Prospective Plantings Report Provides First Look at Acreage Intentions

Economist

Vice President of Public Policy and Economic Analysis

Faith Parum, Ph.D.

Economist

John Newton, Ph.D.

Vice President of Public Policy and Economic Analysis

Key Takeaways

- Corn acreage declines from 2025 highs

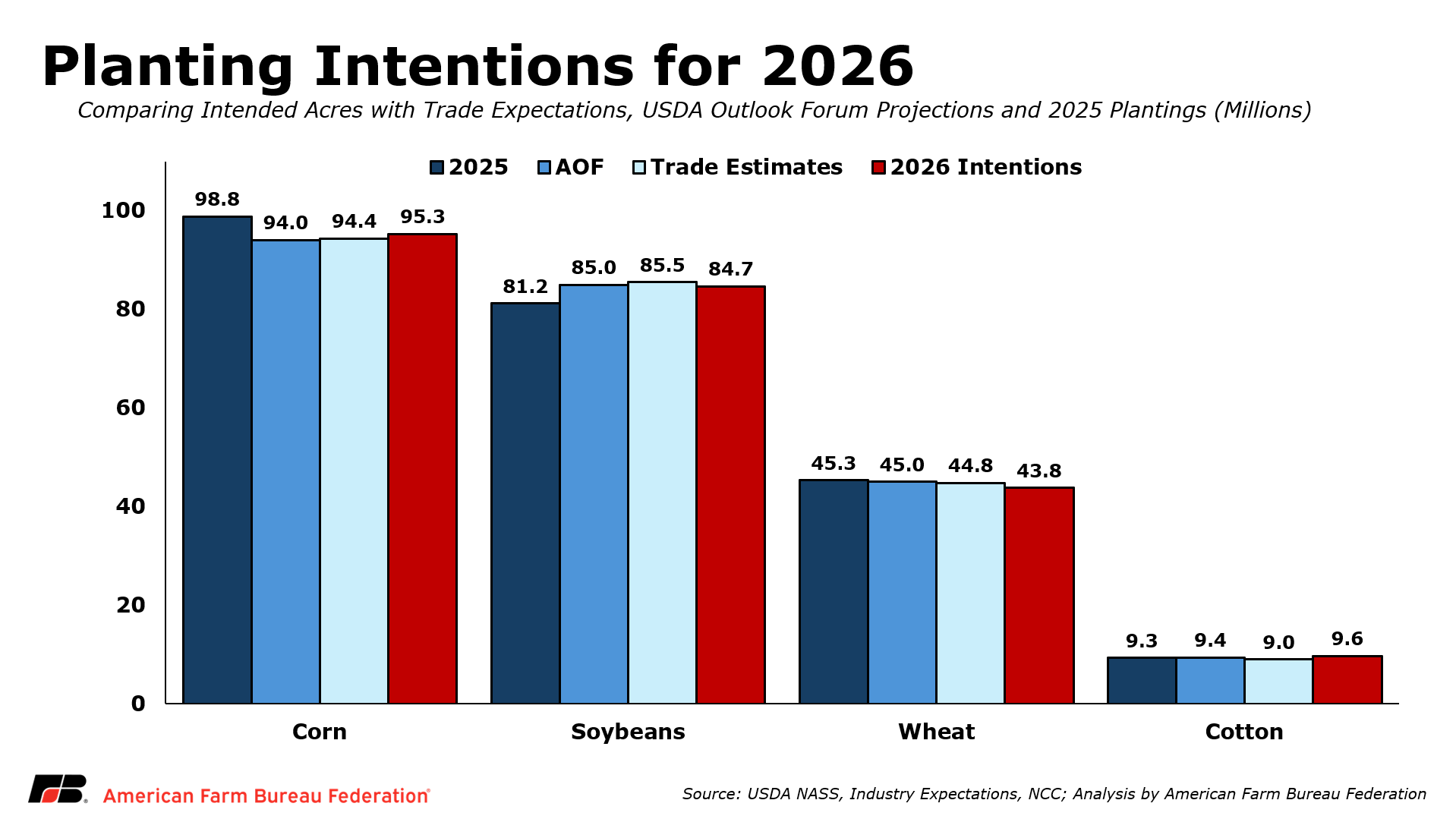

Farmers intend to plant 95.3 million acres of corn in 2026, down 3% from last year’s elevated levels, reflecting tighter margins and higher fertilizer costs.

- Soybean acreage expands modestly

Soybean plantings are expected to reach 84.7 million acres, up 4% year over year, supported by lower nitrogen requirements, strong domestic crush demand and crop rotation following large corn acreage in 2025.

- Market uncertainty could still shift final acreage decisions

Planting intentions were surveyed in early March, and ongoing volatility in fertilizer markets, evolving export demand, particularly from China, and spring weather conditions may influence how acres are ultimately allocated.

USDA’s much-anticipated Prospective Plantings report, released on March 31, reveals farmers’ intentions for planted acreage for principal crops in 2026. Based on farmer responses to a survey conducted during the first two weeks of March, the report provides the first glimpse into how farmers are likely to allocate acres across major crops. Particular attention is on corn and soybean acreage this year after recent disruptions in fertilizer prices and availability following the closure of the Strait of Hormuz on March 2. However, planting intentions may still shift in the weeks ahead as farmers continue to monitor fertilizer markets, weather conditions and evolving price signals.

