Proposed Rail Merger Comes at Farmers’ Expense

photo credit: Getty Images

Daniel Munch

Economist

Key Takeaways

- The Union Pacific–Norfolk Southern merger would further exacerbate agricultural shippers’ already limited transportation options. In many regions, competition is limited not by efficiency but by geography and infrastructure, leaving farmers exposed to pricing and service decisions they cannot control.

- By eliminating independent carriers across key gateways and interchange points, the rail merger would reduce the limited bargaining leverage shippers still have today. Fewer routing and carrier options would leave large portions of the country dependent on a single railroad for end-to-end service.

- Agricultural shippers are uniquely vulnerable to consolidation because rail demand is highly inelastic. When rates rise, farmers cannot easily reduce shipments or switch modes and instead absorb higher costs through weaker basis and tighter margins.

- As railroads are primarily accountable to shareholders rather than rural shippers, consolidation weakens the remaining competitive pressures for pricing, service quality and capital allocation. Surface Transportation Board data show that agriculture is carrying a growing share of railroads’ cost recovery, with farm-product rail revenue above variable costs more than doubling between 2004 and 2023 as non-competitive movements expand.

- Large rail mergers increase systemic and resilience risks for time-sensitive agricultural supply chains. Fewer independent networks reduce redundancy, amplify the consequences of service disruptions, and raise broader food, export and national resilience concerns.

Railroads, Agriculture and a System Under Strain

Freight railroads are a vital component of the U.S. agricultural supply chain. Shippers of bulk commodities such as grain, oilseeds, fertilizer, feed ingredients and food products rely on rail for long-distance movement where trucking is cost-prohibitive and waterways are unavailable. In recent years, farm and food products have consistently accounted for roughly one-fifth of total U.S. rail tonnage, reflecting agriculture’s dependence on a rail network that connects rural production regions with domestic processors and export markets.

In 2023 alone, U.S. railroads carried more than 80 million tons of corn, 26 million tons of soybeans and nearly 26 million tons of wheat, much of it originating in the Midwest and Northern Plains and moving toward coastal ports or major processing hubs. For many regions, particularly those far from navigable waterways, rail is not simply the lowest-cost option. It is often the only viable one.

Against this backdrop, Union Pacific and Norfolk Southern have proposed an $85 billion merger that would create the first coast-to-coast Class I railroad in U.S. history. The combined system would span roughly 50,000 route miles across 43 states, linking the dominant western and eastern rail networks into a single carrier. Proponents describe the transaction as an “end-to-end” merger that would streamline operations, reduce interchange delays and improve service efficiency.

However, the economic implications of such a consolidation extend beyond operational integration. For agriculture and rural America, the central question is not whether railroads could operate a larger network, but how further concentration would affect pricing power, service reliability and accountability in markets where shippers already have limited alternatives.

