Balancing Data Center Growth with American Agriculture

Autumn Lankford Higgins

Director, Government Affairs

Bernt Nelson

Economist

Key Takeaways

- Farmland conversion is generally permanent, making site selection and land-use policy critical for long-term agricultural viability.

- Data centers create both economic opportunities and resource pressures, particularly around land, water and energy.

- Data centers represent multi-billion-dollar investments that can bring jobs, tax revenue and infrastructure improvements to rural communities.

- Balanced policy and local engagement are essential to ensure rural communities benefit without undermining agriculture.

Overview

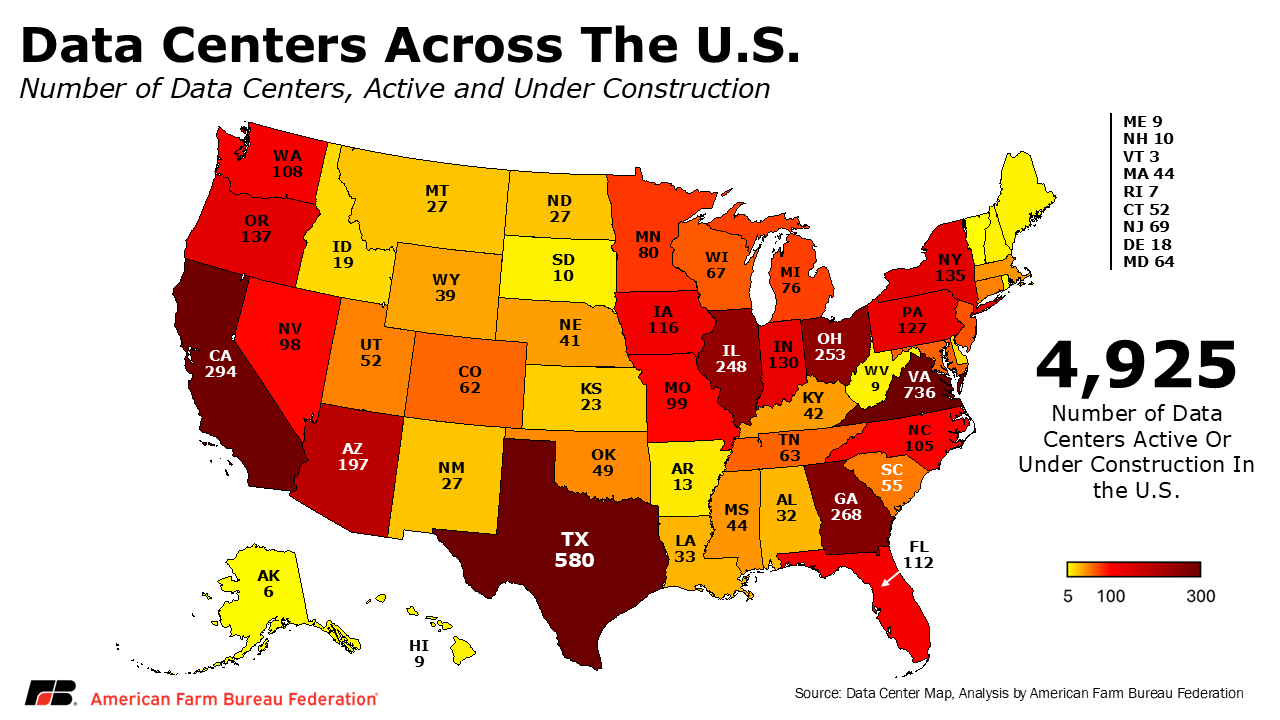

Demand for data centers – large, secure facilities that house computers and servers used to store, process and manage vast amounts of digital data – is accelerating as cloud computing, artificial intelligence and other digital services expand across the United States. These facilities form the backbone of the modern economy, powering the internet and enabling the applications and services relied upon by businesses, governments and everyday consumers. According to Data Center Map and analysis by AFBF, it is estimated, that there are 4,925 active or under construction data centers across the U.S. These facilities, often requiring hundreds of megawatts of power are increasingly sited in rural areas where land availability, energy access and proximity to transmission infrastructure make development feasible.

