Middle East Tensions Raise Spring Planting Concerns

Faith Parum, Ph.D.

Economist

Key Takeaways

- With spring planting beginning around the U.S., it is critical to secure transit, along with the necessary risk‑coverage insurance, for vessels carrying fertilizers through the Strait of Hormuz. If farmers are unable to obtain the remaining supplies in time, we could see reductions or shifts in planted acreage and lower yields, which affects our nation’s food security and the affordability of essential goods.

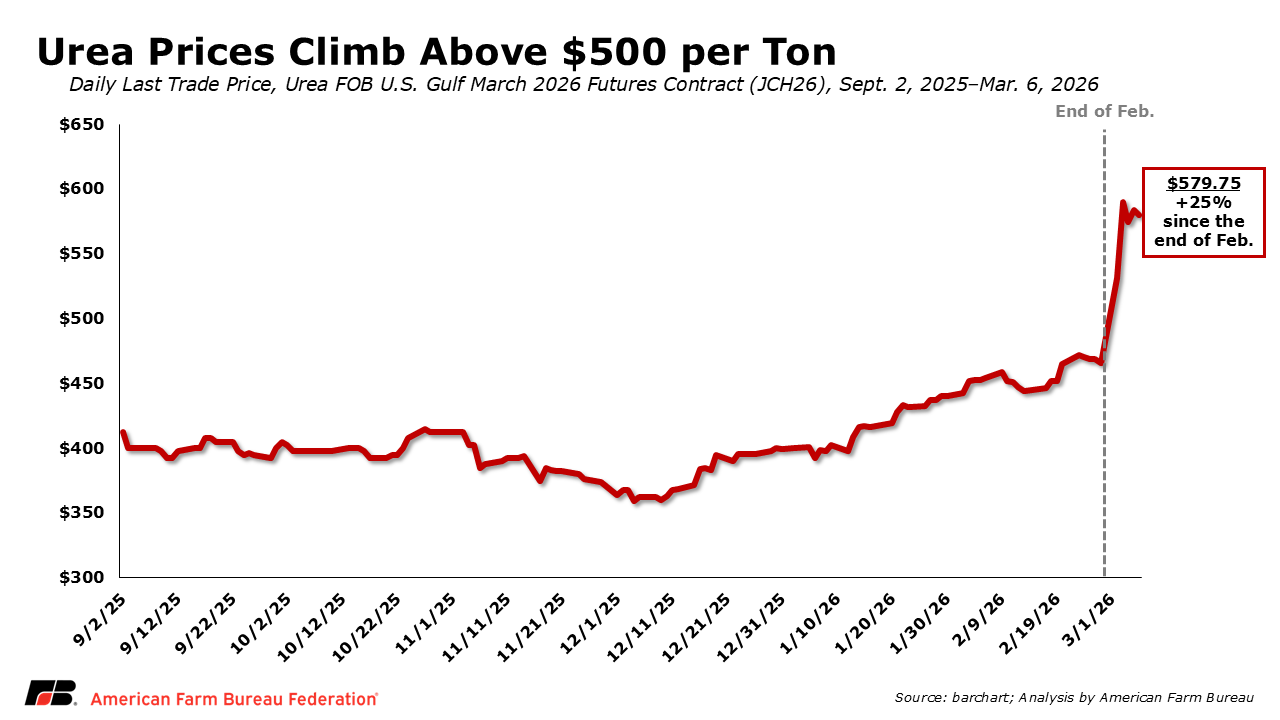

- Middle East tensions are adding uncertainty to fertilizer markets at the start of the U.S. planting season. Farmers are attempting to make or finalize fertilizer purchases just as global energy and fertilizer markets react to instability in a major fertilizer-producing region.