Market Concentration and the Loss of Competitive Discipline

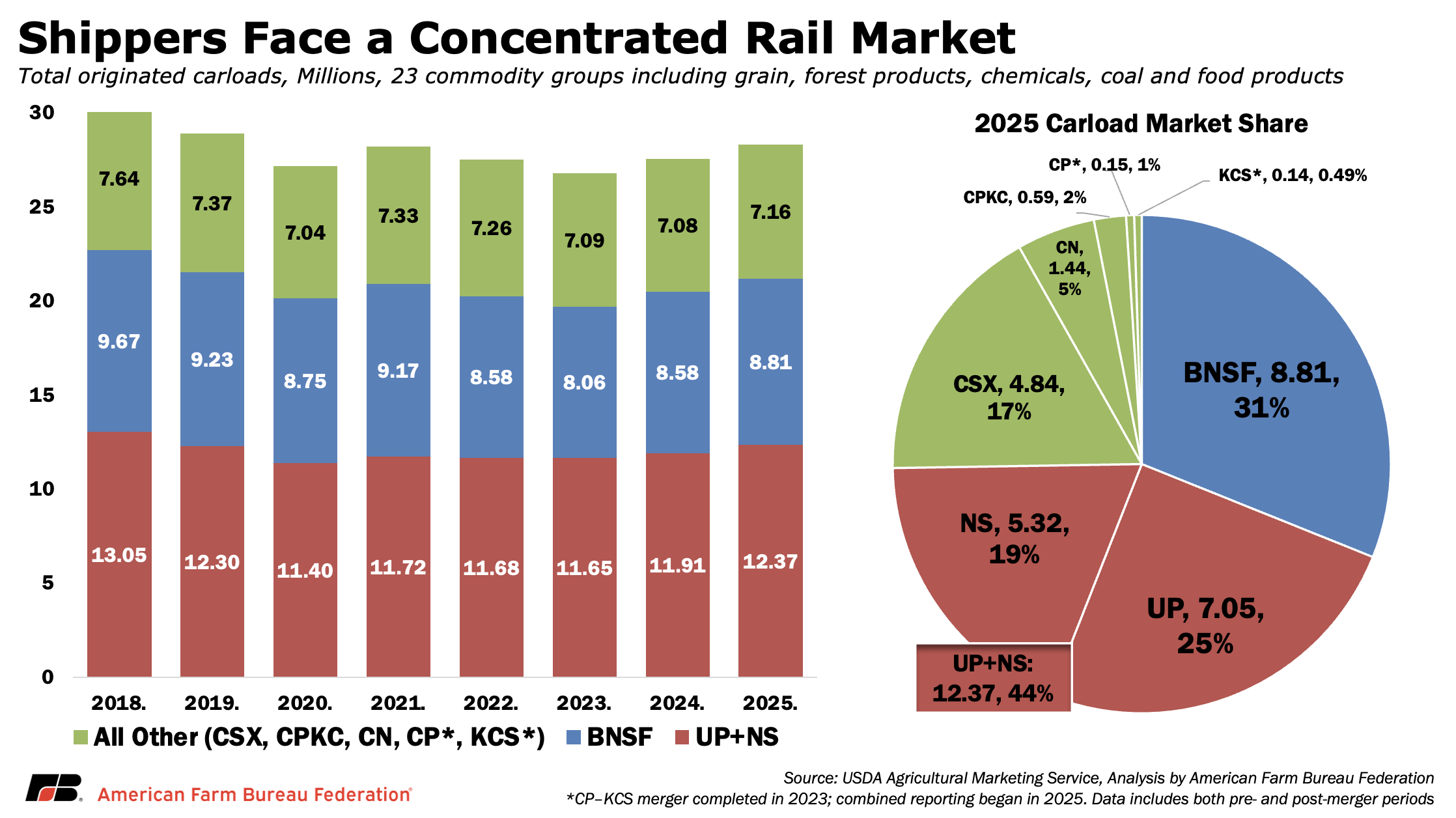

The U.S. freight rail industry has undergone decades of consolidation. Since deregulation under the Staggers Rail Act of 1980, the number of Class I railroads has fallen from more than 40 to just six. Four carriers now account for nearly 90% of total U.S. rail freight revenue, a level of concentration well above thresholds typically considered “highly concentrated” under federal antitrust guidelines.

Empirical measures make this consolidation clear. One commonly used yardstick is the Herfindahl–Hirschman Index (HHI), which adds up the market shares of all major firms in an industry to show how concentrated a market is. Lower values indicate more competition, while higher values signal that market power is concentrated in fewer hands. For Class I railroads, the HHI rose from 589 in 1978, a level consistent with a competitive market, to more than 2,200 by the mid-2000s, well above the U.S. Department of Justice’s threshold for a highly concentrated industry. Subsequent rail mergers have only reinforced this structure, leaving much of the eastern United States effectively served by a CSX–Norfolk Southern duopoly and much of the West dominated by Union Pacific and BNSF.

