America's Top Farm-Raised Fish Faces Growing Pressures

Daniel Munch

Economist

Key Takeaways

- Many U.S. catfish farms now operate with little margin for error, as rising feed, labor, fingerling and fuel costs push production costs close to market prices – before accounting for disease, bird predation or weather losses.

- Imported Vietnamese swai has grown from virtually no U.S. market presence in the 1990s to a $330 million competitor today, with retail prices roughly $2 per pound below comparable U.S. catfish products.

- Fish-eating birds, disease and weather can quickly turn profitable production into losses. Bird predation alone can swing farm profitability by nearly $3,800 per acre, while disease costs the industry tens of millions of dollars annually.

- Despite major advances in genetics, aeration and production technology, U.S. catfish acreage has fallen by roughly 75% since its peak and the number of farms has declined from more than 1,300 to fewer than 400.

- The challenges facing catfish producers extend beyond the farm gate. Continued industry contraction threatens processors, hatcheries, feed mills and rural communities across the Southeast that depend on America's largest aquaculture industry.

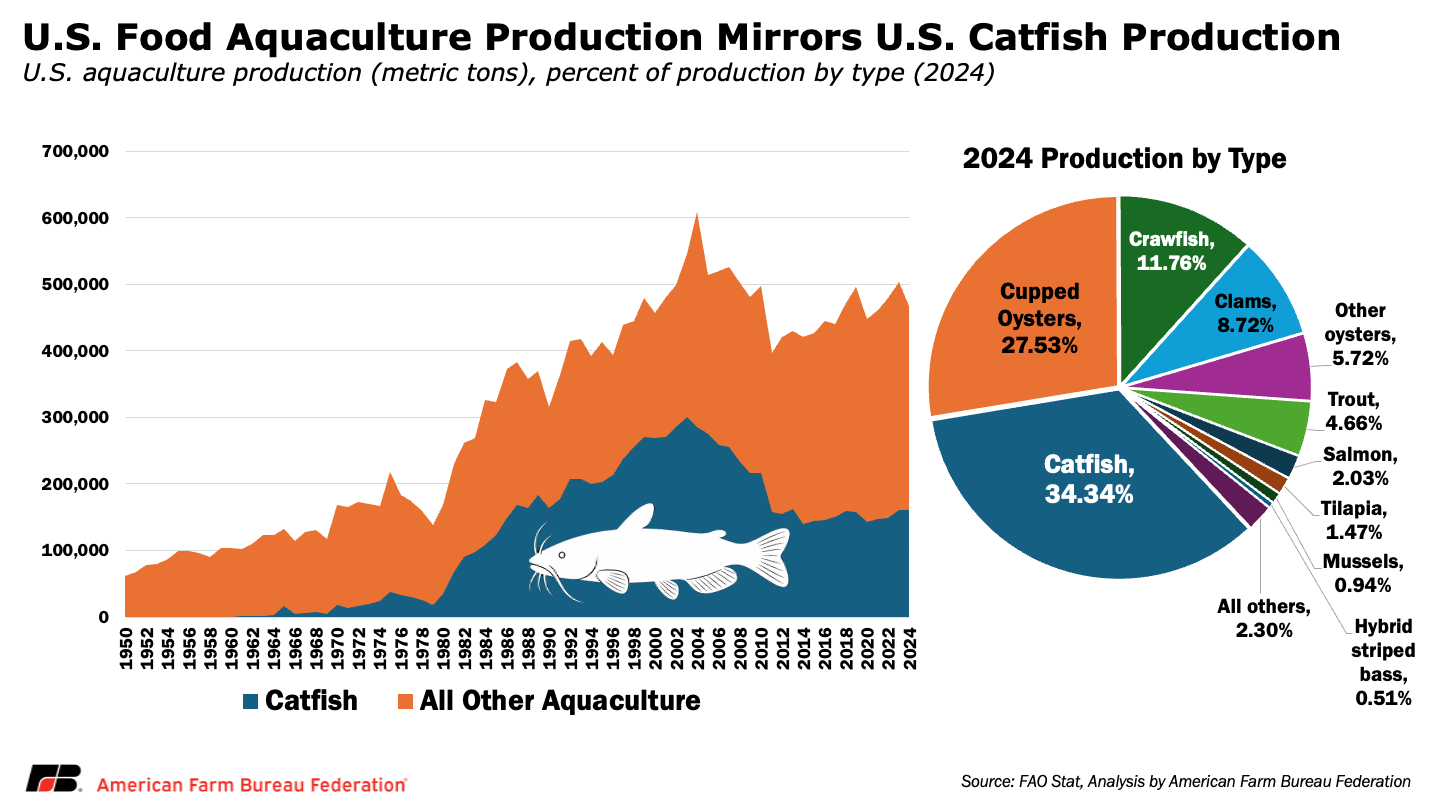

Whether served fried at a fish fry, blackened in a restaurant or sold as fillets in the grocery store, farm-raised catfish has become one of the most recognizable seafood products in the United States. It is also America's largest aquaculture industry, supporting hundreds of farms, processors, feed mills and rural communities across the country. Research from Mississippi State University, Virginia Tech, and Auburn University shows that industry contributes $1.91 billion to the tristate economy of Alabama, Arkansas and Mississippi alone, while generating $76 million in tax revenues and providing over 9,100 jobs.

But behind the familiar product is a matured industry navigating a growing list of challenges. Feed, labor, fingerling (baby fish) and energy costs have climbed steadily. Disease outbreaks and fish-eating birds continue to erode profitability. Weather extremes create additional biological risks, while imported competition has reshaped the marketplace and narrowed margins. Farmers have responded with new technologies, improved genetics and more intensive production systems, yet the number of catfish farms and production acreage continue to decline.

