1.3 million acres to 275.1 million acres.

Notable in USDA’s long-term projections: soybean acreage is expected to remain below 2018’s record-high for the next decade – remaining at or below 86 million acres planted each year, Figure 1. The main beneficiaries of the pullback in soybean acres are expected to be corn and wheat in the short-run and corn in the long-run, with corn acres remaining near 92 million to 93 million acres planted over the next decade, Figure 1.

In October, USDA World Agricultural Supply and Demand Estimates projected U.S. soybean exports at 2.06 billion bushels for the 2018/19 crop year. Going forward, USDA projects soybean exports to increase 1 percent annually, reaching 2.26 billion bushels by 2028 – a lofty goal if better trade relations are not restored with China.

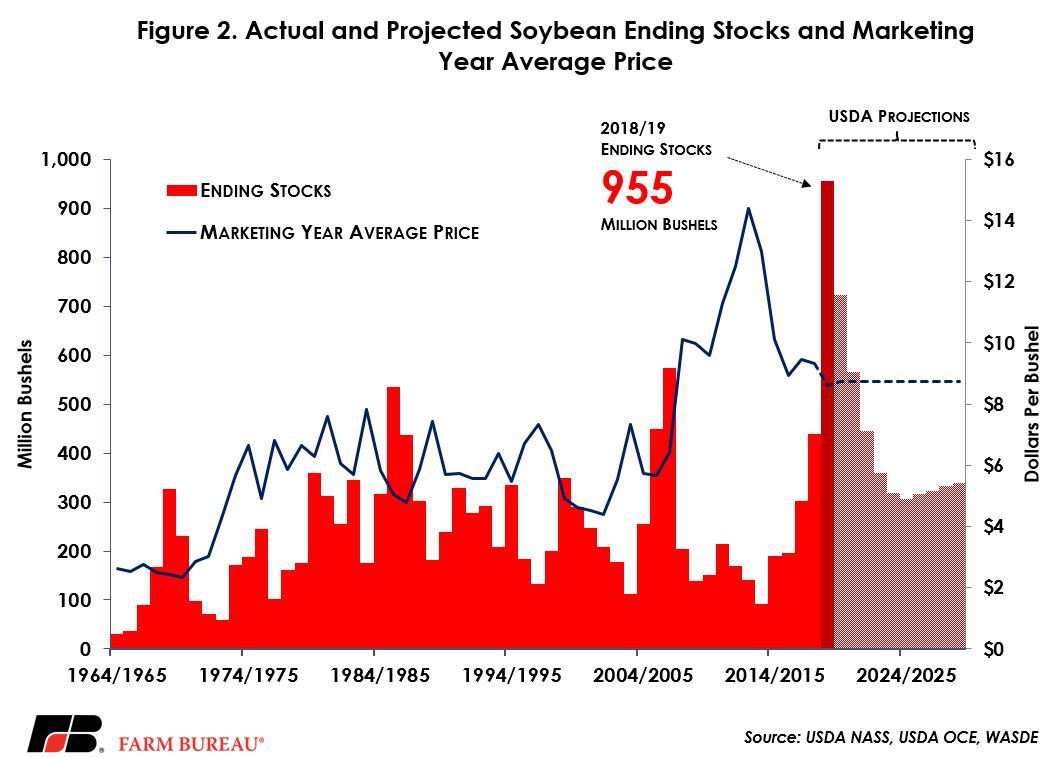

Expecting a combination of lower acreage and continued growth in total use, USDA projects soybean ending stocks to fall from the record-high 955 million bushels expected for the 2018/19 marketing year. Soybean prices are expected to remain flat over the next decade, averaging $9.50 per bushel, Figure 2.

