Meat Demand Sizzles as Memorial Day Nears

Bernt Nelson

Economist

Key Takeaways

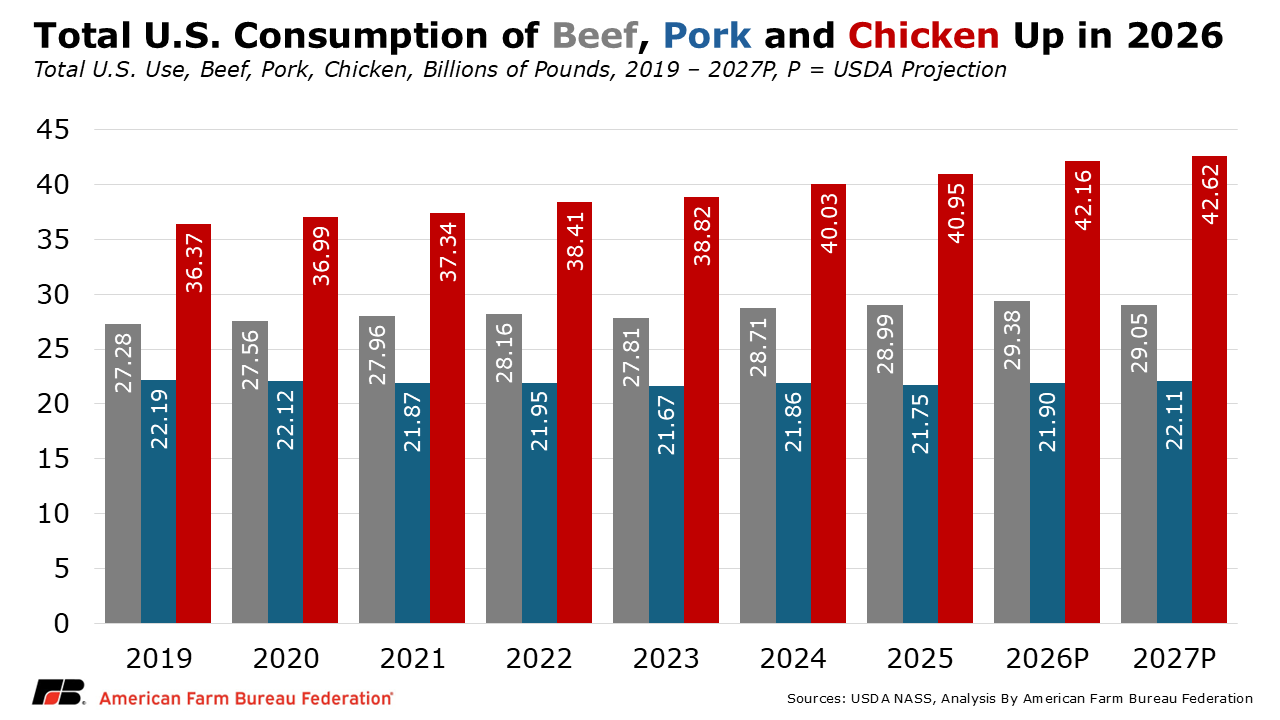

- Americans are eating more meat than ever. USDA is forecasting a rise in U.S. consumption of beef, pork and chicken in 2026 – all staples for summertime cookouts.

- Beef prices continue to set records driven by strong demand and the smallest U.S. cattle herd in 75 years – a result of years of drought and elevated operating costs that have led farmers to liquidate their herds.

- Slightly higher pork prices reflect a balanced supply of hogs and growing consumer demand. Despite disease challenges, hog farmers are producing more with a smaller breeding herd.

- Chicken continues to be the most affordable and abundant meat option. Growing production, and lower prices at the meat counter have kept chicken the most consumed meat in America. This is thanks to the chicken farmers who continue to exercise vigilant biosecurity measures in the fight against HPAI.

Memorial Day is a time for Americans to honor military personnel who made the ultimate sacrifice in service of the nation. It also marks the unofficial start to summer, and for all those pitmasters out there – grilling season. Home grown meat continues to be a staple for America’s families. According to Meat Institute, meat sales hit a record-high $112 billion in 2025 with more than 98% of American households purchasing meat for daily meals. U.S. consumption of three grill favorites – beef, pork and chicken – are all expected to rise in 2026. Here’s a closer look at these summertime staples and the challenges facing American farmers who work hard to put meat on your table.