The result is an industry that remains a cornerstone of U.S. aquaculture but operates with increasingly little margin for error, where a disease outbreak, a spike in feed costs, or drop in fish prices, or a season of heavy bird predation or extreme weather events can quickly turn a profitable year into a financial loss.

Background: How U.S. Catfish Production Works

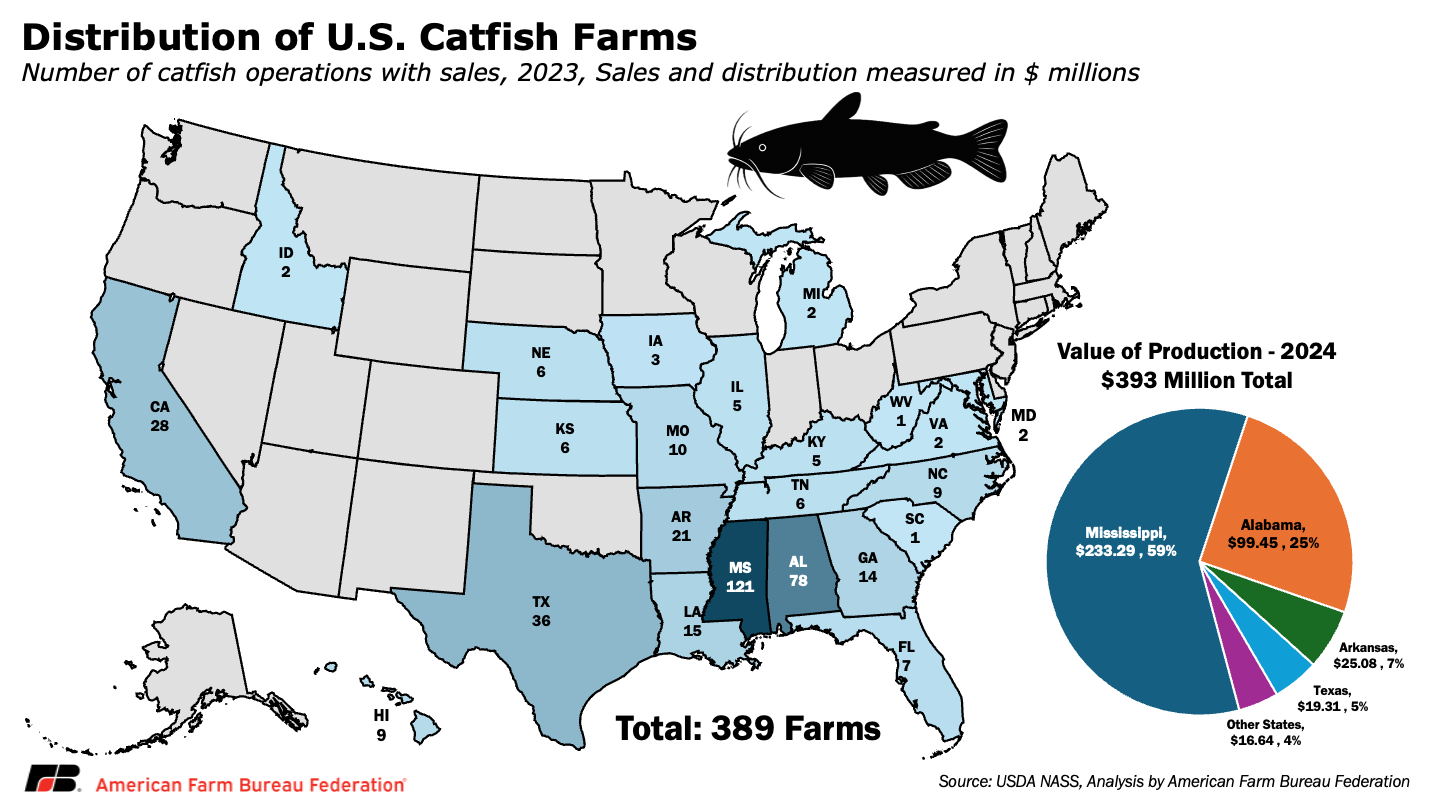

Few aquaculture industries are as geographically concentrated as U.S. catfish production. While catfish farms operate in 23 states, commercial production is overwhelmingly centered in the Mississippi Delta and surrounding states of Mississippi, Alabama, Arkansas, Louisiana and Texas. Together, those five states account for the vast majority of U.S. catfish output, with Mississippi alone producing nearly 60% of the nation's farm-raised catfish value. This concentration is no accident. The region's warm climate, abundant water resources, relatively flatland and proximity to feed mills and processing plants have made it the center of U.S. catfish production for more than half a century.

Unlike wild-caught fisheries, catfish are raised in carefully managed outdoor ponds where producers control stocking rates, feeding, water quality and harvest timing. Most fish begin life in hatcheries before being transferred to fingerling ponds and eventually moved into larger grow-out ponds, where they are raised to market size, which typicallytakes from 18 months to more than two years. Feed is delivered daily and dissolved oxygen levels are maintained and continuously monitored using paddlewheel aeration and automated oxygen monitors.

