Egg Prices Ease, Farmers Prepare for Spring Migration

TOPICS

Egg Prices/HPAI

Bernt Nelson

Economist

Key Takeaways

- Egg prices have fallen sharply as production recovers after HPAI-driven volatility.

- HPAI detections rose sharply in January and February 2026 with 15.5 million birds affected in those months. While this is substantial, it is 56% fewer birds than at the same time in 2025. Detections slowed in March, reflecting progress in managing the outbreak.

- USDA is urging farmers to be vigilant with biosecurity. As the spring migration gets underway, HPAI is being detected in both wild birds and domestic poultry flocks across the country, increasing the risk of exposure.

- USDA biosecurity assessments provide poultry and egg farmers with resources to protect flocks and safeguard food supply.

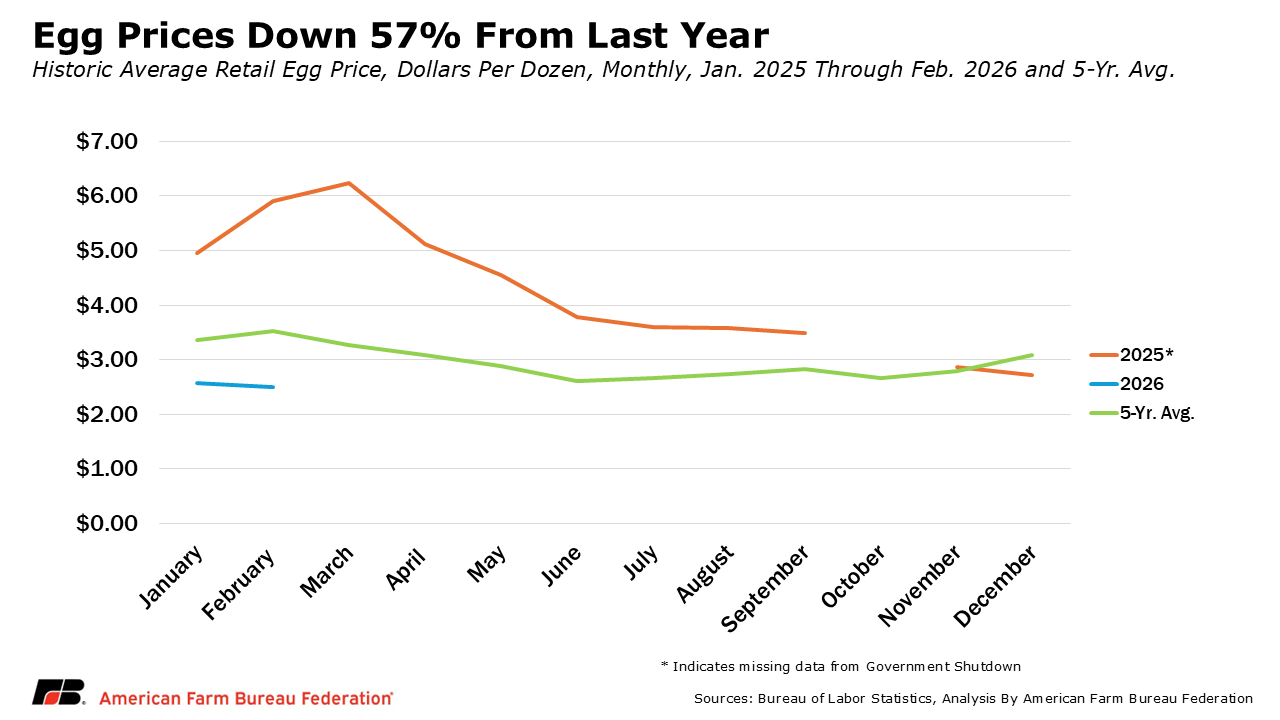

After a period of sharp volatility driven by Highly Pathogenic Avian Influenza (HPAI), egg markets are beginning to stabilize with prices easing by 57% from last year’s highs as production recovers.

That progress comes as the industry enters the spring migration period; a time of year typically associated with increased disease pressure from HPAI. However, stronger biosecurity practices, ongoing flock rebuilding and a more coordinated USDA response are helping support continued stability in both supply and markets.

HPAI Detections Moderate After Early-Year Rise

HPAI detections increased sharply in January and February with 15.5 million birds affected in those months. While this is substantial, it is 56% fewer birds than at the same time in 2025. Detections have begun to moderate in recent weeks, with overall impacts tracking below last year’s pace. So far in 2026, 20.62 million birds have been affected by HPAI, down about 11% from 23.2 million birds affected at this time last year.