Beef

According to data from USDA-Economic Research Service (ERS), the national average retail price for all-fresh beef was a record-high $9.64 per pound in April 2026, up $1.14 per pound, or about 13%, from April 2025. When it comes to beef, steaks are the king of the grill. According to data from the Federal Reserve Bank of St Louis (FRED), the national average price of all uncooked beef steaks in U.S. cities was record high at $13.02 per pound, up 17% from $11.12 per pound last year.

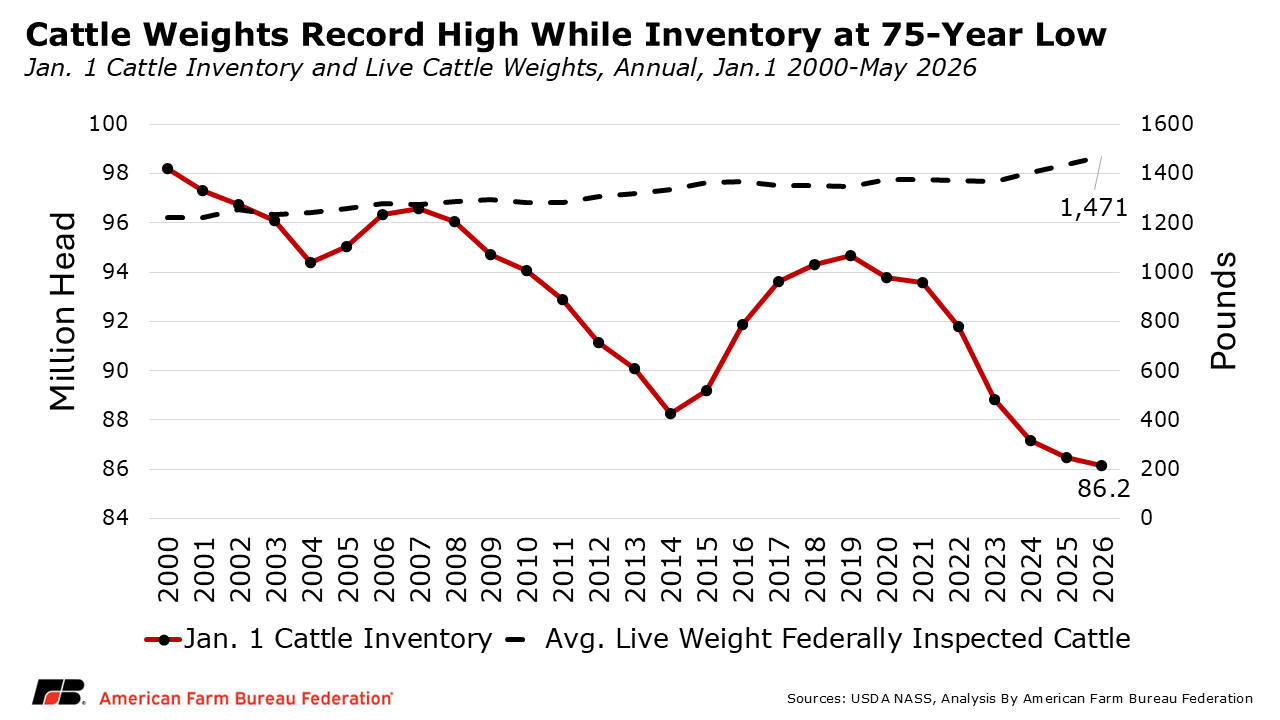

Behind these higher prices, the United States is navigating the lowest cattle supply in 75 years. This smaller supply follows years of drought and elevated operating costs that have led farmers and ranchers to liquidate their herds. Ongoing disruptions tied to New World screwworm (NWS) restrictions along the southern border have further restricted the domestic cattle supply.

On the other side of the beef price equation is demand, which is poised to climb even higher during the summer grilling months, likely pushing prices above their current record highs. This increased demand goes back to the COVID-19 shutdowns when beef quickly became the meat protein of choice for the majority of consumers who were now cooking at home. USDA’s latest World Agricultural Supply and Demand Estimates (WASDE) report estimates that 2026 total U.S. beef consumption will be 29.38 billion pounds, up 1.3%, or 390 million pounds, from 2025. This projection would be 7.7%, or about 1.8 billion pounds, more than 2019.

USDA’s WASDE reports that total 2026 beef production will be 25.55 billion pounds, down 456 million pounds, or 1.7%, from 2025. It’s important to note this is about 3.83 billion pounds, or 13%, below USDA’s projection for total U.S. beef use in 2026. This means Americans are eating more beef than U.S. farmers and ranchers can supply.

