Ground Shift: What’s Reshaping America’s Agricultural Land Base

Daniel Munch

Economist

Key Takeaways

- Since 1982, cropland, pastureland and rangeland have declined, while developed land has increased by nearly 48 million acres (66%), roughly the size of Nebraska.

- Acres moving between cropland, pasture and the Conservation Reserve Program may remain connected to agriculture, while land converted to housing, industrial sites, roads or other built uses is far less likely to return to production.

- In 2024, more than 2 million landowners rented out 347.8 million acres for agricultural purposes, with non-operating landlords controlling 79% of rented-out acres.

- More than a third of non-operating landlords are 75 or older, but less than 5% of owned farmland is expected to be sold or gifted in the next five years, leaving trusts, wills, heirs and lease decisions central to who can keep farming.

Farmland pressure is often discussed as a national acreage-loss problem, but for farmers and ranchers the more immediate challenge is land access. Land can remain technically “agricultural” while becoming harder to rent, buy or keep in production. At the same time, acres converted to development, energy infrastructure or other built uses often do not return to farmland or ranchland.

The U.S. is not facing a sudden farmland cliff, but agricultural land is being reshaped by two concurrent forces: physical land-use change and ownership transition. Some acres are shifting among cropland, pasture and the Conservation Reserve Program (CRP), while others are being permanently converted to development. Meanwhile, a large share of land used for farming is controlled by absentee landlords, raising questions about succession planning, access for young, beginning and new farmers, rental access and long-term affordability.

Two recent USDA reports help frame these pressures. The 2022 National Resources Inventory (NRI), released in September 2025 by USDA’s Natural Resources Conservation Service, tracks land cover and land-use changes on non-federal lands, including cropland, pastureland, rangeland, forestland, developed land and CRP land. The 2024 Tenure, Ownership, and Transition of Agricultural Land survey, released in March 2026 by USDA’s National Agricultural Statistics Service and Economic Research Service, adds the ownership lens by examining rented agricultural land, landlord ownership structures and expected land transfers.

For agriculture, the risk is not just how many acres remain on paper. It is whether productive land remains available, affordable and workable as development, energy projects, data centers and generational ownership turnover increase competition for the same land base.