The industry has also undergone a significant technological transformation over the past two decades. Farmers increasingly utilize hybrid catfish, which combine the growth performance of channel catfish with the disease resistance and production characteristics of blue catfish. Many farms have adopted more advanced production systems, including split-pond technology (which separates fish-holding areas from water-treatment areas to improve water quality and increase production efficiency) and expanded aeration, allowing producers to raise more fish per acre while improving feed efficiency and overall productivity. These changes have allowed farms to produce more fish with fewer land resources and have helped offset some cost increases. Recent studies comparing aquaculture species and production systems found U.S. catfish operations among the most productive and cost-efficient users of water, labor, energy and capital. Yet despite those gains, the industry has continued to contract, underscoring the magnitude of the economic challenges facing catfish producers.

Production Cost Challenges

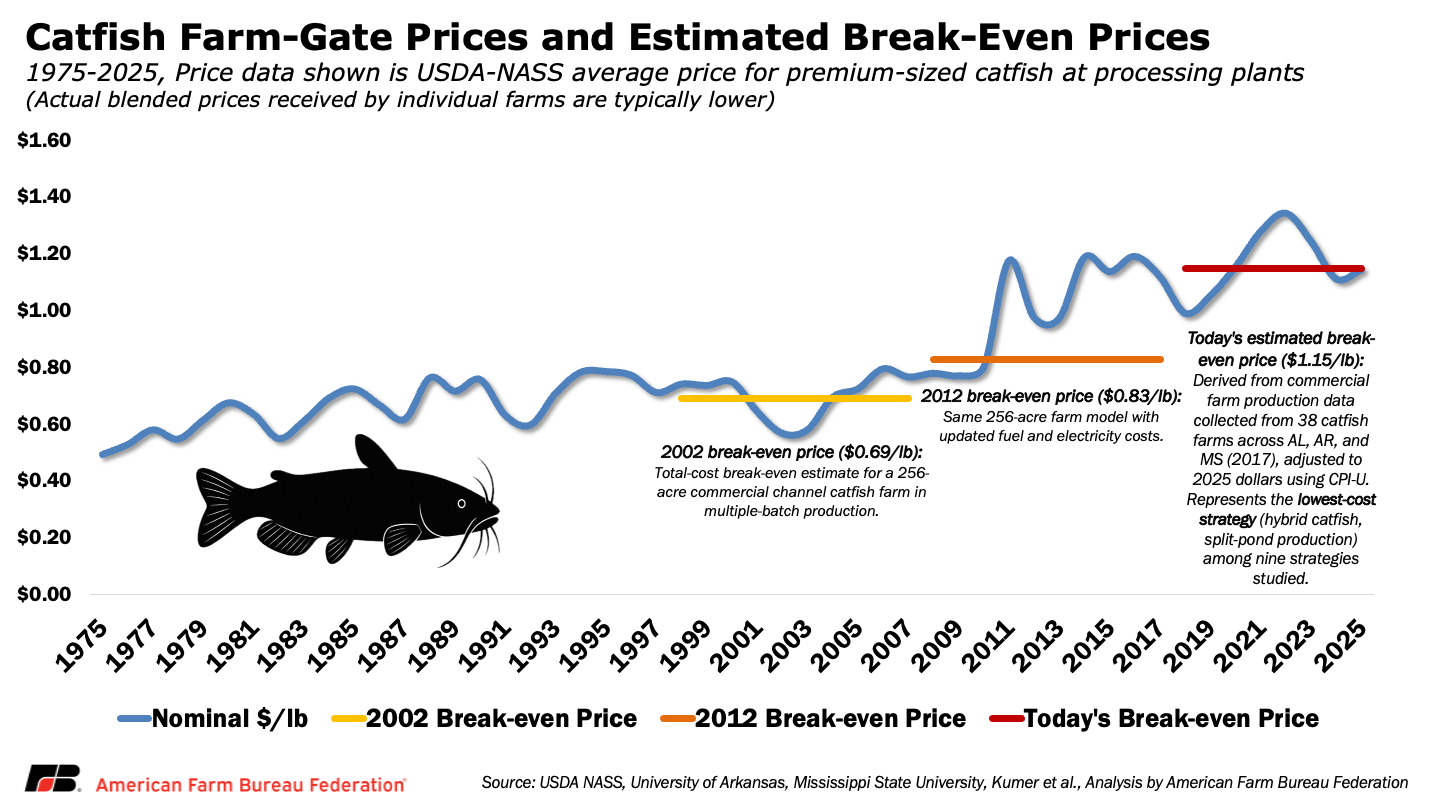

Catfish farming has always been a business won or lost by a few cents per pound of fish sold. What has changed over the past two decades is that those margins have grown thinner even as the cost of maintaining them has grown higher.

Feed remains the industry's dominant expense, typically accounting for 45 to 55% of the total costs on catfish farms. Current spot prices for 28% protein floating feed, a commonly used feed ration for food-fish catfish production, exceed $400 per ton, well below the $550-per-ton peaks reached in early 2023 but still nearly double the roughly $227-per-ton price producers paid in 2002. Because modern intensive production systems commonly apply 10 to 20 tons of feed per acre annually, even relatively modest changes in feed costs can dramatically alter profitability. Research from Mississippi State University found that even the industry's most productive production model, hybrid catfish raised in split-pond systems, becomes unprofitable once feed prices exceed roughly $500 per ton, a threshold the industry surpassed as recently as two years ago.

Fingerling (baby fish) costs have risen sharply as well. Prices for channel catfish fingerlings averaged roughly 1.5 to 1.75 cents per inch in early 2024 and have since climbed to approximately 2.5 cents per inch, an increase of more than 40% in little more than a year. Supply constraints have contributed to those increases. Most domestic catfish hatcheries are located in Mississippi, and disease outbreaks and production challenges at the hatchery level have periodically tightened availability. At the same time, producers have increasingly shifted toward hybrid catfish fingerlings, which offer improved growth performance and disease resistance but carry a higher purchase price.

