Why Domestic Capacity Matters for U.S. Agriculture

Faith Parum, Ph.D.

Economist

Key Takeaways

- Domestic processing capacity supports farm demand and rural economies. When commodities are processed in the United States, more of the food dollar stays in the domestic economy — supporting rural jobs, strengthening local markets for farmers and anchoring economic activity in agricultural communities.

- Loss of capacity increases export reliance and vulnerability. As processing and manufacturing shift overseas, farmers become more dependent on global markets to absorb production, exposing both farm income and rural economies to trade disruptions, geopolitical risks and supply chain shocks.

- Once capacity leaves, it is difficult to rebuild. Processing facilities require large capital investments, skilled labor and established supply chains. When plants close, rural communities lose major employers and rebuilding that infrastructure can take decades.

American agriculture is among the most productive sectors in the world. Advances in plant and animal genetics, mechanization and precision agriculture have driven remarkable yield gains. Corn yields have risen from 38 bushels per acre in 1950 to about 187 today, nearly a fivefold increase, while soybean yields have more than doubled. Yet, productivity alone does not determine farm profitability.

Agricultural commodities must move through processors, manufacturers and retailers before they generate income for farmers. Where that processing occurs determines where the economic value accumulates. Oilseeds become cooking oils and renewable fuels. Grains become ethanol and animal feed. Cotton becomes textiles and apparel. When these activities occur domestically, the value created supports American businesses, workers and rural communities. When processing moves overseas, that value moves with it.

On March 10, American Farm Bureau Federation President Zippy Duvall testified before the Senate Committee on Agriculture, Nutrition and Forestry on the importance of rebuilding domestic demand and maintaining a resilient agricultural supply chain. This Market Intel highlights several sectors where the erosion of domestic processing capacity has reshaped how farmers market their crops and where they absorb risk.