The Land Base is Changing, but not all Change is the Same

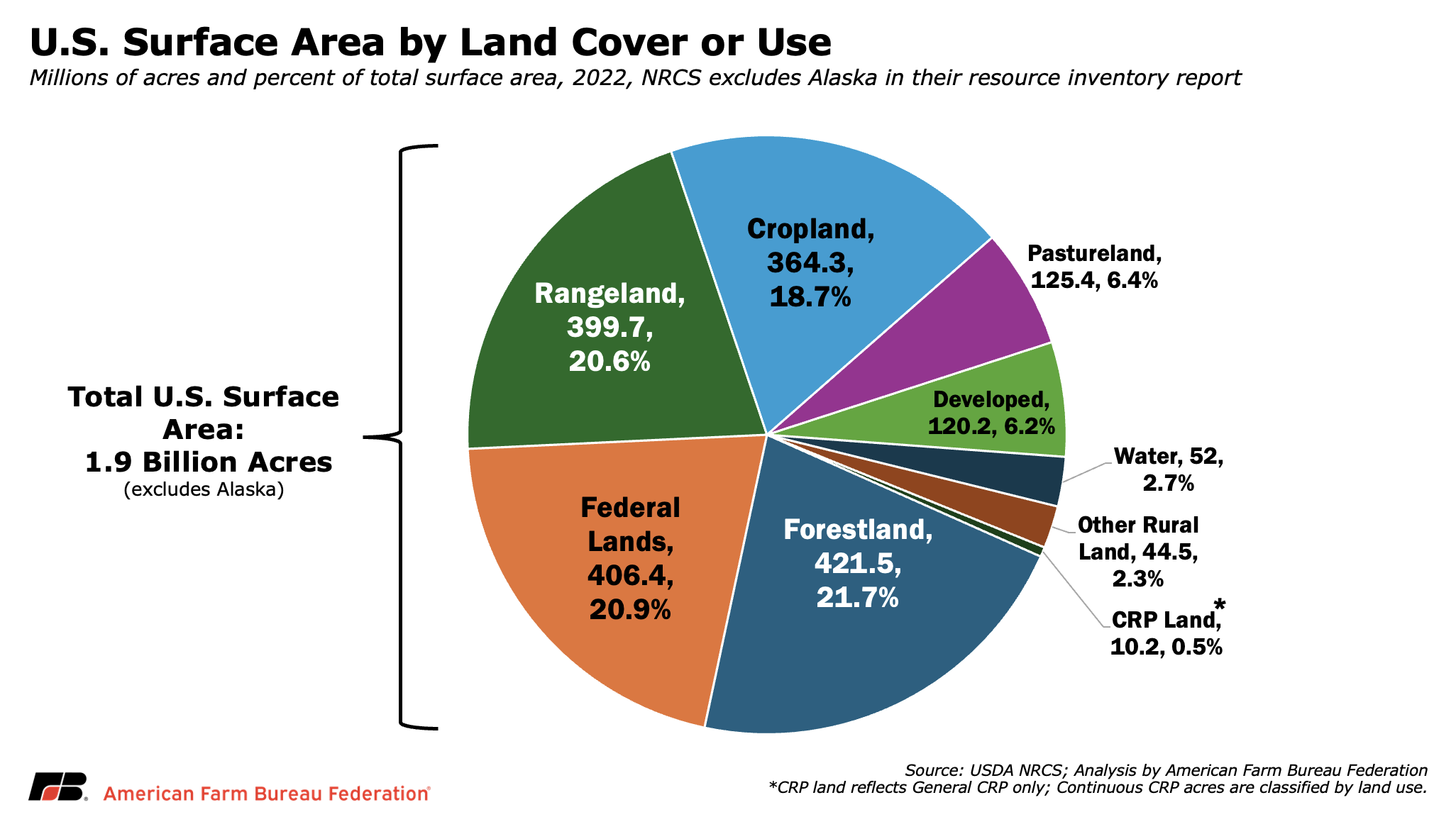

The NRI shows how large and varied the U.S. land base remains. In 2022, forestland was the largest land-use category in the NRI study area at 421.5 million acres, followed by federal land at 406.4 million acres, rangeland at 399.7 million acres and cropland at 364.3 million acres. Pastureland totaled 125.4 million acres, just above developed land at 120.2 million acres.

These categories are not the same as an all-purpose measure of “farmland.” The 2022 NRI covers the 48 contiguous states, Hawaii, Puerto Rico and the U.S. Virgin Islands, but not Alaska, which contains a large share of U.S. federal land (over 220 million acres). Federal land is also reported separately from the non-federal rural land-use categories the NRI tracks most closely. As a result, NRI totals are best used to understand land cover and land-use change across the primary agricultural footprint, not as a direct substitute for all-50-state land ownership or land-in-farms estimates.

