Relaxing Beef Import Quotas Sends Mixed Signals to Ranchers

Daniel Munch

Economist

Key Takeaways

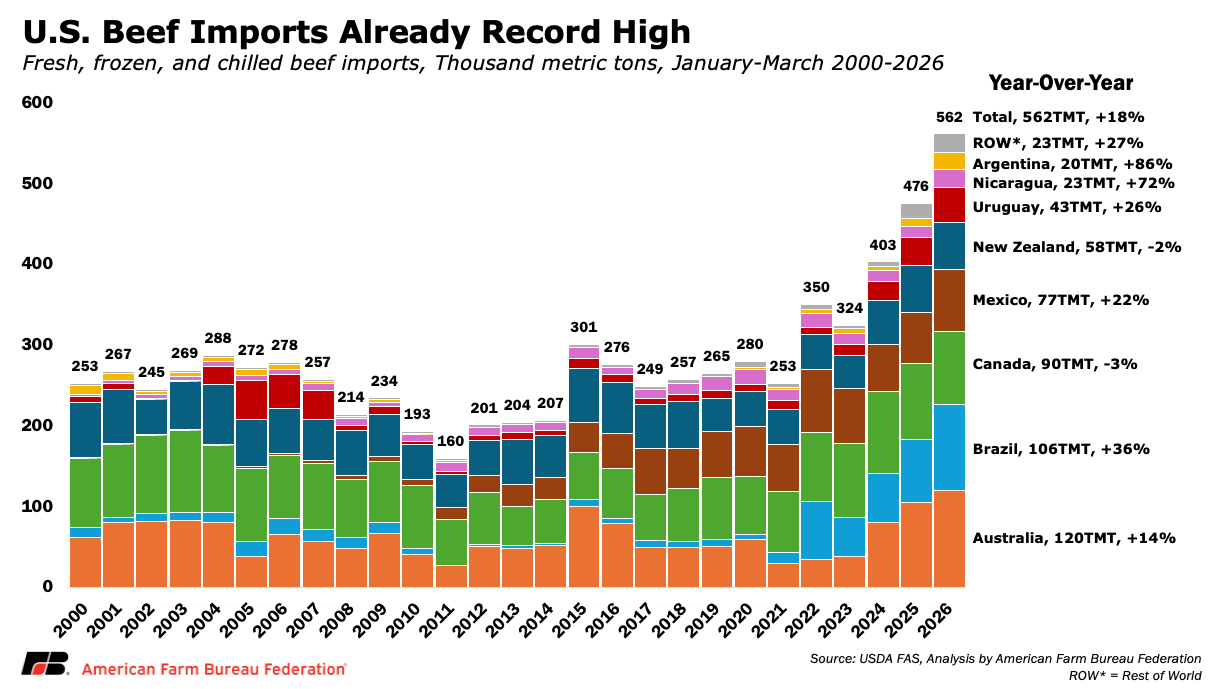

- U.S. beef imports are already running at historically elevated levels. During the first quarter of 2026, the U.S. imported 562,000 metric tons of beef and beef products valued at nearly $4.5 billion, up 18% from last year and 122% higher than five years ago.