One way farmers and ranchers have helped fill the gap between supply and demand is by feeding cattle to higher weights. The average monthly live weight of all federally inspected cattle in March 2026 was a record-high 1,475 pounds. This follows the average monthly live weight rising in every month since June 2025.

Heavier cattle mean fattier beef, and more fat beef means a higher proportion of fat trimmings available for use in ground beef production. According to data from Oklahoma State University, ground beef makes up the largest portion of beef consumed in the United States, accounting for slightly less than 48% of all U.S. beef consumed in 2025. Ground beef is made from a combination of fat trimmings and lean trimmings. Due to the abundance of fat trimmings from heavier domestic cattle, and the undersupply of lean trimmings, the U.S. imports lean trimmings to balance the scale. This, along with U.S. demand exceeding the domestic supply, has led to higher beef imports over the last few years. During the first quarter of 2026 the U.S. imported 562,000 metric tons valued at nearly $4.5 billion – up 18% from the same period last year and 122% from five years ago.

For beef prices to come down, ranchers have to rebuild U.S. cattle herd or consumer demand would have to drastically cool. Looking ahead, cattle producers still face substantial uncertainty that clouds herd rebuilding decisions. Ongoing animal health threats, including NWS, along with the potential for another severe drought year, continue to raise costs and production risk despite strong underlying demand.

For this to happen, it takes about two years from the time a farmer decides to retain a heifer until she produces a calf of her own. This means if farmers begin retaining heifers now, it will be 2028 before those heifers’ calves contribute to growth in cattle supplies.

Pork

Seasonal demand for pork also peaks during the summer. However, strong seasonal hog birth rates from June to August often lead to a surplus of market-ready hogs in November and December, just in time to supply the holiday hams. This can bring lower grocery store prices, triggering an additional spike in demand.

According to the Bureau of Labor Statistics’ (BLS) most recent Consumer Price Index (CPI) report, the CPI for pork products for all urban consumers in April was 2.3% higher than a year ago. Pork chops are the most popular cut of pork. According to data from FRED, the average retail price for pork chops in U.S. cities was $4.33 per pound in April 2026, up 9 cents per pound, or 2.1%, from $4.24 last year.

U.S. demand for pork has been steady over the last decade but has increased some in the last year. According to USDA’s latest WASDE, total pork use in the United States in 2026 is estimated to be 21.9 billion pounds, up about 185 million pounds, or slightly less than 1%, from 2025. USDA is projecting U.S. pork use to increase again in 2027 to 22.11 billion pounds, up about 21 million pounds or slightly less than 1% above the 2026 projection.

One place demand is decreasing is California, where the state’s Proposition 12 has pushed average prices for pork products covered under the measure 20% higher than the rest of the country.

USDA’s latest WASDE report forecasts 2026 pork production will be 27.98 billion pounds, up 1.4% from 2025. Note that 2026 production is more than 6 billion pounds more than USDA’s projected domestic use. The United States has been a net exporter of pork since 1995 and became the world's largest pork exporter by 2005. In 2025, the United States exported over 2.94 million metric tons of pork valued at over $8.4 billion. The top markets of U.S. pork are Mexico, Japan, China/Hong Kong, Canada and South Korea.

Though markets have improved since 2023, one of hog farmers’ most challenging years hog farmers continue to face hurdles, like porcine reproductive and respiratory syndrome (PRRS) and other diseases. PRRS is a viral respiratory disease that can cause reproductive failure in sows and cause respiratory issues in growing pigs. A recent study by Iowa State University, indicated that losses from PRRS cost hog farmers about $1.2 billion annually.