HPAI detections were front loaded at the beginning of the year with about 4 million birds affected in January followed by a sharp increase to more than 11 million birds in February. Detections in March have come down with 5.2 million birds affected.

While this is far greater than 128,000 in March of 2023 and 31,000 in March 2024 it is 54% less than February of this year. With spring migration about to begin, USDA is urging farmers to be vigilant with biosecurity to help mitigate the risk of flock exposure.

While HPAI continues to circulate in wild bird populations, impacts remain concentrated in poultry and broader livestock exposure has been more limited. There has not been an HPAI detection in dairy cattle in 2026, with the last detection occurring on Dec. 13, 2025. This marks the effectiveness of USDA’s “Secure Our Herds” program and the national milk testing strategy.

Taken together, the early rise in detections followed by moderation, along with limited spillover into other livestock sectors, points to a more contained and manageable phase of the outbreak.

Egg Production Rebuild Drives Sharp Price Relief

Egg Layers

Spring demand for eggs is picking up, with tens of millions expected to be consumed over the coming weeks as multiple holiday seasons get underway. This seasonal increase in demand comes at a time when egg markets are showing clear signs of improvement.

According to data from the Bureau of Labor Statistics (BLS), the national average retail price for a dozen eggs was $2.50 in February, down 57% from a near-record $5.89 per dozen in February 2025 and 29% below the five-year average of $3.52. After last year’s price surge driven by HPAI-related losses in laying flocks, current price levels reflect a more balanced supply.

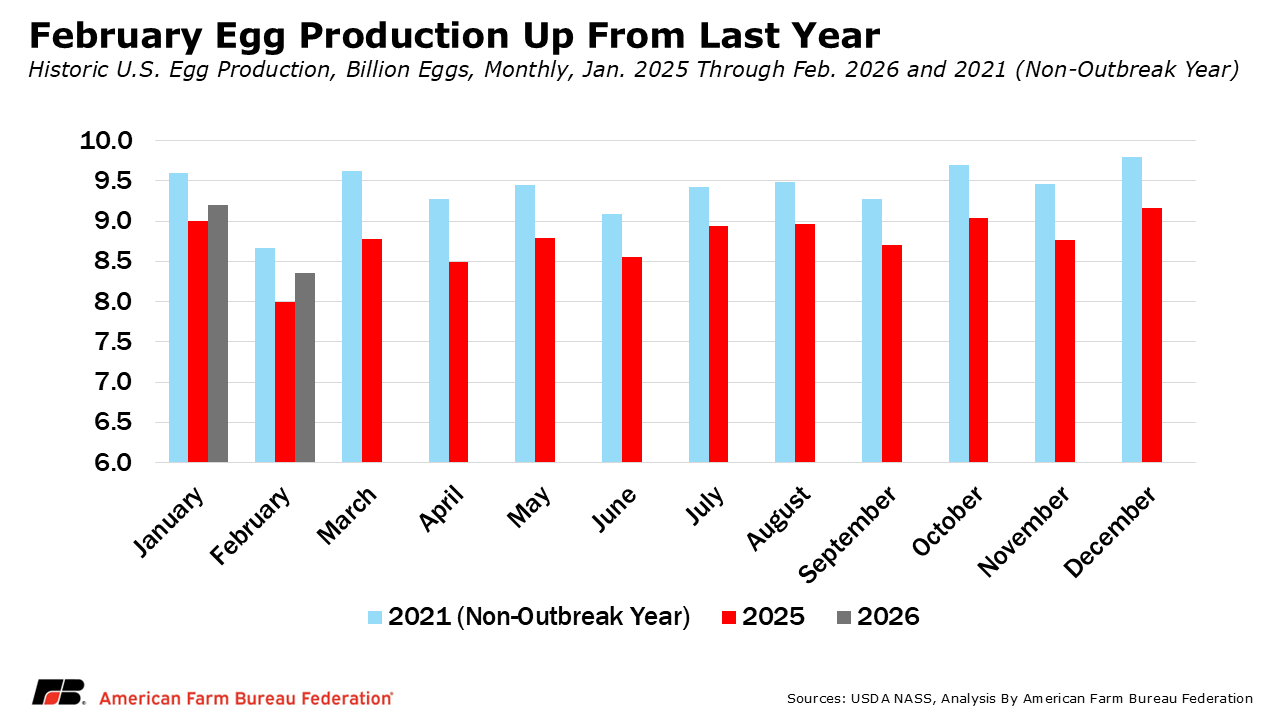

Production data supports that shift. According to USDA-National Agricultural Statistics Service’s (NASS) latest monthly Chicken and Eggs report, U.S. egg production totaled 8.36 billion eggs in February, up 5% from 2025 but still well below pre-outbreak production levels. This includes 7.17 billion table eggs, up about 7.4% from the same time last year.