A combined UP–NS system would further tighten this landscape. Based on USDA and Surface Transportation Board (STB) data, the merged carrier would account for roughly 44% of total originated carloads across major commodity groups and more than one-third of all grain rail movements nationwide. In practical terms, this would leave large portions of the country dependent on a single railroad for end-to-end service, eliminating key interchange points, such as Chicago, St. Louis or New Orleans, where shippers previously could bargain between UP and NS.

For agricultural shippers, concentration matters because rail competition is already limited at the local level. Approximately 95% of grain elevators are served by only one railroad. In these settings, competitive discipline does not come from the ability to switch carriers, but from regulatory oversight that substitutes imperfectly for market forces.

Inelastic Demand and Pricing Power in Agricultural Rail Markets

The vulnerability of agricultural shippers to further consolidation is magnified by the inelastic nature of rail demand, meaning farmers often cannot meaningfully reduce or change how they ship, even when rail costs rise. For many bulk commodities, especially grain produced far from river systems or major processing centers, rail is not easily substitutable. Trucking long distances significantly increases per-unit costs, while barge access is geographically limited.

Decades of transportation economics research shows that demand for rail transportation of agricultural commodities becomes increasingly inelastic as transportation alternatives disappear. Across rural regions where shippers lack nearby barge access or cost-effective trucking options, railroads have historically carried 85% to 95% of grain output, reflecting a near-total reliance on rail service. When rates increase in these regions, shipments do not fall proportionally. Instead, farmers often absorb the cost through lower net prices at the elevator or reduced margins on sales.

This dynamic gives railroads pricing power in captive markets. Under deregulation, carriers are permitted to engage in differential pricing, charging higher markups to customers with less elastic demand while offering lower rates where competition exists. Grain shippers served by fewer railroads or located farther from barge terminals consistently pay higher rates per ton-mile than similarly situated shippers with more transportation options.