The scale of investment is significant. Construction costs range from $9 million–$15 million per megawatt, meaning a typical 250-megawatt facility can cost between $2.3 billion and $3.8 billion, while the price tag for larger campuses can reach tens of billions of dollars. These projects are not just industrial developments; they are long-term infrastructure commitments that shape local economies for decades.

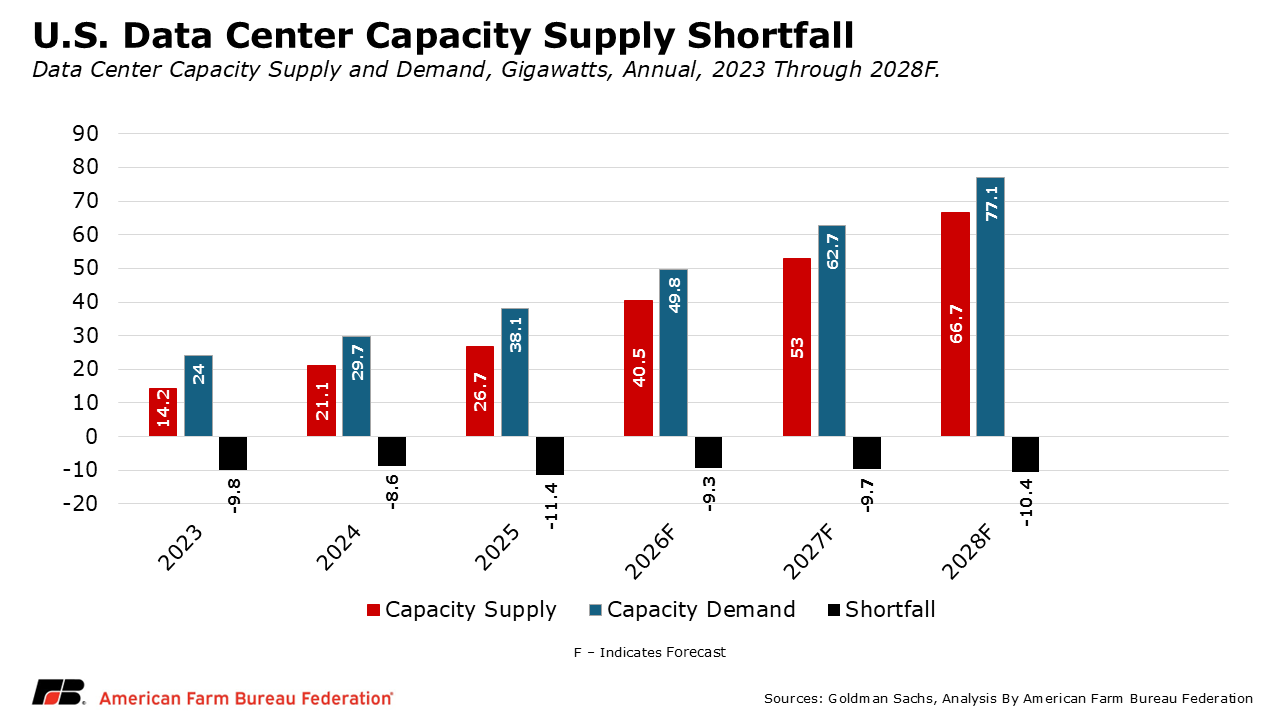

Demand for data centers, driven by the growth of artificial intelligence (AI), high performance computing and cloud service adoption, is continuing to outpace U.S. supply capacity. According to a study by Goldman Sachs, in 2025 U.S. demand for data center capacity outpaced supply by about 11.4 gigawatts or about 43%. The study forecasts the capacity supply to increase by 150%, from 26.7 gigawatts in 2025 to 66.7 gigawatts by 2028. Even with this rapid growth, 2028 demand for capacity is forecast to outpace capacity supply by 10.4 gigawatts or about 16%.