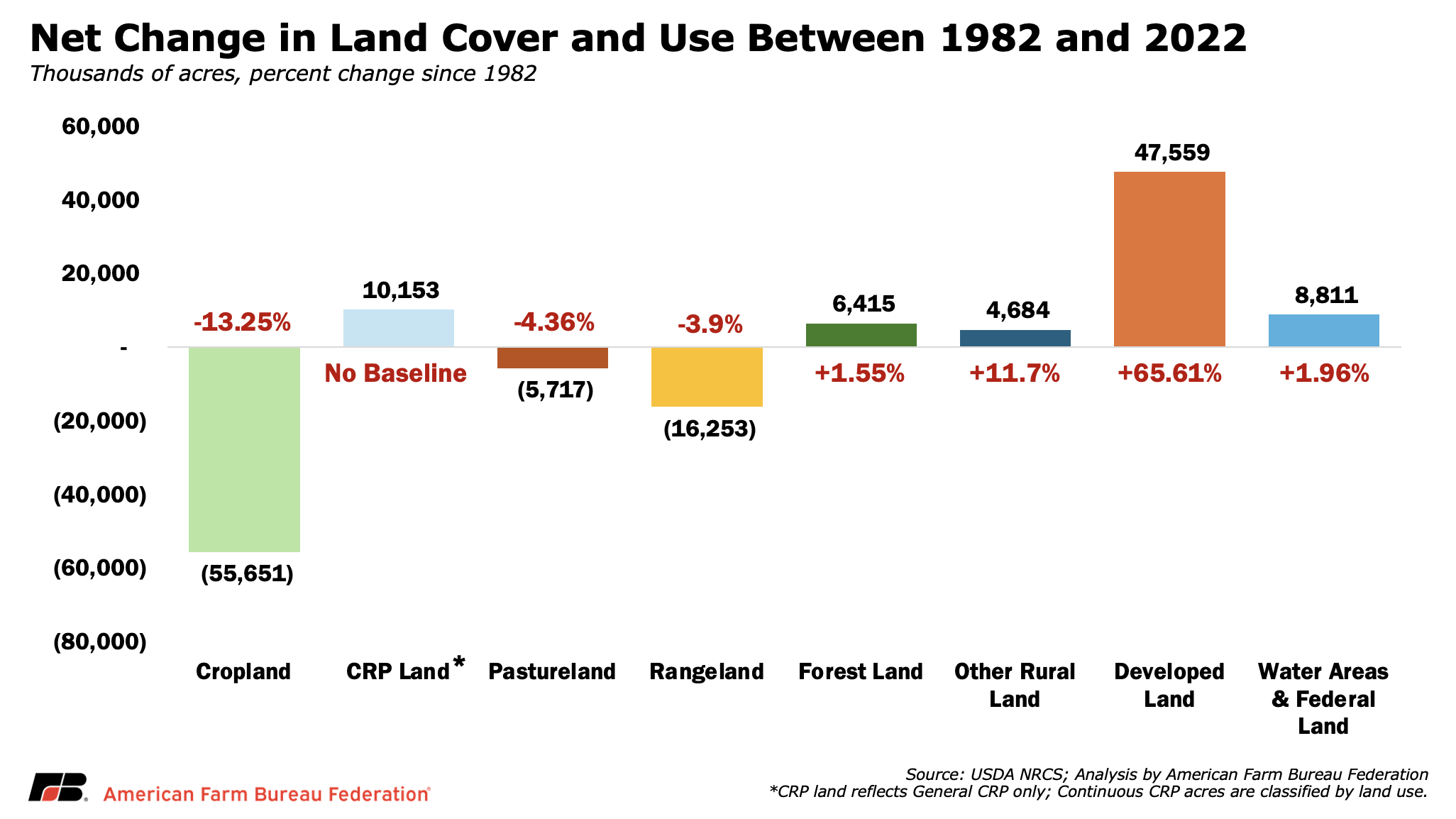

Even with those limitations, the long-term direction is clear. From 1982 to 2022, cropland declined by 55.7 million acres, a 13% drop from 1982 levels and an acreage loss similar to the size of the state of Kansas. Rangeland declined by 16.3 million acres (about the size of West Virginia), down 4%, while pastureland declined by 5.7 million acres, also about 4%. Over the same period, developed land increased by 47.6 million acres, an expansion roughly the size of Nebraska and equal to about 2.5% of the entire NRI study area. Developed land now totals 120.2 million acres, or about 6% of the land and water area covered by the inventory. Forestland, other rural land and land enrolled in the CRP also increased, reinforcing that the land base is moving in multiple directions.

These comparisons put the scale in perspective, but they should not be read as a one-for-one transfer from farmland to development. A decline in cropland does not mean every acre became housing, warehouses or pavement. Some acres shifted into pasture, conservation cover, forest or other rural uses, while temporarily fallow acres generally remain within the cropland category. Other acres can move back into production as commodity markets, livestock needs, conservation contracts, drought conditions or management decisions change. Net acreage changes show direction, but it does not fully capture how much land is moving among rural uses beneath the surface.

The Conservation Reserve Program is a federal conservation program that pays landowners to remove environmentally sensitive land from production and establish long-term vegetative cover. It was created under the Food Security Act of 1985, so CRP does not appear in the 1982 baseline. In the NRI, the CRP category generally reflects land enrolled through general CRP signup. Acres enrolled through continuous CRP, which targets specific conservation practices or environmentally sensitive areas, are instead counted based on their observed land cover or use, such as grassland, forest or marsh. As a result, the NRI’s CRP category is useful for tracking land-use change, but it should not be read as identical to total CRP enrollment.