Labor costs have followed a similar trajectory. Wage rates for farm workers have roughly doubled since the early 2000s, while the industry's transition away from smaller family-labor models toward larger operations employing multiple full-time workers has increased labor costs per farm. Ironically, many of the technologies that have improved productivity also require more active management. Intensive production systems demand more feeding, aeration management, water-quality monitoring and harvesting once ready, increasing the amount of skilled labor needed to operate modern catfish farms efficiently. Harvesting and hauling fish to processors can add roughly 6.5 cents per pound to production costs, creating another significant expense that has steadily increased alongside wages and fuel prices.

Energy costs represent another growing pressure point. Aeration systems account for the majority of electricity use on catfish farms and are essential for maintaining dissolved oxygen levels during warm-weather periods when oxygen demand is highest. While electricity typically represents a smaller share of total production costs than feed or labor, farmers have limited flexibility to reduce aeration without increasing biological risks. As energy markets face continued volatility from broader supply concerns and geopolitical uncertainty, electricity remains an important operating expense that is largely outside a producer's control.

These rising costs have pushed producers toward increasingly intensive production systems. Farms utilizing high-aeration and split-pond technologies can achieve yields exceeding 15,000 to 20,000 pounds per acre, spreading fixed expenses such as land, equipment and depreciation across a larger volume of fish and reducing costs on a per-pound basis. However, the capital investment required to achieve those yields is substantial, and the economics leave little room for error. Elevated interest rates in recent years have further complicated those investments by increasing borrowing costs and delaying infrastructure upgrades on some farms. Research using actual commercial farm data found that traditional low-intensity channel catfish operations producing 4,500 to 5,000 pounds per acre were unprofitable at every farm size evaluated under price conditions common throughout much of the past two decades.

The result is a narrow and increasingly fragile window of profitability. Estimated breakeven costs for a representative commercial catfish farm have risen from roughly 69 cents per pound in 2002 to 83 cents per pound in 2012 and to an estimated $1.15 per pound today, based on inflation-adjusted commercial farm production data collected from operations across Alabama, Arkansas and Mississippi. With weighted-average farm prices currently hovering around $1.17 per pound, many producers are operating at or near breakeven, leaving little cushion to absorb losses from disease, bird predation, adverse weather or further increases in production costs.

Even those figures likely overstate actual returns. The price shown reflects USDA-National Agricultural Statistics Service averages for premium-sized fish, but individual producers receive blended prices based on the size distribution of fish they deliver. Processors pay the highest prices for fish weighing between 1 and 4 pounds, the size range most desirable for retail and foodservice markets. Fish that fall outside that range whether undersized due to poor feed conversion, weather-related setbacks, or oversized because of harvest delays and inventory challenges — receive significantly lower prices. As a result, producers face a steep performance cliff: missing production targets does not simply reduce profits; it lowers both the volume of fish sold and the price received per pound, compressing margins from both sides simultaneously.