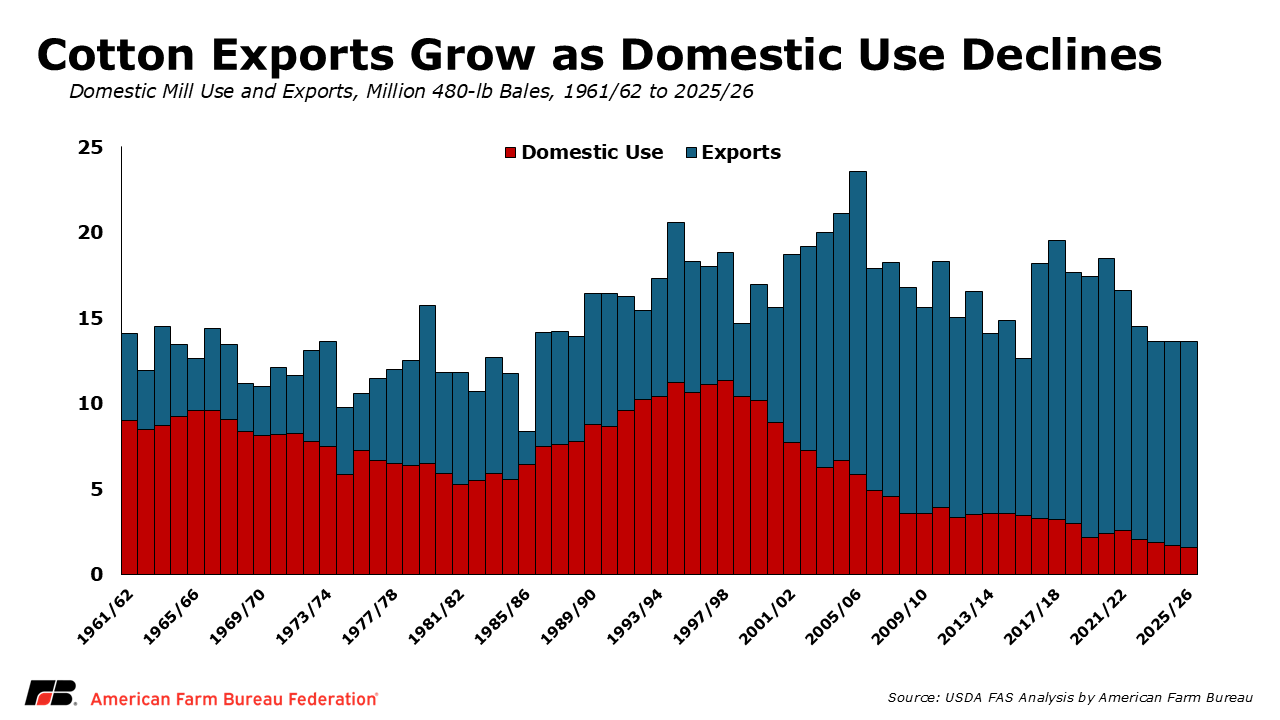

Cotton: Export Reliance Following the Loss of Domestic Textile Manufacturing

Cotton offers one of the clearest examples of how the loss of downstream manufacturing can reshape an agricultural market.

U.S. textile mills were a reliable buyer of domestic cotton through much of the 20th century, with domestic mill use peaking at roughly 11.3 million bales in the 1997/98 marketing year. That relationship eroded as apparel manufacturing shifted to lower-cost regions abroad. Today, domestic mill use stands at roughly 1.6 million bales, the lowest level in recent history.

Exports now absorb the vast majority of U.S. production. Over the past decade, the United States exported about 85% of the cotton it produced, making cotton one of the most export-dependent major U.S. crops.