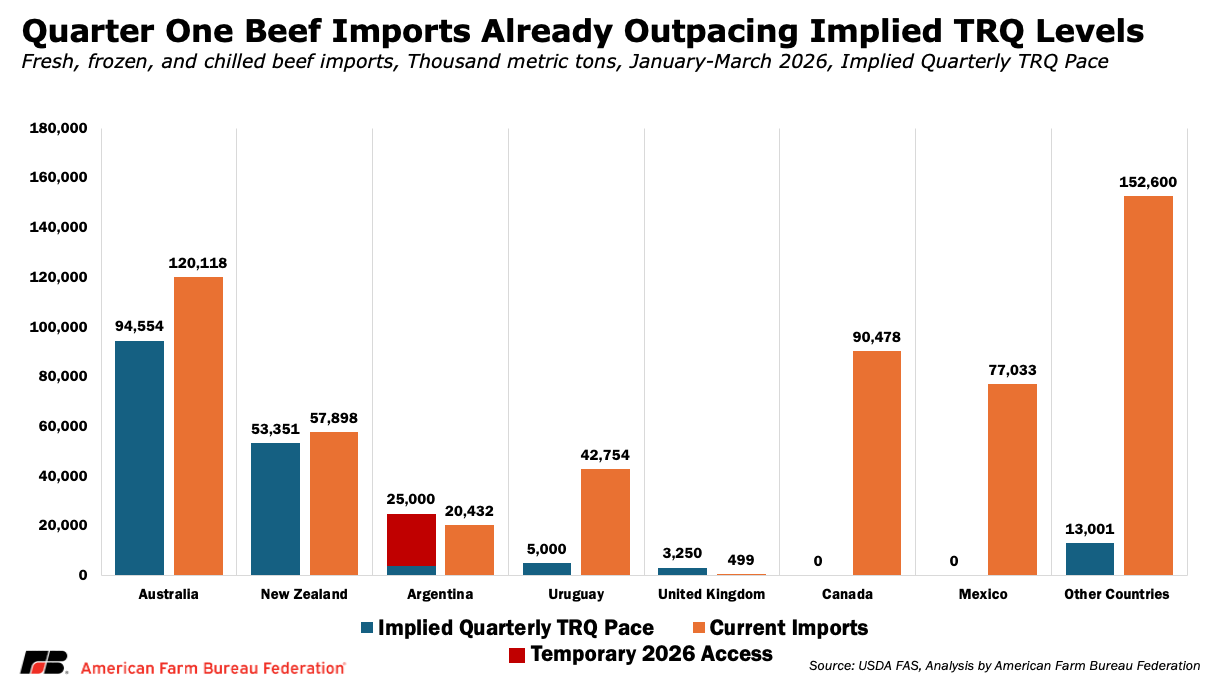

- Existing import volumes are already higher than the implied quarterly pace of several annual beef tariff-rate quotas (TRQs). Suspending quantitative TRQ limits for 200 days would significantly reduce the tariff burden on additional imported beef entering the U.S. market.

- Persistent drought and weak snowpack continue to constrain herd rebuilding. More than 79% of the beef cow herd across the 26 largest cattle-producing states is currently affected by drought conditions, increasing feed, forage and water costs.

- Expanding import access during a period of herd contraction discourages U.S. cattle producers from making a long-term investment in rebuilding domestic cattle supplies.

The United States cattle industry is navigating one of the tightest supply environments in decades. The domestic cattle herd remains near multi-decade lows following years of drought, elevated feed and operating costs, herd liquidation and ongoing disruptions tied to New World screwworm restrictions along the southern border. At the same time, beef imports have already hit records. During the first quarter of 2026, the U.S. imported 562,000 metric tons of beef and beef products valued at nearly $4.5 billion, up 18% from the same period last year and 122% higher than five years ago.

