2025 Specialty Crop Bridge Payments Finalized

Daniel Munch

Economist

Key Takeaways

- USDA has finalized the Assistance for Specialty Crop Farmers (ASCF) Program, making $1.625 billion in one-time payments available to producers of eligible fruits, vegetables and tree nuts based on 2025 planted and reported acreage. Applications open June 1, 2026, and close August 7.

- ASCF payments are structured as flat per-acre rates across four tiers, ranging from $25 to $650 per acre, based on average national revenue per acre for each crop.

- The ASCF Program covers eligible fruits, vegetables and tree nuts as defined under the USDA Specialty Crop definition. Floriculture, nursery crops, herbs, hops and other horticultural commodities are not included.

- Controlled environment agriculture, with limited exceptions for mushrooms, is excluded from eligible acreage.

- The $1.625 billion available under ASCF reflects a $625 million increase over the $1 billion originally announced.

USDA has finalized details for the Assistance for Specialty Crop Farmers (ASCF) Program, establishing approximately $1.625 billion in economic assistance for producers of eligible fruits, vegetables and tree nuts. The program provides one-time bridge payments intended to help offset elevated production expenses and market challenges experienced during the 2025 crop year.

The announcement closes a question left unresolved when USDA unveiled the broader Farmer Bridge Assistance (FBA) Program earlier this year. At the time, $11 billion was immediately directed to producers of covered commodities, while USDA indicated an additional $1 billion would be reserved for specialty crop and sugar producers pending further analysis.

This assistance is much needed as specialty crop farmers continue to navigate weak returns, elevated labor expenses, high borrowing costs and increasing import competition. The final rule provides that clarity, but also highlights a broader challenge: specialty crop agriculture remains significantly harder to evaluate through traditional economic safety-net frameworks than most row crop sectors.