For agriculture, this trend presents both opportunity and risk. Farms and ranches depend on land, water and energy, the same inputs data centers require at scale. At the same time, agriculture increasingly depends on the digital infrastructure data centers provide.

The central question is how to integrate them into rural America without compromising agricultural productivity and community stability?

Why It Matters to Agriculture

Farmland is the foundation of agricultural production and a generational asset for farm families. Once converted to industrial use, it is rarely returned to production. In regions experiencing rapid development, the cumulative loss of prime farmland is a growing concern.

At the same time, modern agriculture is deeply connected to the digital economy. Precision agriculture, cloud-based management tools, and real-time data analytics all rely on robust data infrastructure.

This creates a dual reality:

- Agriculture depends on data centers for innovation and efficiency.

- Data centers are increasingly competing with agriculture for access to land, water and energy.

Land Values and Site Selection

Site selection for data centers is about more than just finding available land. Land for data centers is treated as critical infrastructure that is selected based on several qualities or characteristics. Some key factors involved with site selection are the proximity to stable, high-capacity power grids, access to major fiber routes for high-speed data transfer, risk for natural disasters, climate conditions that could reduce cooling costs, and regulatory or tax incentives.

Virginia and Texas are the two leading U.S. states for data center development, with 706 and 546 data centers active or under construction, respectively. Virginia, particularly northern Virginia, is home to the world’s largest data center market due to elite fiber connectivity, tax incentives and affordable, reliable power. Texas is in second place for U.S. data center markets due to its low energy costs, abundant land, regulatory environment, independent power grid, and tax incentives. In Texas and Virginia for example, qualifying data centers are exempt from state and local sales tax on hardware, software, cooling systems and emergency generators. Electricity and fuel used by qualifying Texas data centers are also exempt from sales tax.

Developers often seek agricultural land as it is often already cleared, graded and laid out in large contiguous tracts, lowering upfront site development costs and shortening project timelines relative to more complex greenfield or urban sites.

Zoning flexibility in rural areas, where agricultural land can be rezoned for industrial use with relatively few barriers, is another factor driving data center site selection. While this flexibility can support economic development, it also introduces a form of land use competition that extends beyond individual sales. As more parcels are rezoned or considered for rezoning, farmland begins to carry speculative value tied to future development potential, increasing both purchase and rental costs for active farmers. Over time, this dynamic can shift local land markets away from agricultural production and toward development-driven pricing, even in areas where little land has been converted. In these high-demand regions, prices for land can reach millions of dollars per acre.

The sale of agricultural land for data center development can also affect land values elsewhere in the state or across the country. Through the use of section 1031 of the tax code, landowners may defer capital gains tax from the exchange of a like-kind asset. This allows, for example, a farmer to sell their farmland for data center development and then to reinvest in farmland elsewhere in the state or country, potentially driving up the value of farmland.