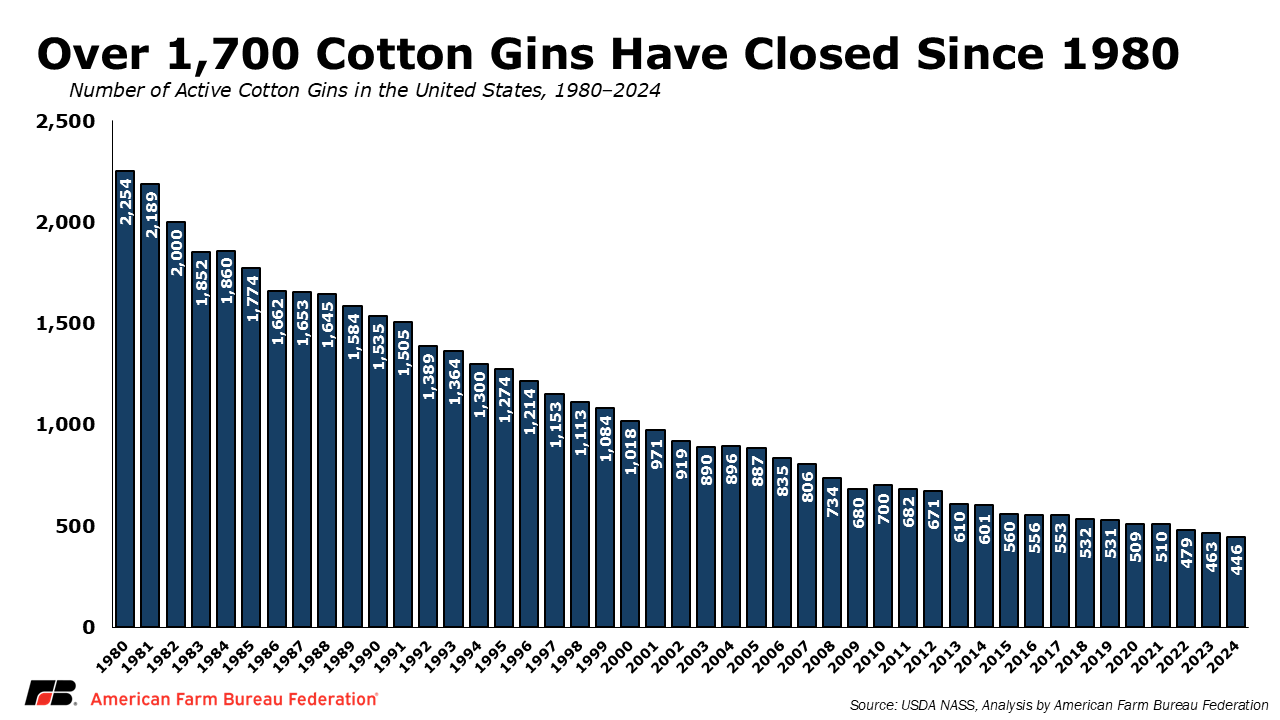

The infrastructure supporting cotton production has contracted alongside domestic demand. Active cotton gins numbered 2,254 in 1980 and have fallen to roughly 500 today. Some consolidation reflects efficiency gains, as remaining gins process far more bales, but the broader trend mirrors the erosion of domestic textile capacity.

The result is a familiar pattern: raw cotton is exported, manufactured abroad and imported back into the United States as clothing, fabric or household goods. Manufacturing value is created overseas rather than within domestic supply chains. For producers, this means export markets must absorb nearly all production. When global demand weakens or trade disruptions occur, there is little domestic cushion.

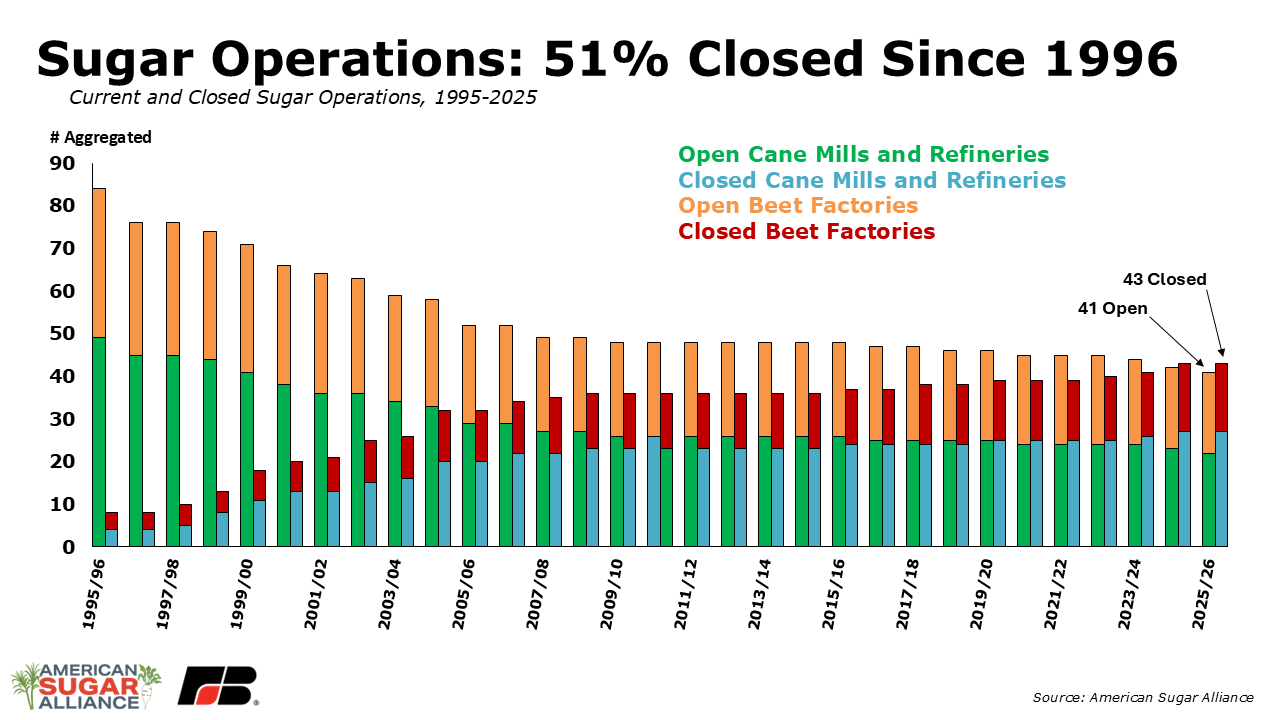

Sugar: Processing Infrastructure Shapes Production

The sugar industry illustrates how processing infrastructure can shape regional agricultural production. Sugarbeets and sugarcane must be processed quickly after harvest to maximize sugar extraction from the harvested plants, tying production closely to nearby processing facilities. Those facilities require large capital investments each year for maintenance and depend on consistent throughput to operate efficiently.