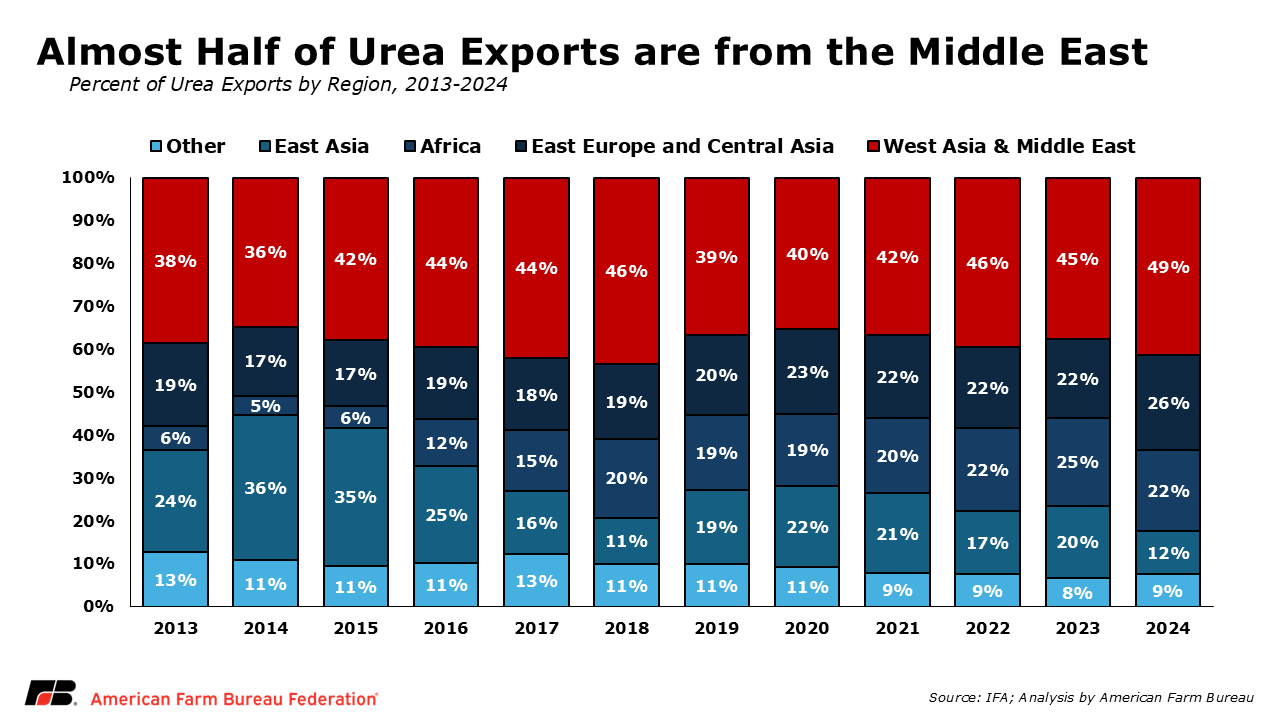

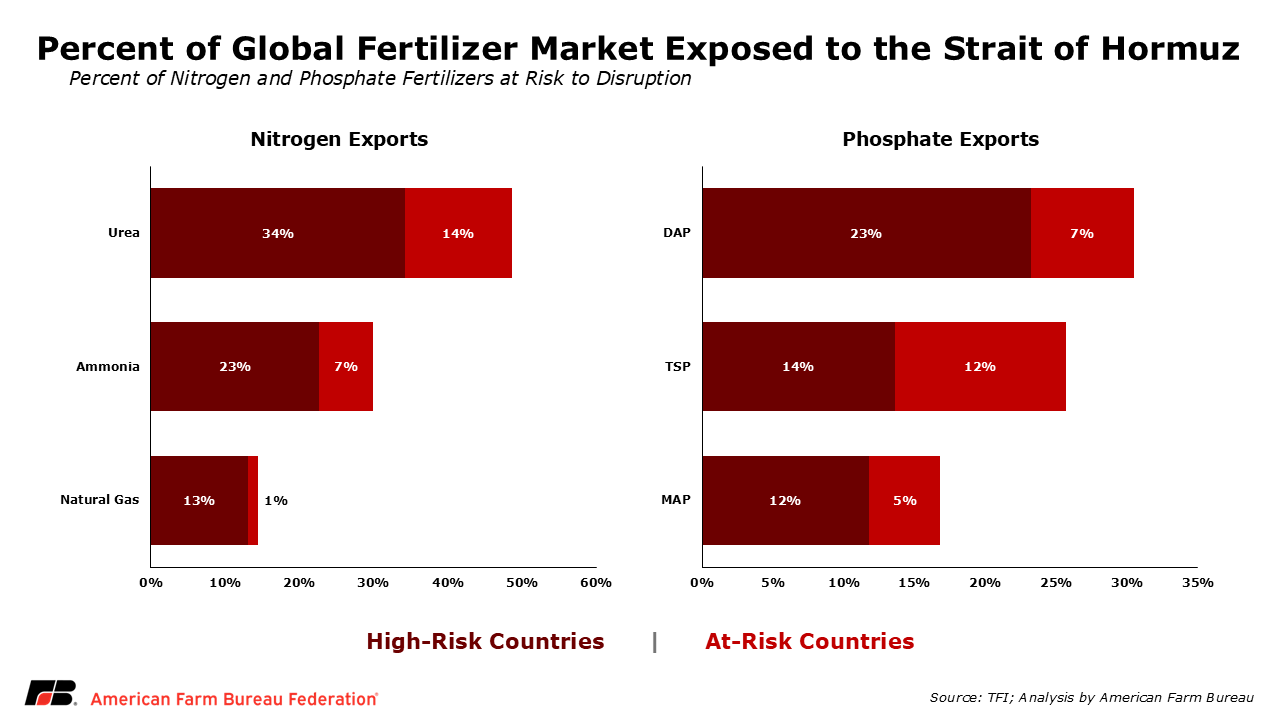

- Nitrogen fertilizer supply chains are closely tied to the Persian Gulf. Countries exposed to disruptions in the region account for nearly 49% of global urea exports and about 30% of global ammonia exports.

- At a time when margins are already tight and input costs record high, global conflicts that disrupt fertilizer supplies or raise fuel prices could increase production costs for U.S. farmers. Fertilizer and fuel prices are largely determined in global markets, meaning U.S. farmers can experience higher input costs even when the Middle East is not the primary direct supplier of specific fertilizer products to the United States.

American farmers are entering the 2026 spring planting season amid geopolitical tensions involving Iran and nearby Persian Gulf countries, which adds uncertainty to global energy and fertilizer markets. This timing matters because fertilizer purchasing, field preparation and early season fertilizer applications are already underway, limiting farmers’ ability to adjust if input prices spike suddenly. Anecdotally, farmers are already considering reducing corn acres planted in exchange for crops like soybeans that are less exposed to fertilizer price volatility.