Summary

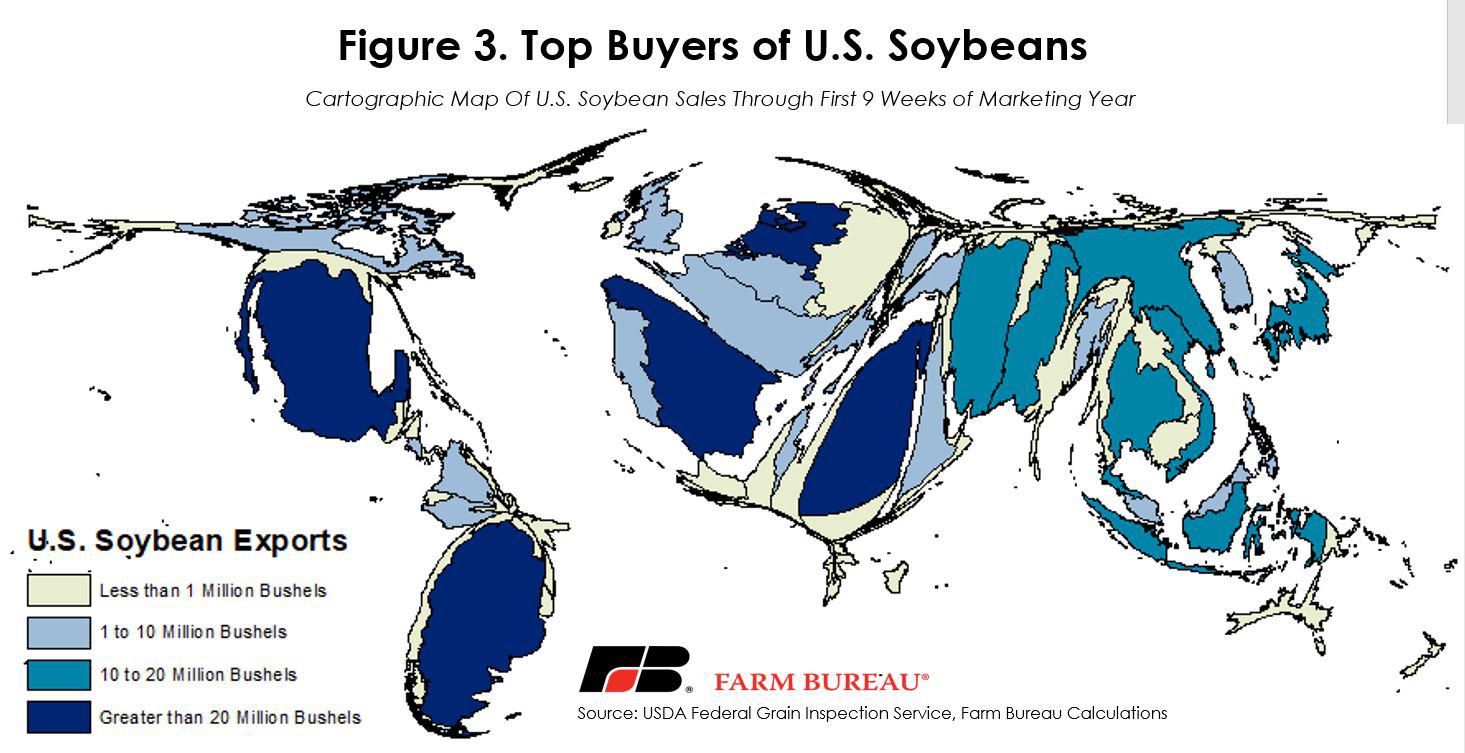

The outlook for U.S. soybeans is increasingly uncertain due to trade tensions with China, the – largest buyer of the commodity. The pace of exports this year remains well below the level needed to meet USDA’s projection of 1.9 billion bushels. Currently, the top buyers of U.S. soybeans include Mexico, Spain, Argentina, the Netherlands and Egypt, Figure 3.

In reducing soybean planted area USDA recognized the headwinds U.S. growers are facing, but the department continues to project growing soybean exports, declining ending stocks and stability in soybean prices. For this scenario to unfold, U.S. soy must find new markets and backfill markets previously supplied by our South American competitors – or quickly restore access to the Chinese market.

Top Issues

VIEW ALL