Over time, low prices and high costs have led to numerous processing facility closures, reducing the number of sugar processing plants. Due to the high risk and low returns to sugar processing, many investors exited and growers were forced, in many cases, to purchase facilities to keep them in operation. Nevertheless, from 1995 to 2026, 43 sugar processing facilities have closed, leaving 41 still open, and some regions have experienced particularly sharp contractions. California, for example, lost all of its beet sugar facilities over several decades. Its final remaining processing facility closed following the 2025 crop. This follows similar trends in other states; the last sugarcane mill in Hawaii closed in 2016 and in Texas in 2024.

Because sugarbeets and sugarcane cannot be transported long distances economically without loss of sugar content, growers depend heavily on nearby processing facilities. When a processing facility closes, production in that region disappears as well, eliminating an important economic engine for those communities. Once a processing hub shuts down, farmers must pivot to other crops as refurbishing a closed facility or building a new one is simply not supported by processing margins today.

Rice: Farm Consolidation and Export Dependence

Rice illustrates a different kind of structural pressure in U.S. agriculture: a growing dependence on export markets combined with intensifying global competition. The number of U.S. rice farms declined sharply from 9,627 in 1997 to just 3,824 in 2024, while average farm size expanded significantly as producers adopted new technologies and pursued economies of scale. This consolidation has not been optional, it has been essential for survival. Larger operations are better positioned to absorb volatile prices, rising input costs and global competition.

The U.S. exports roughly 40% to 50% of its rice crop in most years, making international demand a central driver of farm income. But that reliance leaves producers exposed to foreign government policies and shifting trade dynamics. One major source of pressure is India, which has become the world’s largest rice exporter in part due to extensive government support. India’s system of minimum support prices, input subsidies and public stockholding programs effectively lowers production costs and enables exporters to sell rice on global markets at artificially low prices — policies that the United States and others argue distort trade and violate World Trade Organization rules.