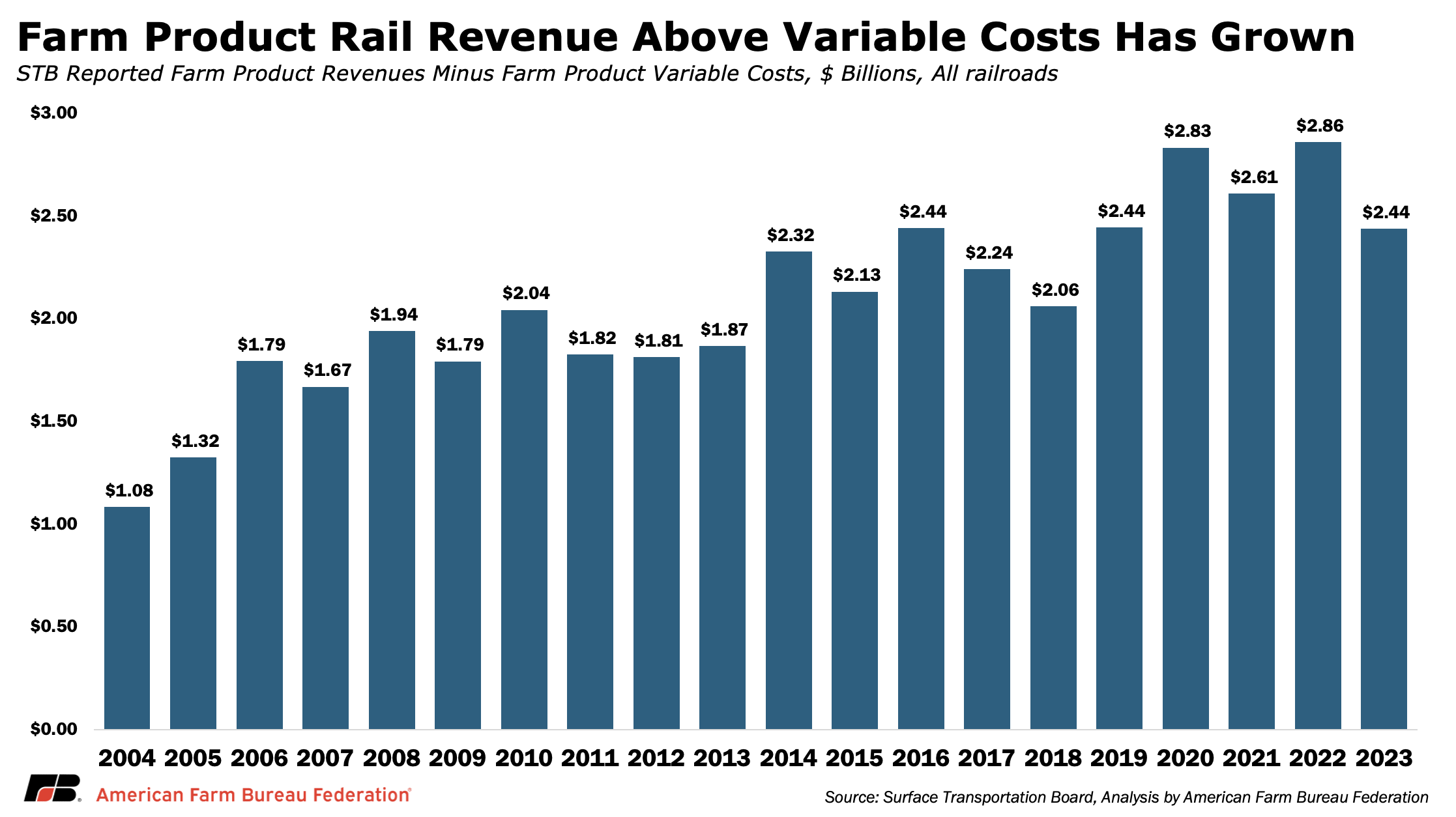

Surface Transportation Board data reinforce this pattern. Since 2004, the share of agricultural rail revenue derived from movements classified as non-competitive (a ratio of revenue to variable costs of more than 180%) has risen from the low-30% range to more than 50% on average since 2020. This means that a growing portion of rail revenue comes from shipments where competitive forces are weak, and regulatory oversight is the primary constraint on pricing behavior.

Unlike farmers, who sell into global commodity markets and routinely operate below cost during downturns, rail carriers operate under a regulatory framework that allows rates to be set above variable costs in order to ensure system viability. While this framework does not necessarily guarantee profitability, it substantially limits downside risk on traffic railroads choose to carry, particularly on movements where competitive alternatives are limited. As rail consolidation reduces competition across a larger share of movements, farmers increasingly bear the brunt of railroad cost recovery. Cost recovery risk increasingly shifts away from carriers and onto captive shippers who have few transportation options and limited ability to absorb higher costs.

STB data show how this shift has played out over time. From 2004 to 2023, farm product–related rail revenue above variable costs more than doubled, increasing from $1.08 billion to $2.44 billion. In practical terms, railroads are collecting more net revenue from farm-product movements than they did in the past. As more revenue flows through these movements, competitive conditions on agricultural rail routes become increasingly important. A merger that reduces routing or carrier options raises the risk that future revenue growth comes from fewer competitive choices rather than from efficiency gains, increasing exposure for agricultural shippers.

A UP–NS merger would not create this structure, but it would expand it. By eliminating one of the remaining independent Class I carriers across large portions of the country, the merger would increase the number of movements where shippers face a single carrier for the majority of their route. Public filings indicate that roughly 60% of Union Pacific’s total revenue is tied to movements that exceed the federal benchmark for limited competition, meaning a substantial portion of its earnings comes from markets with many captive shippers and few transportation options. In such environments, historical evidence suggests that pricing power increases even if nominal efficiencies are achieved.