Imports Reshaped the Competitive Landscape

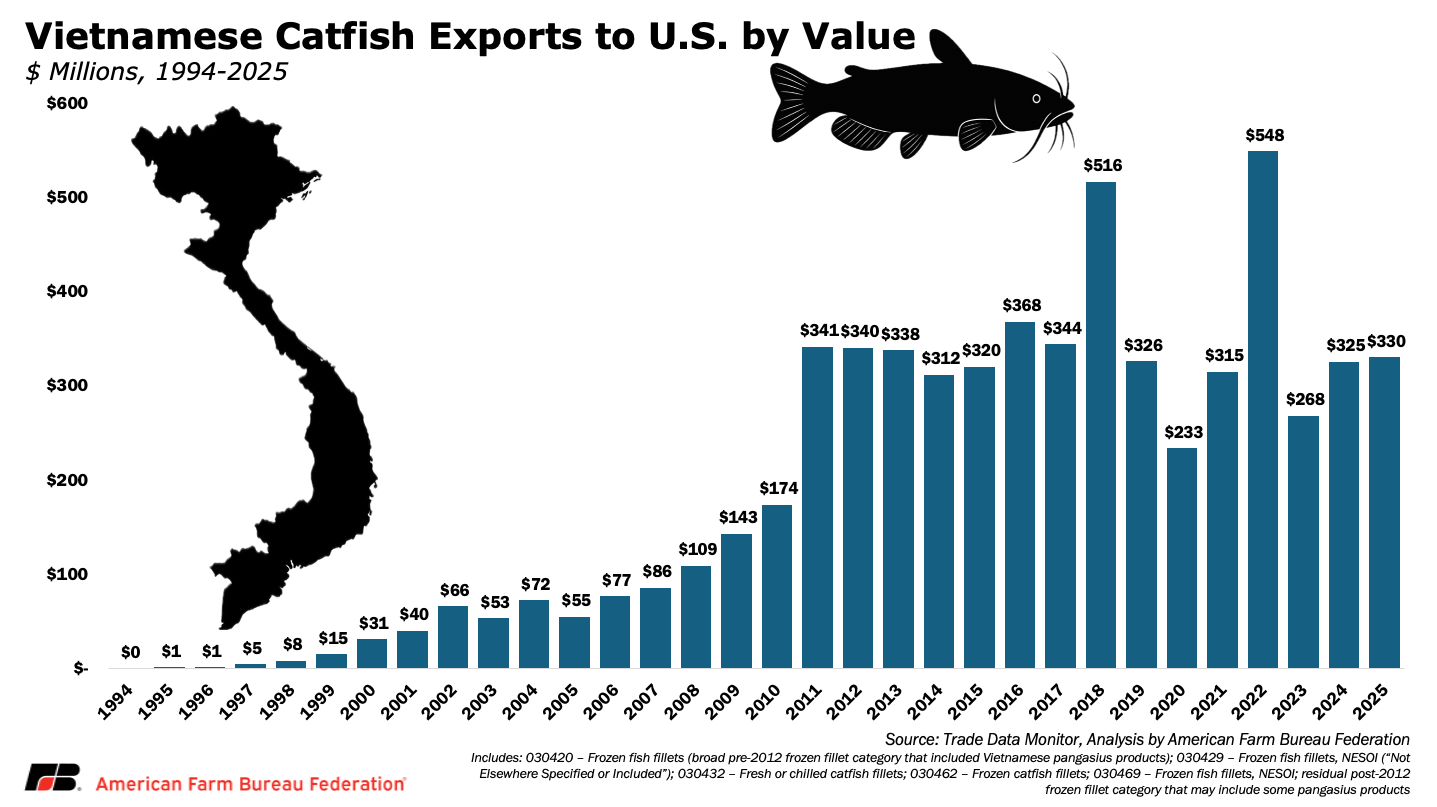

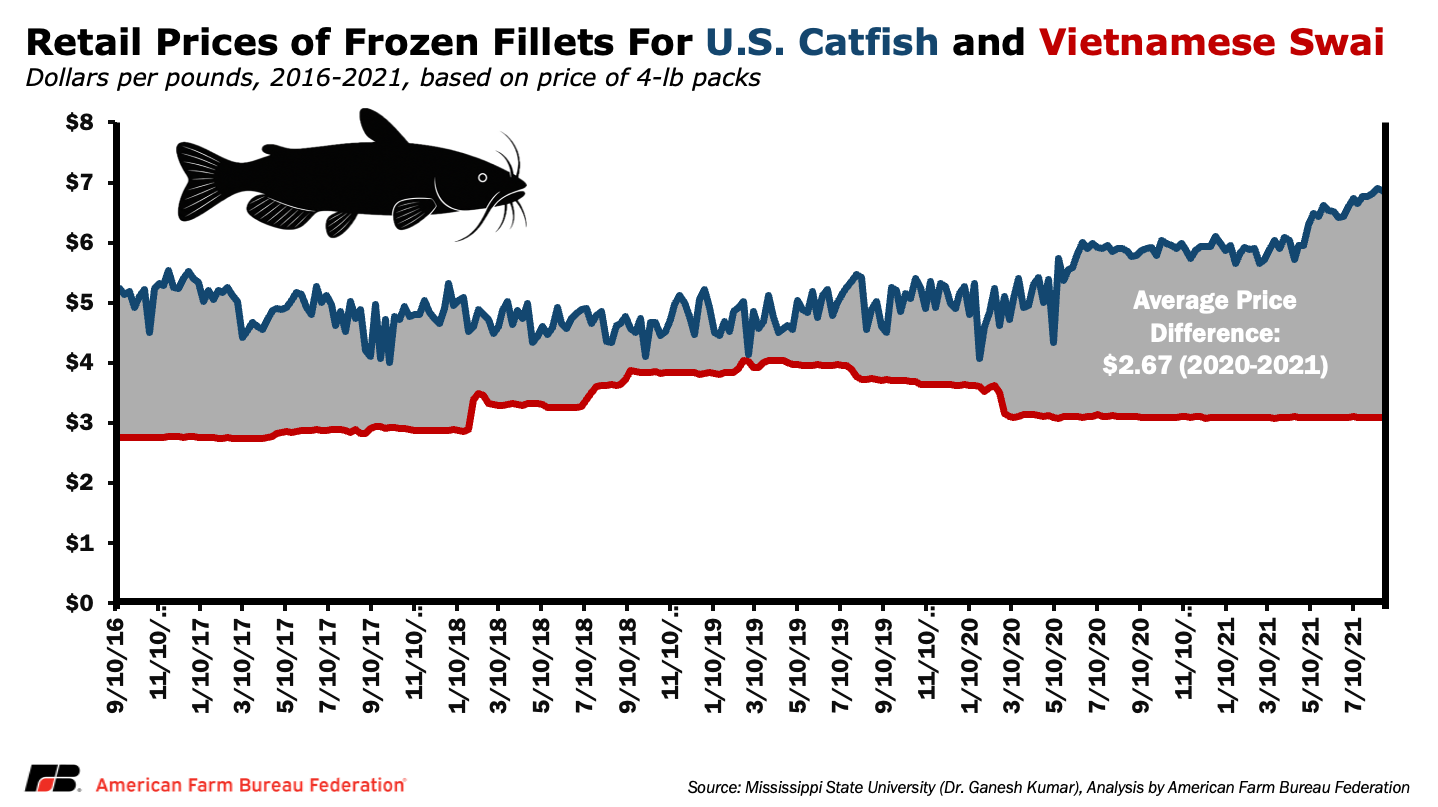

Few forces have altered the U.S. catfish industry more profoundly than the rise of imported Vietnamese pangasius. From virtually no presence in the mid-1990s, Vietnamese catfish exports to the United States grew into a market exceeding $300 million annually by the 2020s. Much of that growth occurred in the frozen fillet segment, where imported pangasius increasingly competed alongside domestically produced catfish, fundamentally changing the competitive environment.