Development has Slowed, but Conversion has not Stopped

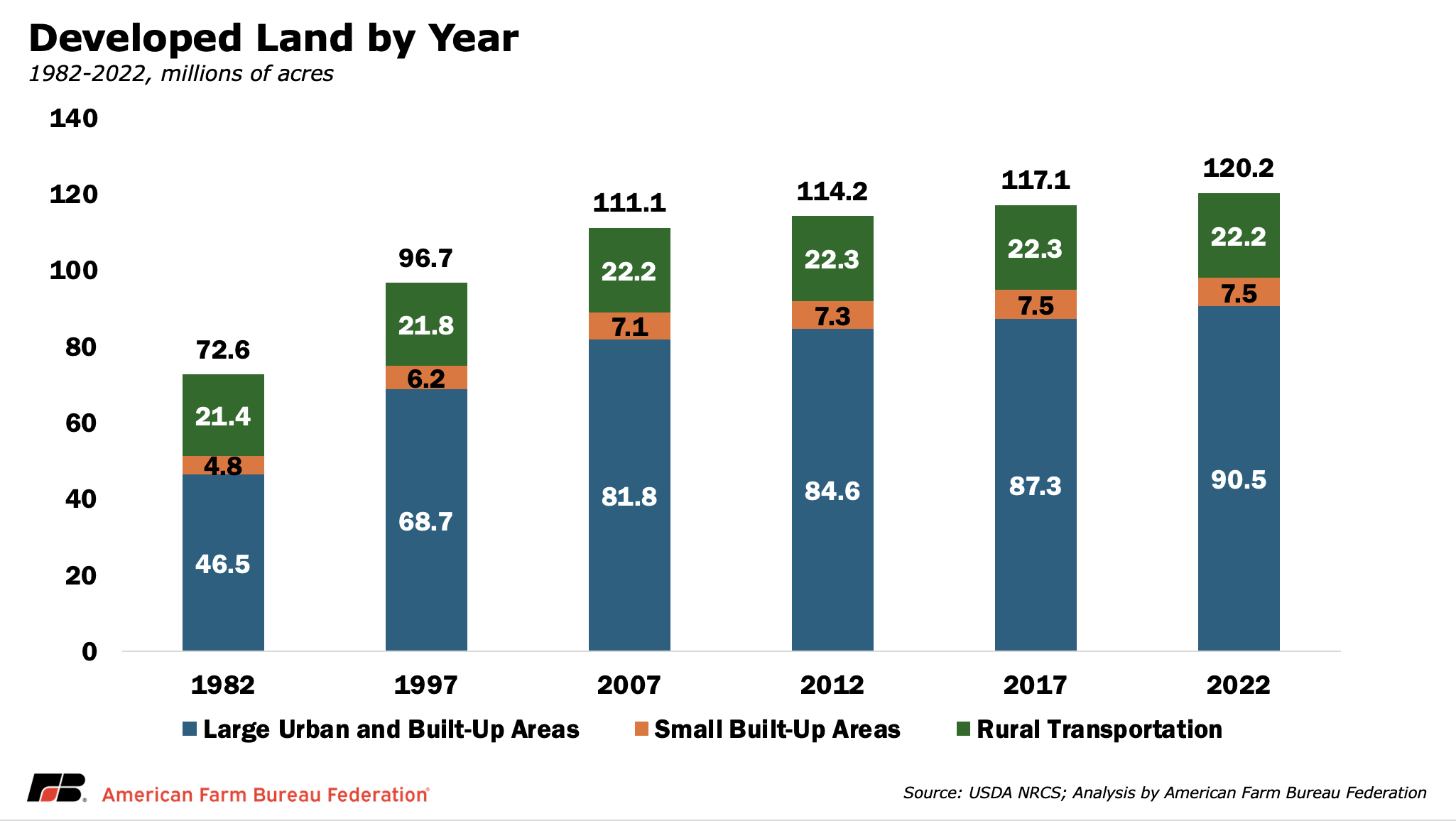

Development is the most permanent land-use pressure in the NRI, but the timing of that growth matters. Developed land increased from 72.6 million acres in 1982 to 120.2 million acres in 2022, a 66% increase. That means about 40% of all developed land in the NRI study area was developed during the last four decades.

