Farm Bureau Survey Reveals Real Impact of Fertilizer Availability and Price

Faith Parum, Ph.D.

Economist

Key Takeaways

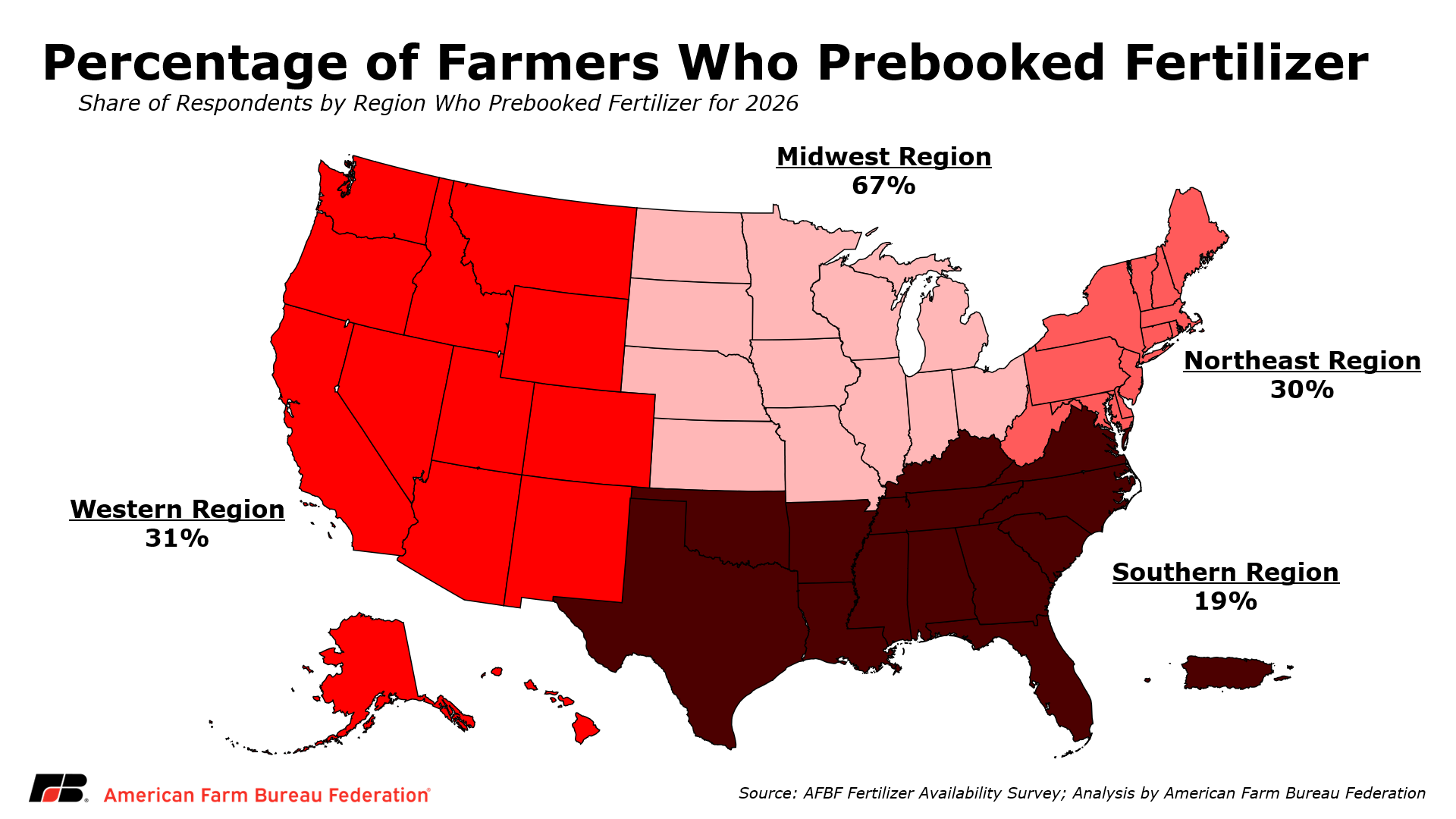

- Fertilizer pre-booking rates varied significantly by region, with just 19% of Southern producers reporting fertilizer purchases secured ahead of the season, compared to 30% in the Northeast, 31% in the West and 67% in the Midwest, reflecting differences in planting decision timelines and exposure to recent price increases.