Resource and Infrastructure Pressures

Energy Demand

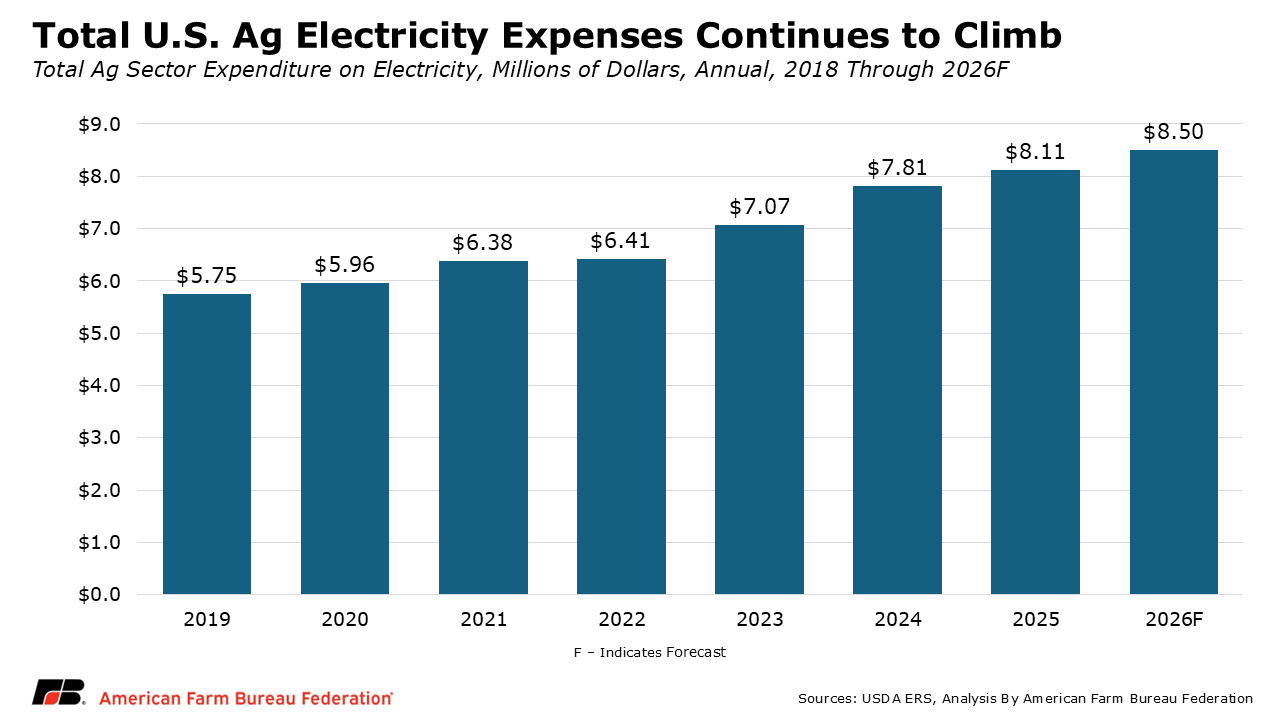

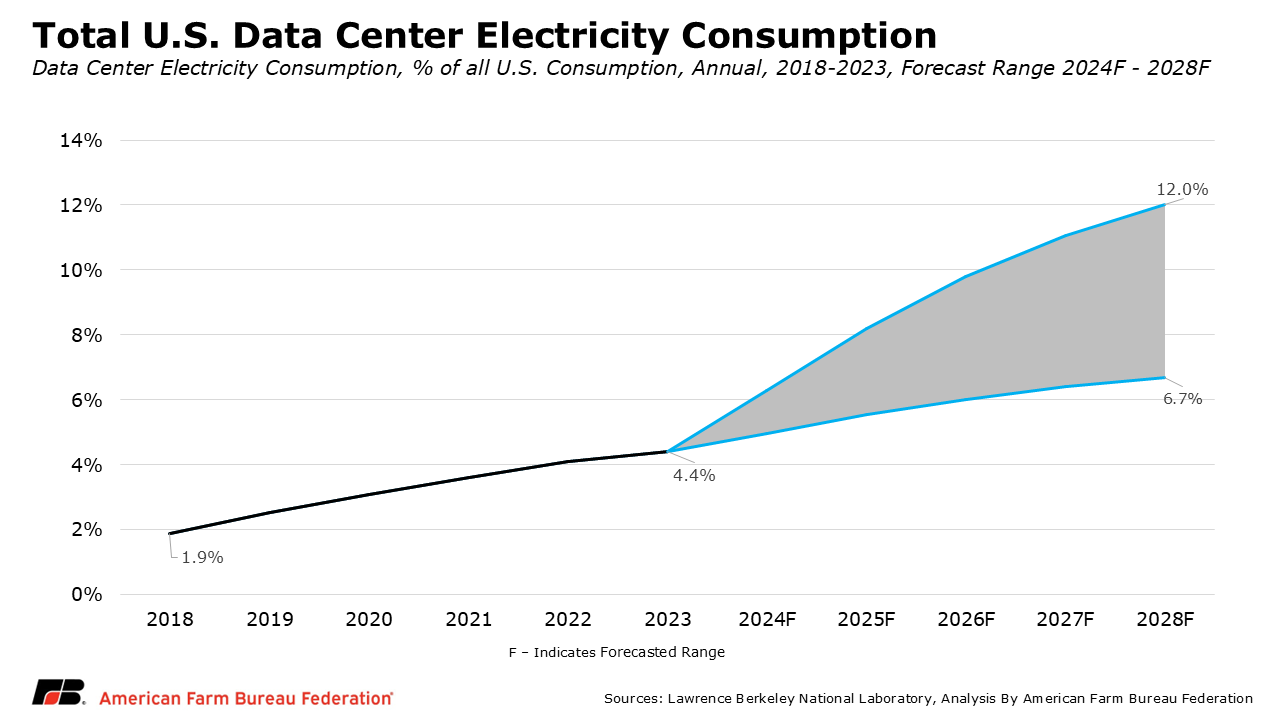

Electricity expenditures on U.S. farms have risen sharply in recent years and are forecast to increase by 48%, or $2.8 billion, from $5.75 billion in 2019 to $8.5 billion in 2026, according to USDA’s Economic Research Service. Growing electricity demand from data centers, electrification and digital infrastructure is adding pressure to an already aging grid. The Department of Energy estimates data centers used about 4.4% of U.S. electricity in 2023, a share projected to rise to between 6.7% and 12% by 2028.

Total electricity demand is expected to increase over the coming years, requiring significant investment in transmission, substations and generation capacity. These costs are often recovered through higher electricity rates, though utilities are increasingly using tools such as large load tariffs to help manage infrastructure expansion and limit impacts on other customers. Ensuring grid investments expand capacity without shifting disproportionate costs onto farm operations will be important for maintaining the competitiveness of U.S. agriculture.

Water Use

Cooling systems for data centers can require substantial amounts of water, which raises concerns in agricultural regions where water supplies are often limited. Increased demand can lead to competition for scarce water resources and create risks for local watersheds. While emerging technologies, including more water efficient cooling systems, such as closed loop cooling, offer ways to reduce these impacts, transparency around water use and accountability measures remain essential to maintaining trust and protecting shared resources.

Rural Economic Development: Promise and Tradeoffs

Data centers can offer meaningful economic opportunities for rural communities, including increased local tax revenue, job creation and the potential revitalization of areas facing economic decline. However, the economic benefits are not guaranteed and can vary widely depending on location and planning. Without careful consideration, communities may also face unintended consequences, including rising costs of living and strain on existing infrastructure.