The rapid growth of imports during the late 1990s and early 2000s prompted a series of federal policy responses. Congress restricted the use of the term "catfish" to species within the Ictaluridae family in the 2002 farm bill, requiring imported products to be marketed under names such as basa, tra or swai. In 2003, the United States imposed antidumping duties on certain frozen fish fillets from Vietnam after determining imports were being sold at less than fair value, which the importers are still trying to contest. Additional actions followed, including the establishment of USDA's Siluriformes inspection program, which placed imported catfish products under the same food-safety oversight framework as domestic production.

While those measures altered the regulatory environment, they did not halt import growth. Vietnamese exports continued expanding through the 2000s and 2010s, reaching a record $548 million in 2022 before moderating to approximately $330 million in 2025. At the same time, successive administrative reviews gradually lowered duty rates for many major exporters. Although the antidumping order remains in place, several Vietnamese exporters now face zero dumping margins, reducing the practical trade barriers that existed during earlier years of the dispute.

The competitive challenge is most evident in the retail seafood case, where Vietnamese swai and U.S. catfish products compete directly for consumers. Retail scanner data collected from more than 67,000 stores nationwide found swai products were consistently priced below U.S. catfish products across every region, city and year studied. In 2020-2021, U.S. catfish products averaged $5.82 per pound at retail compared to $3.14 per pound for swai, a difference of more than 46%. Researchers also found the price gap widened for larger package sizes, reinforcing swai's position as a lower-cost alternative in grocery stores.

The persistent price disparity reflects important differences in production systems and cost structures. U.S. catfish producers operate in regulated earthen pond systems that require active management of water quality, oxygen levels and fish waste. Vietnamese pangasius production generally relies on production systems capable of supporting substantially higher stocking densities, while benefiting from lower labor costs and other structural cost advantages. Those differences contribute to lower costs throughout the supply chain and ultimately lower-priced fillets in U.S. markets.

The result is a marketplace in which domestic catfish producers and processors must compete against imported products that frequently reach consumers at substantially lower prices. While U.S. catfish continues to command a premium in many markets based on quality, product differentiation and consumer preference, imported swai has established a significant presence by competing aggressively on price. For many domestic farmers, that competitive pressure remains one of the defining economic challenges facing the industry today.

Bird Predation: When Wildlife Becomes a Production Cost

For catfish farmers already operating on razor-thin margins, fish-eating birds are not simply a nuisance — they are one of the largest uncontrollable costs of doing business. Unlike feed, labor or energy expenses, bird losses arrive without warning, cannot be budgeted with certainty and can quickly erase a year's profit.

Double-crested cormorants are the primary culprit. These migratory diving birds arrive in the Mississippi Delta each fall and winter, concentrating around catfish ponds from October through April at precisely the time when ponds contain the highest densities of fish. A single cormorant consumes roughly one pound of fish per day. When flocks number in the thousands, and concentrations of 8,000 to 10,000 birds at a single farm have been documented, losses accumulate rapidly. American white pelicans, great blue herons and great egrets add further pressure, with pelicans capable of consuming substantially larger fish in a single feeding event.