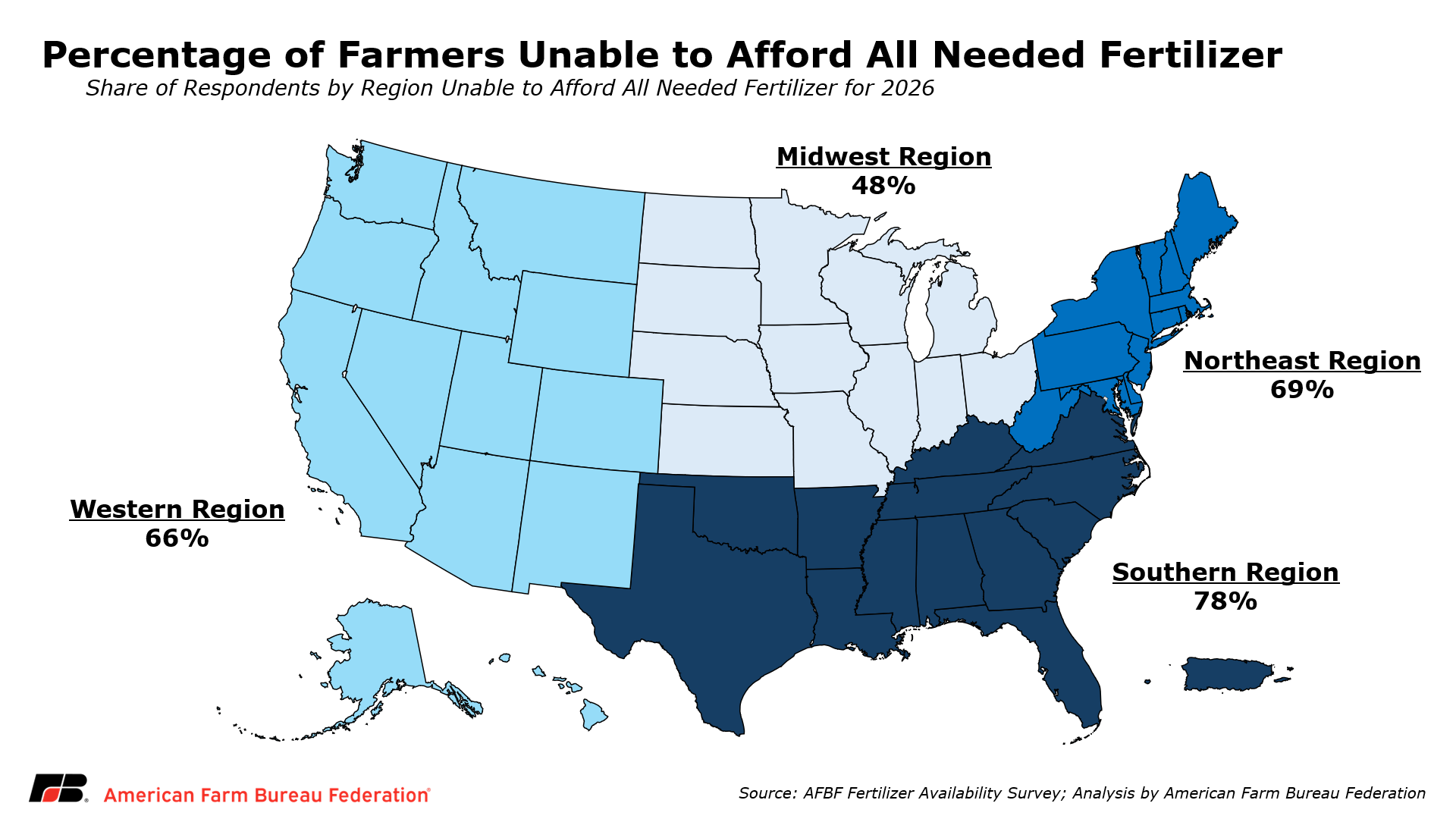

- Fertilizer affordability challenges are most acute in the South and Northeast but remain a concern for farmers across all regions. Around 70% of respondents report being unable to afford all the fertilizer they need.

