U.S. Crawfish Farmers Face Strong Headwinds

Daniel Munch

Economist

Key Takeaways

- Crawfish prices have stagnated while costs rise: Crawfish prices remain largely unchanged from a decade ago, while production costs have climbed roughly 40% since 2014, pushing returns into negative territory.

- Labor disruptions threaten market access: The loss of H-2B labor in 2026 could eliminate processing capacity that typically absorbs about 40% of the crop, driving up to $299.5 million in total economic losses.

- Imports are undercutting domestic production: Following the removal of antidumping duties, import prices fell from $5.53 to $2.56 per pound, intensifying competition and pushing domestic prices below breakeven levels.

- Environmental and biological pressures are mounting: Drought and heat reduced yields by more than 37% in 2024, while bird depredation (up to 1 pound per bird per day) and invasive species continue to erode production and increase costs.

Few agricultural sectors capture the identity of a state in the way crawfish defines Louisiana. From roadside boils to restaurant menus far beyond the Gulf Coast, crawfish is both an economic engine and a cultural institution. But behind that visibility, the industry is navigating a convergence of pressures - rising production costs, intensifying import competition, a critical labor supply disruption and increasing weather volatility - that are testing the financial resilience of producers across the region.

Background: How Crawfish Production Works

Crawfish production in the United States is overwhelmingly concentrated in Louisiana, though smaller production occurs in other states, including Texas, and is centered on integrated rice–crawfish rotational systems. Farmers plant rice in the spring and reflood those same fields in the fall, creating ideal habitat for crawfish, which feed on decomposing rice stubble and natural vegetation. Adult crawfish burrow during the summer, reproduce underground and emerge when fields are flooded, allowing harvests to begin in late fall and continue through spring. The dominance of this system reflects both strong demand growth and the need for a reliable rotational crop in a region where options are limited. While soybeans are sometimes used in rotation with rice, yields are often constrained by difficult growing conditions and weather risk, leaving returns inconsistent. As a result, crawfish has become a critical diversification tool, helping stabilize farm income in years when rice profitability is marginal. This system has expanded rapidly, with acreage and production increasing roughly 200% over the past two decades, reaching nearly 386,000 acres in 2025 and helping push total industry value above $640 million.

Harvesting is highly labor-intensive, relying on baited traps that are checked daily across flooded ponds. Larger crawfish are sold live in fresh markets, while smaller crawfish are processed into tail meat and whole-boiled products, providing a critical outlet for a significant share of production. This dual-market structure is essential to maintaining price stability, particularly later in the season when volumes increase and size distribution shifts. At the same time, production is highly sensitive to weather and water conditions, with farms requiring 2.5 to 4 acre-feet of water per acre and yields closely tied to rainfall and temperature patterns. These characteristics make the industry both efficient and uniquely vulnerable, as disruptions to labor, processing capacity or environmental conditions can quickly ripple through the entire system.