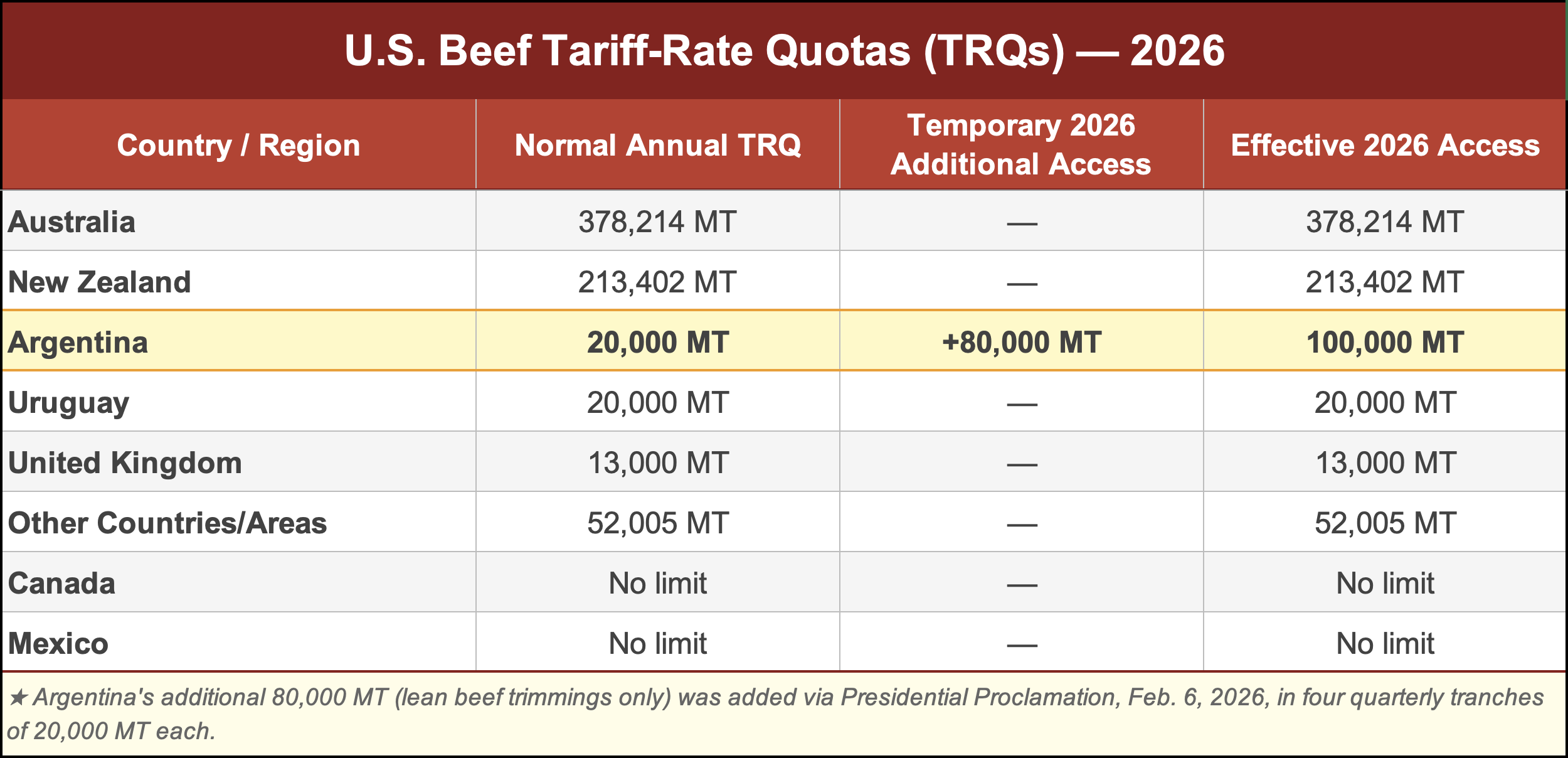

Against that backdrop, the administration is reportedly considering a 200-day suspension of quantitative limits under the U.S. beef tariff-rate quota system, temporarily allowing eligible trading partners to ship unlimited volumes of beef into the U.S. market at lower in-quota tariff rates. While such a policy may modestly supplement short-term imported beef availability, it does not address the underlying factors constraining U.S. cattle production. More importantly, encouraging additional imports risks weakening incentives for ranchers to retain heifers and rebuild domestic cattle inventories over the long run.

Imports Are Already Running Ahead of Implied TRQ Pace

Tariff-rate quotas allow specified volumes of imported beef to enter the United States at substantially lower tariff rates before higher over-quota tariffs apply. Under the current WTO beef TRQ framework, imports entering under quota generally face a tariff of just 4.4 cents per kilogram, while imports above quota face a 26.4% tariff. For beef valued around $7 per kilogram, that difference can exceed $1.80 per kilogram in tariff costs. As a result, suspending quantitative TRQ limits would significantly reduce the effective tariff burden on additional imported beef volumes entering the U.S. market.

Several major exporters already compete aggressively within the current quota system. Countries such as Australia, New Zealand, Uruguay and Argentina receive country-specific allocations, while other exporters, including Brazil and Nicaragua, compete within the pooled “Other Countries” quota category. Although imports above quota remain permissible, the substantially higher tariff structure currently serves as an economic constraint on additional low-cost imported product entering the U.S. market.