Developed land in the NRI is broader than subdivisions or city growth. It includes large urban and built-up areas of at least 10 acres, small built-up areas between 0.25 and 10 acres and rural transportation corridors such as roads, highways and rail lines. Large urban and built-up areas drove most of the increase, nearly doubling from 46.5 million acres in 1982 to 90.5 million acres in 2022. Small built-up areas rose from 4.8 million acres to 7.5 million acres, while rural transportation remained near 22 million acres, meaning the long-term increase in developed land has come mostly from built-up expansion rather than new transportation corridors.

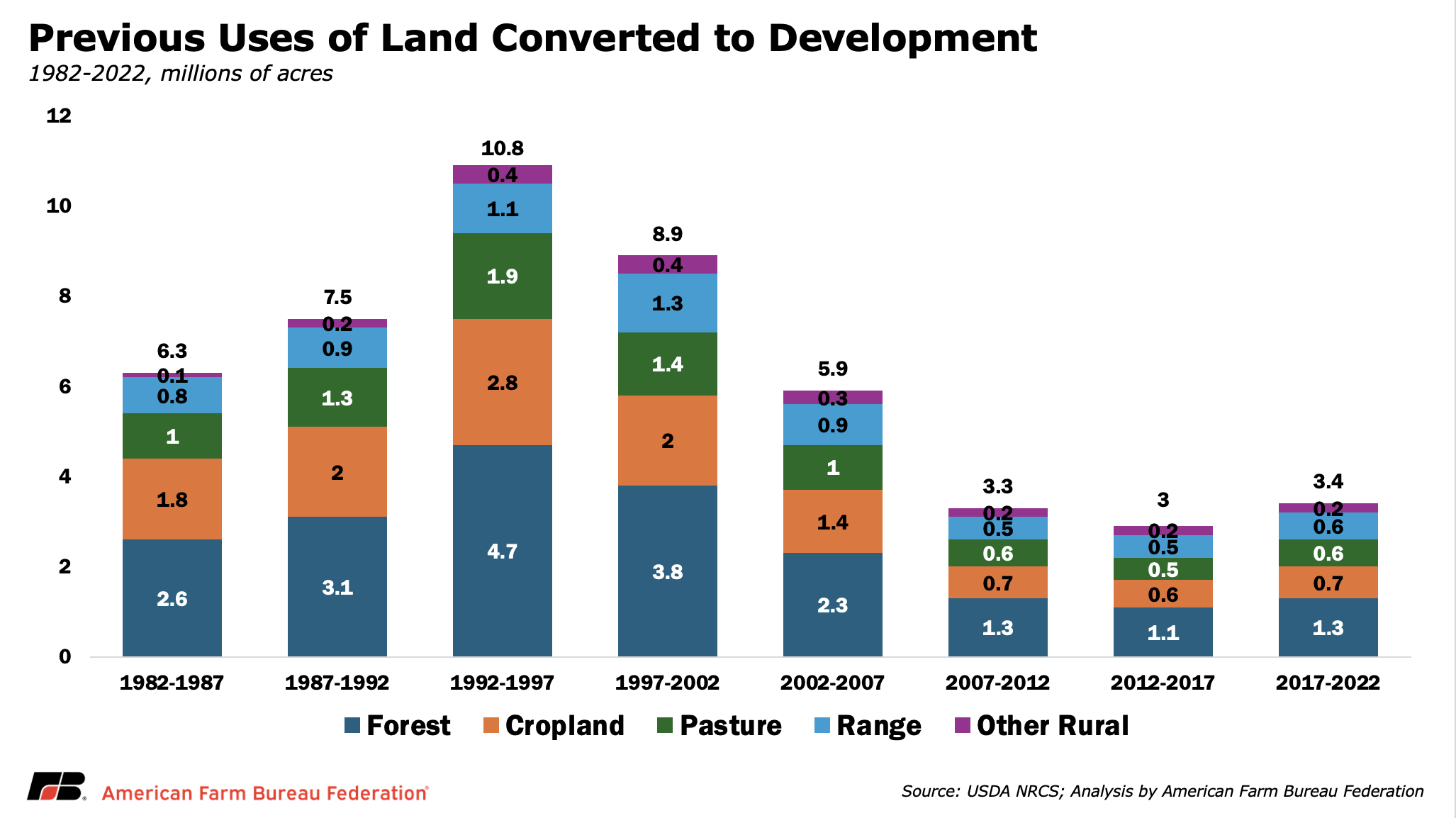

The pace of conversion, however, has slowed. New development peaked during the 1992–1997 period, when 10.8 million acres moved into developed uses. By comparison, newly developed land totaled roughly 3 million to 3.4 million acres in each of the last two five-year periods. That slowdown matters, but it should not be mistaken for a halt in conversion. Even at a slower pace, millions of acres are still being removed from the rural land base every five years.