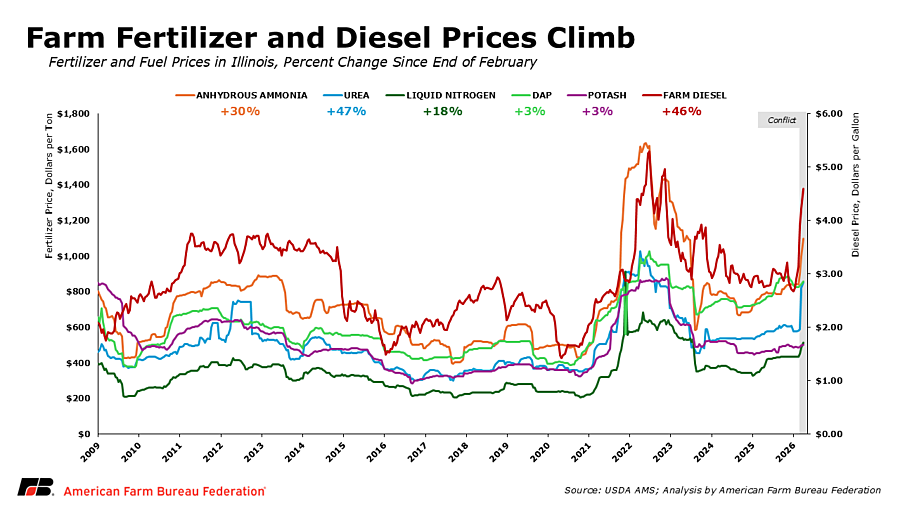

- Farm diesel prices have increased 46% since the end of February, raising costs for fieldwork, fertilizer transport and irrigation during both planting and growing seasons.