How ASCF Payments Work

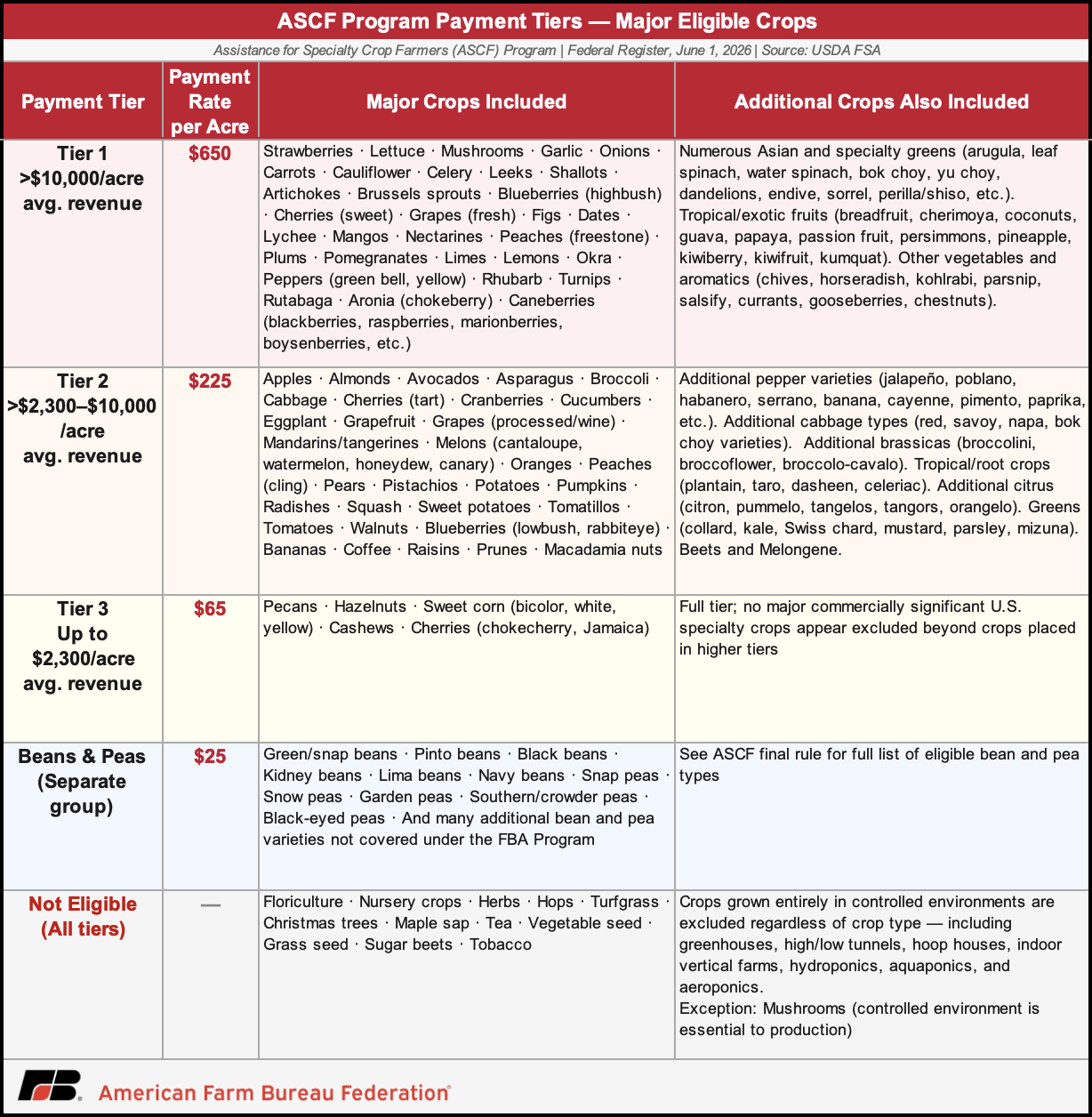

ASCF payments are calculated by multiplying a producer's eligible planted acres of each specialty crop, as reported to FSA by April 24, 2026, by the per-acre payment rate assigned to that crop's tier. USDA established four payment groups based on average annual revenue per acre, using 2024 National Agricultural Statistics Service (NASS) yield data and NASS or Agricultural Marketing Service (AMS) price data as primary sources.

Tier 1, at $650 per acre, covers the highest-revenue specialty crops (those averaging more than $10,000 per acre annually) including strawberries, lettuce, fresh grapes, highbush blueberries and sweet cherries. Tier 2, at $225 per acre, covers crops averaging between $2,300 and $10,000 per acre, a broad middle group that includes apples, almonds, potatoes, tomatoes and wine grapes. Tier 3, at $65 per acre, applies to a small group of relatively lower-revenue crops including pecans, hazelnuts and sweet corn. A separate beans and peas group receives $25 per acre for varieties not already covered under the FBA Program.