Production Cost Challenges

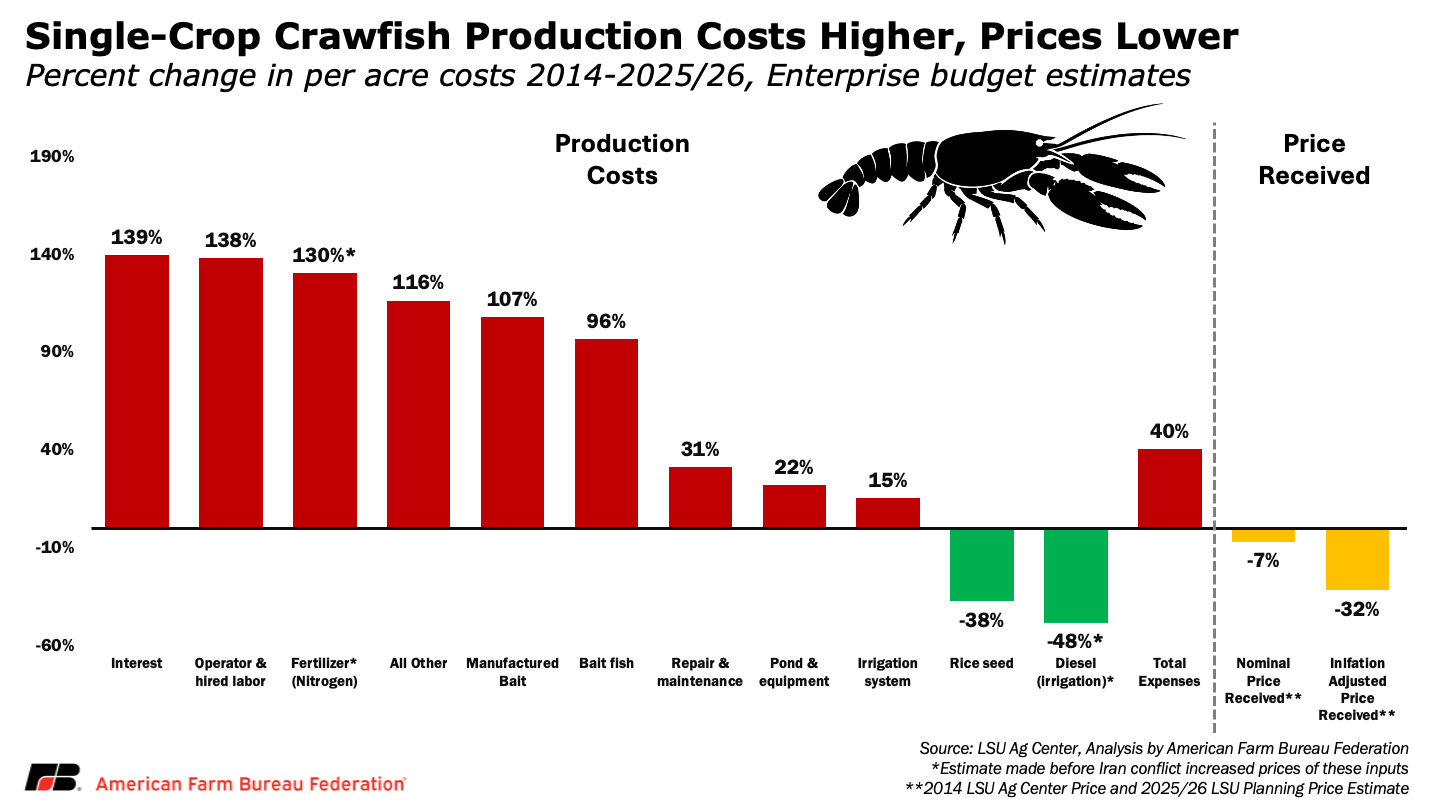

Louisiana crawfish producers entered the 2025/26 season facing production costs that have risen much faster than the prices they receive. According to Louisiana State University AgCenter enterprise budget estimates, per-acre total specified costs for single-crop crawfish production have risen approximately 40% since 2014 in nominal terms (from $727 per acre to $1,018 per acre), while the planning price used in the 2025/26 budget of $1.25 per pound is virtually unchanged from a decade ago in nominal terms and represents a real decline of approximately 32% when adjusted for inflation.