Egg-type chicks and pullets remain key to maintaining and rebuilding supply. Egg-type chicks hatched in February were estimated at 55.8 million, up 2%, while eggs in incubators totaled 58.5 million, up 4% from a year ago. Placement of egg-type pullets — young chickens that will grow into future egg layers — reached 250,000, up 6% from 2025. These strong replacement numbers point to continued recovery from HPAI-related disruptions over the past several years and position the sector to respond to any future increases in disease pressure.

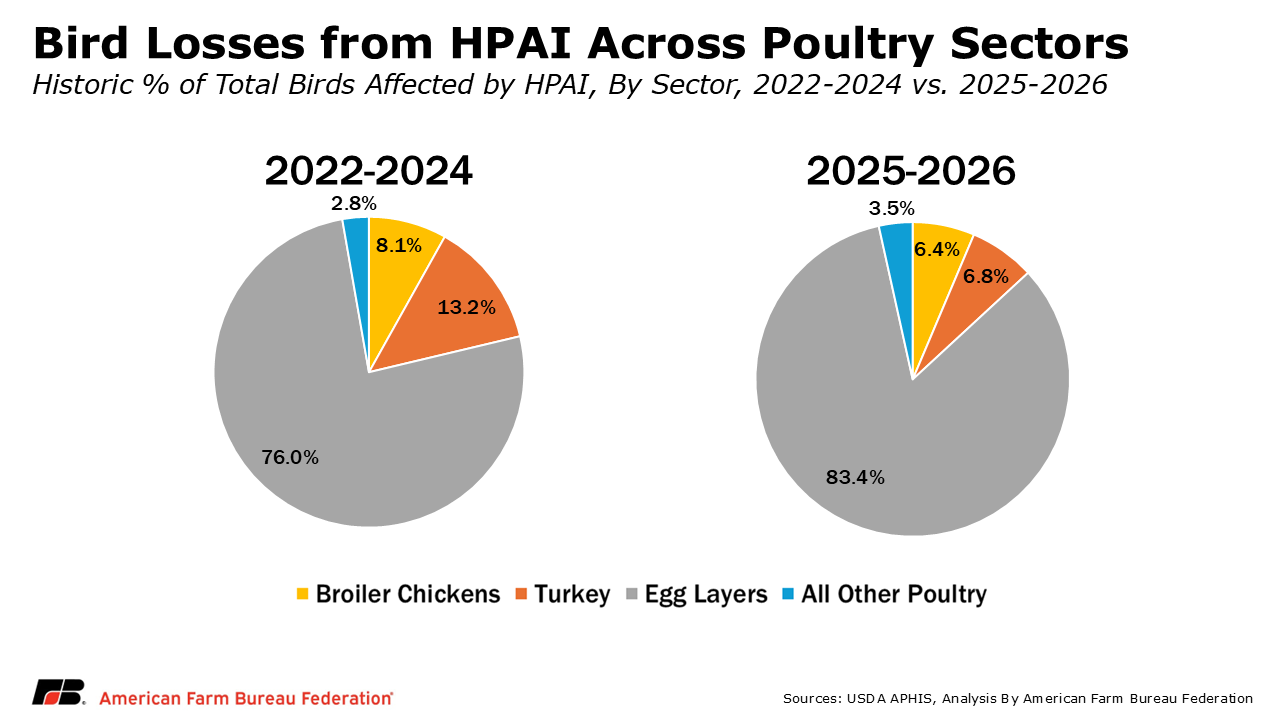

Egg layers account for nearly 80% of all birds affected by HPAI, underscoring why rebuilding laying flocks is central to stabilizing the broader poultry market. The combination of improving production and strong replacement activity is helping restore supply and ease price pressures, even as the industry moves into a season of higher demand.