Rail Merger’s Implications for Farm Costs and Food Prices

Transportation costs are a critical component of farm profitability, particularly for crops and livestock products that must move long distances to reach markets. When rail rates rise, farmers have limited ability to offset the increase. Commodity prices are set in global markets, input costs are largely fixed in the short run and production decisions cannot be easily adjusted after harvest. As a result, higher rail rates will be absorbed directly into farm margins.

Published rail tariff data provide a sense of how transportation costs grain shippers faced evolved over time. Across major carriers, average rail tariffs plus applicable fuel surcharges for corn, soybeans and wheat increased between 2015 and 2025. By 2025, tariff rates per bushel were between roughly 10% and more than 50% higher than a decade earlier across key commodities. While these figures reflect published tariffs rather than confidential contract rates, they illustrate a higher baseline cost for moving agricultural commodities by rail.

Over time, these costs can also ripple through the broader food system. Grain, oilseeds and feed ingredients are foundational inputs for livestock, dairy and food manufacturing. Increases in transportation costs function as a form of cost-push inflation, raising expenses throughout the supply chain. While not all costs are passed through fully or immediately, the cumulative effect can contribute to higher consumer prices, particularly for staple foods.

Railroads argue that operational efficiencies from single-line service offset these risks. However, historical evidence suggests that efficiency gains in concentrated rail markets do not reliably translate into lower rates for captive shippers. Following earlier mega-mergers, promised service improvements often materialized slowly, while pricing power increased as competitive alternatives diminished. In this context, the concern is not that efficiencies are impossible, but that absent competition, there is little incentive to share those efficiencies with agricultural customers.

Rail Merger Threatens Service Reliability and Creates Systemic Risk

Beyond pricing, service reliability is a core concern for agriculture. Farming operates on biological and seasonal timelines that do not accommodate prolonged transportation disruptions. Grain must move after harvest; livestock require consistent feed deliveries; and food processors depend on predictable inbound shipments.

This risk is not hypothetical. During the 2013–2014 rail congestion in the Northern Plains, driven by a surge in oil-by-rail traffic and a harsh winter, grain shipments were backlogged for weeks. At the time, shippers reported that railroads prioritized higher-revenue traffic such as crude oil over grain, leaving loaded grain cars sidelined. A North Dakota State University analysis estimated that delayed grain movement reduced farm income by more than $160 million as basis levels weakened, while USDA analysis found that Minnesota grain farmers lost roughly $100 million from rail-related delays that year.

Large rail mergers have historically struggled with integration. The Union Pacific–Southern Pacific merger in the late 1990s is frequently cited as a cautionary example. Following that merger, network congestion and operational failures led to months of service disruptions across the West and South. Grain shipments stalled, feed deliveries were delayed and agricultural losses mounted. Congressional inquiries later estimated the broader economic damage at $4 billion.

More recent integration challenges, including the CP–KCS merger, highlight similar risks. STB “cars not moved” data show massive spikes in railcars held for more than 48 hours following 2025 system integrations, reflecting transitional stress that can disrupt supply chains even without a full network breakdown.

Additionally, in seeking approval for the CP–KCS transaction, the combined carrier projected that removing interchanges and offering single-line service would shift 64,000 trucks to rail. Nearly three years later, reported conversions total approximately 16,000, around 74% below the initial projection. While each rail merger differs, recent experience suggests that volume and efficiency claims often prove difficult to achieve in practice.

A combined UP–NS system would create a single, contiguous rail network spanning much of the country. While the two railroads do not run parallel tracks across most regions, they currently operate as independent systems, providing redundancy across interchange points, gateways, operating centers and long-haul corridors. Merging those systems concentrates operational control and reduces system-level redundancy. As a result, weather events, labor disputes, cyber or technology failures, or bottlenecks affecting shared gateways or key corridors would have broader consequences when fewer independent networks exist to absorb disruptions.

For agriculture, this matters because redundancy is resilience. Multiple independent carriers provide alternative routings and operational workarounds during disruptions, even when physical track does not overlap. A single coast-to-coast network reduces those options, increasing the severity of service failures and raising broader national resilience and security concerns given rail’s role in food, energy and defense supply chains.