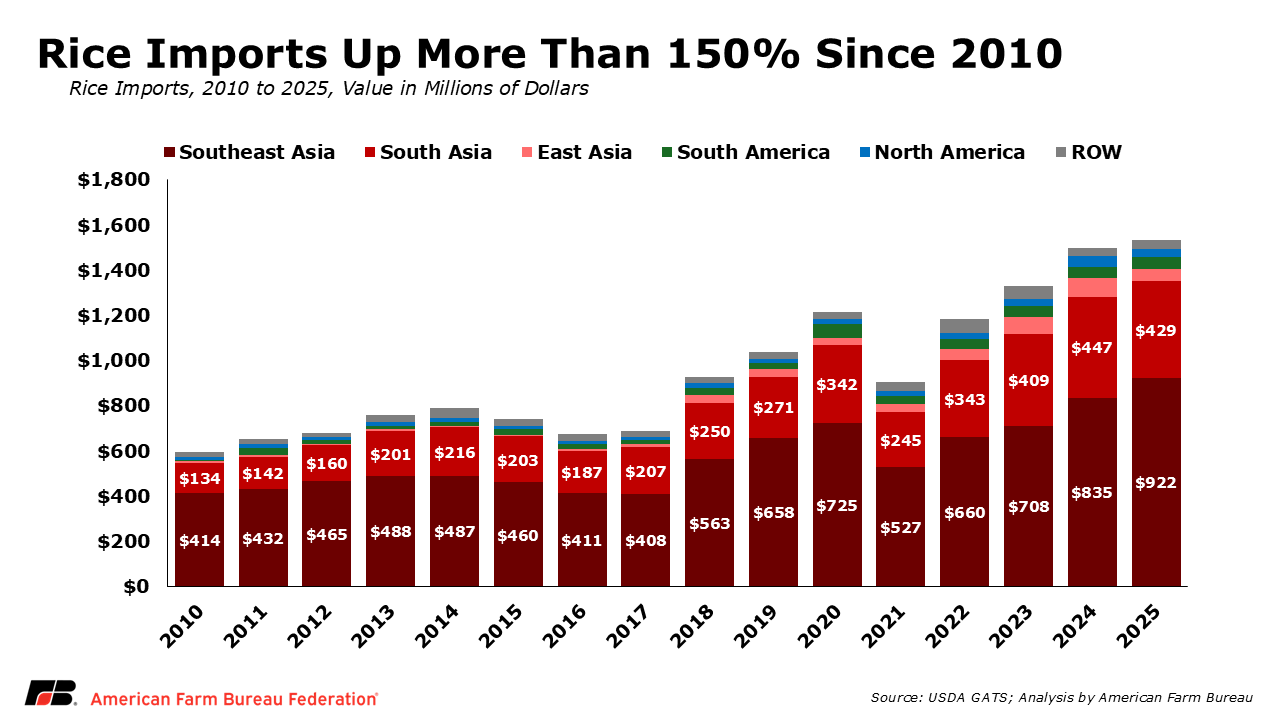

At the same time, U.S. rice imports have surged more than 150% since 2010, reaching about $1.5 billion in 2025. Much of this growth is driven by shipments from Southeast and South Asia, where lower labor costs and government support programs enhance competitiveness. Meanwhile, South American exporters — particularly Brazil and Uruguay — have expanded production and improved logistics, further intensifying competition in key export markets.

Taken together, these forces have reshaped the U.S. rice sector. Consolidation has helped maintain overall production, but it has also concentrated risk: fewer, larger farms are now more deeply tied to volatile global markets. As a result, U.S. rice farmers are increasingly dependent not just on yields and efficiency, but on trade policy, international subsidies and access to foreign markets to remain viable.

Corn and Soybeans: What Investment Looks Like When Demand Is Stable

The recent expansion in soybean crushing capacity shows how quickly processing investment can respond when domestic demand grows. According to the National Oilseed Processors Association feedstock study, oilseed processing capacity in the United States has increased by more than 25% since 2021, representing billions of dollars in new investment in crushing and processing facilities driven largely by growing biofuel demand.

Corn provides a similar example. Ethanol production now consumes roughly 5.6 billion bushels of corn annually, creating one of the largest domestic markets for U.S. farmers. Policies that expand biofuel use can strengthen this demand. Allowing year-round sales of E15 gasoline, for example, would provide a stable outlet for additional corn production while supporting domestic fuel supply. Year-round E15 could increase demand for corn by 2.4 billion bushels a year.

Further investment in domestic processing efficiencies and new crush facilities could support production of an additional 1.4 billion gallons of biofuels. However, continued growth in these markets will depend on regulatory clarity. Strong Renewable Volume Obligations (RVOs) under the Renewable Fuel Standard and clear implementation guidance for the 45Z Clean Fuel Production Credit will determine how quickly these investments translate into expanded domestic demand for agricultural feedstocks.

Once Processing Capacity Leaves, it is Difficult to Rebuild

Processing infrastructure is difficult to recreate once it disappears. Agricultural processing systems depend on skilled labor, specialized equipment, regulatory approvals and established supply chains. When plants close, those networks often disperse.

Rebuilding that infrastructure can require years, or even decades, of sustained investment. The cotton sector illustrates this challenge clearly. Even though the United States remains one of the world’s largest cotton producers, the textile manufacturing ecosystem that once consumed large volumes of cotton has largely moved overseas. Reestablishing that capacity would require rebuilding an entire industrial network.

A Foundation for Rural Economies

Domestic agricultural processing does more than create demand for farm commodities. It anchors economic activity in rural communities. Processing plants provide jobs, support local supply chains and generate economic activity throughout the agricultural economy. When facilities close, rural communities often lose major employers and economic anchors.

American farmers continue to lead the world in agricultural productivity. Ensuring that this productivity translates into stable markets and resilient rural economies will require maintaining a balance between strong export opportunities and durable domestic demand.

Top Issues

VIEW ALL