Broiler Chickens

Broiler chickens (used for meat production) continue to be minimally affectedrelative to other poultry sectors. So far in 2026, 1.28 million broiler chickens have been affected. The percentage of broiler chickens affected out of all birds affected has fallen from 8.1% from 2022-2024, to 6.4% in 2025-2026.

Production indicators remain strong and point to continued stability in supply. According to NASS’ Chickens and Eggs report, broiler-type chicks hatched in February totaled 798 million, up 2% from 2025. Eggs in incubators were estimated at 763 million on March 1, also up 2% from a year ago. Placement of broiler-type pullets reached 9.06 million, up 10% from 2025, further strengthening the pipeline for future production.

These strong supply indicators have supported higher production expectations. USDA’s latest World Agricultural Supply and Demand Estimates (WASDE) report forecasts 2026 broiler production at 48.7 billion pounds, up 1.4% (or approximately 694 million pounds) from 2025.

Consistent production and effective disease management have helped maintain stable prices through the outbreak. According to BLS data, the national retail composite price for chicken in February 2026 was $2.39 per pound, down 2% from last year and just 1 cent above the five-year average. This stability highlights the sector’s ability to maintain steady supply even amid ongoing HPAI challenges.

Turkey

Turkey production is continuing to adjust to recent disease pressures while maintaining overall supply. So far in 2026, less than 1 million turkeys have been affected, accounting for just 5% of all birds affected. The share of turkeys affected has declined in recent years, down from 13.2% during 2022–2024 to 6.8% since the start of 2025, indicating a reduced concentration of impacts within the sector.

USDA’s March WASDE report estimates total turkey production will be 4.93 billion pounds. While this is up about 1.7% from 2025, this estimate is 35 million pounds lower than the February estimate and reflects fewer eggs in incubators. Turkey eggs in incubators on March 1 were estimated to be 24.4 million. Up about 1% from 2025, but down 6% from February’s estimate of 25.8 million eggs.

Addressed in a previous Market Intel, Avian Metapneumovirus (AMPV) is also widespread and causing major disruptions in the turkey industry. Fewer eggs in incubators leaves the turkey supply chain more vulnerable to both HPAI and AMPV. As a result, USDA’s March WASDE report is forecasting the national average farm price for an 8–16-pound hen turkey in 2026 will be $1.56 per pound, up 14% from 2025 and up 66% from 2024.

Even with these pressures, the turkey sector continues to adjust production and maintain supply, reflecting ongoing adaptation to evolving disease conditions.

Biosecurity and Preparedness

Spring and fall are high-risk seasons for HPAI due to the seasonal movement of migratory birds. With spring migration beginning, USDA-Animal and Plant Health Inspection Service’s (APHIS) wild bird surveillance program has indicated a high viral load of HPAI in wild birds in all four major migratory flyways (Atlantic, Central, Mississippi and Pacific).

Farmers are entering this period with stronger tools and more experience managing the disease. Biosecurity remains the most effective line of defense, and adoption of enhanced practices has expanded significantly across the poultry sector. USDA offers two types of biosecurity assessments for commercial poultry farms that are designed to provide actionable strategies to help protect flocks from HPAI. Wildlife biosecurity assessments involve an on-farm assessment conducted by APHIS Wildlife Services that identify how wildlife could spread HPAI to a flock, while domestic biosecurity assessments focus on structural and operational biosecurity plans and practices.

A total of 2,980 assessments have been completed as of March 25 These efforts are helping reduce exposure pathways and strengthen the industry’s ability to manage HPAI alongside ongoing production.

Conclusion

Early 2026 data show an industry navigating HPAI with growing resilience but continued vulnerability. Poultry losses remain significant, though March brought a welcome slowdown in detections, and strong biosecurity recommendations from USDA reflect the heightened risk posed by spring migration. Dairy cattle remain unaffected so far this year, underscoring the effectiveness of targeted prevention programs.

Across the poultry sector, production indicators point to rebuilding and strengthening supply chains. Egg and broiler operations are supported by solid hatchery and pullet numbers, helping stabilize output and ease price pressures after last year’s volatility. Turkeys, however, continue to face tighter supplies due to both HPAI and AMPV, leading to reduced hatchery inventories and higher projected prices.

With viral loads high in wild birds across all major flyways, biosecurity remains the single most important defense. Nearly 3,000 completed USDA assessments highlight how seriously producers are taking these risks. As the year progresses, maintaining rigorous biosecurity and strong replacement flocks will be critical to supporting market stability, protecting animal health and ensuring a reliable food supply.

Top Issues

VIEW ALL