Ahead of USDA’s Prospective Plantings report, early acreage expectations from both USDA’s Agricultural Outlook Forum and private trade estimates pointed to a shift in planting intentions away from corn and toward soybeans. At USDA’s February 2026 Agricultural Outlook Forum (AOF), the department estimated farmers would plant 94 million acres of corn and 85 million acres of soybeans in 2026. Ahead of the Prospective Plantings report, trade expectations were similar but pointed to a modest shift away from corn and toward soybeans. Analysts surveyed by Reuters projected corn plantings at 94.4 million acres, soybeans at 85.5 million acres and wheat at 44.8 million acres. If realized, that would represent a decline of more than 4 million corn acres and an increase of over 4 million soybean acres compared to 2025, reflecting weaker corn returns and higher fertilizer costs heading into planting season. Wheat acres would be down 1.5 million acres if trade estimates were realized. A survey by the National Cotton Council expects farmers to plant 9 million acres in 2026, which would be down 400,000 acres if realized.

The Prospective Plantings survey results revealed farmers intend to plant 95.3 million acres of corn, down 3% from 2025, and 84.7 million acres of soybeans, up 4% from last year. For corn, USDA’s acreage estimate was below prior-year levels, but above USDA’s February AOF projections and above the average trade estimate. For soybeans, USDA’s estimate was above prior-year levels, but below USDA’s February AOF forecast and below the average trade estimate. All wheat planted area is estimated at 43.8 million acres, down 3% year over year and the lowest level on record since 1919. This estimate is below both trade expectations and USDA’s February AOF forecast. All cotton planted area is estimated at 9.64 million acres, up 4% from 2025 and above both USDA’s February AOF estimate and trade expectations.

Corn

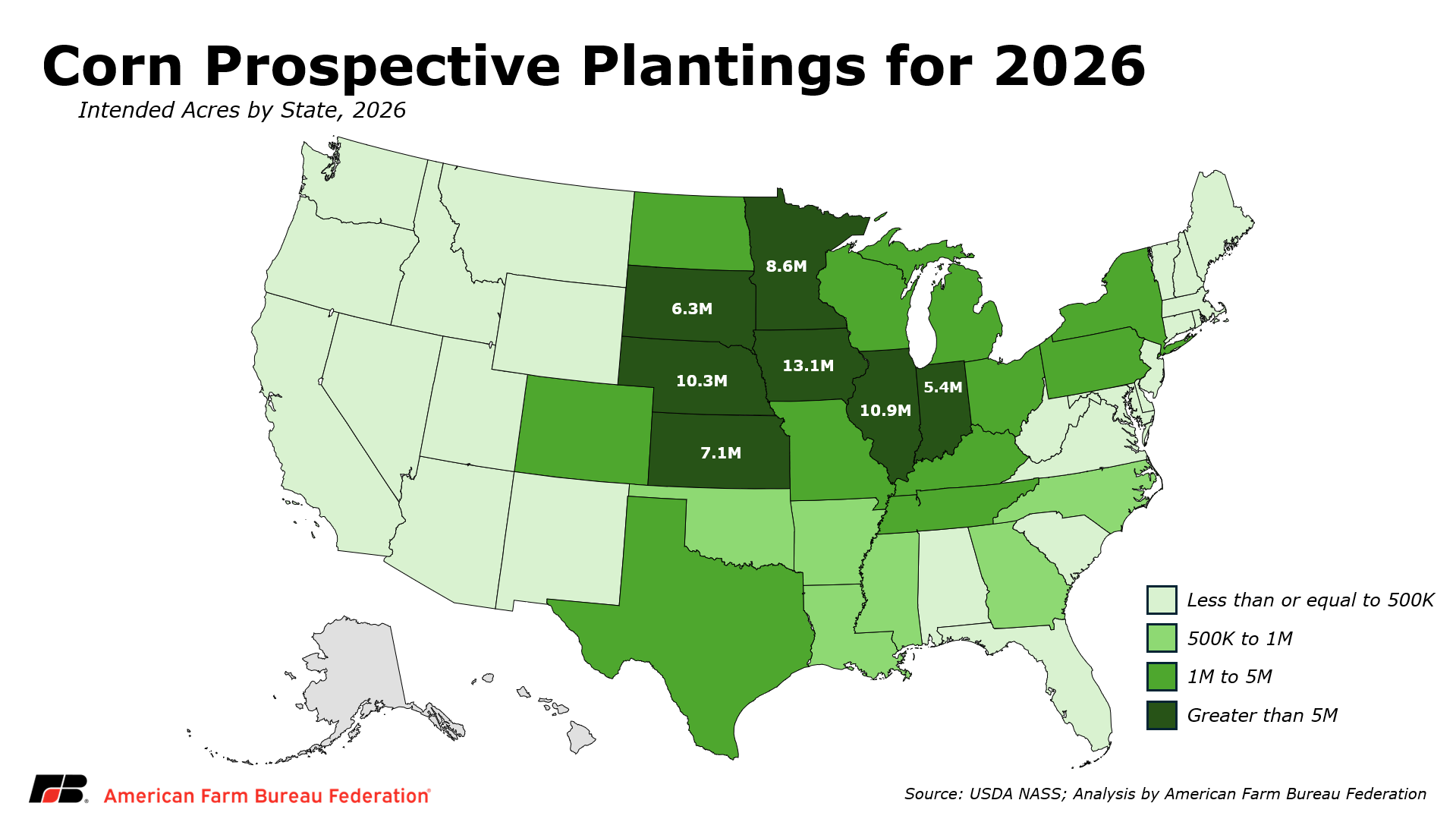

For the 2026/27 marketing year, U.S. producers intend to plant 95.3 million acres of corn, down 3%, or 3.45 million acres, from the prior year. Corn acreage is expected to be highest in Iowa at 13.1 million acres, followed by Illinois at 10.9 million acres and Nebraska at 10.3 million acres.

