Low Australian Sheep Supply Could Provide Opportunity for U.S. Lamb Market

AFBF Staff

photo credit: Alabama Farmers Federation, Used with Permission

Australia supplies the U.S. with over 100 million pounds of lamb per year, representing about 75 percent of total imports on a carcass weight basis. To Australia, the U.S. is the largest lamb market. In the last 12 months, the U.S. has imported more than 10,000 metric tons more than the second largest importer, China.

The Australian sheep industry is undergoing significant flock rebuilding, retaining many lambs to build the breeding herd. Stronger wool prices have also incentivized producers to retain Merino wether and wether lambs to produce income from wool. Collectively these two factors have led to smaller lamb supplies. According to Meat and Lamb Australia, the 2017 lamb slaughter forecast is down 6 percent from 2016. Australian demand for lamb is also quite strong and in the past hasn’t shied away from higher prices. Domestic consumption is estimated at 46 percent of production.

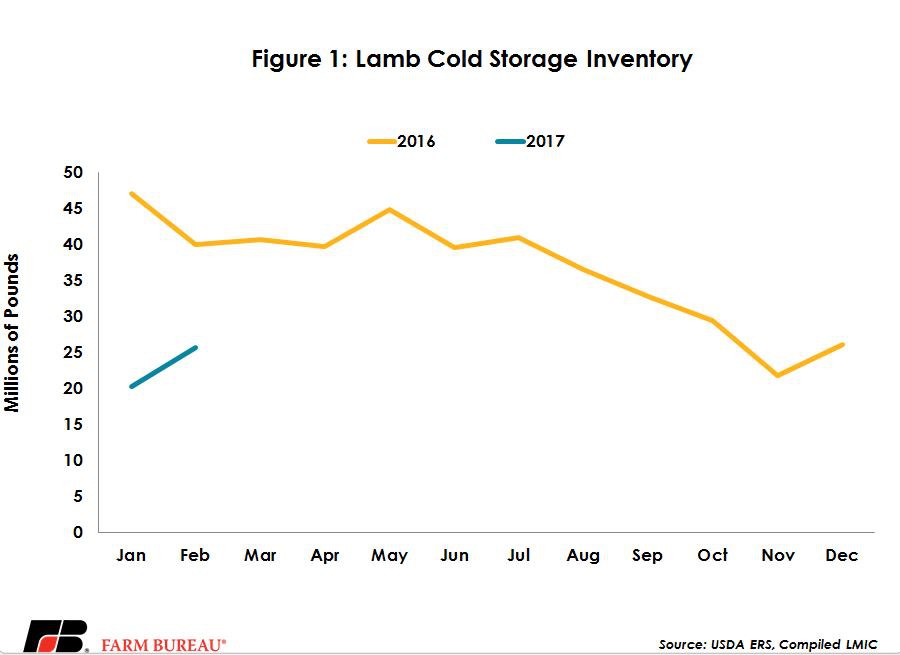

The U.S. has had high levels of lamb in cold storage for the last couple of years, however, 2016 saw a significant draw down of those levels. The latest data (February 2017) showed cold storage was down 36 percent from last year at this time. Figure 1 shows cold storage levels for the last 14 months. The U.S. imports over 50 percent of domestic disappearance annually, most of which is from Australia. Further pointing to contracting supply, sheep inventory figures noted domestic lamb supplies are also expected to be down slightly this year.

So far, Australian exports of lamb to the U.S. are down 6 percent through March 2017, according to Meat and Livestock Australia. But, timing as with many agricultural products is critical. The latest update from Meat and Livestock Australia implied the tightest lamb supplies will likely be in April-September, which also tends to be the lower slaughter months for U.S. lambs as well. Prices are expected to increase in 2017 for lambs, but upside potential will likely be limited. Although Australia does ship the most lamb to the U.S., New Zealand lamb also plays a big role in U.S. markets, accounting for 25 percent of imports. Expectations for higher prices hinge on U.S. consumption over the summer quarters and if there is a deficit in supply because of lower imports.

Top Issues

VIEW ALL