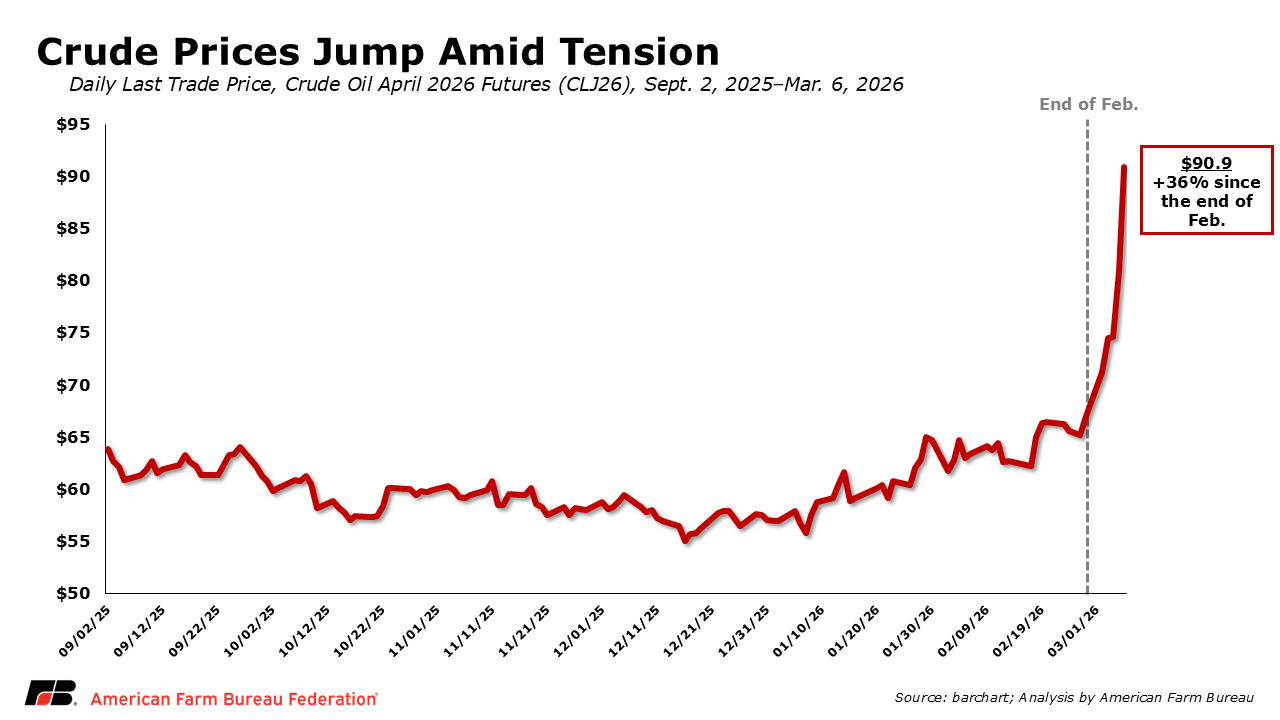

At the same time, many farmers are already facing significant cost pressures as production expenses remain elevated, reducing working capital that would normally help absorb unexpected shocks. In this environment, disruptions in global energy markets can quickly translate into higher input costs for farmers. One reason these geopolitical developments matter for agriculture is the region’s role in global energy and fertilizer markets, particularly through the Strait of Hormuz.