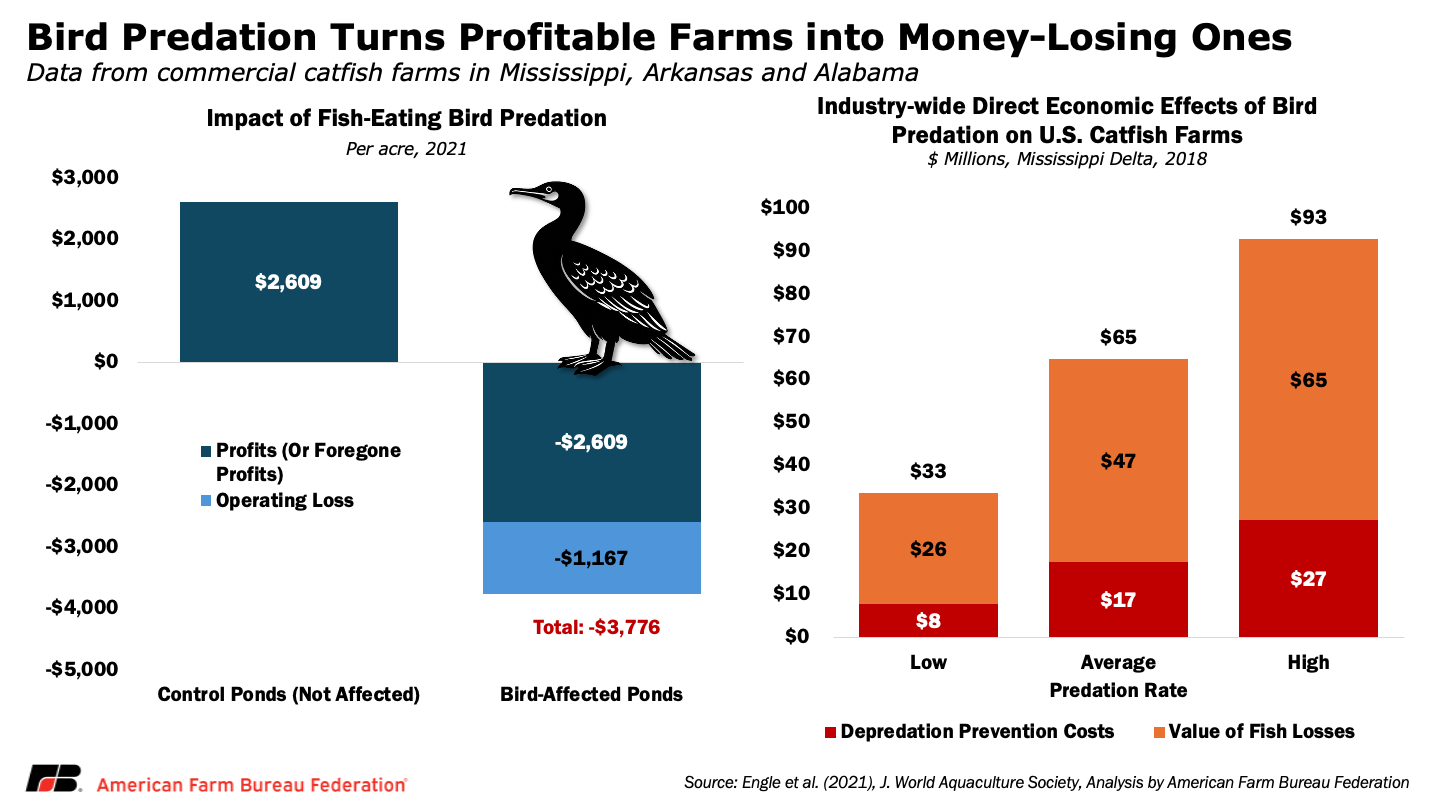

The economic impacts can be staggering. Research from commercial catfish farms unaffected by bird predation generated average profits of approximately $2,600 per acre. On ponds experiencing significant bird predation, however, those profits disappeared and were replaced by operating losses of roughly $1,200 per acre. The result was an overall economic swing of nearly $3,800 per acre attributable to fish-eating birds. In other words, bird predation alone was capable of turning profitable farms into money-losing ones.

Another study in 2019-2020 showed that across the Mississippi Delta, cormorants alone are estimated to consume approximately $47 million or $896 per acre worth of catfish annually. The costs extend well beyond the fish that are consumed. Farmers spend an average of $350/acre, or $18 million annually, to deter birds, making bird control on farms the fifth-largest production cost. These expenses include labor, trucks, fuel, pyrotechnics and ammunition, levee repairs, bird fencings, etc. Collectively, total direct economic losses average roughly $65 million per year and can reach as high as $93 million during periods of elevated predation pressure. What makes these losses particularly frustrating is that the primary predator species are federally protected under the Migratory Bird Treaty Act. Producers can use harassment techniques to disperse birds, but lethal control generally requires federal depredation permits that remain subject to agency approval and timing constraints. The consequences of limited control can be severe. During permit delays between 2016 and 2018, documented fish losses at a Mississippi research facility reduced fish survival by 33% to 95% in affected ponds, generating economic losses estimated between $3,500 and $4,000 per acre.

The broader impact on farm profitability is substantial. Researchers found that removing bird predation from the equation converted roughly one-third of otherwise unprofitable catfish production scenarios into profitable operations.

For years, catfish producers had little federal assistance available to help absorb those losses. Unlike cattle ranchers, who can access the Livestock Indemnity Program when protected predators kill livestock, catfish farmers were largely excluded from comparable disaster assistance programs. That changed with passage of the One Big Beautiful Bill Act, which expanded the Emergency Assistance for Livestock, Honeybees and Farm-Raised Fish Program (ELAP) to explicitly include catfish losses associated with fish-eating birds. Eligible producers may now receive assistance for deterrence expenses, fish losses attributable to predation, and certain disease losses linked to bird activity, with a minimum payment rate of $600 per acre applied to eligible production acreage.

The expansion of ELAP represents one of the most significant policy victories for the catfish industry in recent years, but it does not eliminate the underlying challenge. Farmers must still bear the burden of annual deterrence efforts, navigate federal permitting requirements and manage a threat that returns with each migration season. Even with federal assistance now available, bird predation remains one of the most persistent and costly biological risks facing U.S. catfish farms.

Disease and Weather: Risks Beyond a Producer's Control

Disease and weather remain two of the most significant biological uncertainties facing U.S. catfish producers. Unlike feed or labor expenses, these threats can quickly erase months of investment after producers have already incurred the costs of fingerlings, feed and daily management.

Edwardsiellosis, one of the industry's most common bacterial diseases, accounts for roughly 31% of reported catfish disease cases and is estimated to cost the industry between $15.5 million and $45.9 million annually. At the farm level, losses can reduce profitability by approximately $1,400 to $5,400 per acre through a combination of fish mortality, slower growth, poorer feed conversion and treatment expenses. More broadly, a seven-year survey of Alabama catfish farms found disease-related losses averaged $1,651 per hectare ($668/acre)annually and reduced state industry revenues by nearly 10%.

Extreme weather events often amplify those losses. Hot summer temperatures reduce dissolved oxygen levels, increasing fish stress and raising the risk of disease outbreaks and fish kills. Flooding can damage levees and allow fish to escape, while drought conditionsconcentrate fish in smaller volumes of water, concentrate birds, and increase predation pressure on remaining ponds. Similarly, a sudden drop in temperature and prolonged icing events would make catfish susceptible to winter fungus and mortalities. Research has found that disease losses are often closely tied to weather patterns, with bacterial outbreaks increasing during periods of extreme heat and other diseases becoming more prevalent during prolonged rainfall events.

For producers already operating near breakeven, disease and weather are more than biological challenges, they are financial uncertainties that can quickly turn a productive growing season into a money-losing one.