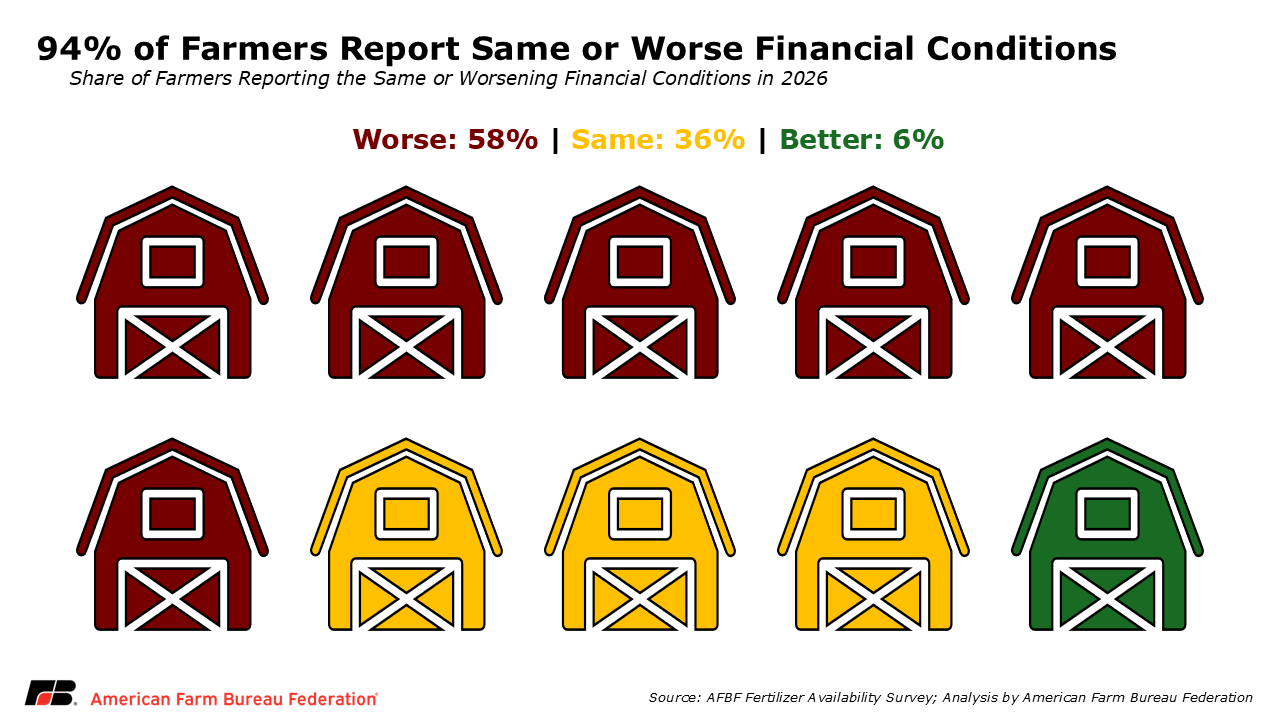

- Nearly six in 10 farmers report worsening finances, reflecting rising fertilizer and fuel costs during spring planting and underscoring the urgent need for immediate economic assistance to keep farms gates open.

Rising input costs tied to the conflict in the Middle East are adding strain to an already challenging farm economy. To better understand how global fertilizer market disruptions are affecting producers during spring planting, the American Farm Bureau Federation conducted a Fertilizer Availability Survey of farmers and ranchers across the country. More than 5,700 farmers responded to the survey, which was conducted April 3 through April 11.

Regional Differences Reflect Crop Mix and Supply Exposure

Survey responses show the closure of the Strait of Hormuz is affecting regions across the United States differently because crop production systems and fertilizer needs vary.

Midwestern producers – often relying on a corn and soybean rotation – reported higher pre-booking rates, with 67% securing fertilizer earlier in the season. Given these crop rotations, pre-booking is more common in the Midwest, where fertilizer needs are typically larger and purchasing decisions are often made well ahead of planting. As a result, a larger share of Midwestern farmers reported being able to secure the inputs they need before recent price increases. Even with higher pre-booking rates, nearly one in three Midwestern farmers still report entering the season without securing all of their fertilizer needs.

In contrast, producers in other regions are more likely to purchase fertilizer closer to application, increasing exposure to in-season price volatility during periods of market disruption. Nineteen percent of southern farmers pre-booked fertilizer this crop year. Southern producers often grow crops such as cotton, rice, soybeans, corn and peanuts that rely heavily on applied nutrients and can be particularly sensitive to changes in fertilizer costs. Pre-booking rates are similarly limited in other regions, with just 30% of farmers in the Northeast and 31% in the West securing fertilizer ahead of the season.