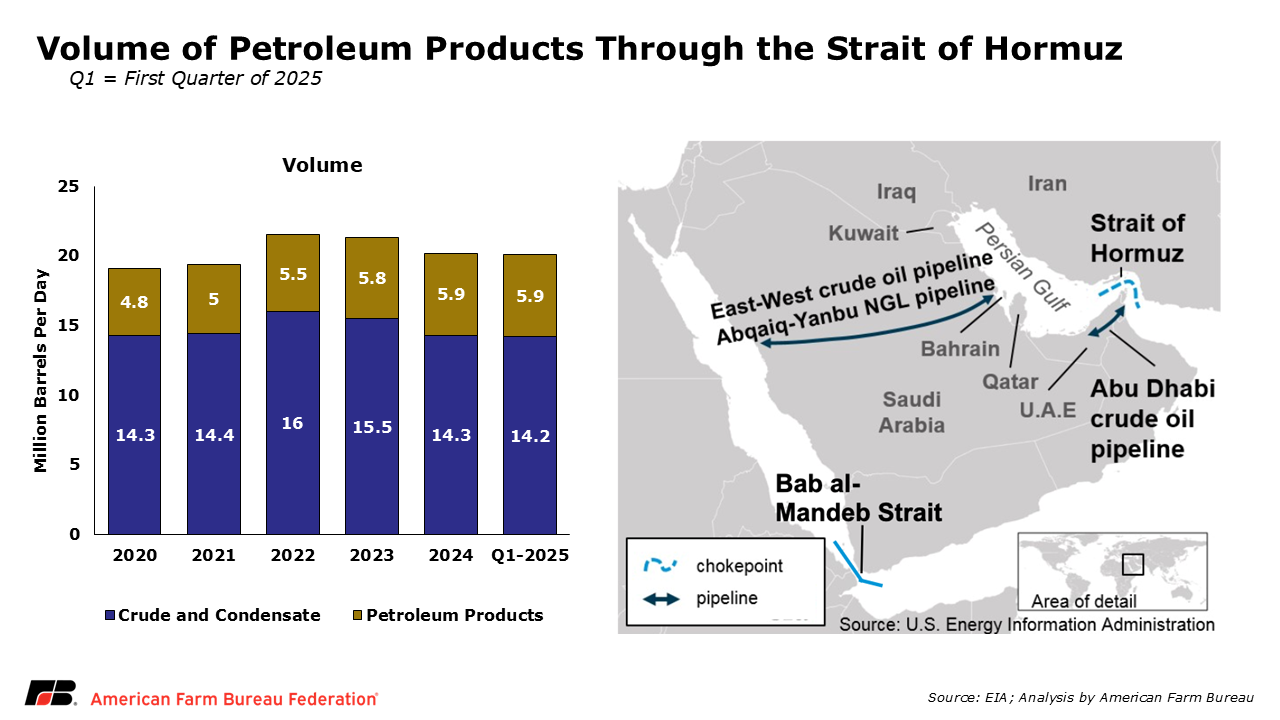

The Strait of Hormuz is central to energy and fertilizer trade. Oil flowing through the Strait averaged about 20 million barrels per day in 2024, roughly 20% of global petroleum liquids consumption. Because energy is a major input to fertilizer production and transportation, disruptions or heightened risk in the region can amplify volatility across agricultural input markets.

The Middle East’s Role in Global Fertilizer Supply

Iran holds some of the world’s largest natural gas reserves, and natural gas is the key feedstock used to produce ammonia, the foundational input for most nitrogen fertilizers. Urea, which contains about 46% nitrogen, is the most widely used solid nitrogen fertilizer globally and plays a central role in crop production systems.

The Middle East is an important hub for nitrogen fertilizer production and exports. Countries exposed to disruption in the region account for nearly 49% of global urea exports and about 30% of global ammonia exports, reflecting the concentration of fertilizer production and export capacity in and near the Persian Gulf. Major exporters include Iran, Qatar, Saudi Arabia and Egypt.

The potential disruption extends beyond Iran’s own fertilizer production. Large volumes of urea, ammonia, phosphates, sulfur and petroleum produced in Gulf countries move through the Strait of Hormuz each year. Egypt also represents a vulnerability in nitrogen markets because fertilizer production there depends heavily on natural gas supplies, which can affect output when gas availability is disrupted.

Taken together, the concentration of fertilizer production, fertilizer inputs and shipping routes in the Persian Gulf means disruptions in the region can influence a substantial share of globally traded nitrogen fertilizer.