Industry Contraction Reshapes the Catfish Supply Chain

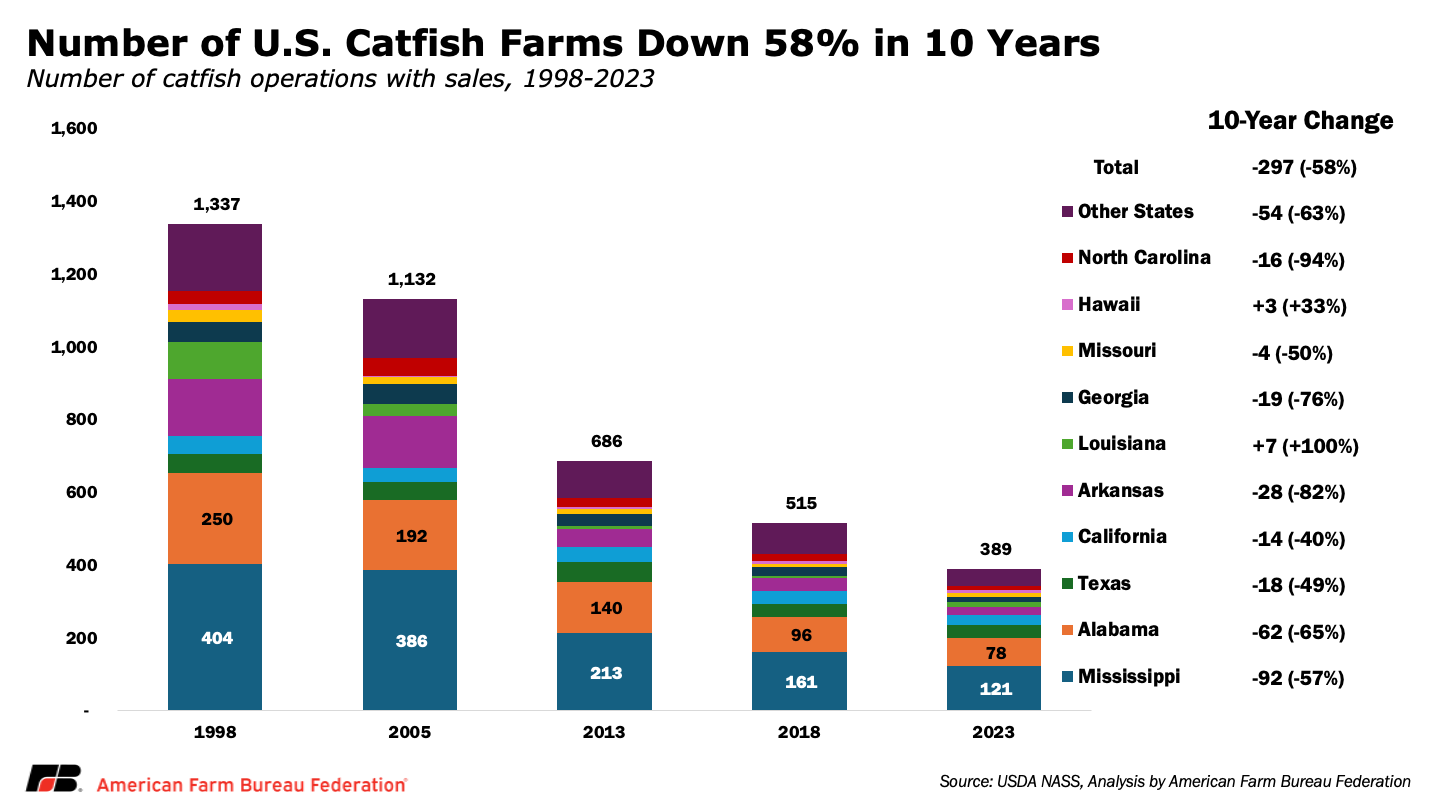

The challenges facing U.S. catfish producers extend beyond individual farm profitability. Over the past two decades, rising production costs, disease pressures, bird predation, and growing import competition have contributed to a steady contraction of the industry. At its peak in the early 2000s, U.S. catfish farmers operated nearly 200,000 acres of production ponds. Today, fewer than 50,000 acres remain, while the number of farms has fallen from more than 1,300 operations in 1998 to just 389 in 2023.

That decline has reshaped the broader catfish supply chain. Processing facilities, hatcheries, feed suppliers and transportation networks all depend on sufficient production volume to remain economically viable. As production has consolidated geographically, supporting infrastructure has consolidated as well. Arkansas, once a major catfish-producing state with more than 30,000 acres of ponds, no longer has a major commercial catfish processor.

While the remaining farms are generally larger and more productive than those of previous generations, a smaller industry means fewer marketing options, greater dependence on a limited number of buyers and suppliers, and less economic activity flowing through the rural communities that depend on catfish production. The industry's future depends not only on the profitability of individual farms, but on maintaining the broader network of processors, hatcheries, feed mills and service providers that make domestic catfish production possible.

Conclusion

U.S. catfish producers have spent decades adapting to a changing marketplace. Advances in genetics, aeration, feeding programs and production technology have allowed farms to become more productive and efficient than ever before. Yet those gains have been increasingly offset by rising input costs, persistent disease pressure, fish-eating bird predation, weather-related uncertainties, and growing competition from imported seafood.

The result is an industry that remains an important source of domestic seafood production and economic activity across the rural South, but one operating with little margin for error. As farm numbers, production acreage and supporting infrastructure continue to decline, the long-term competitiveness of U.S. catfish production will depend not only on producers' ability to innovate but also on policies and market conditions that allow those investments to generate sustainable returns.

Top Issues

VIEW ALL