Key Policy Considerations

The American Farm Bureau Federation (AFBF) supports responsible data center development in rural areas that delivers meaningful economic benefits while respecting local resources and private property rights. State and local policymakers play a critical role in balancing growth with long-term land preservation by recognizing farmland as a strategic economic asset, protecting against unnecessary conversion of highly productive agricultural land, and prioritizing brownfields or previously developed sites whenever possible.

Because data center projects often move quickly and can outpace local planning processes, strong local governance is essential. Transparent zoning and permitting decisions, along with early and consistent engagement with landowners and other stakeholders, help ensure that communities have a voice in development decisions and that outcomes reflect local priorities.

AFBF also emphasizes the importance of responsible resource management. Data centers should be located and operated in ways that protect agricultural water resources, including clear disclosure of water use and the adoption of water‑efficient technologies such as closed‑loop cooling systems. Policy frameworks should address shared demands on critical resources by encouraging continued innovation in water efficiency, supporting energy infrastructure that benefits both agriculture and data center operations, and promoting solutions that strengthen the resilience of rural communities overall.

Bottom Line

Rural communities can support both agriculture and responsible data center development, with farmers, ranchers and landowners ultimately deciding how their private property is used. Smart site selection, local engagement, and long-term planning can ensure rural America remains both a hub for agricultural production and a partner in responsible technological growth.

With thoughtful policy, strategic siting and strong local engagement, rural America can serve as both a global leader in agricultural production, and a critical partner in the digital economy.

Top Issues

VIEW ALL