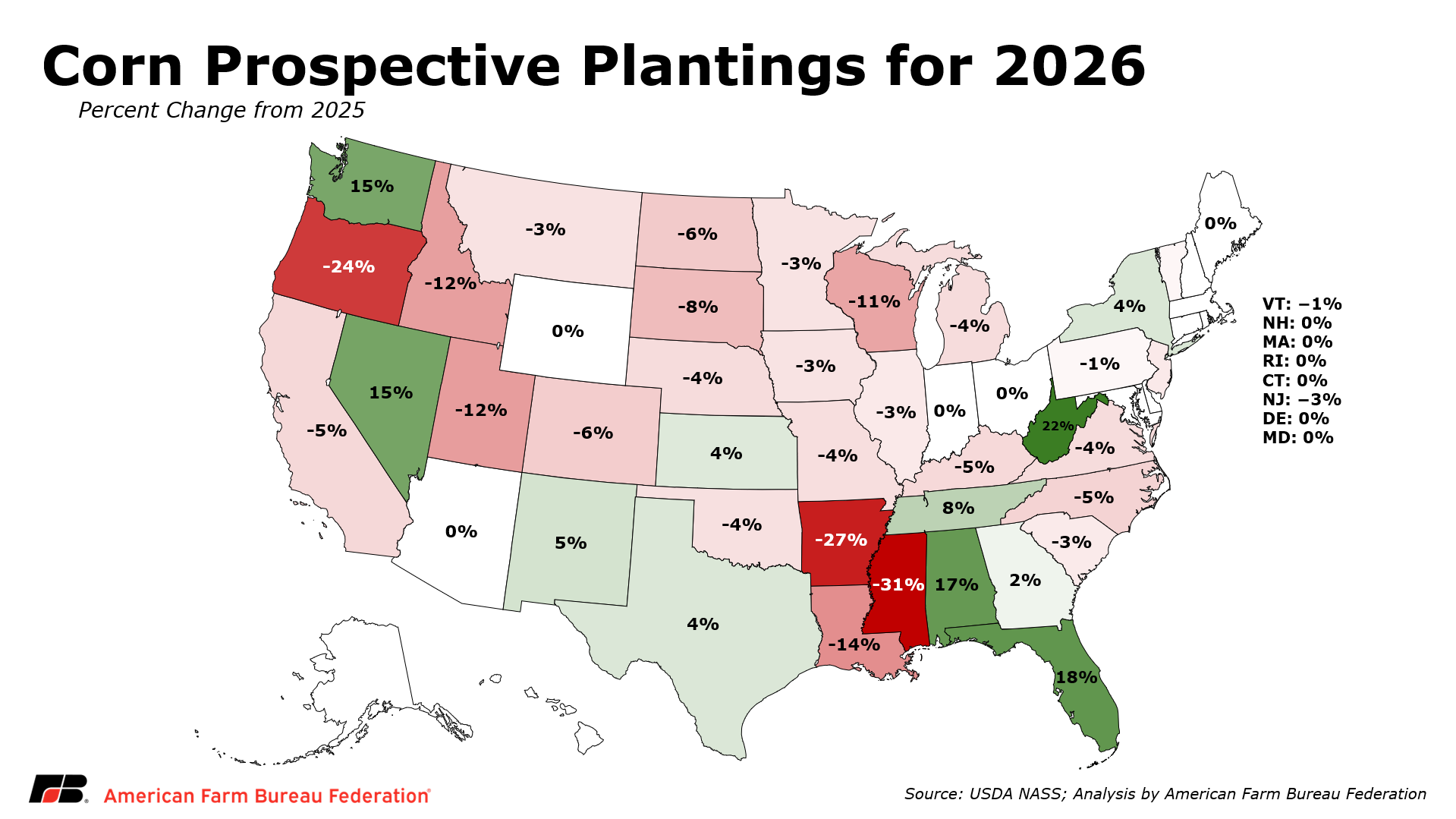

Compared with last year, planted corn acreage is expected to be down or unchanged in 37 of the 48 estimating states. The largest acreage decline occurred in South Dakota, where growers intend to plant 550,000 fewer acres, an 8% decrease. The largest acreage increase occurred in Kansas, where farmers plan to plant 250,000 additional acres, a 4% increase. In percentage terms, the largest decline occurred in Mississippi, where planted area is expected to fall by 31% (-280,000 acres), while the largest increase occurred in West Virginia, where acreage is projected to rise by 22% (+9,000 acres). Several Midwest states show modest corn acreage reductions consistent with expectations for some shift toward soybeans.