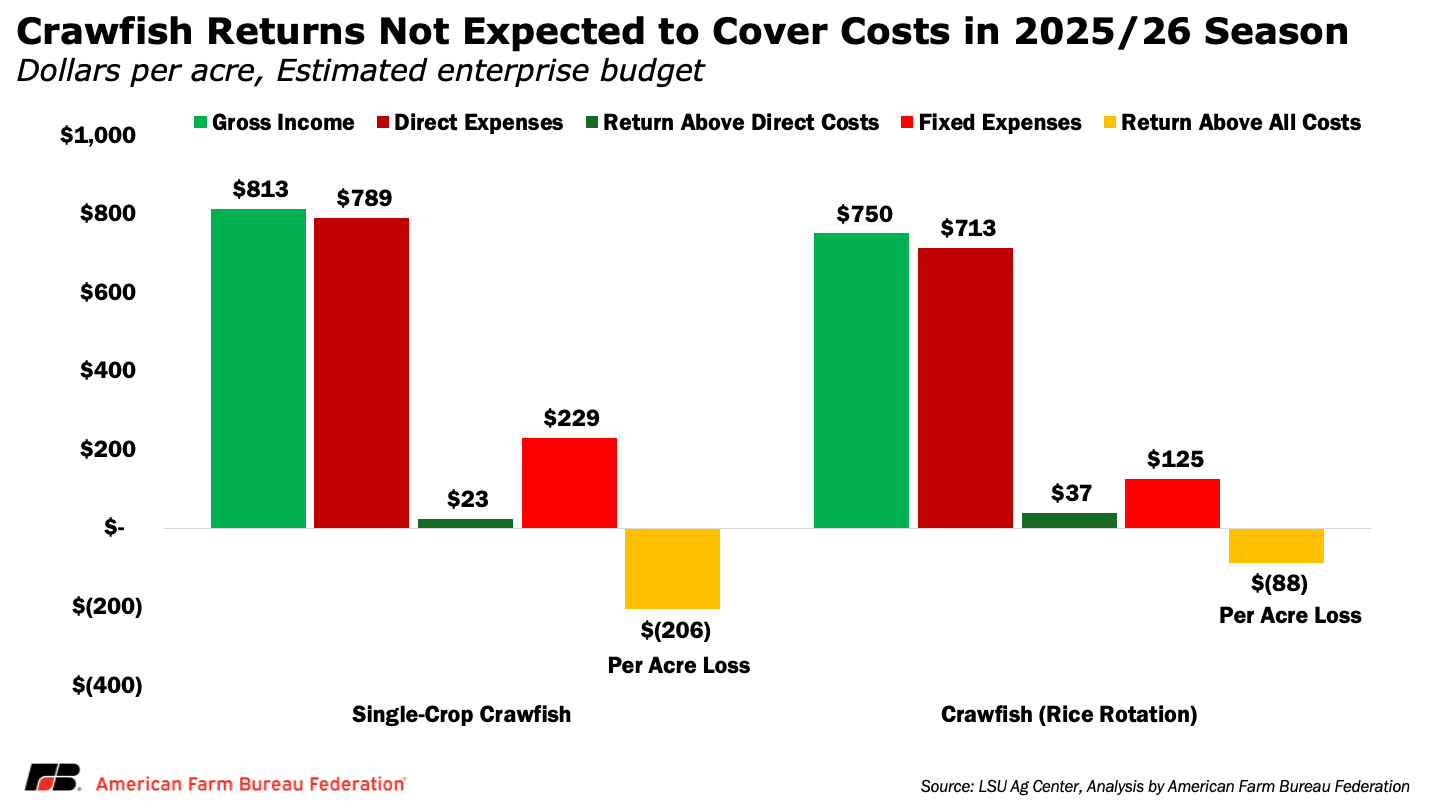

The result is a significant and widening cost-price gap. At a yield of 650 pounds per acre and a price of $1.25 per pound, single-crop crawfish producers face estimated returns of only $23 per acre above direct expenses and a loss of approximately $206 per acre once fixed costs are included. Producers in rice-crawfish rotation systems fare somewhat better due to diversified revenue, but are still projected to lose approximately $88 per acre on the crawfish-only portion of the enterprise after fixed costs.

The input cost increases driving this squeeze are concentrated in categories that have risen well above general inflation. Interest on operating capital increased an estimated 139% between the 2014 and 2025/26 budgets, reflecting the jump from historically low borrowing rates to the 8.25% short-term rate used in current planning estimates. Operator and hired labor costs rose approximately 138%, driven by wage rate increases. Nitrogen fertilizer costs climbed an estimated 130% — a figure that was calculated before the conflict in Iran further pressured fertilizer input markets and may now understate the true increase. Both manufactured crawfish bait and fish bait prices have roughly doubled. Traps, a capital item not separately tracked in the 2014 budget, now account for $30 per acre in annual replacement costs under the assumption that one-fifth of the trap inventory is replaced each year.

Partial offsets exist. Rice seed costs declined due to a change in assumed seeding rates, and irrigation diesel costs had been lower than 2014 levels earlier in the year. However, like with fertilizer, recent volatility in energy markets tied to geopolitical tensions has begun to push fuel costs higher, limiting those savings relative to broader cost increases. Ongoing drought conditions have also increased irrigation demand, driving higher pumping frequency and raising diesel and energy use above typical levels.