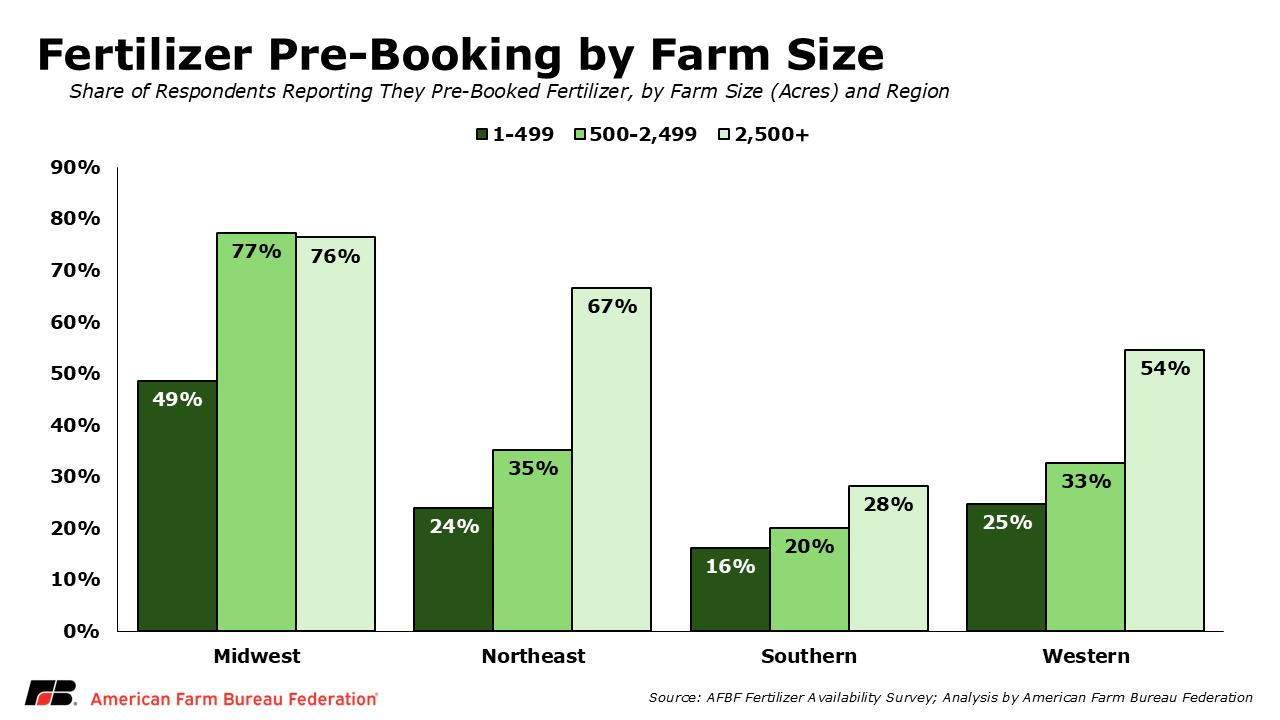

Smaller farms reported substantially lower fertilizer pre-booking rates than larger operations across every region, suggesting greater exposure to recent price volatility during the spring purchasing window. In the Midwest, 49% of farms with 1–499 acres pre-booked fertilizer, compared to 77% of farms with 500–2,499 acres and 76% of farms with 2,500+ acres. The gap was even more pronounced in the Northeast, where only 24% of the smallest farms pre-booked fertilizer, compared to 35% of mid-sized farms and 67% of the largest operations. Similar patterns appeared in the South (16% for 1–499 acres vs. 28% for 2,500+ acres) and West (25% vs. 54%). Because smaller farms are less likely to secure fertilizer ahead of the season, they are more exposed to in-season price increases, which can make it harder to afford full application rates and increase the risk of reduced yields and tighter margins in 2026.

Farmers in the Southern region reported the greatest difficulty securing fertilizer, with 78% unable to afford all needed inputs this season. Producers in the Northeast and West also reported significant challenges, with 69% and 66%, respectively, unable to afford all required fertilizer, compared to 48% in the Midwest. When producers cannot afford full fertilizer application rates, they may reduce nutrient use or shift acreage decisions, both of which increase the risk of lower yields and reduced production potential in the 2026 crop year.