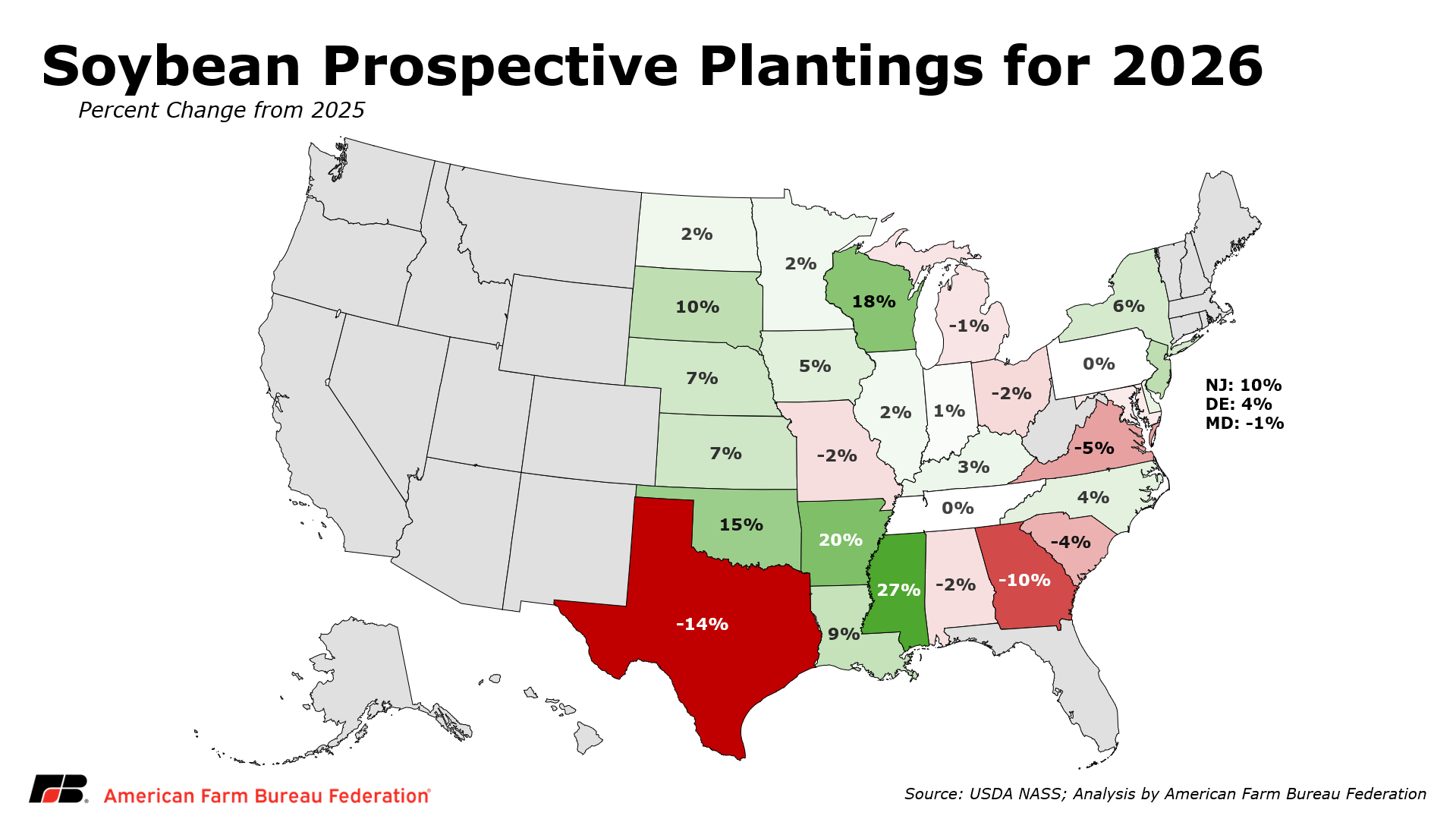

Soybeans

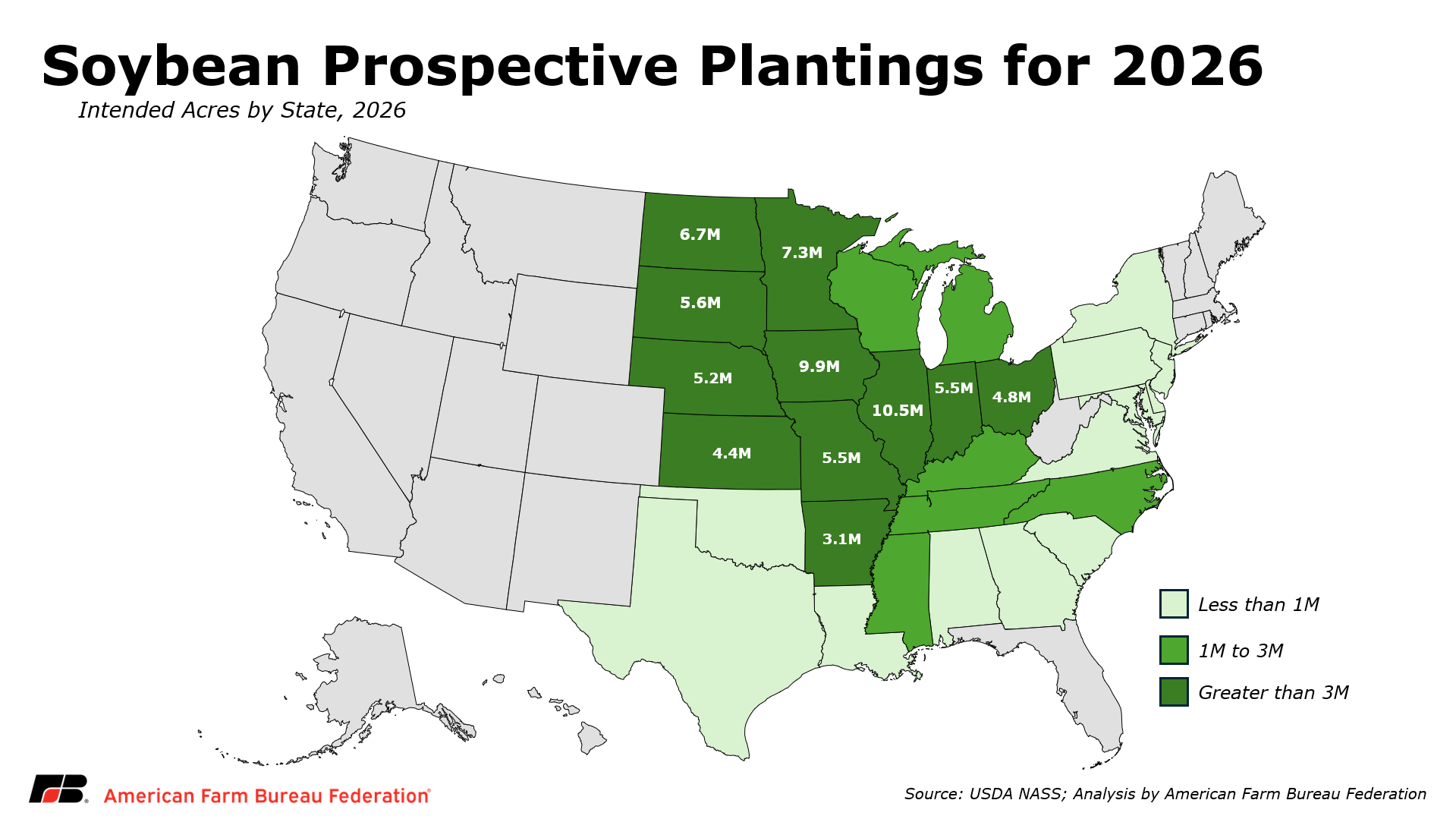

For the 2026/27 marketing year, U.S. producers intend to plant 84.7 million acres of soybeans, up 4%, or 3.49 million acres, from the prior year. Soybean acreage is expected to be highest in Illinois at 10.5 million acres, followed by Iowa at 9.9 million acres and Minnesota at 7.3 million acres.

Compared with last year, planted soybean acreage is expected to be up or unchanged in 20 of the 29 estimating states. The largest change in planted acreage occurred in Arkansas, where growers intend to plant 510,000 additional acres (+20%) of soybeans. In percentage terms, Michigan farmers plan to increase soybean acreage by 27% (+490,000 acres), while Texas farmers plan to decrease soybean acreage by 14% (-15,000 acres).

Trade Tensions & Global Conflict

Several additional factors could influence how acreage ultimately shifts between corn and soybeans this spring. Ongoing conflict involving Iran has increased volatility in global fertilizer markets, particularly nitrogen supplies, as countries exposed to disruptions in and around the Persian Gulf account for roughly 49% of global urea exports and about 30% of ammonia exports. Because corn is significantly more fertilizer-intensive, particularly for nitrogen, rising fertilizer costs tend to weigh more heavily on corn than soybeans, which require comparatively less applied nitrogen. As a result, higher input costs may encourage some growers to shift acres toward soybeans at the margin.

At the same time, soybeans in storage are increasing, with 2.10 billion bushels in storage as of March 1, up 10% from a year earlier, including 900 million bushels stored on farms and 1.20 billion bushels stored off-farm. Reduced export demand could place additional pressure on storage levels, particularly as China continues to account for roughly half of U.S. soybean export demand but recent purchases have remained uneven, creating additional uncertainty around soybean market incentives heading into the growing season.