It is important to note that LSU AgCenter enterprise budgets are engineering-based estimates, not surveys of actual producer costs, and reflect a standardized operation under current input prices. While individual producers may see different cost structures, the broad increases across labor, capital, bait and fertilizer reflect real pressures contributing to deeply negative margins industrywide.

Applying estimated per-acre losses to Louisiana's approximately 367,761 crawfish acres suggests statewide losses could plausibly range from roughly $32 million to $76 million depending on the mix of production systems. These estimates also do not capture additional losses from depredation, invasive species, disease or extreme weather, all of which can further reduce yields and deepen financial strain.

Trade and Import Competition

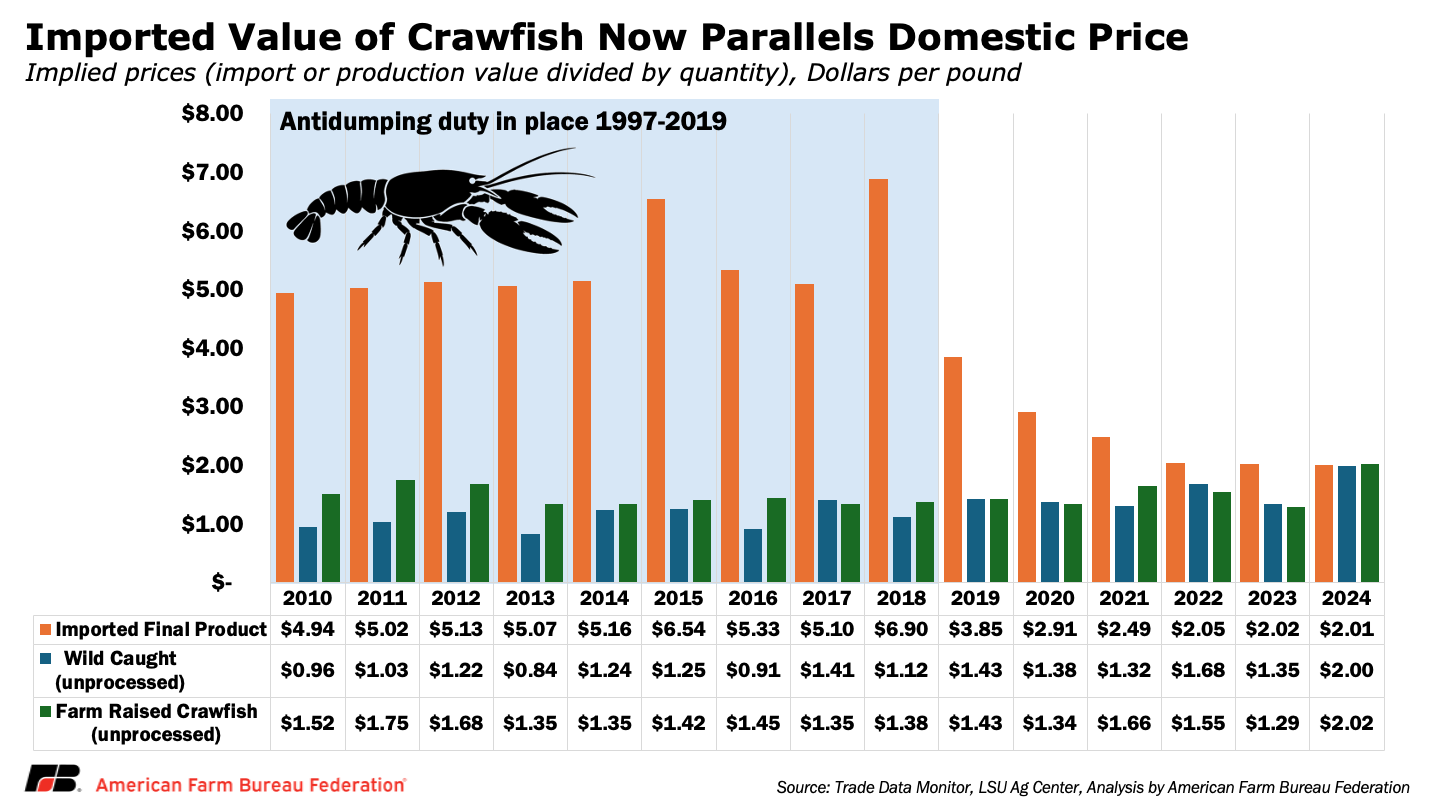

The crawfish industry has operated in the shadow of import competition for nearly three decades. In the late 1990s, the U.S. International Trade Commission confirmed that imported crawfish tail meat, primarily from China, was being sold in the U.S. market at less-than-fair value, injuring domestic producers. Antidumping duties exceeding 200% were imposed in 1997 and repeatedly upheld through subsequent administrative reviews, as evidence of continued injury to domestic producers remained consistent even as U.S. production grew.

Those duties were not renewed in 2019, not because dumping had stopped, but because the cost of maintaining participation in the annual administrative reviews became too burdensome for the relatively small domestic industry. The consequences were immediate and lasting. Average landed import prices fell from roughly $5.53 per pound during the final years of the duty period to approximately $2.56 per pound from 2019 through 2024 — prices approaching what crawfish farmers and processors receive for unprocessed live product and well below the estimated $9 or more per-pound cost of producing domestic crawfish tail meat.