Fertilizer Is a Global Market

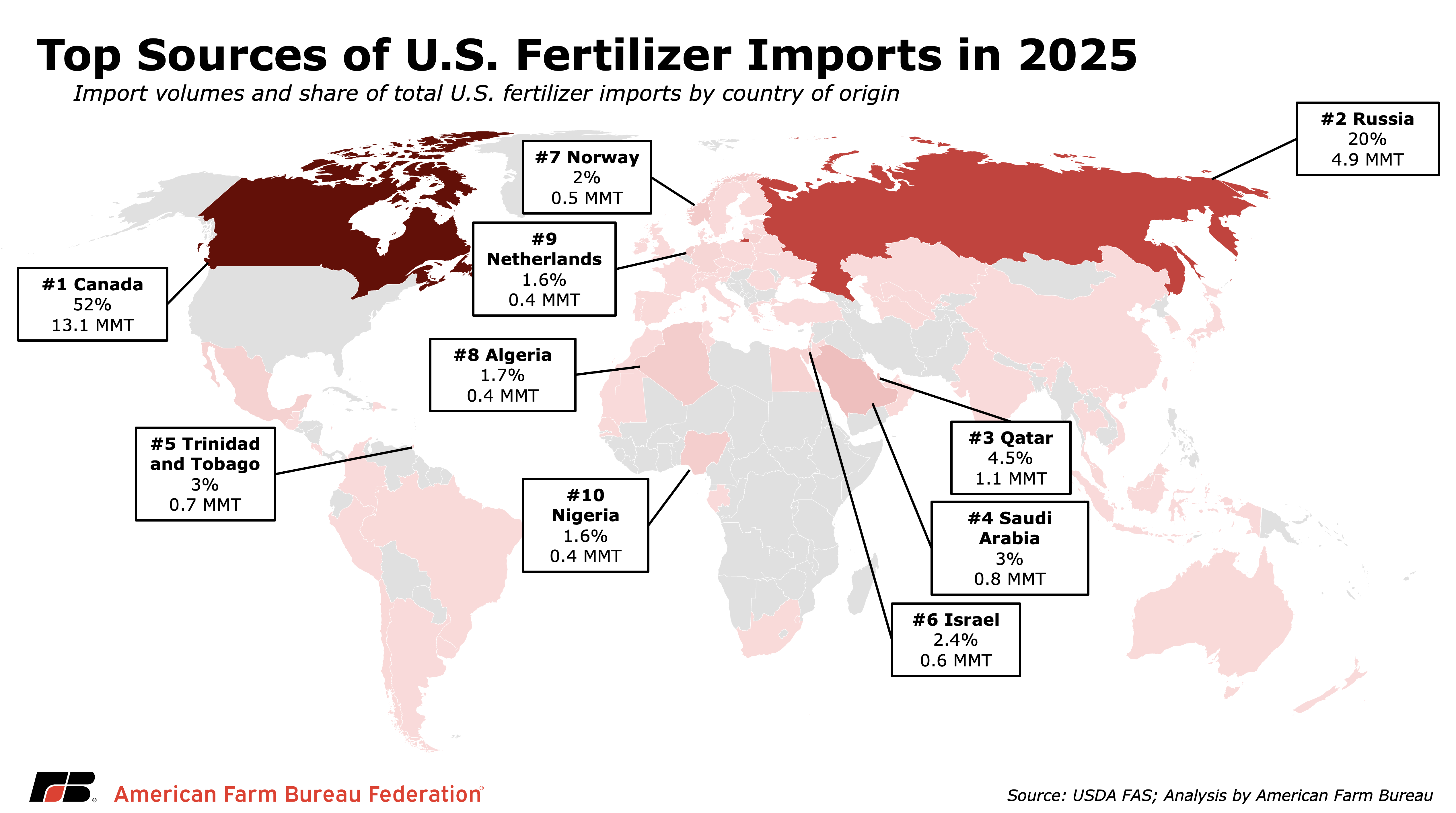

Fertilizer markets are globally integrated, so supply disruptions in one region can influence prices and availability elsewhere. The United States relies on both domestic production and imports to meet fertilizer demand, and import exposure varies by nutrient. Roughly 97% of potassium is imported, 18% of nitrogen and 13% of phosphate. This import exposure increases sensitivity to global trade disruptions, particularly during seasonal demand peaks.

This means that even though the United States does not directly import large quantities of fertilizer from the Middle East, domestic fertilizer markets still respond to price movements in the region. For instance, if countries that rely more heavily on Persian Gulf fertilizer supplies, such as India or Brazil, are forced to seek alternative sources, their demand may shift toward other global suppliers, increasing competition for available product and driving prices higher for U.S. farmers. Global fertilizer supply conditions can also be affected by policy actions in other major producing countries. For example, China has periodically considered or implemented fertilizer export restrictions to prioritize domestic supply, which can tighten global availability, particularly for phosphate fertilizers. They currently are restricting exports until the end of August 2026.

Impacts on Energy Markets

Fuel prices also influence farm operations more broadly. Diesel powers many aspects of agricultural production, including field preparation, planting, fertilizer application and crop transportation. Rising energy prices therefore affect both fertilizer production costs and on-farm operating expenses.