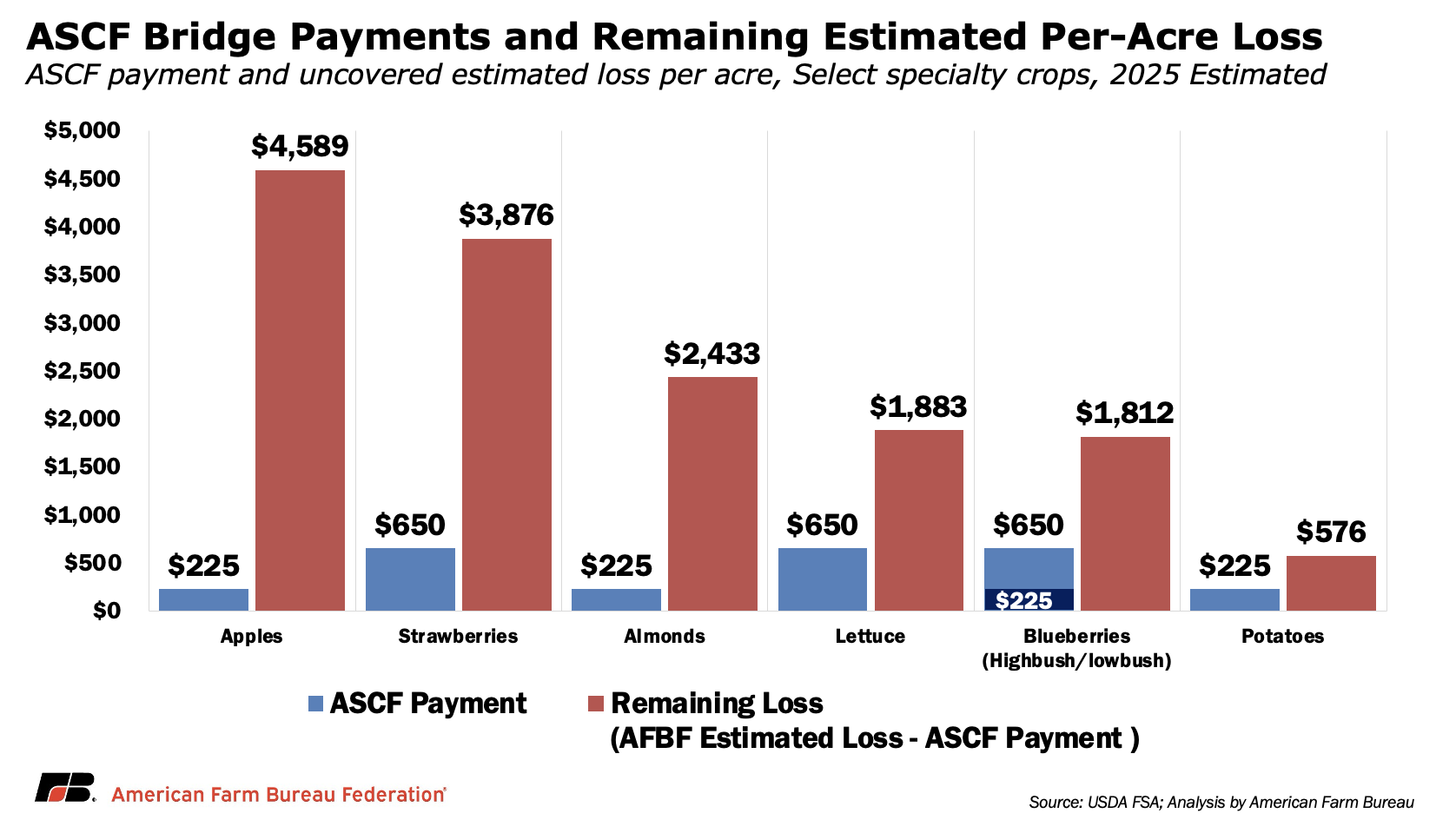

ASCF is designed as a bridge program, providing near-term cash-flow assistance rather than full compensation for economic losses. Across the crops where losses are best documented, payment rates cover a meaningful but modest share of losses producers absorbed in 2025, leaving substantial uncovered losses even after ASCF payments are applied. For example, for strawberry growers receiving $650 per acre, an estimated $3,876 per acre in losses remains; for apple growers receiving $225, the remaining gap is $4,589 per acre. The remaining gap highlights why discussions around longer-term risk management, economic assistance and safety-net improvements continue across specialty crops and other sectors facing similar margin pressure.

The variation within a single crop can be just as wide. Apple growers farming high-density vertical spindle systems in Washington face total production costs of $46,000–$55,000 per acre, far above the national average revenue that anchors the Tier 2 rate, while traditional low-density orchards carry substantially lower per-acre costs but also lower yields and revenue. Both receive $225 per acre. Similarly, strawberry producers on intensive plasticulture systems face production costs exceeding $110,000 per acre, while lower-intensity operations in the same crop face a very different cost structure. The flat rate is an administratively workable solution, but producers in high-cost, high-intensity systems will find it offsets a smaller share of their actual per-acre losses than the national average might suggest.

Payment limits include a $250,000 cap per person or legal entity and an average adjusted gross income limit of $900,000 (averaged over tax years 2021–2023). These terms are notably more generous than the FBA Program's $155,000 per-entity cap, reflecting the higher per-acre revenue and cost structures common in specialty crop production.

Notably, for perennial fruit and nut crops, both bearing and non-bearing acreage are eligible for payments. This reflects USDA recognition that growers continue to incur significant costs on orchards and plantings before they reach commercial production, even when those acres are not yet generating marketable output.