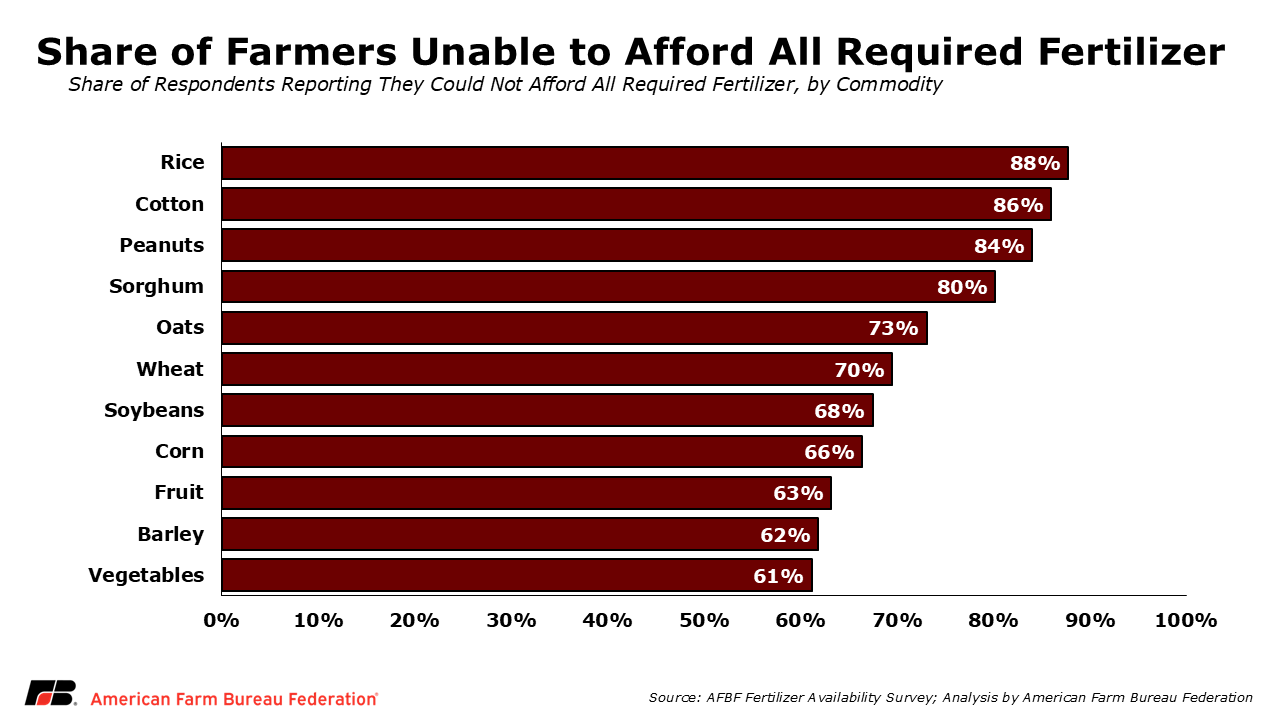

Fertilizer Impact by Commodity

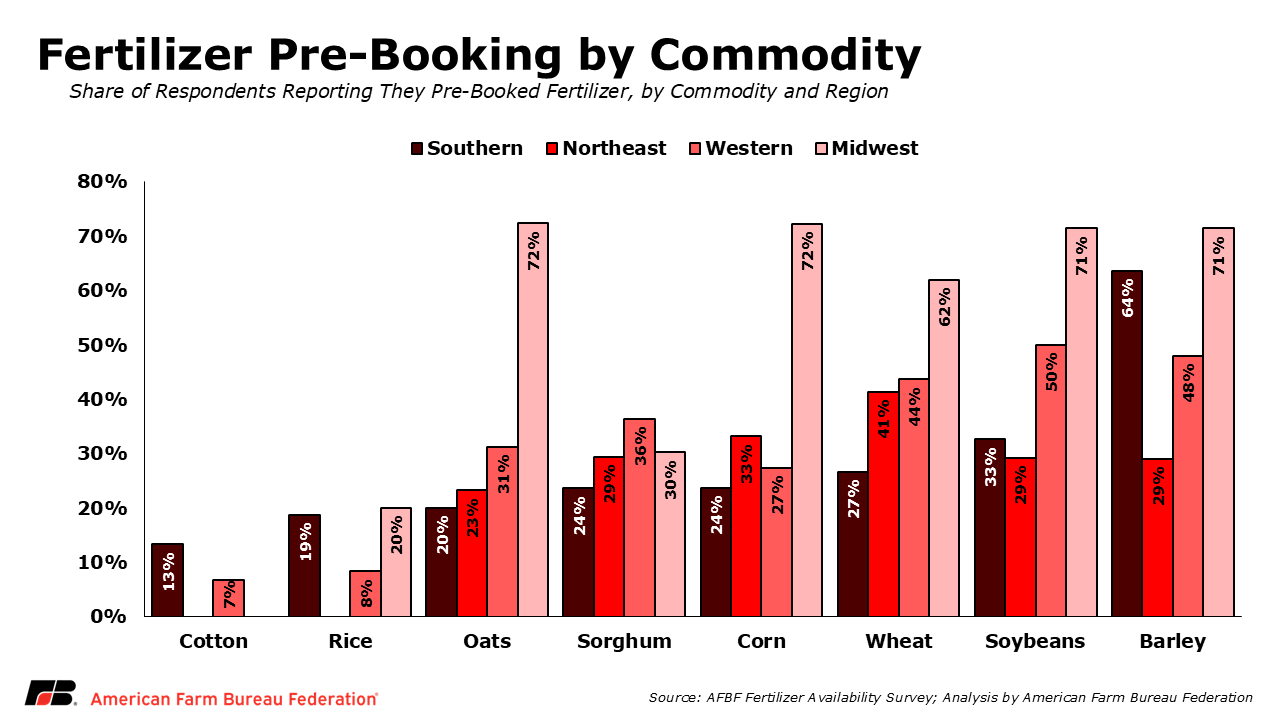

Pre-booking behavior varies significantly across commodities. Nearly half of soybean producers reported pre-booking fertilizer (49%), followed by barley (47%), corn (44%), and wheat (42%) growers. Lower pre-booking rates among cotton (13%) and peanuts (9%), both crops grown in the southern U.S., suggest greater farm exposure to in-season price volatility.

Affordability concerns are even more pronounced when viewed by commodity. More than 80% of rice, cotton and peanut producers reported they cannot afford all required fertilizer, highlighting the vulnerability of these production systems to input cost shocks. Over half of all commodities report not being able to afford all fertilizer needs this year.

Farm Financial Health Remains Under Pressure

According to the survey, 94% of respondents reported their financial situation has worsened or remained the same since last year, while only 6% reported improvement. Poor financial conditions going into this growing season impacted planting and purchasing decisions, and as a result, rapidly changing fertilizer and fuel market price volatility impacted farmers across the country in different ways – as confirmed by our survey.

Spring planting decisions depend heavily on access to fertilizer and diesel fuel, both of which have been impacted by geopolitical risks that have disrupted global markets. Since the escalation of tensions in the Middle East, nitrogen fertilizer prices have risen more than 30%, while combined fuel and fertilizer costs have increased roughly 20% to 40%. Urea prices have increased by 47% since the end of February, marking the largest month-to-month percentage increase in the price of urea. These increases are occurring when many producers were already facing tight margins for many consecutive years.

Fuel is a major operating expense during spring planting, affecting machinery operation, fertilizer transport and irrigation. As energy markets tightened following the closure of the Strait of Hormuz, diesel and gasoline prices increased significantly, raising costs across nearly every stage of production. Farm diesel prices have risen 46% since the end of February, marking the largest month-to-month percentage increase in diesel prices over the period.