The source of that newly developed land also complicates the story. Development is not coming only from cropland. Across the period studied, forestland contributed the largest share of newly developed land, followed by cropland, pastureland, rangeland and other rural land.

For agriculture, the concern is where conversion happens. Development pressure is often concentrated near population growth, transportation corridors, energy infrastructure and expanding regional economies. In those places, the loss of even a relatively small number of acres can matter if it fragments fields, raises nearby land values, complicates livestock operations or reduces the supply of land available for farmers trying to rent or buy.

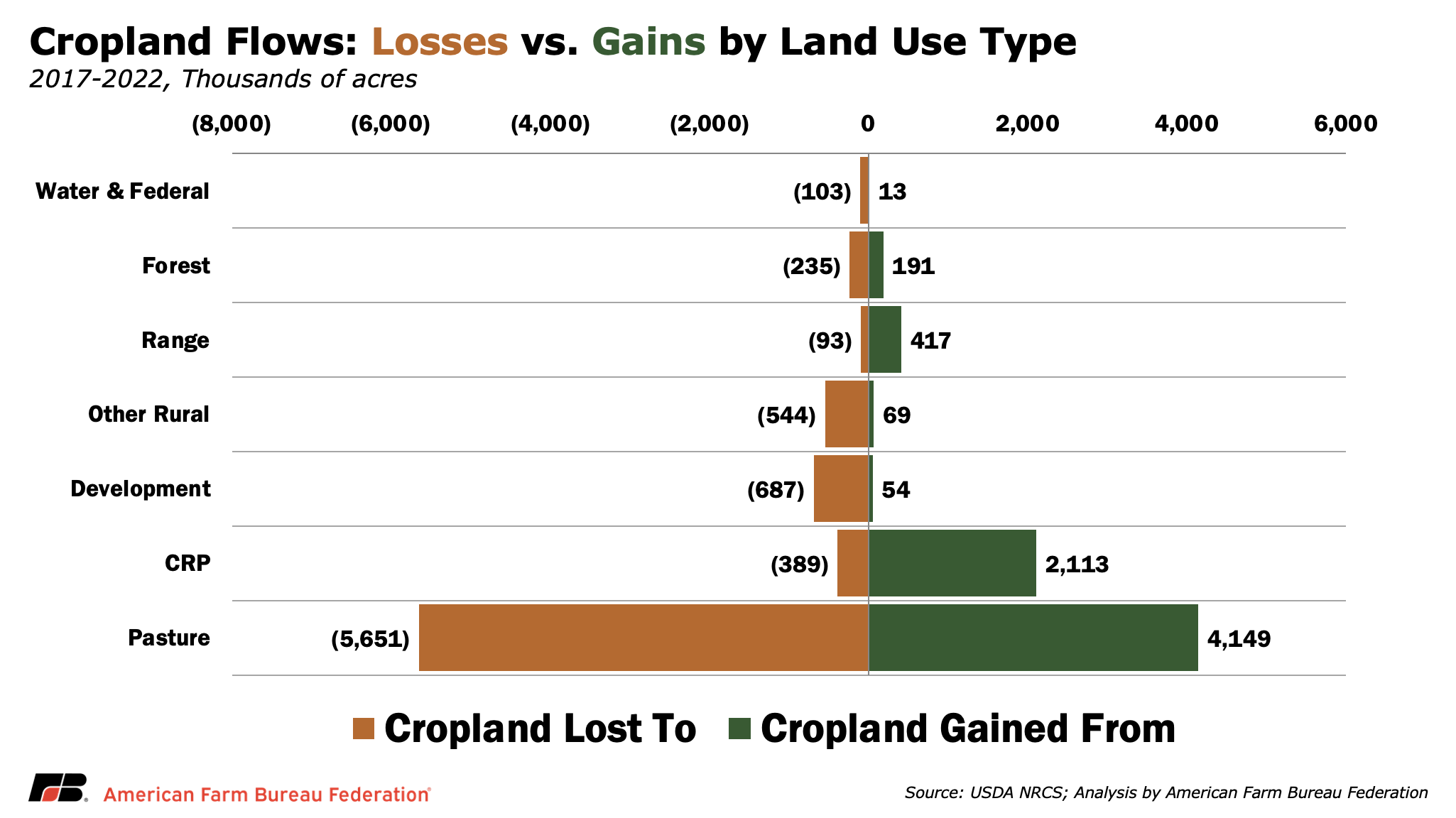

Cropland is Moving, not Just Disappearing

From 2017 to 2022, most cropland remained in place. Of the 365 million acres classified as cropland in 2017, 357.3 million acres were still cropland in 2022. Among cropland acres that did shift to other uses, the largest movement was into pastureland at 5.65 million acres. By comparison, 687,000 acres moved from cropland into developed land (roughly the size of Rhode Island).

Cropland also gained acres from other rural uses. The largest source was pastureland, which contributed 4.15 million acres to cropland between 2017 and 2022, followed by 2.11 million acres from land enrolled in the CRP. In other words, the biggest recent exchange was not cropland to development, but cropland and pasture moving back and forth.

Land Access is Also a Control Issue

The land-use data show what acres are used for. The ownership data shows who controls access to farmland. That distinction is important because rented land is a major part of U.S. agriculture, not a small corner of the land market. In 2022, 39% of U.S. agricultural land was rented, roughly consistent with the share seen over the previous five decades. Rented land is especially important for larger operations and for farmers who use leasing as a way to expand without taking on the full cost of land ownership.