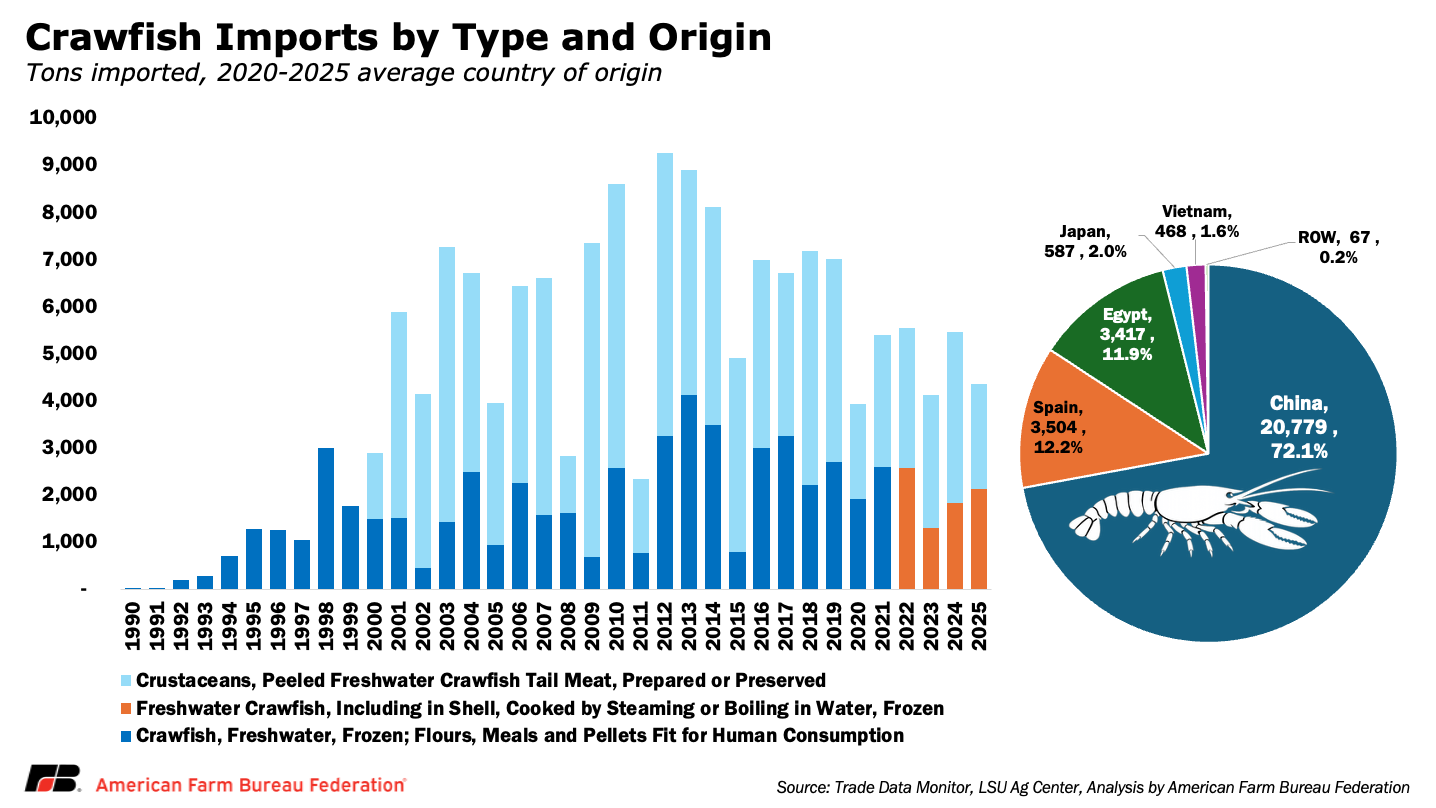

Import volumes and product composition have also shifted in ways that expand competitive pressure beyond the traditional tail meat market. Frozen whole-boiled crawfish, a product form that now accounts for nearly half of all crawfish imports, has opened competition in channels that were previously dominated by domestic processors. Between 2020 and 2025, China accounted for approximately 72% of total U.S. crawfish imports by volume, followed by Spain and Egypt at 12% each, Japan at 2% and Vietnam at 1.6%.

For domestic producers, the downstream consequences are direct and compounding. Processors unable to compete with artificially low-priced imports have been forced to either limit purchases from farmers or push prices paid below breakeven levels.

More broadly, the influx of underpriced imports, driven by structural excess capacity in foreign aquaculture systems, has suppressed domestic price signals, displaced production and eroded the economic viability of small, family-run crawfish operations. Without renewed trade enforcement or structural policy intervention, the risk is that domestic processors continue to lose market share to foreign competitors in ways that prove difficult to reverse.

The H-2B Labor Situation

If rising costs and suppressed prices represent a slow-building structural challenge, the collapse of H-2B visa access for crawfish processors in 2026 represents an acute, season-defining crisis. Crawfish processing, the peeling and packaging of tail meat and whole-boiled products, depends almost entirely on seasonal foreign labor through the H-2B visa program (which allows employers to hire temporary nonagricultural workers from approved countries).

For the 2026 season, changes to supplemental visa allocations resulted in more than 75% of returning worker applications being denied. These changes were implemented during a period of administrative disruption, including two Department of Homeland Security shutdowns, and culminated in a joint DHS–Department of Labor rule issued Jan. 30, 2026. Under that rule, agencies limited consideration for supplemental visas to applications with start dates after Jan. 1, 2026.

Because crawfish processors typically require labor beginning in the fourth quarter of the prior year, most applications fell outside that window and were excluded from consideration altogether. As a result, the majority of the industry’s processing labor requests were effectively denied, with limited clarity from agencies on the rationale behind the decision.