Higher energy prices also increase the cost of producing nitrogen fertilizer, which relies heavily on natural gas as feedstock. Together, these overlapping increases in fuel and fertilizer expenses help explain why more than 90% of farmers surveyed reported that their financial conditions have worsened or remained the same since last year.

Bottom Line

Fuel and fertilizer markets are the most volatile since Russia’s invasion of Ukraine, and the duration of disruptions in the Middle East and closure of the Strait of Hormuz will ultimately determine farm production expenses in the months ahead – a variable that significantly impacts farm margins given historically low crop prices. While the United States is the world’s largest producer of oil and natural gas, fuel and fertilizer markets remain globally interconnected.

Countries exposed to instability in and around the Persian Gulf account for roughly 49% of global urea exports and about 30% of global ammonia exports. Because these products are essential for crop production, disruptions in the region can influence fertilizer availability and prices well beyond the Middle East.

Survey results suggest many farmers are already adjusting fertilizer purchases and application decisions in response to rising costs. If disruptions persist, these adjustments could affect yields, acreage decisions and overall production potential in the 2026 crop year. The first opportunity to see how farmers reacted will come with USDA’s May World Agricultural Supply and Demand Estimates (WASDE) report, followed by the June 30 Acreage report.

Domestic Food Production Security is National Security

The administration has announced plans to help ensure the safe passage of fuel shipments through key global shipping lanes. Expanding these protections to include agricultural input supplies such as fertilizer should also be a priority given their importance to food production and national security.

Given the worsening financial conditions on the farm, support is building for additional economic aid for farmers in any upcoming legislation to help offset economic hardships made more challenging by recent increases in fertilizer and fuel prices.

Top Issues

VIEW ALL