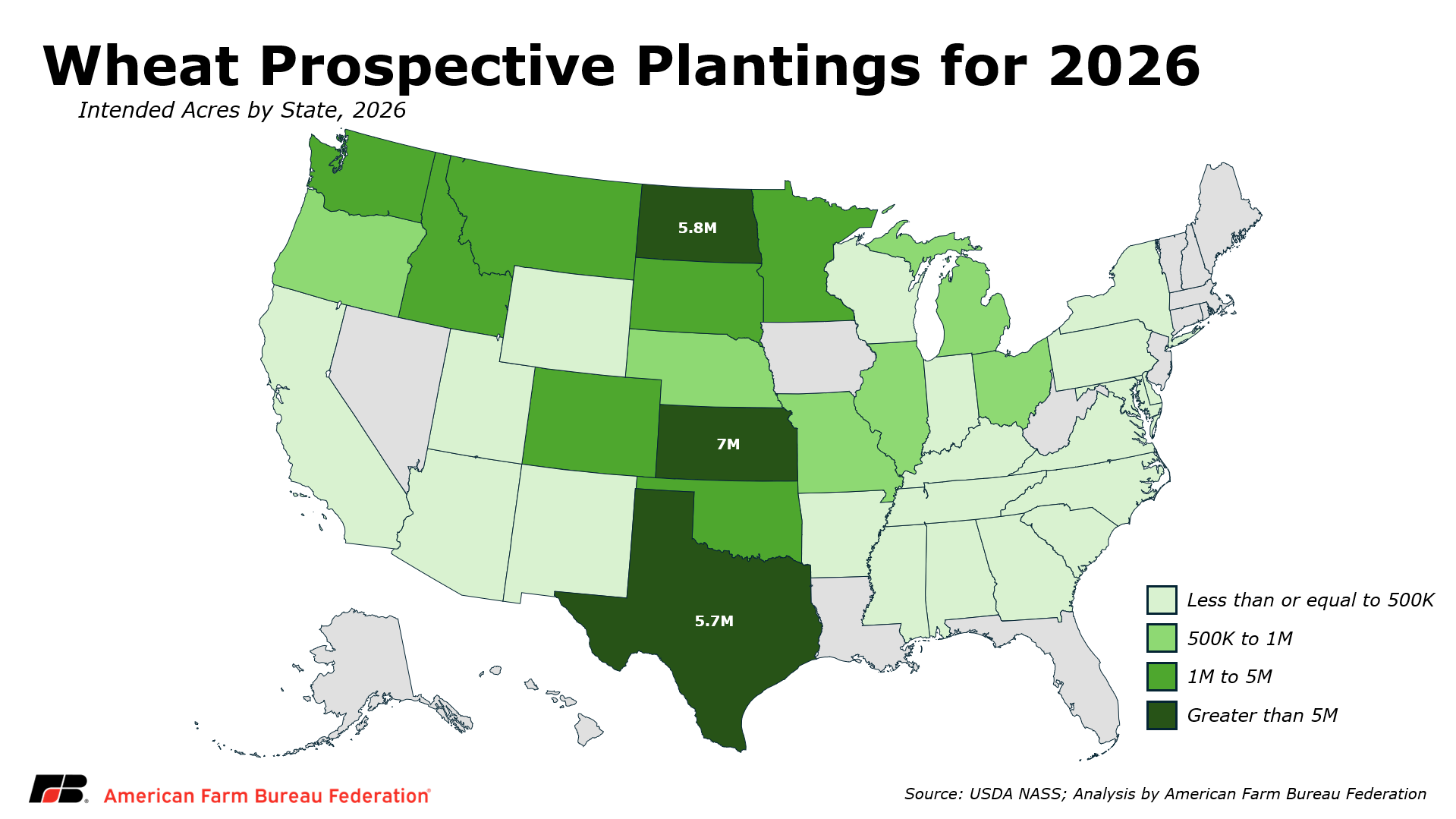

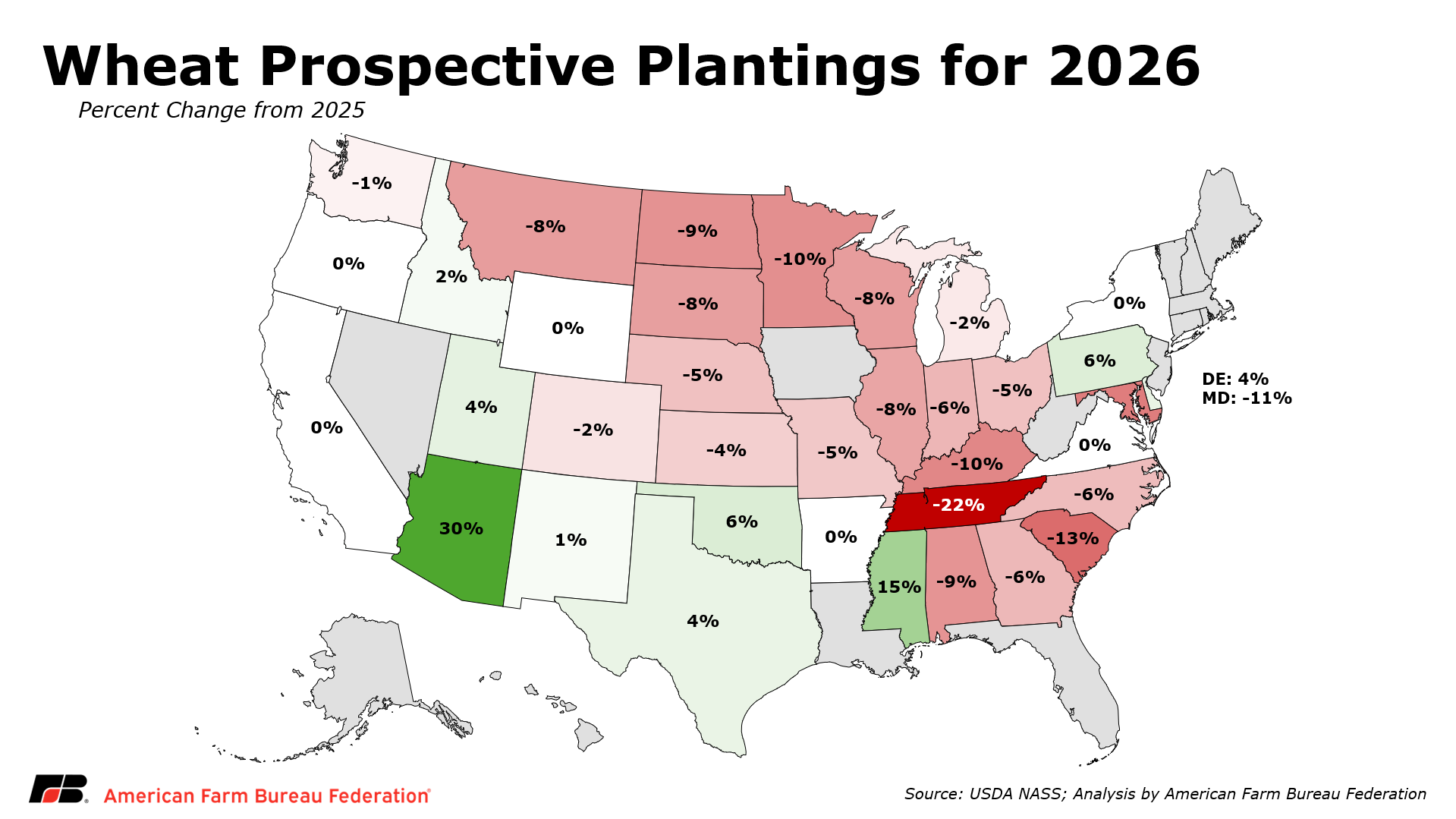

Wheat

For the 2026/27 marketing year, U.S. producers intend to plant 43.8 million acres of wheat, down 3%, or 1.53 million acres, from the prior year. Wheat acreage is expected to be highest in Kansas at 7 million acres, followed by North Dakota at 5.84 million acres and Texas at 5.7 million acres.

Compared with last year, planted wheat acreage is expected to be down or unchanged in 30 of the 37 estimating states. The largest change in intended planted acreage occurred in North Dakota, where growers intend to plant 595,000 fewer acres of wheat. In percentage terms, Arizona farmers plan to increase wheat acreage by 30% (+15,000 acres), while Tennessee farmers plan to decrease wheat acreage by 22% (-75,000 acres).