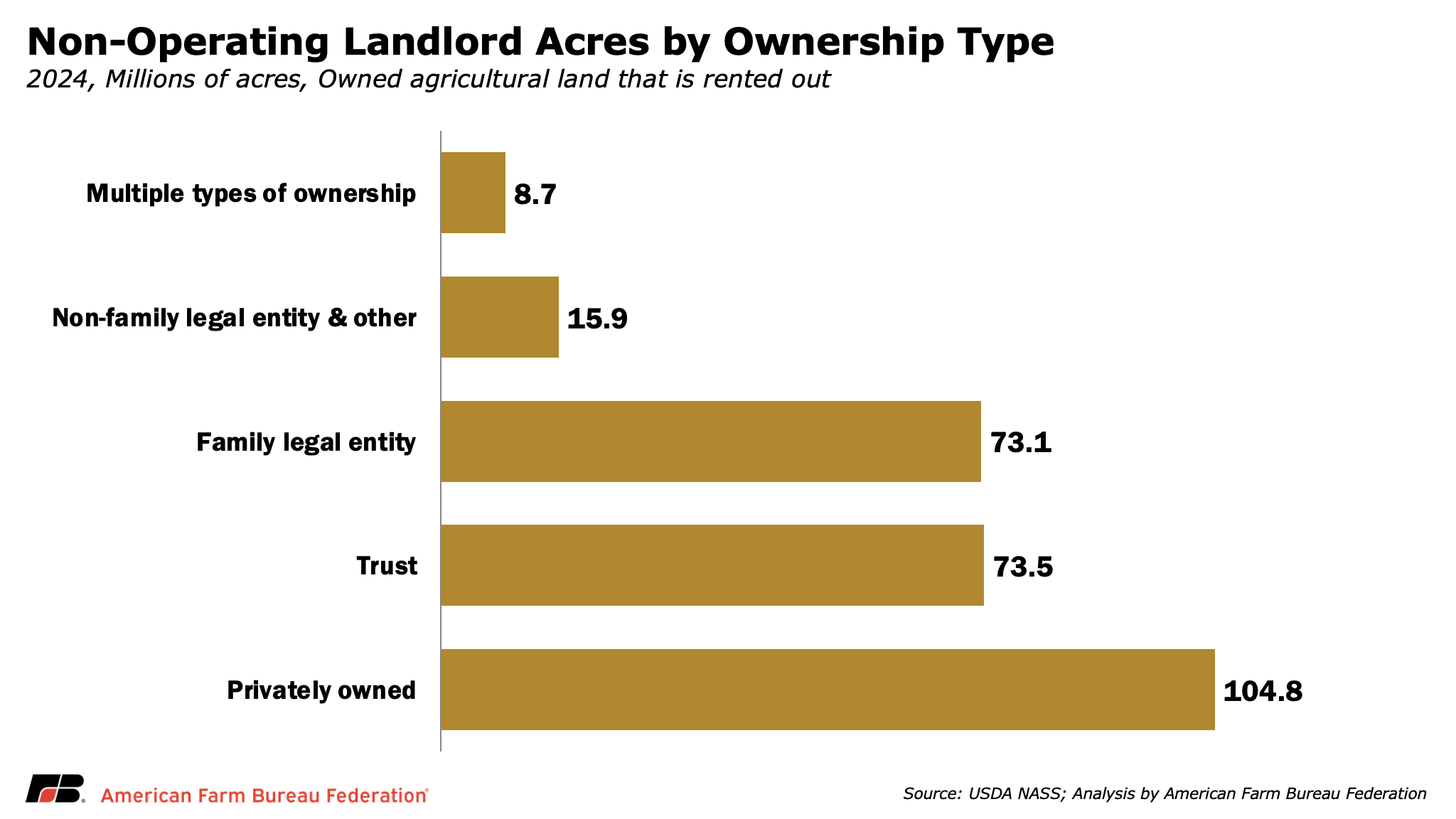

USDA’s 2024 Tenure, Ownership, and Transition of Agricultural Land survey shows how much of that rented land is controlled outside active farm operations. In 2024, more than 2 million landowners rented out 347.8 million acres for agricultural purposes. Cropland accounted for 59% of those rented acres, and non-operating landlords controlled 276.1 million acres, or nearly four out of every five rented acres. In practical terms, a large share of the land farmers operate depends on decisions made by landlords who are not actively farming that ground.

Those decisions are shaped by how land is owned. Among non-operating landlords, privately owned land accounted for 104.8 million rented acres, while trusts and family legal entities accounted for another 146.6 million acres combined. That ownership structure matters for access because the decision to keep land rented, sell it, place it in a trust, pass it through a will or consider non-farm offers often sits outside the farm operator’s control.

More than a third of non-operating landlords were 75 or older, and that group controlled over 40% of rented acres held by non-operating landlords. At the same time, less than 5% of owned farmland is expected to transition through sales or gifts in the next five years. Larger shares are tied to estate planning, with 10% expected to be placed in a trust and 15% written into a will.

For farmers and ranchers, the land question increasingly comes down to continuity. Land can remain agricultural but become harder to access if heirs choose different lease terms, ownership shifts into a trust, or competing offers from development, energy or other non-farm uses raise the opportunity cost of keeping land in production. The generational handoff underway may not place a large share of farmland on the market, but it will shape who can rent, buy and keep working agricultural land.

Local Pressures Reshape Land Competition