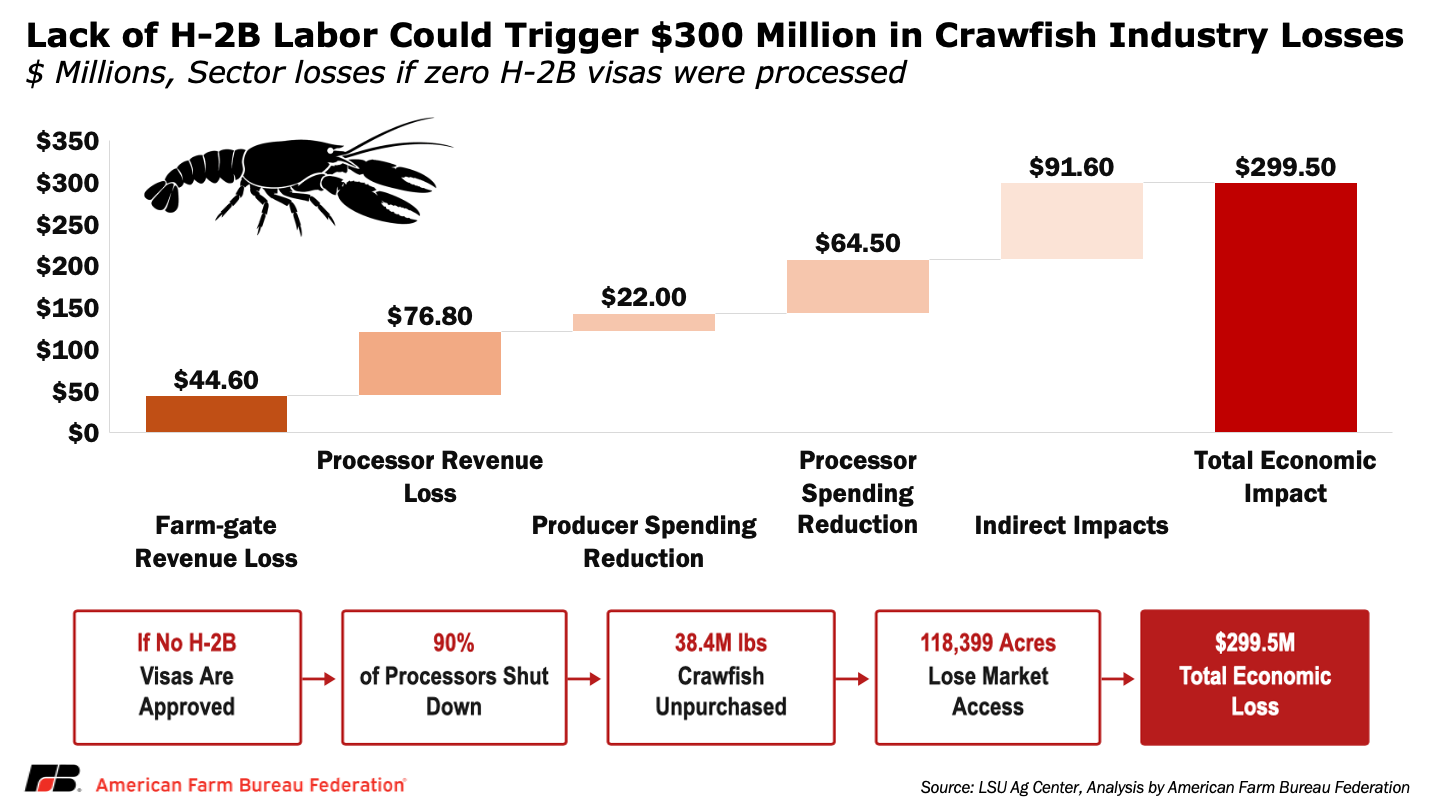

Without that labor, processors cannot operate peeling lines, drastically reducing the processing market for the 2026 season and restricting purchases to live crawfish. This is a critical disruption. Processing typically absorbs around 40% of the total crop, largely smaller crawfish that cannot be sold live. In 2025, processors purchased about 91 million pounds statewide, with 38.4 million pounds processed. The loss of that outlet would translate to an estimated $44.6 million in direct farm-gate losses, as product that would normally be processed goes unsold.

At the processor level, the inability to produce roughly 4.4 million pounds of tail meat and 6.4 million pounds of whole-boiled product eliminates an additional $76.8 million in revenue, $56 million from tail meat and $20.8 million from whole-boiled products, bringing total direct revenue losses to about $121 million. The impacts extend further. LSU AgCenter analysis shows approximately 118,399 acres would lack a viable market during the April–July peak, leading producers to cease harvesting and cut input spending. That reduction, combined with an estimated $64.5 million decline in processor spending, brings total direct losses to roughly $208 million. These impacts are already being felt in real time, as rising input costs and reduced market access continue to compress margins at the farm level.

Including indirect multiplier effects ($91.6 million), total economic losses are estimated at $299.5 million statewide, impacting transportation, retail, feed supply, packaging and local service sectors. Beyond economics, reduced harvesting leads to overcrowded ponds, stunted growth and lower-quality crawfish, while excess supply pressures live prices. Longer term, the loss of domestic processing capacity risks ceding market share to imports, potentially extending the disruption beyond the 2026 season.