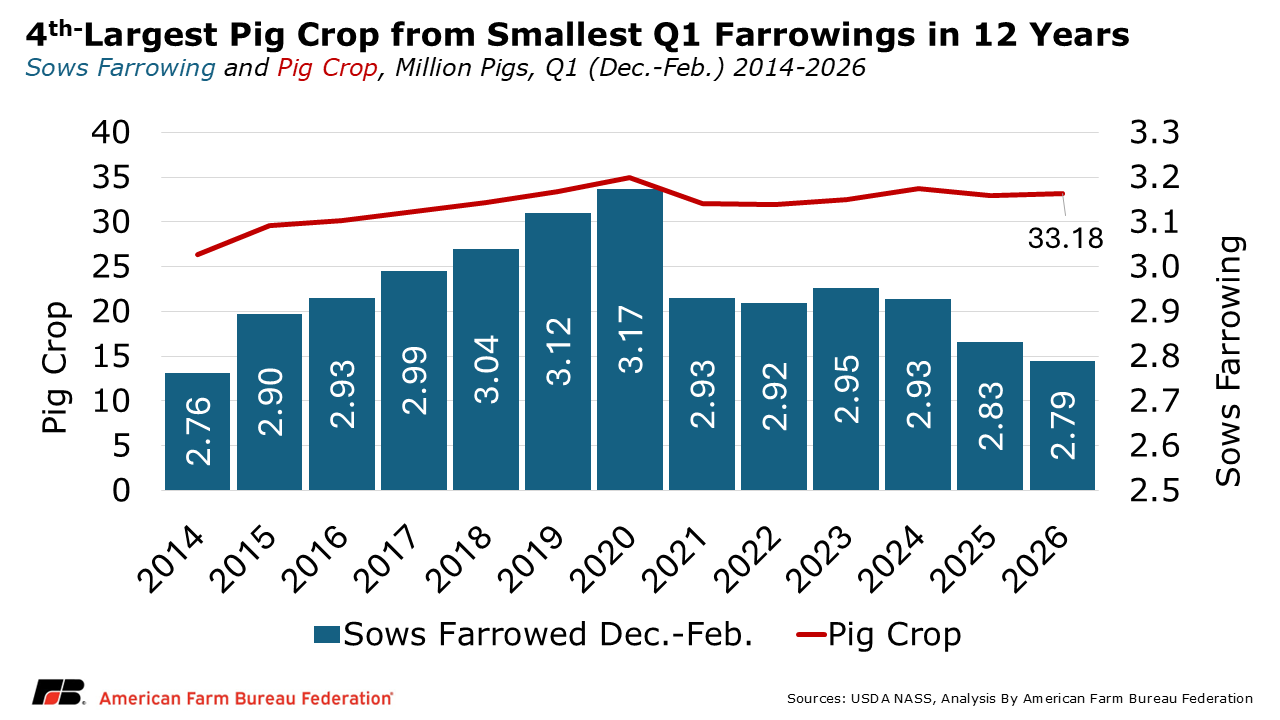

Even with these disease pressures, hog farmers have demonstrated remarkable resilience producing more pork with fewer breeding hogs. USDA’s March 2026 Quarterly Hogs and Pigs report estimated that the U.S. breeding hog herd was 5.89 million head for the first quarter of 2026, down 1.5%, or 89,000 head, from last year, and the lowest since 2014. Sows giving birth during the first quarter were 2.79 million head, representing about 47% of the breeding herd. The first quarter pig crop was 33.18 million, the fourth-highest on record. This means that 11.9 piglets were saved from every litter during the first quarter of 2026, the third-highest save rate in any quarterly report.

Chicken

Chicken is the most consumed meat in America. BLS reports the CPI for chicken for all urban consumers in April fell by 0.7% compared to 2025. This is the only product in this article that went down in price. The most popular cut of chicken in America is boneless, skinless chicken breast. According to FRED data, the average retail cost per pound for boneless skinless chicken breast in U.S. cities was about $4.17 in April 2026, down about a penny per pound from last year.

U.S. demand for chicken has risen sharply over the last decade. USDA’s latest WASDE report estimates about 42.16 billion pounds of chicken will be consumed in the U.S. in 2026, up 46 million pounds, or 1%, from 2025, and up a whopping 8.8 billion pounds, or 26%, from 10 years ago.

While summer is peak season for chicken, demand is consistently high throughout the year because it is often a lower-price alternative to more expensive proteins like beef or pork. Value-added items such as wings often help keep demand elevated throughout the year. For example, Americans consume over a billion chicken wings during Super Bowl weekend alone.