What the Program Does — and Doesn't — Capture

The Controlled Environment Exclusion

ASCF excludes acreage grown in controlled environments, defined broadly to include greenhouses, high and low tunnels, hoop houses, indoor vertical farms and hydroponic, aquaponic and aeroponic systems. USDA determined that these production systems can extend growing seasons and reduce certain production and market risks relative to traditional field-grown agriculture. As a result, acreage grown in controlled environments is generally not eligible for ASCF payments.

Mushrooms are the primary exception. USDA noted that controlled environments are integral to mushroom production rather than a production choice used to manage risk.

The exclusion means some specialty crop operations will not qualify for assistance despite facing many of the same economic pressures, including labor, energy, financing and compliance costs.

Wild Blueberries and Atypical Production Structures

The ASCF payment structure is built around FSA-reported planted acreage, which suits most specialty crops reasonably well. However, wild blueberry production in Maine, Michigan, and other northeastern states differs. Wild blueberry fields are perennial managed barrens, not planted acreage in the conventional sense, and production rotates on a two-year cycle across managed fields. Reporting structures for these acres may differ from planted specialty crops, and growers will need to work closely with local Farm Service Agency (FSA) county offices to ensure their acreage is captured accurately.

This reflects a broader reality the ASCF Program navigates throughout: specialty crops are not a single sector. Over 350 commodities grown under distinct regional production systems and marketing arrangements make standardized program design difficult. The ASCF Program's acreage-based approach is a practical solution, but producers with non-standard acreage measurement, multi-year or non-annual cropping cycles, or extensive controlled environment infrastructure should verify how their operations will be treated before the Aug. 7, 2026, application deadline.

Crops Outside Current Bridge Assistance Programs

ASCF addresses eligible specialty crops, while separate USDA funding has been reserved for sugar producers. Together with the FBA Program, these initiatives cover a large share of U.S. agricultural production, but some sectors remain outside the current bridge assistance framework. Alfalfa and other forage crops, for example, were not included in either the FBA Program or ASCF despite ongoing economic challenges.

The Original $1 Billion vs. $1.625 Billion

When the FBA Program was announced, USDA reserved $1 billion for specialty crops and sugar. The ASCF final rule establishes a program budget of $1.625 billion, a $625 million increase, allocated exclusively to specialty crop fruits, vegetables and tree nuts (sugar is addressed separately). USDA has not publicly detailed how the additional funding was determined, but the final rule notes that total outlays will depend on the volume of applications submitted and approved, with a program cap of total authority at $1.625 billion.

How to Apply

Eligible producers must have planted qualifying specialty crops in 2025 and filed a crop acreage report (FSA-578) with FSA by April 24, 2026. FSA will prepare a pre-filled application (CCC-556) for each eligible producer. Applications are available through the ASCF program webpage electronically beginning June 1, 2026, or at any FSA county office beginning June 8, 2026. The application deadline is Aug. 7, 2026.

Producers must also ensure the following eligibility forms are on file: CCC-902 (Farm Operating Plan), CCC-941 (AGI Certification), and AD-1026 (Conservation Compliance). These forms must be submitted by Aug. 9, 2027 if not already on file.

Conclusion

The ASCF Program delivers welcome financial relief to a sector that has absorbed years of mounting financial pressure while operating with fewer federal safety-net tools than many other crop sectors. The $1.625 billion in one-time bridge payments will provide partial relief as growers continue to navigate elevated costs, trade uncertainty and tight margins.

The program also highlights a longstanding challenge in specialty crop policy. Specialty crop producers generate more than $75 billion in annual farm-gate value and account for over one-third of U.S. crop sales, yet the diversity of the sector and the limited availability of consistent cost-of-production and profitability data make economic conditions more difficult to evaluate than many other areas of agriculture. Developing assistance across hundreds of crops with distinct production systems, marketing channels and cost structures requires a different analytical approach than programs designed for major commodity crops.

USDA's acreage-based payment formula is a practical solution given those constraints, but it also highlights a broader opportunity. Continued investment in specialty crop cost-of-production research, price reporting and acreage data would improve future program delivery and targeting. As the Senate continues work on a much-needed farm bill and broader discussions around economic and disaster assistance move forward, policymakers will continue to face questions about how best to support specialty crop producers and other sectors, including alfalfa and forage crops, that remain outside recent bridge assistance programs.

Top Issues

VIEW ALL