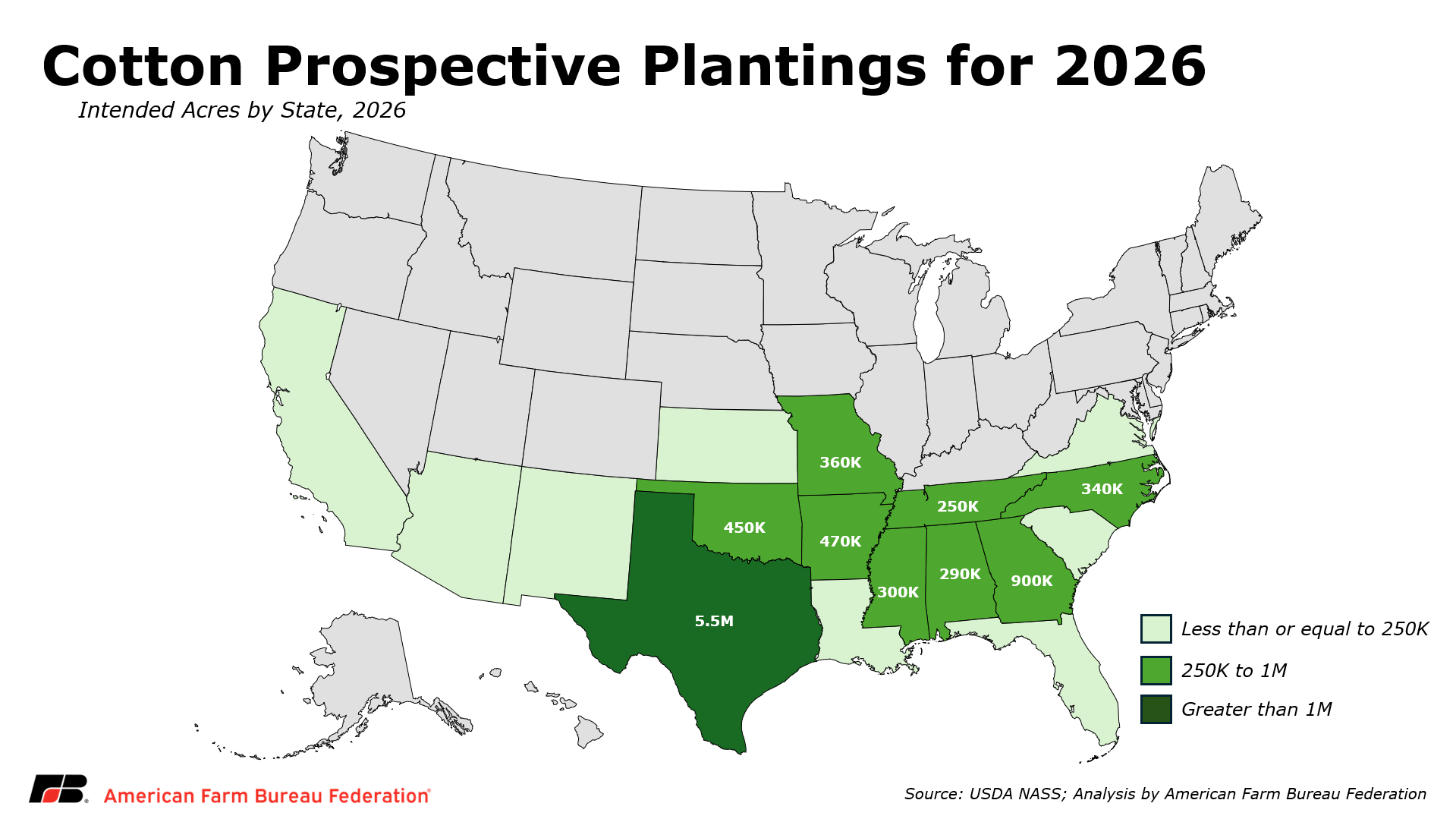

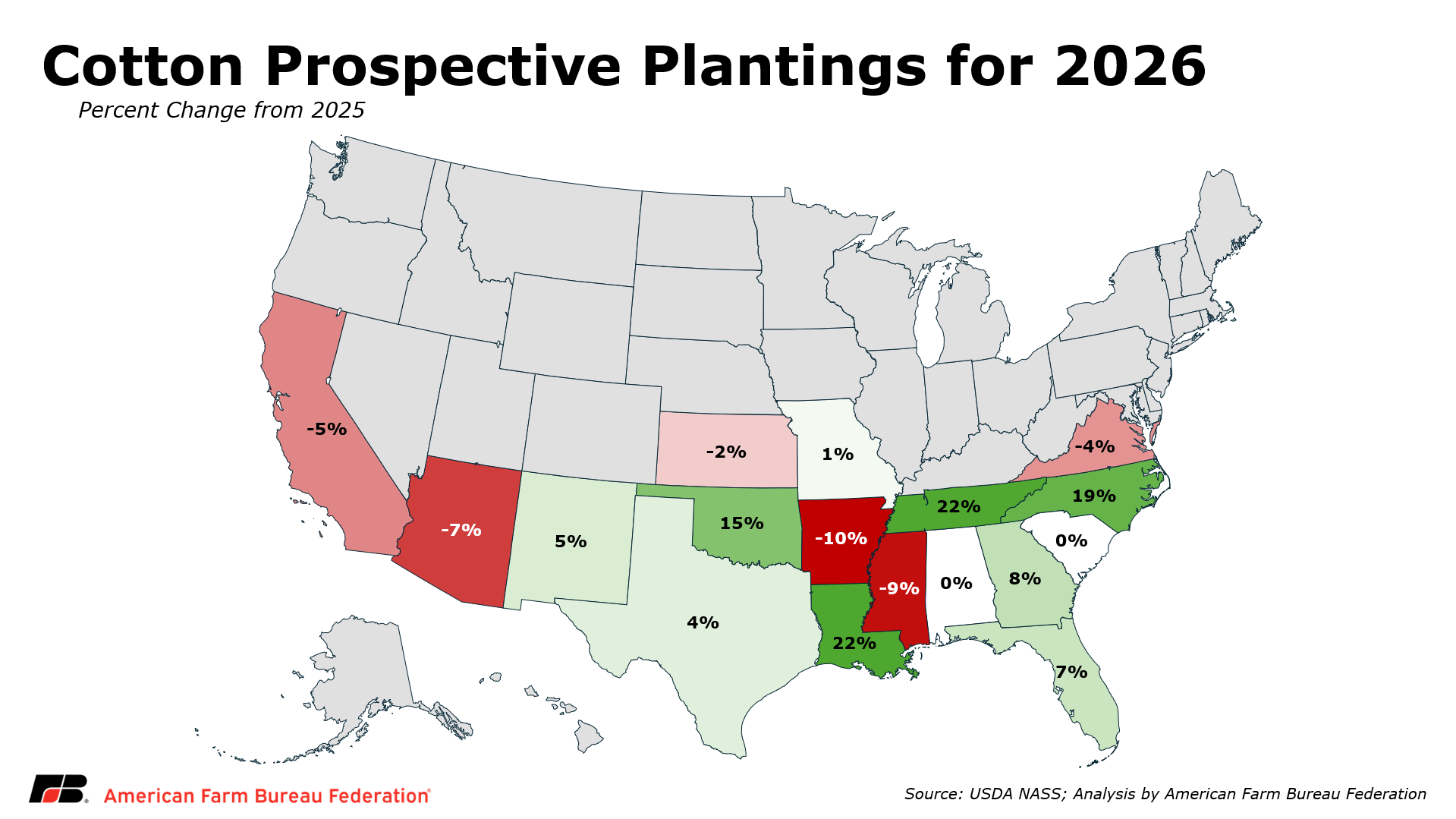

Cotton

For the 2026/27 marketing year, U.S. producers intend to plant 9.64 million acres of cotton, up 4%, or 0.36 million acres, from the prior year. Cotton acreage is expected to be highest in Texas at 5.52 million acres, followed by Georgia at 0.90 million acres and Arkansas at 0.47 million acres.

Compared with last year, planted cotton acreage is expected to be up or unchanged in eight of the 15 estimating states. The largest change in intended planted acreage occurred in Texas, where growers intend to plant 199,000 additional acres of cotton in 2026. In percentage terms, Arkansas farmers plan to decrease cotton acreage by 10%, or 50,000 fewer acres, in 2026.

What to Watch Next

USDA’s Prospective Plantings report provides the first survey-based estimate of acreage for the upcoming crop year, but several factors could still influence final planting decisions. Continued expansion in domestic soybean crush capacity has supported expectations for increased soybean acreage in 2026, with farmers indicating plans to plant 84.7 million acres, up 4% (3.49 million acres) from 2025. Large corn plantings last year (98.8 million acres in 2025) also reduce rotation incentives for another corn year in some regions, while higher and more volatile fertilizer costs further favor soybeans, which require fewer nitrogen inputs than corn.

Trade conditions will also remain important to monitor. The 2025 U.S.–China agricultural trade agreement helped stabilize expectations for export demand, but the pace of purchases and broader trade policy developments will continue to influence soybean acreage incentives.

As planting progresses this spring, changes in weather, input costs and market conditions may still lead farmers to adjust how acres are ultimately allocated across crops. Given these uncertainties, markets will now turn their attention to planting progress, early-season weather conditions and export demand signals. The next major opportunities to update crop balance sheets will come with USDA’s May World Agricultural Supply and Demand Estimates (WASDE) report, followed by the June 30 Acreage report.

Top Issues

VIEW ALL