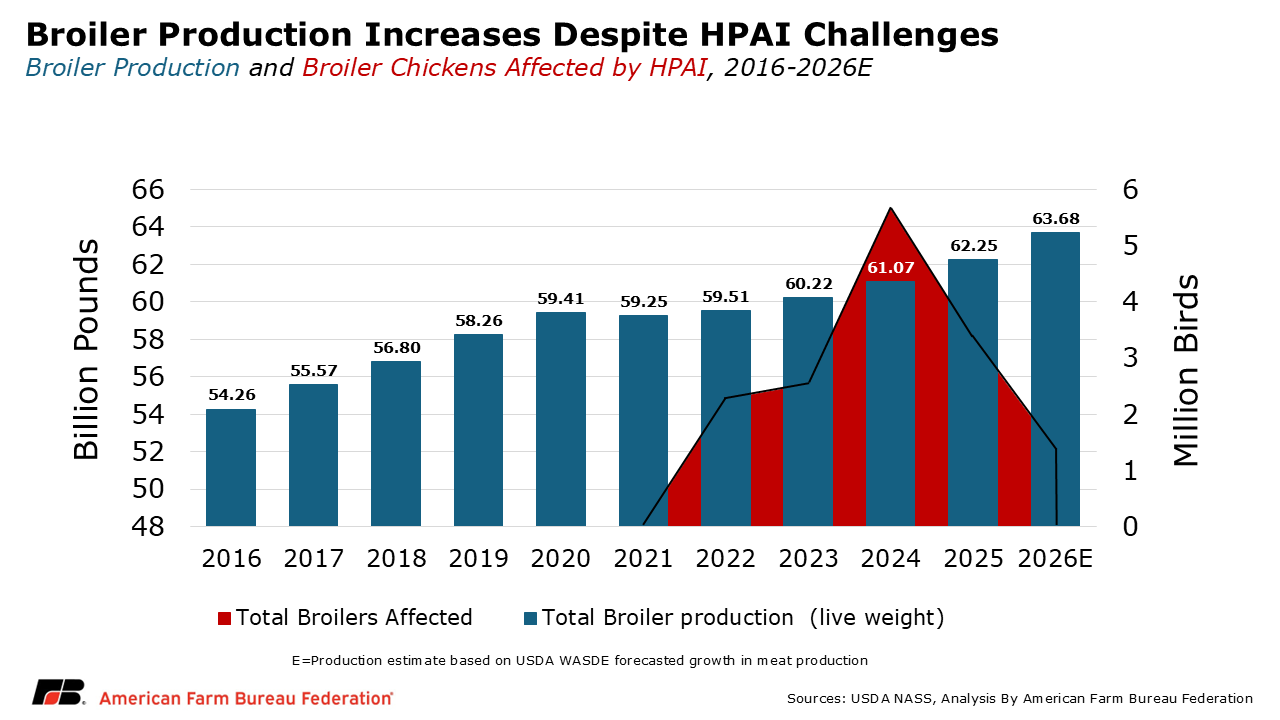

On the production side, Highly Pathogenic Avian Influenza (HPAI) has had a major impact on the entire poultry industry. While HPAI has affected millions of broiler chickens, it has had a more limited impact on broilers than other pillars of the industry such as egg-layers and turkeys. Vigilant biosecurity measures and location of major production regions have helped protect broilers from exposure to the virus, allowing rising broiler production during the outbreak.

USDA estimates that 2025 broiler production was 62.25 billion pounds (live weight), up 1.8 billion pounds, or 1.9%, from 2024. Using production data from USDA’s WASDE, a 2.3% increase in live weight would bring total broiler chicken production to 63.68 billion pounds, up over 4 billion pounds, or 7%, from 2022, when HPAI detections began. This demonstrates how determined chicken farmers are to protect their flocks.

Conclusion

As Memorial Day ushers in the summer grilling season, the meat case reflects strong demand meeting constrained and evolving supply. Beef remains the centerpiece of many cookouts, but record-high prices and historically tight cattle inventories continue to challenge both consumers and producers. Pork offers relative value and stability, supported by efficient production and strong export markets, even as producers navigate ongoing disease risks. Meanwhile, chicken stands out as the most accessible option, with steady production growth and modest prices, helping maintain its place as America’s most-consumed protein.

All three meats have one thing in common: growing demand. Despite higher costs, supply disruptions and ongoing production challenges, families trust America’s farmers and ranchers to grow the food they put on the grill and on dinner tables across the country. For farmers and ranchers, meeting that demand requires navigating drought, disease and rising production costs — factors that will shape not just this grilling season, but the years ahead.

For shoppers looking to save some money, retailers and grocery stores generally increase sales and specials as holidays draw closer. This can be a great way to save money – and for all those pitmasters to stock up their favorite cuts.

Keep an eye out for more on meat and consumer demand with American Farm Bureau Federation’s 2026 July 4th Cookout Survey, expected June 24!

Top Issues

VIEW ALL