Weather, Depredation and Invasive Species

Beyond structural economic pressures, crawfish producers face persistent biological and environmental risks that compound yield losses and raise costs in ways not fully captured in enterprise budgets. Weather remains the most powerful external variable. Because the life cycle is tightly tied to seasonal temperature and precipitation, deviations can have outsized impacts. Heat and drought are especially damaging, reducing dissolved oxygen, slowing growth and lowering survival, while extreme summer heat can weaken or eliminate brood stock before the season begins. The 2023 drought and heat event illustrates this risk, cutting farm-raised yields by more than 37% in 2024 and contributing to nearly $140 million in losses. Freeze events, such as the February 2021 winter storm, can disrupt harvests and damage infrastructure, though they have tended to cause short-term slowdowns rather than the season-long biological impacts associated with heat extremes.

Wildlife and ecological pressures add further strain. Bird depredation is a persistent but under-quantified loss, as shallow ponds attract large populations of migratory birds. Key species can consume 0.3 to more than 1 pound per bird per day, with double-crested cormorants averaging about 1 pound daily, while additional losses occur from injury and stress to crawfish not consumed. Control efforts can cost up to $100,000 annually, with effectiveness declining over time, and federal protections under the Migratory Bird Treaty Act limiting management options.

Invasive species are also emerging as a growing threat. Apple snails damage rice forage and clog traps, increasing labor costs, while rice delphacids (capable of transmitting disease) have reduced rice yields by up to 50% in nearby regions, raising concerns for Louisiana’s dual-crop systems. Chemical controls are limited, as some treatments risk harming crawfish. Flooding events further complicate production by displacing crawfish, introducing predatory fish and disrupting water management. Together, these pressures represent a steady and often unpredictable drain on yields and margins that extends beyond what standard cost models capture.

An Industry Without a Safety Net

Despite its economic importance, the crawfish industry operates with far less federal support than most major agricultural sectors, a gap that is increasingly consequential under current conditions. Crawfish producers are excluded from the $11 billion Farmer Bridge Assistance Program (FBA), which provides support to traditional row crops. While an additional $1 billion has been proposed for specialty crops and sugar crops, eligibility does not include crawfish producers.

The primary program is the Emergency Assistance for Livestock, Honeybees and Farm-Raised Fish (ELAP), which has been expanded in recent years to include crawfish. Prior to 2021, only farm-raised game and bait fish were eligible under ELAP. Following the February 2021 winter storm, USDA extended the program to food-fish aquaculture species, including crawfish, allowing producers to apply for indemnity payments for eligible weather-related losses. In 2024, USDA made a further update to specifically cover crawfish losses from excessive heat, directly addressing the type of summer drought damage that devastated the 2024 season. These expansions represent meaningful progress and reflect genuine responsiveness to the industry’s needs.

However, drought-related losses remain only partially addressed under current rules. While ELAP recognizes drought impacts in other sectors, payments for farm-raised fish are generally tied to documented mortality from qualifying events. Because crawfish are classified under the broader “farm-raised fish” category, the program does not fully align with the unique rice–crawfish production cycle, where drought can significantly reduce production without causing immediate, verifiable death losses.

As a result, ELAP functions primarily as an event-based disaster program and does not extend to broader market or cost-related pressures such as rising input costs, import competition or labor constraints. This structure leaves producers more exposed to year-to-year variability, particularly when multiple challenges occur simultaneously.

Conclusion

The challenges facing the crawfish industry are not the result of a single shock, but the convergence of multiple pressures hitting at once: rising costs, suppressed prices, labor shortages, import competition and environmental risk. Each of these factors alone might be manageable. Together, they are eroding margins, disrupting markets and testing the financial viability of an industry that has grown rapidly but without the policy support structure afforded to most other U.S. commodities.

Without targeted policy attention, the risk is not just short-term loss, but longer-term contraction. The loss of processing capacity, continued import pressure and lack of risk management tools threaten to reduce production, shift market share overseas and weaken the rice–crawfish production systems that underpin much of Louisiana’s rural economy. Ensuring the industry’s stability will require a more complete approach, one that recognizes crawfish as both an economic driver and a sector uniquely exposed to risks that current policy frameworks were not designed to address.

Top Issues

VIEW ALL