National acreage totals can make emerging land pressures look small, but farmers and ranchers experience land competition locally. A solar project, data center, subdivision or outside investment may represent a small share of U.S. agricultural land, but it can have a much larger effect in a specific county, irrigation district or production region where land, water, power and road infrastructure are limited.

Solar facilities are not tracked as a separate NRI land-use category, but utility-scale projects can create long-term competition for farmland in areas with strong transmission access. Data centers bring similar tradeoffs, offering tax base and infrastructure investment while competing for land, power and water. Foreign ownership remains a small share of the national agricultural land base, but recent increases have been tied in part to renewable energy-related acquisitions. High land values add another layer by increasing the opportunity cost of keeping land in production.

Conclusion

The U.S. is not facing an immediate farmland cliff, and recent cropland movement shows that many acres continue to shift among crop, pasture and conservation uses. But those shifts are not the same as development. Once land moves into housing, industrial sites, roads, energy infrastructure or other built uses, future agricultural use becomes far less likely.

That distinction is increasingly important as land competition intensifies. Development, solar projects, data centers, high land values and ownership transitions do not affect every acre equally, but they can quickly reshape local land markets where farmers are already competing for limited ground. For farmers operating on rented land, those pressures are even more significant because access often depends on decisions made by landlords, heirs, trusts or entities outside the farm operation.

The long-term challenge is not just preserving acreage on paper. It is maintaining a land base that can actually support production. As agriculture faces rising costs, tighter margins and increasing competition from non-farm uses, land-use decisions made today will shape whether the next generation of farmers and ranchers can enter, expand and keep working the land needed to support the U.S. farm economy.

Top Issues

VIEW ALL