The current debate is not occurring in a low-import environment. Existing import volumes are already running ahead of the implied quarterly pace of several annual TRQ structures. During the first quarter of 2026, imports from Australia reached roughly 120,000 metric tons compared to an implied quarterly TRQ pace of approximately 95,000 metric tons, while imports from New Zealand totaled roughly 57,000 metric tons against an implied pace near 53,000 metric tons. Imports from Uruguay also exceeded their implied quarterly pace, while pooled “Other Countries” exporters such as Brazil and Nicaragua shipped roughly 153,000 metric tons compared to an implied quarterly pace of just 13,000 metric tons under the shared quota structure.

Import composition also shapes the likely market impact of additional TRQ liberalization. A large share of U.S. beef imports consists of boneless lean beef and trimmings used primarily for ground beef blending rather than the premium muscle cuts commonly produced through the U.S. grain-fed beef system. As a result, additional imported products may have a greater influence on ground beef supplies than on prices for steaks, roasts and many other retail beef cuts.

Domestic Herd Expansion Remains Constrained

Persistent drought and weak snowpack conditions across much of the Western U.S. continue to constrain the ability of ranchers to rebuild the domestic cattle herd. In many Western states, snowmelt supplies a substantial share of annual water availability, supporting pasture, forage and hay production critical to cow-calf operations. However, 2026 snowpack levels across major Western basins remain well below historical averages, limiting runoff potential and increasing uncertainty around grazing conditions and feed availability.

Drought conditions have also expanded well beyond the West. According to analysis highlighted by Oklahoma State University Extension, more than 79% of the beef cow herd across the 26 largest cattle-producing states is currently affected by drought conditions, representing over 70% of the total U.S. beef cow herd. As forage conditions tighten, producers face higher feed, hay and water costs, making herd expansion financially risky even amid strong cattle prices. While early signs of heifer retention have emerged, Oklahoma State notes that continued drought could interrupt those rebuilding efforts and further delay meaningful herd expansion.

Beef Market Does Not Need Mixed Signals

Additional import liberalization sends a conflicting market signal. Rather than reinforcing the long-term economic incentives needed for domestic herd rebuilding, further expanding imported beef access signals to producers that future supply shortfalls may increasingly be addressed through foreign product rather than domestic production recovery. That uncertainty can discourage heifer retention and long-term investment at precisely the moment ranchers are weighing whether conditions justify rebuilding the U.S. cattle herd.

Announcements related to expanded imported beef access have also contributed to heightened volatility in both cash and futures cattle markets. In October 2025, the announcement increasing Argentina’s beef tariff-rate quota access from 20,000 metric tons to 100,000 metric tons triggered a sharp market response, with cash cattle prices falling nearly 13% over the following month before eventually recovering. Several CME cattle contracts experienced multiple daily limit price movements during that period, creating additional challenges for farmers and ranchers using risk management tools such as futures hedging or Livestock Risk Protection (LRP) insurance. LRP coverage is unavailable on days when certain CME cattle contracts trade at daily price limits, temporarily limiting producers’ ability to manage downside market risk during periods of elevated volatility.

At the same time, consumer demand for beef has remained historically strong despite record-high retail prices. Under normal market conditions, sustained increases in beef prices would encourage consumers to shift toward lower-cost protein alternatives such as pork or chicken. Instead, beef demand has remained resilient and has become a key source of support for cattle prices during the current period of historically tight domestic supplies.

Conclusion

The current cattle market reflects years of drought, herd liquidation, elevated production costs and biological constraints that cannot be resolved through short-term import policy changes alone. Beef imports are already running at record levels, and additional TRQ liberalization would further lower barriers for imported product entering the U.S. market during a period when ranchers are weighing whether conditions support long-term herd rebuilding. While temporary import expansion may modestly supplement certain beef supplies, particularly for ground beef blending, it risks sending mixed signals to domestic producers at a critical stage in the cattle cycle. Long-term resiliency in the U.S. beef supply will ultimately depend on the economic confidence and ability of American ranchers to rebuild the domestic herd.

Top Issues

VIEW ALL