Pressure Compounded by Planting

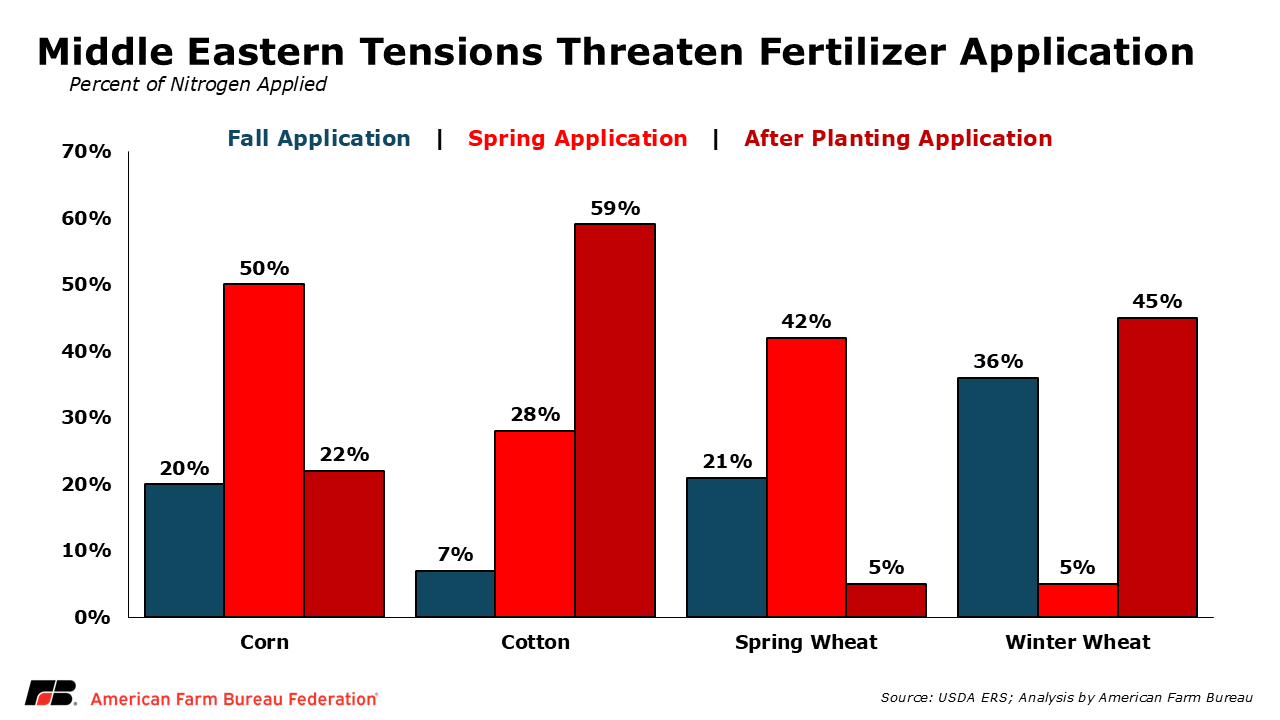

These developments come just as fertilizer and fuel demand rises ahead of spring planting. In the South, including Texas, Louisiana, Mississippi, Georgia and the Carolinas, corn planting can begin as early as late January and continues into March, with cotton planting beginning as early as February and continuing through May. Winter wheat planted last fall is also breaking dormancy across the Southern Plains and requires nitrogen applications during early spring growth.

In the Corn Belt, including Iowa, Illinois, Indiana, Ohio and Nebraska, corn planting generally begins in late April through mid-May, followed by soybean planting shortly afterward. Farmers in these states are currently finalizing fertilizer purchases and preparing for spring fieldwork.

Further north, producers in Minnesota, North Dakota and South Dakota typically plant from May into early June, with most activity concentrated in May. Farmers in these northern regions face a shorter planting window due to colder climates; and even though their planting season occurs later, fertilizer prices and availability may still be affected by earlier supply disruptions or shipping delays in global markets.

In total, about 50% of nitrogen applied to corn, 28% applied to cotton and 42% applied to spring wheat is typically applied in the spring. As a result, disruptions to fertilizer supply chains during this early period could have outsized effects on input availability and prices, potentially affecting crop yields and farm operational schedules during the most critical months of the planting season.

Bottom Line

Markets remain uncertain, and the duration of disruptions in the Middle East will ultimately determine how much fertilizer and fuel prices move in the months ahead. While the United States is the world’s largest producer of oil and natural gas, fuel and fertilizer markets remain globally interconnected.

Countries exposed to instability in the Persian Gulf account for nearly half of globally traded urea exports and roughly 30% of ammonia exports. Because these products are essential for crop production, disruptions in the region can influence fertilizer availability and prices well beyond the Middle East.

As farmers prepare to plant the 2026 crop and finalize fertilizer purchases, developments in global energy and fertilizer markets will be an important factor shaping input costs and farm budgets in the coming months. The administration has announced plans to help ensure the safe passage of fuel shipments through key global shipping lanes. Expanding these protections to include agricultural input supplies such as fertilizer should also be a priority given their importance to food production and national security.

Top Issues

VIEW ALL