Rural Access, Investment and Long-Term Accountability

The long-term effects of consolidation extend beyond rates and short-term service metrics. Railroads allocate capital based on expected returns, prioritizing high-density corridors and traffic with the strongest revenue profiles. Low-volume rural lines and branch routes often struggle to compete for investment in this environment.

Following past mergers, some rural shippers have seen reduced service frequency, fewer car allocations or pressure to shift traffic to trucking. Short-line railroads, which often serve as first-mile connections for agriculture, have in some cases faced reduced interchange flexibility and routing options following large Class I mergers, limiting local competition and service alternatives for rural shippers.

The financial trajectory of the merging carriers also warrants attention. Between 2014 and 2024, Union Pacific’s total carload volumes declined by approximately 13%, while revenue per unit increased by roughly 17%. Over the same period, combined UP–NS volumes have fallen by about 11%. Against that backdrop, projections that the merged system will quickly reverse course and grow volumes by double digits in just a few years deserve scrutiny.

These outcomes are not driven by malice, but by incentives. Publicly traded railroads are accountable primarily to shareholders, whose ownership is dominated by large institutional investors generally concentrated in major financial centers rather than rural America. As a result, management performance is evaluated through financial metrics such as operating ratios, earnings growth and capital efficiency, rather than the service needs of the rural communities most dependent on rail access. None of these metrics explicitly reward maintaining service levels or price discipline in captive rural markets.

In competitive environments, shippers discipline behavior through choice. In captive markets, regulation is the primary substitute. As consolidation increases, the effectiveness of that substitution becomes more critical and more strained. Regulatory remedies, when they arrive, often follow prolonged disputes and do not fully reverse losses already incurred by farmers and rural businesses. Regulatory oversight cannot replicate the discipline of competition. Once competition is eliminated, service and pricing harms occur immediately, while remedies arrive, if at all, only after damage is done.

The Rail Merger Review Process

Unlike mergers in most industries, which are reviewed under traditional antitrust standards in federal court, large railroad consolidations are decided by the STB under a heightened “public interest” standard adopted after earlier waves of rail consolidation. The railroads must submit a detailed application addressing competitive impacts, service implications and public benefits. Before the Board evaluates the merits, it conducts a threshold review to determine whether the filing is complete. Only after an application is accepted does the STB establish a formal schedule for evidence, shipper testimony, environmental review and potential conditions.

Union Pacific and Norfolk Southern filed their merger application in December 2025, but in January 2026 the STB rejected it as incomplete, citing deficiencies in required documentation and impact analysis. In a Feb. 17 letter to regulators, the railroads stated they will submit a revised application on April 30, 2026. Only if that refiling is accepted as complete would the case move into months of formal review and public scrutiny. For agricultural shippers, that regulatory phase represents the primary opportunity to weigh competitive harms and service risks before consolidation becomes permanent.

Conclusion

The risk of the UP–NS merger is clear. It would leave farmers more dependent on fewer railroads at a time when they already have almost no ability to walk away from higher costs or poor service. The merger does not create new competition for agriculture. It removes what little leverage remains by eliminating key routing and interchange options that currently help keep rates and service in check. When that pressure disappears, history shows that farmers do not ship less — they get paid less.

If the promised growth and efficiencies do not materialize, the financial obligations of an $85 billion acquisition still must be recovered. In a system where agriculture is already carrying a growing share of rail cost recovery, those pressures will not fall evenly. They will fall where alternatives are few and demand cannot adjust.

For farmers and rural communities, this merger is not about bigger trains or faster routes. It is about who has choices and who does not, and whether the risks of consolidation are borne by shareholders or by the people who depend on rail to get their crops to market.

These risks spurred farmer and rancher voting delegates to the American Farm Bureau Federation’s 107th Convention in January to oppose the proposed merger between Union Pacific and Norfolk Southern.

Top Issues

VIEW ALL